A 401k is a retirement investment account. It’s the first foray into investing for many of us and is an important part of your overall portfolio. We’ll break down how much to contribute to your 401k retirement account based on your age.

A 401k is What Now?

A 401(k) is an employer-sponsored retirement savings vehicle that allows you to invest part of your paycheck, pre-tax, into a retirement investment account where it grows tax-deferred until you are ready to start withdrawing from it after age 59 1/2.

Most 401(k) plans consist of mutual funds with a mix of stocks, bonds, and money market investments. This diversified strategy balances risk and growth potential, catering to various risk tolerances and retirement goals.

Money is taken directly from your paycheck before it reaches your checking account, ensuring consistent savings. This automatic process is a key component of successful investing, as it promotes disciplined and regular contributions to your retirement fund.

A key to any retirement plan is to save consistently. Determine a percentage of your salary you will contribute each month and stick to it.

While you only have the choices your employer offers, Empower can help you set a fund allocation that works well with your other investments.

Contributing to a 401(k) also lowers your taxable income. For example, if you earn $5,000 a month and invest $1,000 into your 401(k) account, you are only taxed on the remaining $4,000. This tax-deferred saving boosts your retirement fund while reducing your current tax liability.

Do You Like Free Money?

Of course, you do. If your employer offers a 401(k) match, it’s like free money because they add to your retirement savings based on your contributions, with the match percentage depending on the employer’s plan.

Even if you have high-interest consumer debt, like credit card debt, you should invest enough to get the match because it is free money!

I believe that free money is as addictive as cocaine.

Tweet ThisIn 2024, the maximum employee contribution to a 401(k) has increased to $23,000 per year. Additionally, if you are 50 years old or older by the end of the year, you can make catch-up contributions of up to $7,500, bringing your total possible contribution to $30,500

To maximize your 401(k), aim to contribute more than the default 3%. Financial experts recommend saving at least 10% of your income to ensure sufficient retirement funds.

Each time you get a raise, increase your contribution. Raises don’t always make a big difference in our paychecks, but that boost in your 401k will make a difference over the time the money has to grow.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

You Can Take It With You

Presumably, most of us are not going to stay at one job for our entire career. On average, people change jobs 5-7 times over the course of their career.

You don’t want to have multiple 401(k) accounts scattered around. You have several options: some employers allow you to leave the account with them, you may be able to roll it over to your new employer’s plan, or you can cash it out.

Cashing out is a poor choice because you’ll face a tax hit and be penalized for early withdrawal if you’re under 59 ½.

The best course of action is to transfer the money to an IRA rollover. There is no tax penalty for this, and you have the flexibility to choose your investments.

Empower can handle this for you.

Plan for retirement with our free tools today.

- Get your Retirement Readiness Score™ in minutes.

- Run the Recession Simulator to get perspective on today’s market.

- Use Fee Analyzer™ to find hidden fees in your retirement accounts.

Bench Marks

Investing in a 401(k) is a great step, but how do you know if it’s enough? While financial goals are individual, there are some benchmarks to ensure you’re on track for a healthy 401(k).

Although this article focuses on 401(k)s, they should be just one part of your overall investment portfolio. Diversifying your investments is crucial for financial stability and growth.

We did a separate article on how much your net worth should be according to your age.

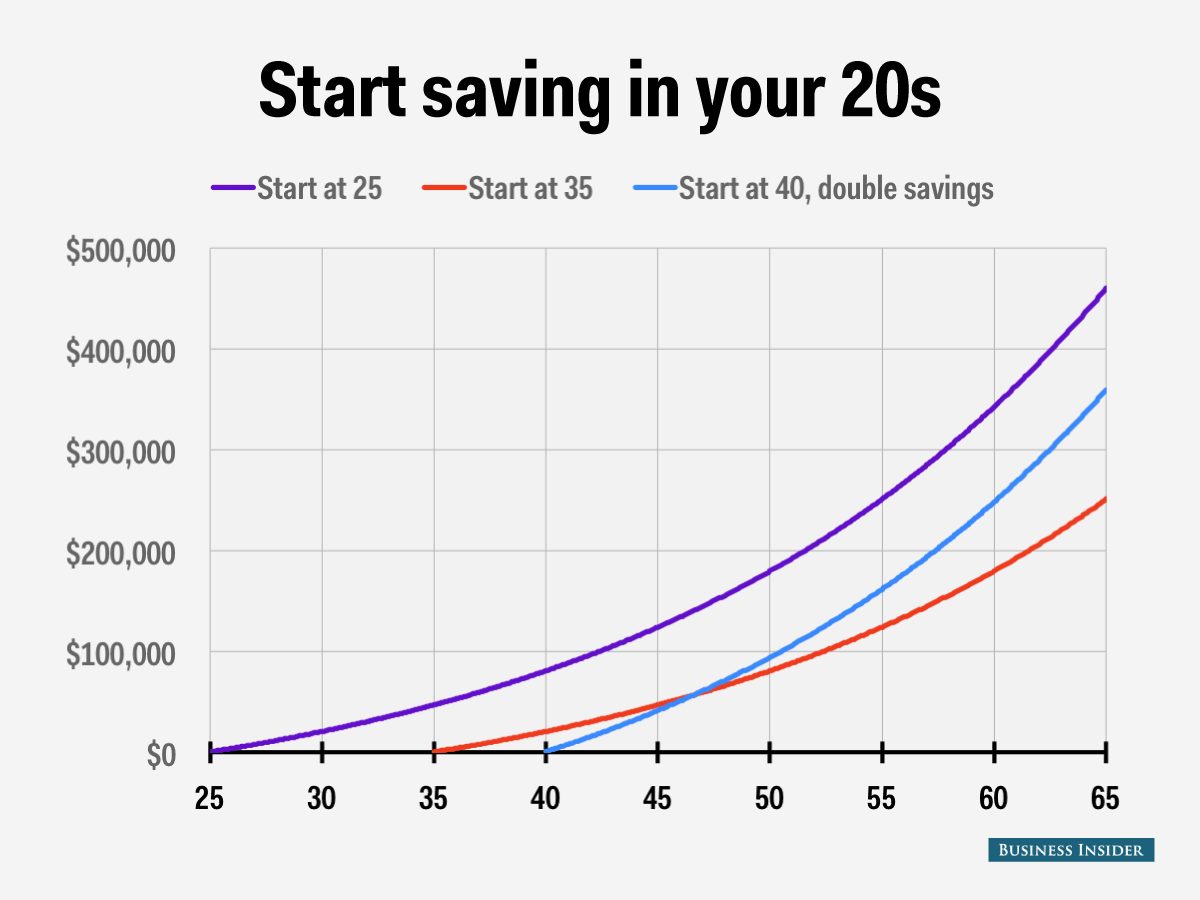

Remember, the earlier you start investing, the better.

In Your 20s

Saving for retirement in your 20s can be challenging due to lower earnings and the burden of student loans and credit card debt.

If your student loan interest is high, consider refinancing to a lower rate with a service like Credible. However, if your interest rate is already low, prioritize investing over aggressively paying down the loan, as the average market returns typically exceed loan interest rates.

Saving for retirement in your 20s can be easier because you typically have fewer financial obligations. Avoid falling victim to lifestyle inflation, which can erode your ability to save effectively. Prioritize saving and investing early to take advantage of compound interest, setting a strong foundation for your financial future.

If you make the right moves now, you will be well on the road to financial independence.

Ideally, you are saving 10% of your income for retirement. You can save that entire 10% in your 401k, or consider additional retirement investments like a Roth or Traditional IRA.

The Golden Butterfly Portfolio is a great option for people in their 20s because it spreads investments across different types of assets, which helps reduce risk and provides stability. It includes a mix of stocks for growth and bonds and gold for safety and inflation protection. This balanced approach means it performs well in various economic conditions, making it easier to stay invested and grow wealth steadily over time.

This portfolio is a modified version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

In Your 30s

Your 30s are often the best decade to save for retirement. By this time, your debt is hopefully paid off or at least manageable. You are likely earning more than you did in your 20s and may be part of a two-income household, reducing financial pressure even after starting a family or buying a home.

You aren’t panicking about paying for college, and your parents may not need financial assistance. However, these circumstances can change, so it’s crucial to save diligently during your 30s.

While it may not be realistic to max out your 401(k) at this point, aim to steadily increase your contributions each year. This consistent effort will significantly benefit your long-term financial security.

If you are earning enough to max out your 401(k), consider opening an IRA as well.

An IRA is another retirement savings account that you can contribute to once you’ve reached the 401(k) maximum for the year. Additionally, if you have or plan to have children, now is the time to start a 529 College Savings Account. This account will help you save for your children’s education expenses efficiently.

If you’re looking to buy a home, having a strong credit score is key to getting a good mortgage rate. While a score of 760 or above is fantastic, scores in the high 600s can still qualify you for competitive rates, saving you money in the long run.

Putting down 20% on a home purchase eliminates the need for private mortgage insurance (PMI). However, this can be challenging. FHA loans offer lower down payments, as low as 3.5%, but you’ll need to pay PMI until you reach 20% equity in the home.

The All Weather Portfolio is ideal for people in their 30s as it diversifies investments across various assets, balancing risk and growth. It includes stocks for growth, bonds and commodities for stability, and cash for safety. This mix helps ensure steady growth over time by protecting against market volatility and inflation, aligning well with long-term investment goals.

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

In Your 40s

In your 40s, it’s crucial to ramp up your savings efforts to ensure a comfortable retirement. By this stage, many individuals are earning their highest incomes and have a clearer picture of their retirement goals. Focus on maximizing contributions to retirement accounts like 401(k)s and IRAs.

Diversifying your investments remains key; consider a balanced mix of stocks for growth and bonds for stability. Additionally, prioritize paying off high-interest debt and building an emergency fund to safeguard against unexpected expenses. This proactive approach helps ensure financial security and a strong foundation for your retirement years.

If you need additional income, consider starting a side hustle. A side hustle can provide financial flexibility, help you pay down debt, or boost your savings. Popular options include freelance work, online tutoring, ride-sharing, or selling products online. This extra income stream can significantly improve your financial situation without major lifestyle changes, offering a practical solution to meet financial goals and unexpected expenses.

The Ivy 5 Portfolio is a solid recommendation for people in their 40s due to its balanced and diversified approach, which aligns well with the financial goals and risk tolerance typical of this age group. The Ivy 5 Portfolio includes equal allocations in five asset classes: U.S. stocks, international stocks, real estate, commodities, and bonds.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes.

In Your 50s

Age has its perks. If you’re 50 or older, you can increase your 401(k) contributions from $23,000 to $30,500 annually, thanks to catch-up contributions. Start doing that; you’re in the final stretch. You can also boost your IRA contributions from $6,500 to $7,500. Taking advantage of these higher contribution limits is a smart move to enhance your retirement savings as you approach retirement.

Retirement Planning

Now is the time to start thinking about what you want your retirement to look like. Consider whether you will continue to work in some capacity. Reflect on your retirement goals, lifestyle aspirations, and financial needs to plan effectively for this next chapter of your life.

Where Will You Live?

Consider whether you will live in the same area or move to a place with a lower cost of living. If you plan to stay, will you remain in your current home or downsize now that you have or will soon have an empty nest?

If you still have a mortgage, prioritize paying it off aggressively. You don’t want to retire with mortgage payments hanging over your head. Ensuring your financial stability in retirement requires careful planning and decision-making about your living arrangements and debt management.

Create a Passive Income Stream

If you have not yet created a passive income stream, now is the time to do so. Consider options like rental properties, REITs, or dividend stocks. Generating some income after retirement is crucial for maintaining financial stability and ensuring a comfortable lifestyle.

The Larry Portfolio is recommended for people in their 50s because it prioritizes risk reduction and capital preservation, which are crucial as retirement approaches. Its high allocation to fixed-income securities (70-80%) provides stability and generates steady income, while the smaller allocation to diversified equities (20-30%) offers growth potential. This balance helps protect against market volatility and ensures a more secure financial footing during the transition into retirement.

This portfolio's goal is to be both high performance and low volatility. It achieves its performance by tilting your portfolio to higher-risk stocks that are underpriced. Its low volatility is due to only holding 30% in stocks while 70% goes to bonds.

In Your 60s

By this stage, you are hopefully well-prepared for retirement. If you have delayed saving until now, you may need to continue working for as long as possible.

Before you retire, there are some final steps to take.

Social Security

Now is the time to decide when to start collecting Social Security. The longer you wait, the higher your monthly benefits will be. For example, starting at age 62 results in a reduced benefit, while waiting until age 70 can increase your benefit by up to 32%. Delaying benefits can maximize your lifetime income, providing greater financial security and peace of mind in retirement.

AARP has a calculator that can help you decide when to claim.

A Retirement Budget

Start compiling a retirement budget to understand your future financial needs, manage savings, and plan for any shortfalls. A well-structured budget ensures you maintain your desired lifestyle, manage healthcare costs, and prepare for unexpected expenses, providing peace of mind and financial stability.

Use resources like AARP’s Retirement Calculator, Fidelity’s Retirement Budget Worksheet, Empower’s Retirement Planner and Vanguard’s Retirement Planning Tools to create a comprehensive budget that supports your financial goals throughout retirement.

Plan for retirement with our free tools today.

- Get your Retirement Readiness Score™ in minutes.

- Run the Recession Simulator to get perspective on today’s market.

- Use Fee Analyzer™ to find hidden fees in your retirement accounts.

Update Your Asset Allocation

The rule of subtracting your age from 120 to determine the percentage of your portfolio that should be in stocks is widely recognized. This approach balances risk and growth, especially considering longer life expectancies and the need for sustained growth to outpace inflation. Reducing risk as you age is essential, but maintaining a higher proportion of stocks can be beneficial if you expect a long life

However, individual circumstances like risk tolerance, financial goals, and retirement savings size are crucial. Meeting with a financial advisor can help tailor a plan that fits your specific needs and risk tolerance, ensuring a balanced and effective asset allocation strategy.

The Permanent Portfolio, which allocates 25% each to stocks, bonds, gold, and cash, is a solid choice for people in their 60s due to its balance of risk and stability. This diversification helps protect against market volatility while still allowing for growth.

The inclusion of gold and cash provides a hedge against inflation and market downturns, ensuring a steady income stream during retirement. This approach can offer peace of mind and financial security as it mitigates the risk of relying too heavily on any single asset class

The Permanent Portfolio (PP) is a portfolio evenly split between stocks, bonds, gold, and cash. It’s best suited for risk-averse investors wanting to minimize losses while still receiving modest returns.

Fees

If you’re not careful, you can lose more than 25% of your investment performance to fees. Empower’s Fee Analyzer can show you how much you’re paying in fees.

If your 401(k) isn’t managed by Empower, you can still use their general investment fee calculator, but it won’t be able to access your specific 401(k) plan details. In that case, you’d need to look for a fee analyzer tool offered by your 401(k) provider or explore the online options mentioned previously.

Empower's free fee analyzer helps you understand how investment fees affect your retirement savings. It analyzes your holdings, estimates future fee impact, and suggests ways to potentially save by lowering fees in your retirement portfolio.

There are several online retirement fee analyzer tools available. These tools can help you understand the different types of fees associated with your 401k and their overall impact on your retirement savings. Some reputable providers include Fidelity, Charles Schwab, and Morningstar.

The Whole is Greater than the Sum of its Parts

Managing your 401(k) effectively is crucial for retirement. Fully funding and maintaining it ensures stability. Once set, you can diversify other investments, balancing risk and returns for a secure financial future.