- Open a Good Checking Account

- And a Savings Account

- Automate Savings

- Get a Credit Card

- Create and Stick To a Budget

- Don’t Be Penny Wise and Pound Foolish

- Find Extra Money

- Don’t Pay For Stuff You Can Get For Free

- Water: Get a reusable bottle and fill it up when you’re at home or see a water fountain.

- Your Credit Score: You can get a free one at Credit Karma or Transunion.

- Your Credit Report: You can get free ones.

- Dates: Well, you can pay for them sometimes, but there are plenty of free, fun date ideas.

- Saturday Nights: Same as for dates. Plenty of free fun to be had on a Saturday night.

- Books: If you like to own your books, I get it, me too. But you can read books for free with a library card. Libraries have all sorts of awesome free stuff, not just books!

- A Financial Advisor: There are some people with such complicated financial situations that it’s worth the expense of hiring a financial advisor, but they’re unnecessary and unaffordable for most people on a low income.

- Cable TV: No one needs cable TV anymore with all of the available streaming services, most of which are far cheaper. This was a tough one for me as a sports fan, but you can find a lot more live sports on streaming services now than even five years ago.

- Lunch at Work: Come on! Buying lunch costs a fortune. Pack up some leftovers. Seriously, you’ll be amazed at the savings. If you don’t like to cook, get a slow cooker. You can make cheap, tasty meals with zero cooking skills in a slow cooker.

- Mind the Creep

- Kill Credit Card Debt

- Expel Student Loan Debt

- Understand your credit score

- Get Personalized Recommendations

- Get Regular updates

- Declare Bankruptcy

- Get a Better Job

- Get More Education

- Negotiate

- Get a Side Hustle

- Build an Emergency Fund

- Invest in Retirement Accounts

- Invest in a Taxable Account

- Be Generous

- Don’t Deprive Yourself

- Educate Yourself on Personal Finance Matters

- Get Financial Friends

- It Gets Better

If you delve into personal finance books, blogs, or podcasts, it often appears that the advice targets individuals who aren’t necessarily in the top 1% but still enjoy a comfortable income and have attained a level of financial success. But what about everyone else? It raises the question: where is the financial guidance for those on a lower income?

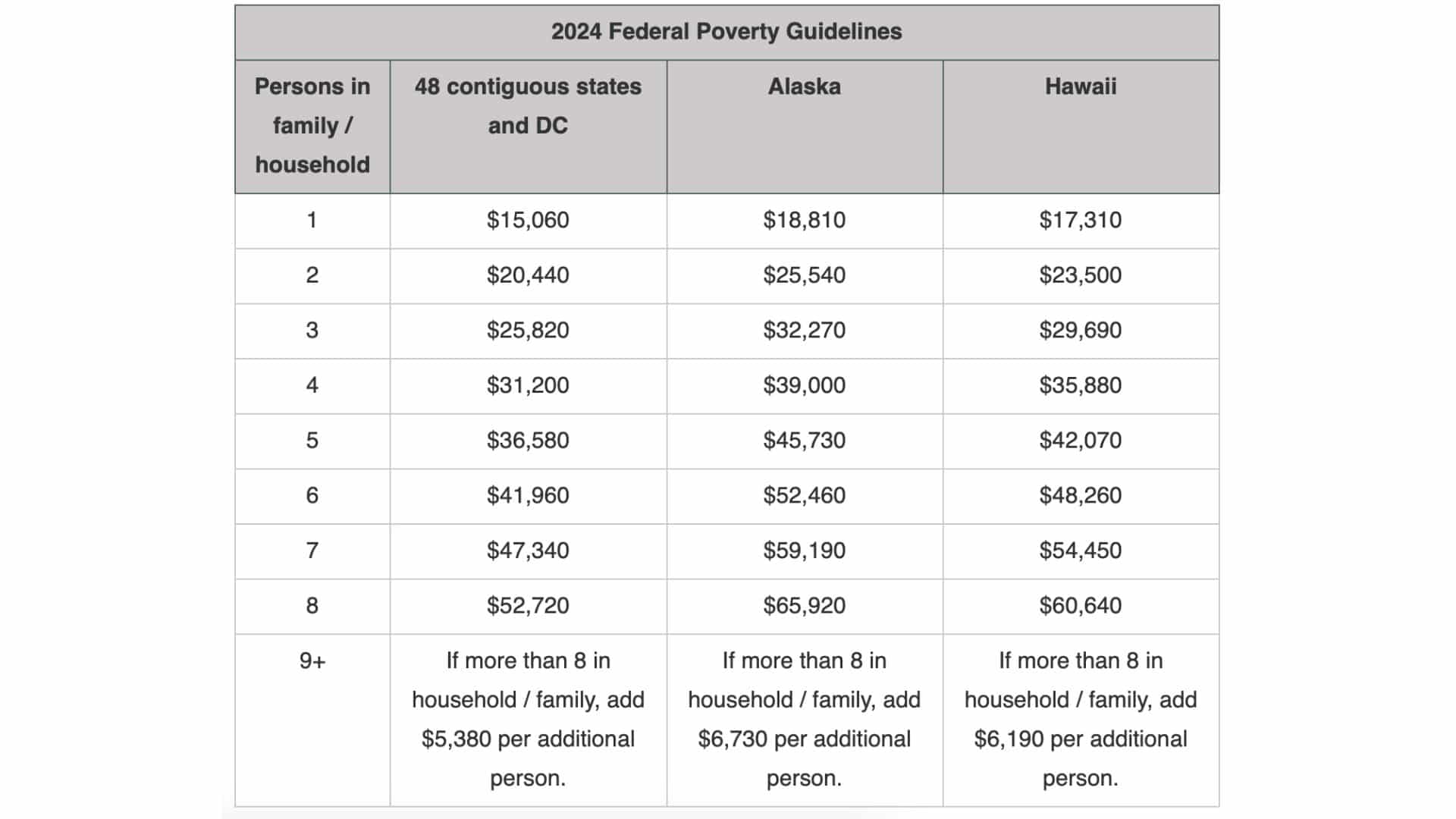

6.4 million individuals were among the “working poor” in 2021, according to the Bureau of Labor Statistics. The working poor are people who spent at least 27 weeks in the labor force ( working or looking for work) but whose incomes still fell below the poverty level.

For reference, the 2024 threshold for poverty level is $15,060 per year for a single person under 65 and $31,200 per year for a family of four.

Many factors contribute to an individual earning less than what most of us would consider a good salary. Society tends to link low wages to a lack of education, ambition, intelligence, or discipline. However, more frequently, low income stems from a scarcity of opportunities well before the job search commences. The notion of an even playing field in America simply does not exist.

Many individuals embark on a career path fully aware it may not lead to significant financial gain. Some opt for jobs they’re passionate about, considering the trade-off worthwhile.

Regardless, navigating life as a low-income earner in America presents its challenges. However, there are financial strategies available to help those earning less achieve a level of financial comfort.

Banking

Lacking a bank account can significantly complicate life, making everyday financial transactions not only more difficult but also considerably more expensive.

Not all checking accounts are made the same. Many banks impose fees for actions such as using out-of-network ATMs, overdrawing accounts, and dropping below a minimum balance requirement.

More than 25% of Americans with checking accounts are paying an average of $24 per month in banking fees, according to a 2023 Bankrate survey.

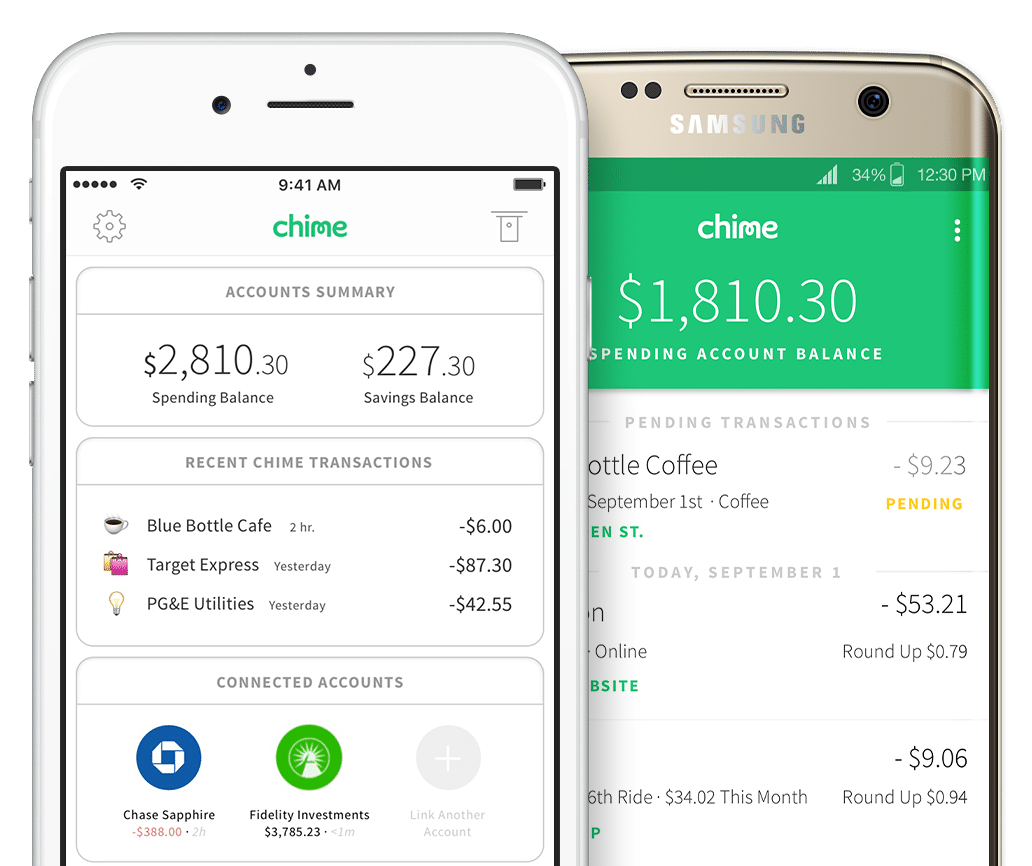

The solution to this is to find a non-traditional bank that offers free accounts. Chime is an online bank that prides itself on being a fee-free online bank, and they do not charge monthly service fees, minimum balance fees, or overdraft fees.

Upgrade also offers a free checking account called Rewards Checking Plus. This account does not have any monthly maintenance fees or overdraft fees. Additionally, it offers some attractive features like cash back and ATM fee reimbursements

Up to 2% Cash Back on common everyday expenses, recurring payments and subscriptions. Unlimited 1% cash back on all other purchases.

ATM Fee Reimbursement - Get cash from any ATM and get a credit for the fees.

According to the FDIC, 5.9 million Americans are “unbanked,” meaning they don’t have a bank account at all. In some cases, people have been blacklisted by ChexSystems and can have difficulty finding a bank that will allow them to open an account. Chime doesn’t do a credit check or ChexSystems check on customers so the unbanked may find a home there.

If you prefer to do your banking at a physical location, choose a credit union (like Consumers Credit Union) over a bank. A credit union is a not-for-profit organization that serves its members and typically has fewer fees and better interest rates than a bank.

Some financial tips are universal, and this is one of them. Open a checking account to store the money you use for your bills and a savings account for the money you’re, the clue is in the name, saving.

Saving money is easier when the money you’re meant to be saving isn’t mingling around having cocktails and flirting with the money you have for spending.

When you only have a checking account, your money is a little too accessible, a little too tempting. When the money is separated, some of that temptation is removed.

As mentioned above, Chime and Upgrade offer both checking and savings accounts, and that’s another of our essential financial tips; keep things simple. Both accounts are in one place.

We all have good intentions when it comes to saving money, but you know what they say about good intentions.

The road to hell is paved with good intentions.

Tweet ThisYou absolutely intend to put some money into savings, but at the end of the month, there’s nothing left to save. This is where automation comes in. Paying yourself first is a pillar of personal finance. Paying yourself is just as important as paying your rent or car payment. With automation, it’s easier to pay yourself first.

Set up an automatic transfer each payday. Every time you get a paycheck, a certain amount of money goes from your checking account to your savings account. That money is safe before you get a chance to spend it; out of sight, out of mind.

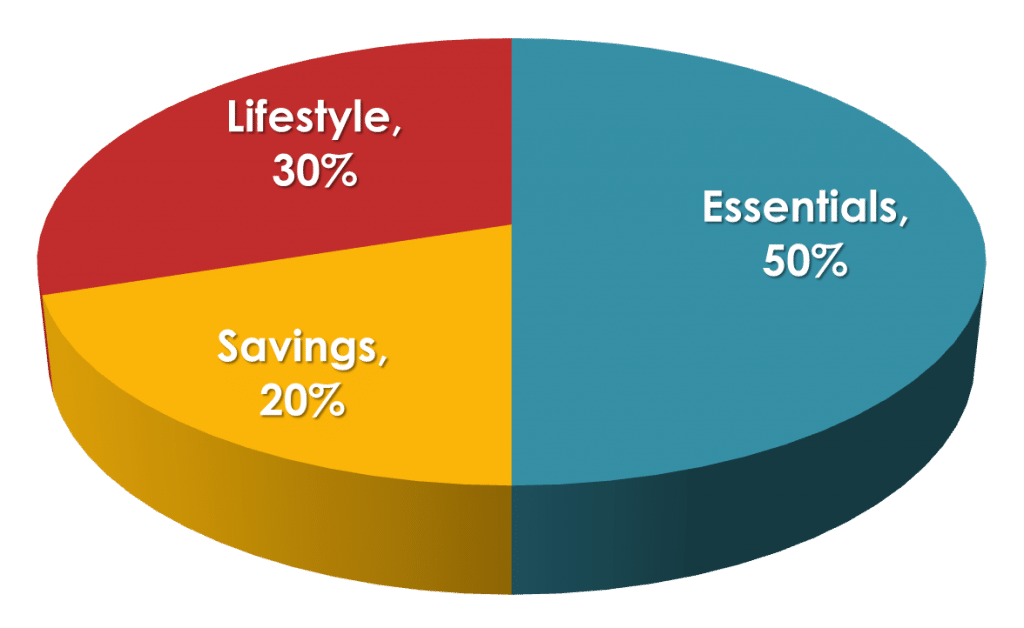

How much money? Enough that it actually has an impact but not so much that you can’t pay your bills with the money left. Ideally, according to the 50/30/20 budgeting method, you’re saving 20% of your income to your emergency fund, retirement fund, or taxable investing account.

This financial advice is non-negotiable. Your financial future depends on your ability to save.

Your credit score follows you around for life much like your Social Security number, and it’s equally important. You need a credit score, often a good credit score, to do everything from renting an apartment to buying a car. A credit card is a great way to build your credit and an excellent way to destroy it.

What does using a credit card responsibly mean? Not using it to buy things you can’t afford and paying off the full balance each month. It’s no more complicated than that. If you don’t have a ton of credit history, it can be tough to be approved for a card, but these credit cards are made for such people.

When choosing a card, look for one that doesn’t have foreign transaction fees (vital if you travel abroad or buy things online from companies outside the U.S.) or an annual fee. Some cards have annual fees, and in the right circumstances, it can be worth it, but if you’re on a low income, they probably aren’t worth it for you. Ideally, you can get a cashback rewards card which gives you a small percent back on each dollar you spend.

Spending

All of the financial tips in the world won’t help if you spend too much, this applies to both low-income and six-figure-earners. The bottom line is, that how much you spend matters more to your financial health than how much you earn.

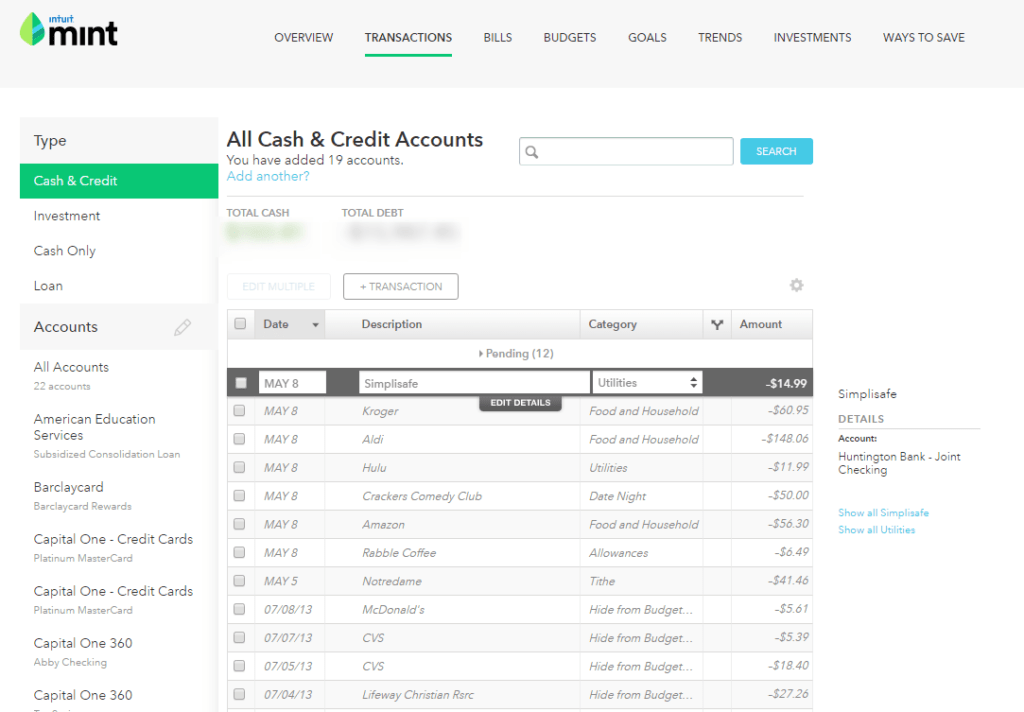

A budget is essential no matter what your income. Your budget shows you how much money is coming in, how much is going out, and most importantly, where that money is going. Create a Mint account and link all of your bank and credit card accounts.

Mint is easy and free to use. It will pull all of the transactions from those linked accounts. It will categorize them for you automatically. Mint is pretty accurate, but you may have to move some transactions to a different category.

Now go through all of the transactions and see what you can cut. Be ruthless. We all have spending leaks; Mint makes them easy to spot. Once you’ve done that, create a budget. We like the 50/30/20 method (mentioned above) because it’s simple and works no matter your income.

This is make or break. Creating and sticking to a budget is the foundation of your entire financial life and in many ways, your whole life. You’ll make mistakes but dust yourself off and try again.

Some people do crazy stuff to save money, like taking lots of condiment packages from fast food restaurants instead of buying their own. Or diligently clip coupons to save a dime on toilet paper. But they think nothing of going out to dinner three nights a week or living in a three-bedroom apartment even though they live alone.

While saving small sums on items like ketchup and toilet paper is commendable, these minor economies have a negligible effect on your overall net worth. To truly save significant money, it’s essential to minimize major living expenses.

Ideally, your housing costs should be no more than 30% of your net income. This is unrealistic in some places, but the closer you can get, the better. If you can’t stay below 30%, you’ll have to make it up in other areas.

You went through your budget and made cuts, but you can still do better. And you don’t have to do it alone. Two excellent services will help you find extra money in your budget pretty painlessly.

Cushion is like having your own financial assistant. The app will grow through your transactions, looking for recurring ones. Things like your subscriptions, music streaming service, gym, and dating site memberships. Cushion will track your bills.

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Or try Dosh to get cash back with your online purchases. Dosh gets you automatic cash back at thousands of places when you shop, dine, or book hotels. No coupons or receipt scanning.

Chime will give you a free checking and savings account, and you can find a credit card with no annual fee, but that’s only the tip of the iceberg when it comes to not paying for stuff you can get for free. Here are some things you should not be paying for:

Not the creep at the bar, but you should probably mind them too. Lifestyle creep. Lifestyle creep is:

A situation where people’s lifestyle or standard of living improves as their discretionary income rises either through an increase in income or decrease in costs. As lifestyle creep occurs, and more money is spent on lifestyle, former luxuries are now considered necessities.

You’ve cut your budget and taken other steps to save yourself some money. Don’t waste it! We’ll show you what to do with it in the Saving section.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Debt

Very few of us can say we are 100% debt-free, but when you’re not making a lot of money, debt is a terrible drain on your money and your energy. Let’s see what we can do to conquer debt.

Aside from payday loan debt or loanshark debt (the two aren’t that different), credit card debt is the worst kind of debt to be in for the same reason; the interest rate. Even a relatively low balance can spiral when you factor in an interest rate in the teens or higher.

Credit card debt is an emergency. Your priority is to pay it off like your hair is on fire.

Luckily there are ways to get out of credit card debt quickly.

Balance Transfer Credit Card: These cards have an introductory period typically ranging from 6-24 months. During that time, you’re not being charged interest. Transfer the balance from the old credit card to the balance transfer card. During the introductory period, every penny you pay goes to paying off the balance, saving you money on interest.

Personal Loan: Get a loan from a company like Upgrade or Credible and use it to pay off your credit cards. The new loan has an interest rate, but if your credit score is good enough, it will be lower than the rate on the cards.

Revolving Line of Credit: Consumers Credit Union gives users a revolving line of credit which is used to pay off credit card debt. Like a personal loan, if your credit score is good enough, the rate will be lower than your credit cards. Mint can also help you create debt tracking, goal setting, and specific debt repayment goals using the stacking method, paying off the cards with the highest interest rates first.

DIY: To qualify for all of the above options, you need a pretty good credit score. If you don’t get approved, you can still create a plan that will help you pay off your credit cards using the stacking or snowball method.

When we think of those burdened by student loans, we often think of Millenials, but the Millenials aren’t alone.

The number of people age 60 and older who still have student loan debt has sextupled since 2004 to 3.5 million, and the amount they owe is up 19-fold to $125 billion.

Do you know what happens if you’re collecting Social Security and still haven’t paid off federal student loans? The government garnishes your benefits. Student loan debt isn’t as problematic as credit card debt because the interest rates are lower, and there are programs designed to help manage it (federal student loans). But it’s still debt and certainly nothing you want to carry into your dotage.

There are companies like Credible and SoFi that specialize in refinancing student loans.

Refinancing your loans will lower your interest rate (depending on your credit score) which will save you money.

Your Credit Health:

Bankruptcy should be a last resort for dealing with debt. The process isn’t free, it’s cumbersome, and it will ruin your credit for years. And some types of debt, including student loans, will not be forgiven under bankruptcy.

That said, if you find yourself with no viable solution to manage overwhelming debt, bankruptcy may be considered as an option.

Making More Money

We all have things we have to pay for and some things we want to pay for, within reason. At some point, there isn’t anything left to cut, so we’ve got to find ways to make more money.

You don’t have to go to college to land a job that pays well. These jobs will enable you to earn a good living without going to college.

We’re not necessarily advocating going to college or going back to college, but there are plenty of ways to get additional education online.

While acquiring new skills may not always secure you a traditional 9-5 job, as some employers prioritize degrees, there’s a wealth of knowledge available online that can propel you into freelance work. Platforms such as Upwork and Guru offer opportunities to develop a side hustle that has the potential to evolve into a full-time career. By leveraging these skills, you can navigate around the conventional job market’s requirements and carve out a successful path for yourself.

Skillshare is an online learning community offering thousands of classes from design to marketing to analytics. Discover hidden passions and explore new skills taught by industry leaders. Or, become a teacher, share your expertise, and make money.

Ask your current employer for a raise. Go about it smartly. Know how much you should be making and why you deserve more. If you don’t get what you want, polish up your resume, start networking, get yourself on LinkedIn, and start looking for something else.

People who change jobs every two years make 50% more throughout their careers than those who stay longer.

Side hustles have now become a staple in the personal finance landscape, and for good reason. The flexibility to undertake many of these ventures online or according to your schedule makes it more accessible than ever to earn additional income. Consequently, there’s no reason not to explore a side hustle opportunity.

Whatever your skillset or free time, there is a side hustle for you.

Best-selling author Chris Guillebeau presents a full-color idea book featuring 100 stories of regular people launching successful side businesses that almost anyone can do.

Saving Money

Saving money is more than just stuffing cash into a savings account; that’s just the kickoff. Real saving is about piling up a safety net for the future, covering yourself for those “just in case” moments, and grabbing chances to grow your money. It’s all about setting yourself up for a comfy financial future where you can chill knowing you’ve got your bases covered.

Having an emergency fund is important for everyone but especially for those who don’t make a lot of money. It’s expensive to be poor in America, and an emergency fund is a strong barrier between you and disaster.

The ideal emergency fund contains 3 to 9 months’ worth of essential expenses, but we know that isn’t realistic when you’re not making a lot of money. So the goal is $1,000.

Remember all of those expenses we cut and the extra money we’re making? This is where it goes. Your $1,000 fund should live in your savings account where it’s easily accessible.

There are two general kinds of investment accounts; tax-advantaged and taxable. Retirement accounts are a way to minimize taxes legally. The best place to start is an employer-sponsored 401k which is usually a choice of a few mutual funds. If your employer offers matching funds, that’s free money so contribute at least enough to get the match.

If you don’t have access to a 401k, you can open an IRA yourself.

Retirement accounts are for long-term investing. With some exceptions, you can’t touch that money until you’re aged 59 1/2. That’s a good thing! It gives compound interest time to work its magic.

But you want to invest in a short-term account too. By short-term we mean the money you invest will be untouched for 5 to 10 years. You might need the money for a down payment on a home or to start a business. But the money in any investment account should be left to grow for at least five years.

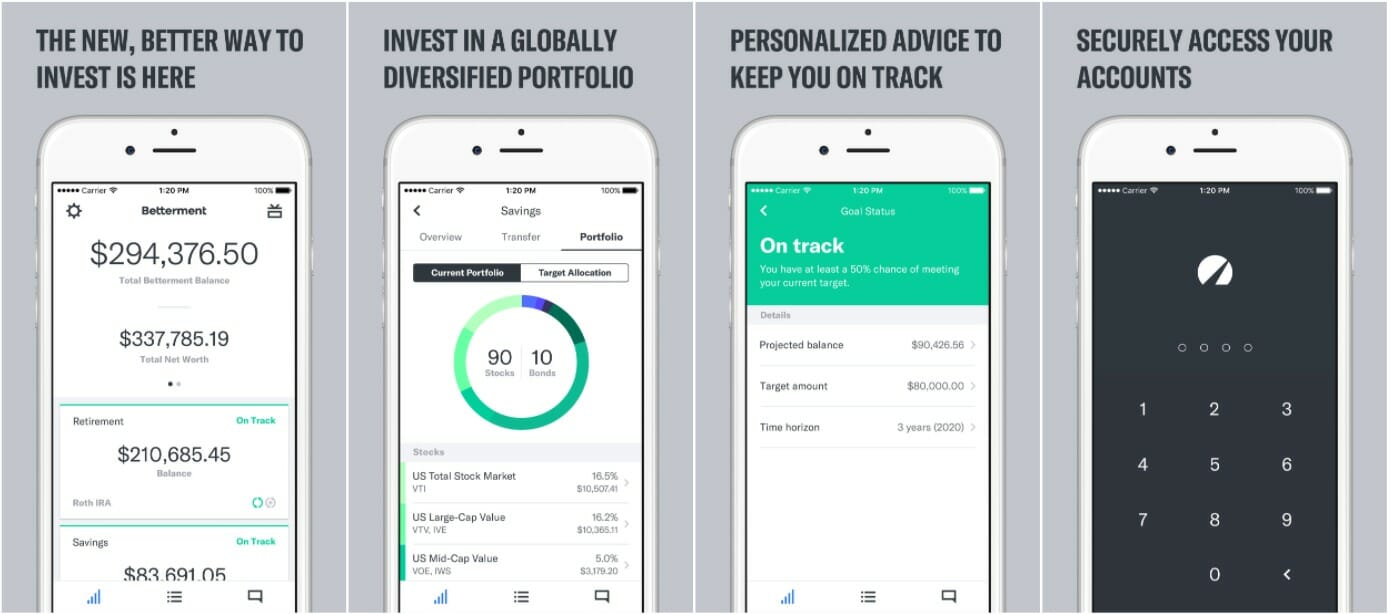

We love Betterment. There is no minimum. If you have $1, you can start investing with Betterment. And you don’t need to know anything about the stock market.

Put your money in, set your asset allocation, and you’re done.

If you’re skeptical, read this. There is no way to grow your wealth on a low income if you’re not investing, and investing regularly. This is another job for automation. Set up monthly contributions.

Financial Tips for the Rest of Us

We aren’t all destined to be rich and maybe being rich isn’t all it’s cracked up to be. Mo’ money mo’ problems after all. But that doesn’t mean we’re destined for a life of eating ramen and living in a hovel working until we drop dead.

By following these financial strategies, you can achieve a level of comfort and security envied by millions worldwide.

Bonus Financial Tips

Here are additional financial tips to help you navigate your financial journey more effectively:

If you’re passionate about certain causes but lack the funds to contribute financially, consider donating your time instead. Many charities highly value the dedication and effort of volunteers, often more than monetary donations. Writing a check is straightforward, but the real challenge lies in the hands-on work, which many are hesitant to undertake. Your time and energy can make a significant impact where it’s most needed.

You dedicate significant effort to earn your income, especially in a low-wage position, where you might work harder than those earning ten times as much. It’s completely justified for you to treat yourself occasionally.

The amount of money you make has nothing to do with whether or not you’re good with your money. Educate yourself on personal finance best practices. Honestly, everything you need to get savvy with money is on LMM, and you don’t have to spend a dime to access it.

If there’s a topic you want to learn about, use the search function on the site to find it. There is bound to be a podcast episode or article that will help. If not, email us and let us know and we will try to cover it.

The people you surround yourself with have a tremendous impact on your life, financial and otherwise.

“Show me your friends and I’ll show you your future”. successfulminded.co

Find at least one financial friend, someone who has the same financial goals that you have. They’re a great sounding board and can keep you accountable.

It’s hard to escape poverty in America. Being born or landing in poverty sets many obstacles in your path, yet improvement is within reach. It demands near-perfect choices, an unfair reality we’d change if possible.

We’re here to share the tools and financial strategies that helped us enhance our own financial standing. Remember, even when it feels like the odds are stacked against you persist in your efforts. Things will improve.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.