When you were in school, you got a report card to let your parents know how well you were doing. Well, a credit score is a financial report card to inform banks and lenders how well you’re doing.

Editor's Note

What Is the Highest Credit Score?

The highest credit score is typically 850 when measured through FICO and VantageScore. It’s a three-digit number that ranges between 300 to 850, though some systems use slightly different scoring models.

This number is used by financial institutions to decide how likely you are to responsibly pay back the money they’ve lent you, whether that is via a credit card or a home loan.

Credit Scoring Ranges:

- 300-630 is bad credit.

- 630-689 is fair.

- 690-719 is very good.

- 720-850 is excellent credit.

There are three credit bureaus who report your creditworthiness to lenders: Experian, TransUnion, and Equifax. Your score is the average number of those three.

A 300 and 850 are both unicorns. To score a 300, you would have to do everything wrong and to achieve 850, you’d have to do everything perfectly.

The better your credit score, the better the terms you can get from a lender. A good credit score can save you thousands of dollars over the life of a loan because of the higher score, the lower the interest rate you can get.

This does not apply to credit cards, where the interest rate is set in advance – though you may be able to qualify for cards with more favorable terms if you have a good score.

However, credit card interest rates are irrelevant if you’re paying off your statement balance in full every month. This is the ideal money-saving approach to take when using a credit card.

Who Has an 850 Credit Score?

Just over 1% of Americans have an 850 FICO score. Yes, it’s rare, but getting a perfect credit score is possible. If you follow the simple steps below, you can potentially land in the mythical 850 Club.

5 Reasons You Need an Excellent Credit Score

Well, it’s a magic number that let’s money lenders know that you’re an ideal person to lend money to. If you want to finance a car, buy a house, or open another credit card, the lenders will check your credit score.

If you want to make big purchases without cash (and get a low-interest rate), you’re gonna need to have a great score (751 or higher).

A good credit score can also be the difference between being able to rent an apartment and even a determining factor in whether you get a job you’ve applied for.

1. Lower Insurance Rates: Did you know that some (if not all) insurance companies run a credit check on you when you purchase insurance? It turns out that having a good credit score will save you 15% or more on car insurance — thanks, Geico!

2. Buyer Protection: When you use a credit card for your purchases, you get outstanding buyer protection, something using a debit card or cash can’t bestow.

3. Help with Renting: If you’re looking to rent a place to live, the landlord will run a credit check and might deny you housing because of a poor score. I’m a landlord, and I ran a credit check on my tenant.

4. Lower Interest Rates on Houses and Cars: Yes, the better your credit score, the lower your interest rates. It might not seem fair to everyone, but that’s the way it is, and I think the best reason to care about your credit score.

5. Employment: This one came as a shock to me, but it turns out that you could be denied a job because of your credit score. It’s an awful truth, but adds weight to the reason you need a kick-ass credit score: makes you look responsible to employers.

While you might read a bunch of articles online filled with tips on increasing your credit score, there are only three things you need to do to improve it.

In this case, big wins go a long way, and if you follow these three simple steps, you will learn how to improve your credit score over time. There is no quickie — sucks, I know.

What Makes up Your Credit Score?

So, how do financial institutions arrive at this number? First, it’s important to remember that lenders often use different scores, including scores they have developed internally – so there is no perfect way to determine what any lender will use.

A credit score is nothing more than a decision in numerical form, and because every lender makes credit decisions differently, every lender will use a slightly different score. However, a credit score is usually based on six components.

1. Payment History

This is the big one. The only way to receive an A in this category is to have 100% on-time payments.

My overall score is still a B and my score is a very solid 730 but this one category has hurt me. This is one of the categories you can’t fix. You just have to wait the seven years until the marks fall off. Pay your bills on time folks.

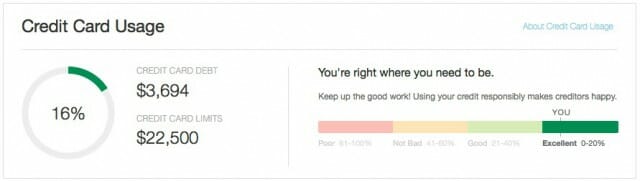

2. Credit Card Utilization

This is the percentage of the available credit you are using. Ideally, the number is less than 20%. So if you have one credit card with a $1000 limit, you want to charge no more than $200 before paying it off. I have $10,000 in credit card limits over three cards. The current total balance is 2% so I have an A in this category.

This indicator changes often and you can increase your rating here by asking your credit card companies to increase your limits. Sometimes you don’t even have to ask. After less than a year of having the Amex Starwood Preferred Card, I got a letter telling me they had raised my limit by $1000.

You can also raise your grade here by opening a new card but you will take a hit in a couple of other areas. Better to ask that your current limits be raised.

Note: Never leave a small balance on your card month to month to show a credit utilization percentage. It does not help you – pay off the full balance every month.

3. Derogatory Marks

These are things like accounts that have gone to collections, bankruptcies, and civil judgments. These take between seven and fifteen years to fall off your report and have a big impact on your overall score.

4. Length of Credit History

This is how long you’ve had credit, averaged over all of your accounts. Luckily, student loans count toward this, so if you took out loans upon graduating from high school, your ticker starts early.

A lot of people mistakenly believe that closing credit cards once they’ve been paid off is good for your score but the age of accounts and utilization are two reasons it harms your score. You don’t have to use an old card often. Perhaps put one recurring payment like a monthly gym membership to keep it open and active.

5. Total Accounts

How many accounts do you have open and are they diverse? It seems counter-intuitive but the more accounts you have, the higher your score. And the more types of accounts, the better.

I have six open accounts, three credit cards, and three student loan accounts. I have a D in this category. If I had a car loan, a personal loan, and a mortgage, the score would be a lot higher. This marker has a pretty low impact on your overall score so don’t rush out and get a loan for a car just to improve this.

6. Credit Inquiries

There are hard inquiries and soft inquiries. A hard inquiry is when someone checks your credit for things like new credit cards, a loan, or a mortgage. They stay on your report for two years. A soft inquiry is when you check your score on a site like Credit Karma and doesn’t impact your history.

This is why people who churn credit cards for rewards do what they call “App’O’Ramas.” They find cards with good sign up bonuses and apply all at once.

That way the two-year clock starts at the same time for each inquiry and because one lender may not see another lender has done a pull since they’re so close together. Overall, this doesn’t give you a big ding on your score.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

How to Get the Highest Credit Score

If you want to improve your credit score for buying a home or just beating your friend’s score, all you have to do is follow these three easy steps, let time do its thing, and you’ll succeed.

1. Get Your Score

How can you improve your score if you don’t know what it is? It’s like losing weight when you don’t know how much you weigh — how will you know if you’re making any progress?

If you have no idea what you’re credit score is, use a site like Credit Karma, or Mint to get a free, simulated score. It won’t be 100% accurate – but, then, no credit score can be 100% accurate, because credit scores vary from lender to lender. But it will be in the ballpark and a good place to start.

NOTE: Watch out for other “free credit report” sites. Some of them will ask for a credit card, and you NEVER need to pay for a simple report like this. By law, you can access a credit report once a year for free.

This is the first step. Once you find out your score, you can determine if it even needs to be improved upon. Hopefully, if your score is above 751, you won’t have to do much but continue what you’re already doing.

2. Set Up Automatic Bill Pay

This is arguably the most crucial mistake people make. If you don’t pay your bills on time, it’s going to affect your score in a very big way. I know we’re all human and not everyone is perfect, but there are ways to protect yourself against…well, yourself.

Even if you’re the best and most punctual bill payer, you never know what might happen in the future. This is why it’s a good idea to make all your bill payments automatic.

I suggest you set up automatic bill pay with your checking account to automatically pay at least the minimum payments on all your bills. By doing this, you will never miss a payment. And don’t worry if you accidentally overpay, because you can get your money back upon request.

This is the easiest way to improve your credit score. If you haven’t been good, it may take a while to improve, but once you set it up automatically, you won’t have to worry about this.

3. Increase Your Credit

The debt-to-credit ratio is the amount of available credit versus used credit. Lowering your credit utilization will increase your credit score.

For example, if you have a credit card with a $1,000 credit limit, and you spent $500 (leaving you an available balance of $500), you are using 50%.

The goal here is to keep it under 20% at all times. Also, the more credit you have, the higher your score.

The most important thing you can do here is to keep your debt low by setting your limits. Right now I have a credit card that has a $3,000 credit limit. However, I imagine that I can only spend $600 a month (and immediately pay it off).

Some credit card companies will even let you set alerts to notify you when you go over a certain amount that you set. If 20% is too low for you, you can increase the amount of credit you have available.

There are two ways to do this:

- Call your credit card company and ask to increase your credit limit.

- Open another credit card.

- As a talking head for “making things easy,” I recommend you try the first way, first. It’s an easy phone call to make, and it will improve your credit score.

If they don’t give you an increase, you might want to think about opening another credit card to give yourself more overall credit. However, do some homework before you go opening up all kinds of credit cards. I recommend having no more than three credit cards that you will use.

When searching for the perfect credit card, look for these factors:

- No annual fee

- A reward system that you will take advantage of

- An annual interest rate of 15% (the lower, the better if you’re not good at paying off your debt every month).

I called up my credit card company and asked them to increase my credit limit by $2,000, and they did. It was the easiest thing in the world. I even recorded the conversation and turned it into a YouTube video so you can see how I did it.

Of course, I edited out the four questions they asked because they were personal, but they only asked what my annual income was, if I owned or rented my place, what my social security number was, and when I was born.

Do Something Right Now To Improve Your Score

Great, you finished the article, and now it’s time to take action. I know it seems simple, and truthfully, it is. You don’t need to fret over the little things. If you take action on these three steps and give it some time, your credit score will improve drastically.

So I want you to do these things, and check them off as you go:

- Open an account with CreditKarma.com and write down your credit score in a place you’ll always see it.

- Set up an automatic bill pay on all your loans and credit cards with your checking account (minimum balance only).

- Do whatever it takes to pay down your debt.

- Call your credit card companies and ask for a credit increase (and ask for a lower interest rate while you’re on the phone).

- If you can’t get a limit increase, look for another credit card you like and open an account.

Wait six months to one full year before checking your credit score again. You don’t want to drive yourself mad checking your score every day. Nothing is going to change overnight, but if you follow these steps, your score will improve, and you’ll be patting yourself on the back in no time.

If you apply for a new credit card, whether you’re accepted or not, you’ll receive the score they used to make the decision. And some credit cards like Discover IT include your score on your monthly statement.

Happy scoring!