In the past, banking options were limited. Most people used a bank near their home or workplace, and access to a local credit union was a bonus. With fewer alternatives, banks had more control over fees, leaving customers with little choice but to accept them.

Banks charge customers for various services, including overdrafts, ATM withdrawals, and monthly maintenance fees. The average overdraft fee is about $30.82 while using an out-of-network ATM can cost around $4.55. Monthly maintenance fees average $13.95. These fees can add up quickly, making it seem unfair to pay them when banks profit by lending your money at higher interest rates.

The idea of paying banks for basic services can be frustrating, especially when they earn significant income from lending and other financial activities. By being mindful of these fees, you can explore options to minimize them and keep more of your money. For instance, finding accounts with no monthly fees or using in-network ATMs can help reduce costs.

Unless you meticulously review your bank statements, whether online or paper (which may incur a fee), you might be unaware of the various charges applied to your account. For instance, a monthly maintenance fee is a regular charge banks impose for account upkeep. Additionally, understanding overdraft protection is crucial; it covers transactions that exceed your account balance but often comes with its own set of fees.

The good news is that banking has changed, giving consumers more choices than ever. With the rise of online banks, you’re no longer stuck with traditional giants like Chase, Bank of America, Citibank, or Wells Fargo. Now, you can shop around for better rates, lower fees, and more convenient banking options.

More choices mean more competition, and banks are stepping up their game to attract customers. Many now offer perks like no-fee accounts and better interest rates. But hidden fees still exist, quietly draining your wallet. Let’s break down some of the most common bank fees and how you can avoid them.

Monthly Maintenance Fees

A monthly maintenance fee is a charge some banks apply to keep your account active. It usually ranges from $5 to $25 per month. This fee isn’t the same as a minimum balance requirement, but if your account balance falls below a certain amount, you might be charged. However, many banks will waive this fee if you meet certain conditions, like keeping a minimum balance or setting up regular deposits.

How to Avoid It

To avoid monthly bank fees, look for no-fee accounts from online banks or credit unions. Many banks waive fees if you keep a minimum balance, set up direct deposit, or use online banking instead of paper statements. Bundling checking and savings accounts or qualifying for student, senior, or military discounts can also help. If you’re being charged, try negotiating with your bank or switching to one with better terms.

Minimum Balance Requirements

Minimum balance requirements are the amount of money a bank requires you to keep in your account to avoid fees or earn certain benefits. If your balance drops below this amount, you could get hit with a monthly maintenance fee. Some banks check your balance daily, while others look at your average over the month.

How to Avoid It

Avoiding minimum balance fees can be challenging, especially considering that recent studies indicate a significant portion of Americans live paycheck to paycheck. For instance, a 2024 report found that 65% of consumers are in this situation.

To reduce or avoid these fees:

- Choose No-Fee Accounts: Many online banks and credit unions offer accounts without minimum balance requirements.

- Set Up Direct Deposit: Some banks waive fees if you have regular direct deposits.

- Link Accounts: Connecting your checking and savings accounts can help meet balance thresholds.

- Use Online Banking: Some banks offer fee waivers for customers who primarily bank online.

If maintaining a minimum balance isn’t realistic, these strategies can help you avoid unnecessary fees and keep more money in your pocket.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Overdraft Fees

An overdraft fee kicks in when you spend more than your checking account. This can happen if you write a check, use your debit card, or make a payment that pushes your balance into the negative.

Overdraft fees can be significant, especially when a small purchase leads to a hefty charge. Historically, these fees averaged around $35 per incident. However, recent regulatory changes have proposed capping these fees at $5, aiming to alleviate the financial strain on consumers. As of March 12, 2025, these new regulations are not yet in effect

There’s no reason to accidentally overdraft your account. With online and mobile banking, most banks let you check your balance anytime, making it easy to stay on top of your finances.

A budget helps you track your income and expenses so you always know where your money goes. Setting aside a small cushion can prevent overdrafts even if you’re living paycheck to paycheck. Keeping a little extra in your checking account beyond your monthly bills can give you a financial safety net.

How to Avoid It

To avoid overdraft fees, keep a small cushion in your account, set up low-balance alerts, and check your balance regularly with online banking. Use direct deposit to maintain a steady balance, link a savings account for backup funds, or opt out of overdraft protection to prevent spending more than you have. If you’re charged a fee, ask your bank to waive it.

If your bank doesn’t offer these alerts, you can create a Rocket Money account. Rocket Money is a budgeting app that helps you save money by canceling unwanted subscriptions and negotiating lower bills. It also sends alerts when your account balance is low, helping you avoid overdrafts and late fees. Some features are free, while others require a paid subscription.

Your bank may offer overdraft protection, which covers transactions when you have insufficient funds, typically for a fee of around $35 per incident. To use this service, you link another account, such as a savings account or credit card, to your checking account. If you overdraft, funds are transferred from the linked account to cover the transaction.

If you choose not to enroll in overdraft protection, any transactions that would overdraw your account will generally be declined, preventing overdraft fees. This approach helps avoid unexpected charges but may result in declined transactions if you don’t have sufficient funds.

ATM Withdrawal Fees

ATM fees are charges that banks or ATM operators apply when you withdraw cash from an ATM outside your bank’s network. Typically, you’ll face two fees: one from the ATM owner for using their machine and another from your own bank for going outside their network.

These fees can add up quickly, averaging $4.77 per transaction. To avoid unnecessary charges, use your bank’s ATMs or choose banks with wide ATM networks or fee reimbursement programs.

I get it—ATM fees can be really frustrating, especially when you’re hit with charges for using an out-of-network machine. While it’s ideal to stick to your bank’s ATMs to avoid these fees, that’s not always practical. To minimize these charges, consider using your bank’s ATMs or choosing banks with wide ATM networks or fee reimbursement programs.

How to Avoid It

The easiest way to dodge ATM fees is to get cash back when shopping at places like grocery stores or pharmacies. If you do end up with a fee, try asking your bank to waive it—sometimes, simply asking does the trick.

- Get cash back during debit purchases at supermarkets or drug stores.

- Call your bank and politely request a fee waiver if charged.

- Choose a bank that doesn’t charge ATM fees or reimburses them.

We’ll share some fee-friendly banks later in the article.

Wire Transfer Fee

Wire transfers are handy when you need to quickly move money, like funding a brokerage account or making a big purchase. However, banks usually charge fees for this service. Typical fees range from $25 to $30 for outgoing domestic wire transfers and about $15 for incoming wires.

Wire transfers are not a big part of most people’s banking behavior, but you may face a situation where you need to get money somewhere fast.

How to Avoid It

To avoid these costs, consider using free alternatives like Zelle or Venmo for domestic transfers. Expect higher fees for international transfers, averaging around $45 for outgoing wires.

Paper Statement Fees

If you prefer paper bank statements, banks often charge a monthly fee—typically between $2 and $5. Many people choose electronic statements because they’re convenient, eco-friendly, and easier to manage.

However, paper statements can still appeal to those who prefer physical records or aren’t comfortable using digital banking tools. Switching to digital statements can help you save money and simplify your financial record-keeping.

How to Avoid It

To avoid paper statement fees, look for a bank that offers paper statements at no extra cost.

Card Replacement Fee

Losing your debit card is a hassle, leaving you wondering if it’s simply misplaced or if someone is fraudulently accessing your funds. Banks typically offer free standard replacement cards, but expedited delivery can cost between $15 and $40.

Either way, call your bank immediately to report it. You’re protected by law from being held liable for unauthorized charges, but only if you report the lost or stolen card promptly.

For ATM and debit cards, your liability depends on how quickly you report the loss: $0 if before use, up to $50 within two business days, up to $500 within 60 days after receiving your statement, and unlimited if reported later.

How to Avoid It

To avoid card replacement fees, report your lost or stolen card immediately and choose standard shipping, which is usually free. If your bank charges a fee, politely ask if they can waive it, especially if you’ve been a loyal customer for several years.

If you urgently need your new card, banks offer expedited overnight shipping, typically for an extra fee. While this fee can be harder to get waived, it’s always worth asking.

Inactivity Fees

Finding a forgotten $5 bill in your coat is great, but forgetting about a bank account can be costly. If your account remains inactive for six to twelve months, many banks will charge inactivity fees, typically ranging from $5 to $25 per month.

These fees can quickly drain smaller balances, potentially causing overdrafts and triggering additional insufficient fund fees. To avoid inactivity fees, regularly check all your accounts and keep them active with occasional transactions or automatic payments.

How to Avoid It

Nearly all banks are FDIC-insured, making your money safe even if your bank goes under. Keeping money spread across multiple banks isn’t usually necessary unless you exceed the FDIC coverage limit of $250,000 per account. To avoid inactivity fees on old accounts, transfer the money out and close accounts you no longer use.

The FDIC insures checking, savings, money market, and CD accounts up to $250,000 per depositor, per bank. Coverage extends separately to account types such as single, joint, and retirement accounts, allowing you to exceed the $250,000 limit at a single bank by using multiple account categories.

There’s an Easier Way

Tired of hidden fees eating into your money? Online banks offer a hassle-free experience with fewer or no fees and better interest rates than traditional banks. They’re a great option for maximizing savings while avoiding unnecessary charges.

We’ve rounded up top online banks that provide competitive interest rates and full-service banking—without nickel-and-diming you. If you want a smarter, more rewarding way to bank, online options are worth considering.

Aspiration Bank

Aspiration Bank is more than just an online bank—it’s a financial platform focused on sustainability and ethical investing. It offers a Spend & Save account, combining checking and savings features, with the potential to earn up to 3.00% APY depending on your plan and spending habits. Aspiration uses a “Pay What Is Fair” model for its basic plan, allowing customers to choose their monthly fee—even if it’s $0. They also offer a premium Aspiration Plus plan for added benefits.

With fee-free ATM access at over 55,000 Allpoint ATMs, you can withdraw cash easily, though out-of-network ATMs may incur fees. For those interested in socially responsible investing, Aspiration offers fossil-fuel-free investment options and supports environmental initiatives.

If you want a banking option that aligns with your values while offering competitive savings and flexible fees, Aspiration could be a great fit.

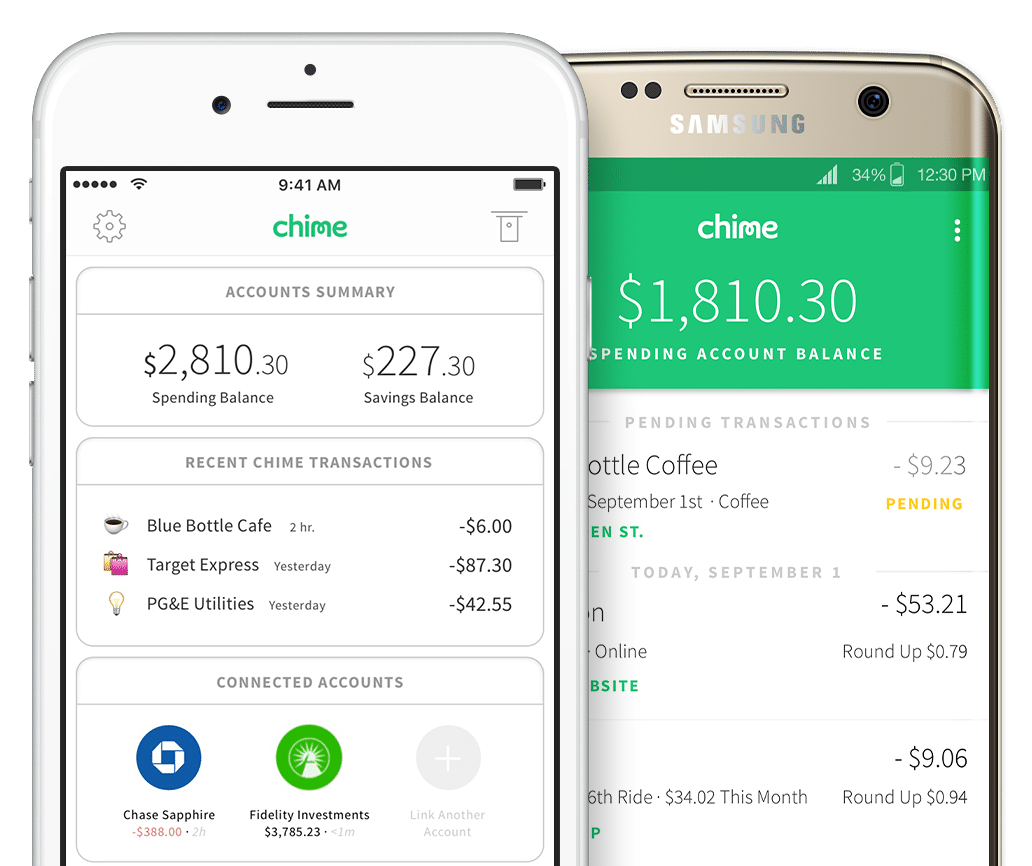

Chime

Chime is a mobile banking app and debit card service offering a fee-free checking experience with no monthly maintenance fees, minimum balance requirements, or international transaction fees. You can get paid up to two days early via direct deposit.

Chime helps you save with automated features like rounding up transactions and transferring a percentage of direct deposits over $500 to savings, supporting the principle of paying yourself first.

Chime provides access to over 60,000 fee-free ATMs, though out-of-network withdrawals incur a $2.50 fee. As a fintech company, Chime partners with FDIC-insured banks to protect deposits up to $250,000.

Chime offers a range of unique perks and features designed for hassle-free banking. Check out our full review to explore everything it has to offer.

It’s Your Money!

These days there are so many banks competing for your business there’s no reason to stay with one that nickel-and-dimes you with fees.

Banking is necessary; banks are not.

Tweet ThisTake your business and money to a bank that values its customers and doesn’t drown you in fees.