I’m sure you’ll agree when I say there’s plenty of places to open an IRA account: Vanguard. Fidelity. Charles Schwab. Wealthfront. M1 Finance . Knowing the best place to put your money is another story.

Where do you begin?

Knowing what kind of investor you are is step one. What’s your money modus operandi?

Are you a DIYer or do you prefer someone else to do it for you? Investing doesn’t have to be as complicated as Wall Street lets you believe.

I’m going to show you the best IRA accounts for your retirement plan and a few things to be mindful of when opening yours – based off of knowing what kind of an investor you are. This will save you time and stress down the road.

Success carries within itself the seeds of failure, and failure the seeds of success. You can’t predict. You can prepare. – Howard Marks

Ready to take a look at the best IRA providers? Let’s get after it!

Individual Retirement Accounts: A Quick Summary

Much like an employer-sponsored 401(k) plan, an individual retirement account (IRA) is also an investment vehicle. The difference is that it’s created and handled by you – not your employer. Hence the word individual.

An IRA can help you save on taxes, but it depends on which type you choose. With a Traditional IRA, you might be able to lower your taxable income now, and you won’t pay taxes on your investment gains until you take the money out in retirement. On the other hand, a Roth IRA doesn’t give you a tax break today because you contribute with after-tax money, but your money grows tax-free, and you won’t pay taxes when you withdraw it in retirement.

For example, if you earn $60,000 and contribute $6,000 to a Traditional IRA, you may only pay taxes on $54,000. Contributions can lower your taxable income now, but you’ll pay taxes when you withdraw in retirement.

Your contributions to a Traditional IRA are usually tax-deductible, meaning you can lower your taxable income now, but you’ll pay taxes when you withdraw the money in retirement.

- Contribution limits: $7,000 annually ($8,000 if 50+ as of 2024).

- Deductibility depends on income and workplace retirement plan coverage.

- Withdrawals are taxed, with required distributions starting at age 73.

That’s a Traditional IRA in a nutshell. Now let’s figure out where you should open yours.

Vanguard

Vanguard is a leading and well-respected investment company globally, managing approximately $10.1 trillion in assets as of September 30, 2024. The firm serves over 50 million investors across more than 160 countries. Vanguard is renowned for its low-cost funds, offering investors affordable options for portfolio diversification.

Vanguard provides two straightforward options for managing investments within an IRA, catering to both hands-off and hands-on investors. Whether you prefer a simple approach or want to customize your portfolio, Vanguard has you covered:

- Target-Date Funds: These all-in-one funds automatically adjust their asset allocation based on your expected retirement date. They are perfect for investors looking for a set-it-and-forget-it strategy.

- Build-Your-Own Portfolio: Choose from a wide selection of stock funds, bond funds, and ETFs to create a customized investment mix. This option gives you the flexibility to tailor your investments to your financial goals and risk tolerance.

These options make it easy for investors to find the right fit for their retirement savings, whether they value simplicity or want more control over their investment choices.

If the idea of doing it yourself isn’t your cup of tea, gain access to their personal advisory services (*) for a low management fee of .3% (**). Your advisor will help you build a custom portfolio based off of your savings and investing goals.

* $50,000 minimum account balance is required for this service.

**0.3% is considerably lower than the ~1% industry average people pay for a human advisor. This service gives robo-advisors a run for their money charging between 0.25% – .50%.

Who’s it for?:

- Long-term investors, which make opening an IRA with Vanguard ideal.

- Investors who can afford minimums. Their all-in-one target-date funds require a $1,000 minimum while many of their mutual funds require a balance of $3,000.

Who Shouldn’t Invest with Vanguard:

- Active traders: Vanguard now offers free online trading for stocks and ETFs, which is great for most investors. However, if you trade options or certain mutual funds frequently, you’ll still face some fees, like $1 per options contract. This may not work for very active traders.

- Investors wanting a mix of Vanguard and non-Vanguard funds: While Vanguard funds are fee-free to trade, buying non-Vanguard mutual funds can come with extra charges. This might not be ideal if you want access to funds from other companies.

- New or low-balance investors: Many Vanguard mutual funds require higher minimum investments, such as $1,000 for Target-Date Funds and $3,000 for most other mutual funds. This can make it harder for beginners with smaller amounts to start investing.

Pro-tip:

- You can avoid the $3,000 minimum investment required for the Total Stock Market Index Fund Admiral Shares (VTSAX) by purchasing its ETF equivalent, VTI, which you can buy for the cost of a single share (around $289 as of December 31, 2024).

- Starting with VTI is a great option, especially if your account balance is low. You can always adjust your portfolio later as your savings grow. The key is to start investing early, as time is your biggest advantage when saving for retirement.

Sidestep the minimum investment requirement and buy the ETF equivalent for the price of one share.

Tweet ThisVanguard can be a great choice for different types of investors. If you’re someone whose net worth is growing quickly and you’re ready to take advantage of Vanguard’s services, it might be a good fit.

Even if you already have a substantial net worth but are unhappy with your current broker’s high management fees (around 1%), switching to Vanguard could save you money. Vanguard is known for its low-cost options, making it appealing for anyone looking to reduce investment expenses while still having access to a wide range of investment choices.

Remember, Vanguard’s Personal Advisor Services charges a fee of about 0.25% to 0.35% for accounts with a minimum balance of $50,000, depending on the investment type. Their investment costs are approximately 82% less than the industry average!

This makes Vanguard one of the best brokers for retirement savings.

Fiscal flexibility that’s funny, free and delivered weekly.

Charles Schwab

Charles Schwab, founded in 1971, is one of the biggest brokerage firms in the U.S. Today, it manages nearly $10 trillion in assets and has about 36 million active accounts.

The best part? You don’t need a minimum amount of money to open most accounts, making it a great option for anyone starting out, even with a small budget.

What we like:

- No Maintenance Fees: Charles Schwab doesn’t charge fees to maintain your account, ensuring more of your money stays invested.

- No Account Minimums: You can open an account with any amount, making it accessible for investors at all levels.

- Helpful Retirement Planning Tools: Schwab offers a variety of tools and resources to help you plan and achieve your retirement goals.

All-in-One Funds: Schwab offers easy options like target-date funds and monthly income funds. These are great for people who don’t want to manage their investments themselves. These funds automatically adjust over time to fit your goals, so you don’t have to worry about making changes.

Build Your Own Portfolio: If you prefer more control, Schwab’s Personalized Portfolio Builder lets you pick a mix of stocks, bonds, and ETFs. You can create a custom portfolio that matches your comfort level with risk and your financial goals.

Charles Schwab continues to be a strong competitor in the investment market with low costs:

- Trading Fees: Schwab now offers $0 commission for online trades of stocks and ETFs, which means you can buy and sell without paying any fees.

- Expense Ratios: Schwab’s total stock market index fund has an expense ratio of just 0.03% and requires no minimum investment. This is slightly better than Vanguard’s similar fund, which has a 0.04% expense ratio and a $3,000 minimum to invest.

- Mutual Funds: Schwab provides access to thousands of mutual funds without transaction fees through its OneSource platform. However, some mutual funds may still have fees up to $74.95 per trade.

- Options Trading: If you’re trading options, Schwab charges $0.65 per contract, which is cheaper than Vanguard’s $1.00 per contract fee.

- Robo-Advisor Service: Schwab Intelligent Portfolios is their automated investing service that builds and manages your portfolio using low-cost ETFs. You need at least $5,000 to start, and there are no advisory fees. They also offer a premium version for $25,000 that includes personal financial advice.

- Schwab Intelligent Portfolios Premium: This upgraded version does require a minimum of $25,000 to start. It includes unlimited access to financial advisors, specifically CERTIFIED FINANCIAL PLANNER™ professionals. Fees for the Premium service are slightly different, $300 one-time planning fee and $30 per month ongoing advisory fee.

Charles Schwab is one of the best options for opening a retirement account.

- Beginner and low net-worth investors will appreciate the $0 minimums, plenty of educational tools, and low-cost mutual funds and ETFs.

- Active traders will love that there are no commissions for online trades of stocks and ETFs, especially with access to Schwab OneSource.

- High net-worth investors can also benefit from Schwab’s wide range of affordable ETFs and mutual funds, along with personalized account management services.

Overall, Schwab offers great options for all types of investors.

If you’re looking to keep your banking and investments under one roof, Schwab is a great option. They also provide banking services like checking and savings accounts.

If you’re looking for a financial advisor or certified financial planner (CFP) with Schwab, you’ll need some cash upfront.

- The basic Schwab Intelligent Portfolios service requires a minimum investment of $5,000.

- If you want the Intelligent Portfolios Premium, which includes access to a CFP, the minimum is $25,000. There’s also a one-time $300 planning fee and a $30 monthly advisory fee after your first meeting with the CFP.

- The basic service has no advisory fees, but you will still pay the costs of the ETFs in your portfolio.

The beginning investor who feels more comfortable with access to a personalized advisor may not find Charles Schwab the perfect fit.

***You do have 24/7 access to their support team. This serves as a close second until you build your account balance to a level that earns you access to a personalized CFP.

Charles Schwab charges a transaction fee of up to $74.95 for mutual funds that are not on their preferred list. This fee is one of the higher ones in the industry. If you have your heart set on a specific fund that isn’t available through Schwab’s no-transaction-fee options, you may want to consider looking elsewhere.

Minimum Investment:

$0

Management Fees:

0.25%

Promotion:

Invest free for up to 1 year

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$21 billion

Minimum Investment:

$500

Management Fees:

0.25%

Promotion:

Invest your first $5,000 free, for life

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$10 billion

Minimum Investment:

$0

Management Fees:

$0

Promotion:

Low cost investing

Tax Loss Harvesting:

No

Portfolio Rebalancing:

Yes

Assets Under Management:

$1 billion

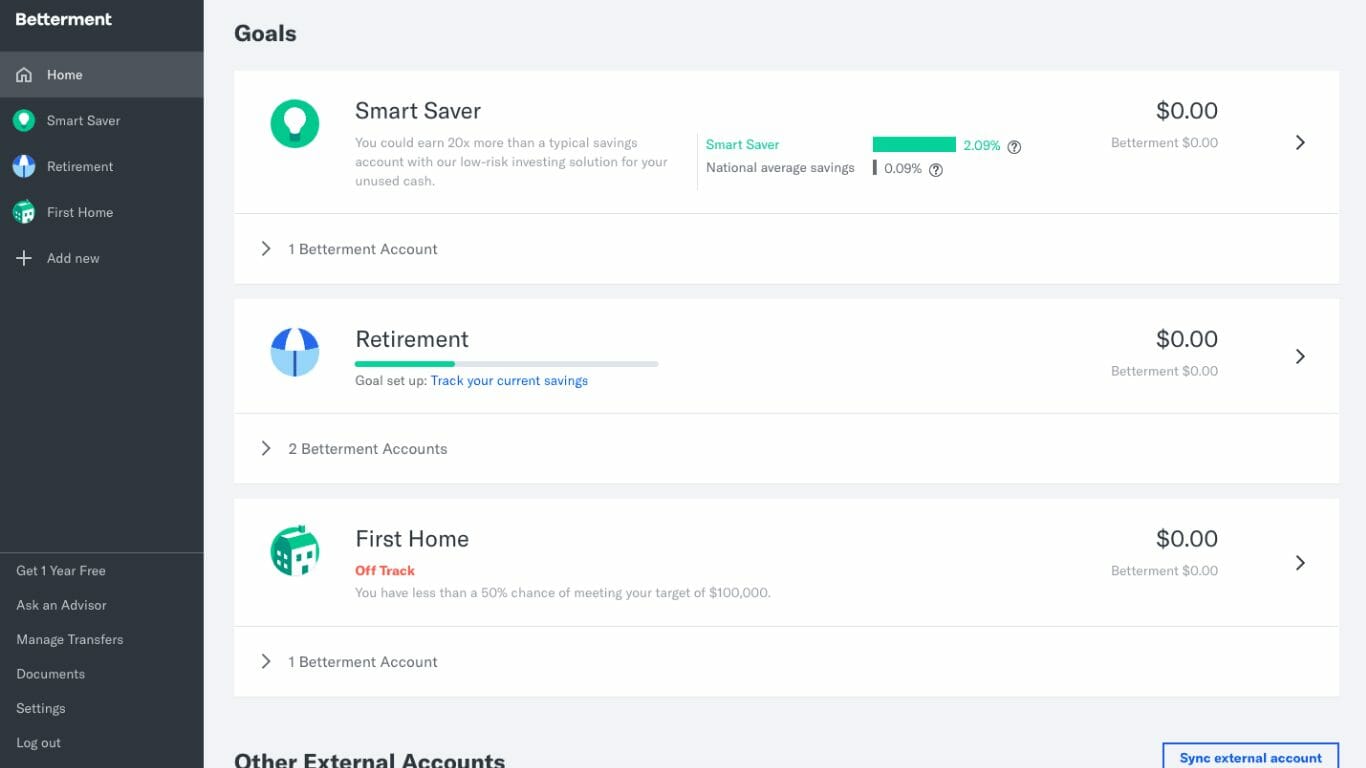

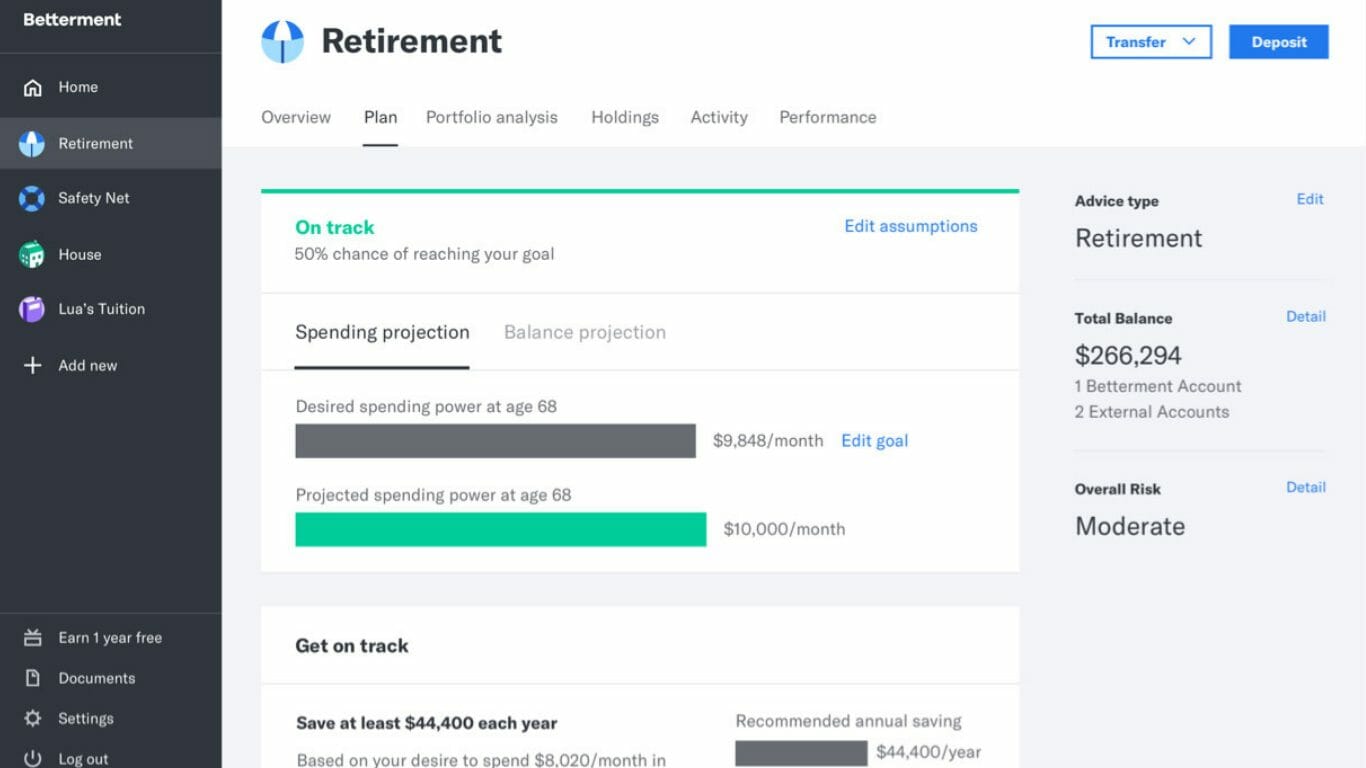

Betterment

Betterment, founded in 2008 by Jon Stein and Eli Broverman, is a leading

Betterment uses technology to simplify investing and provide personalized advice, helping clients achieve their financial goals efficiently. Its rapid growth underscores its reputation as one of the top robo-advisors in the industry.

What we like:

- No Trade or Withdrawal Fees:

Betterment does not charge transaction fees for adding or withdrawing money, making it as seamless as using a savings account. - Easy Hands-Off Investing:

Betterment handles everything, from portfolio management to tax optimization, so you don’t need to research investments or worry about daily monitoring. Ideal for beginners or those who prefer automation. - Affordable Portfolio Management: With a 0.25% annual fee for the basic plan and 0.40% for the premium plan (which includes financial advisor access),

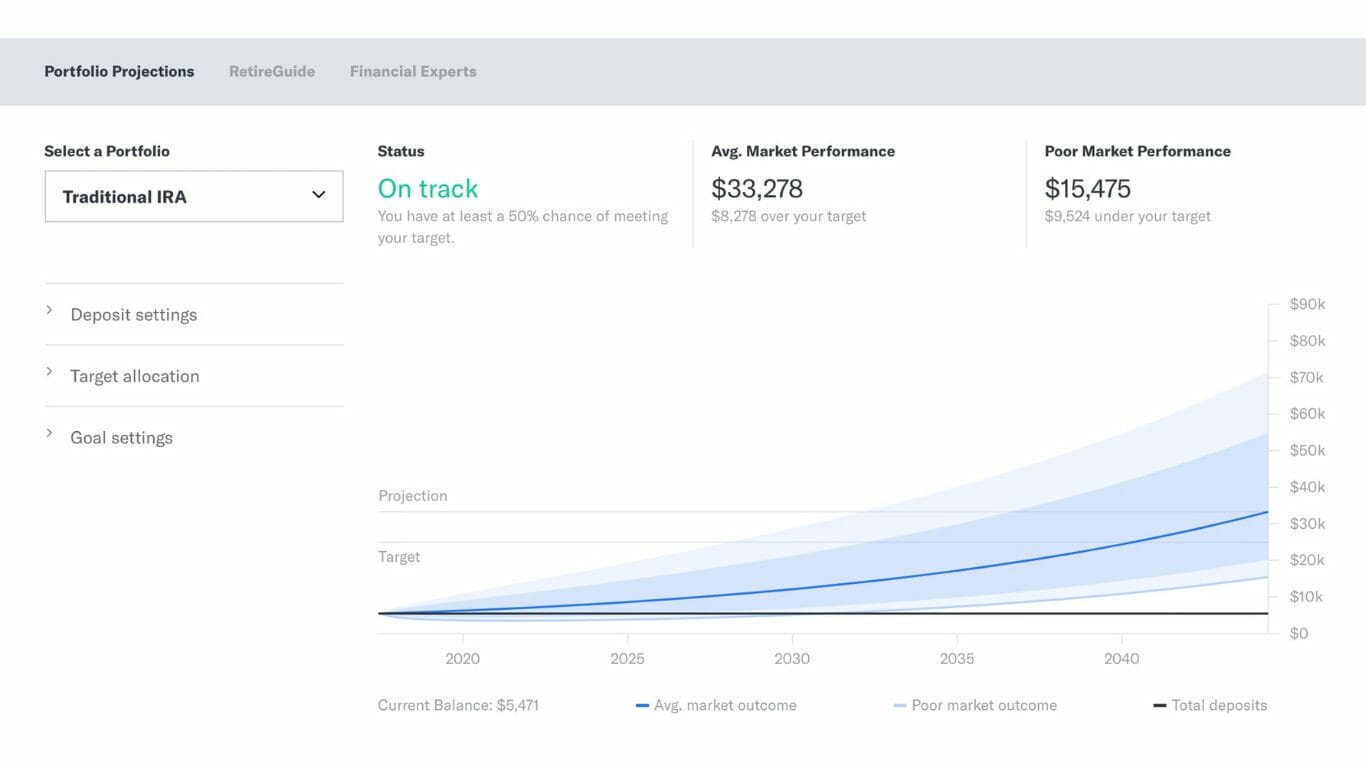

Betterment remains much cheaper than traditional advisors charging ~1%. - RetireGuide for Retirement Planning: This integrated tool evaluates your full financial picture and helps plan for retirement by setting goals and tracking progress, giving you confidence for the future.

Betterment’s Current Fee Structure

- No Account Fees: There is no fee to open an account, and accounts with a $0 balance are not charged.

- Accounts Under $20,000 Without Recurring Deposits: For accounts with balances under $20,000 and no recurring deposits, a flat fee of $4 per month applies.

- Accounts Meeting Balance or Deposit Thresholds: Accounts with balances of $20,000 or more, or those with recurring monthly deposits of at least $250, are charged an annual fee of 0.25%.

- Premium Plan:

Betterment offers a Premium plan for accounts with at least $100,000, which charges a 0.65% annual fee and provides unlimited access to certified financial planners. - High-Balance Discount: For accounts with balances over $2 million, there is a 0.10% fee discount on the portion of the balance above $2 million.

- Fee Calculation:

Betterment ‘s fees are calculated daily based on your average daily account balance and charged monthly.

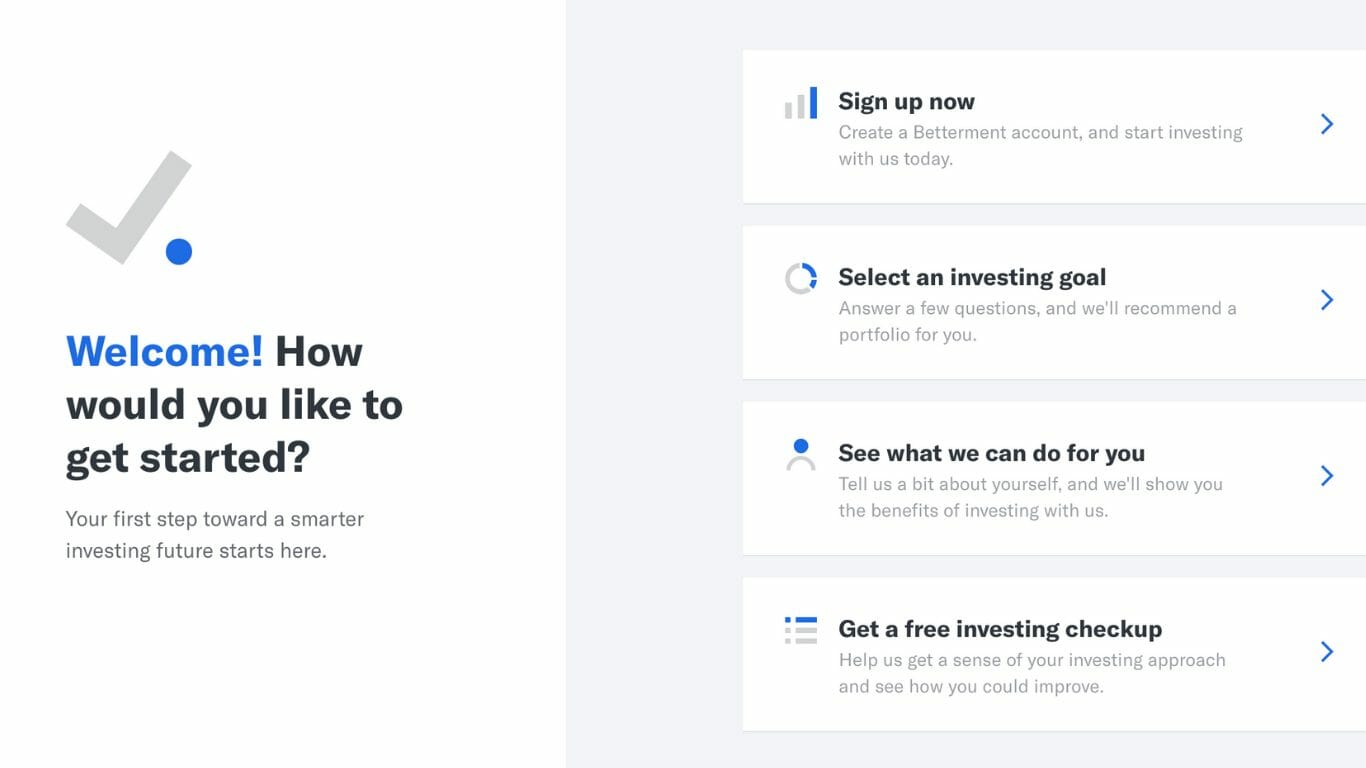

An account can be set up in under five minutes.

The first thing

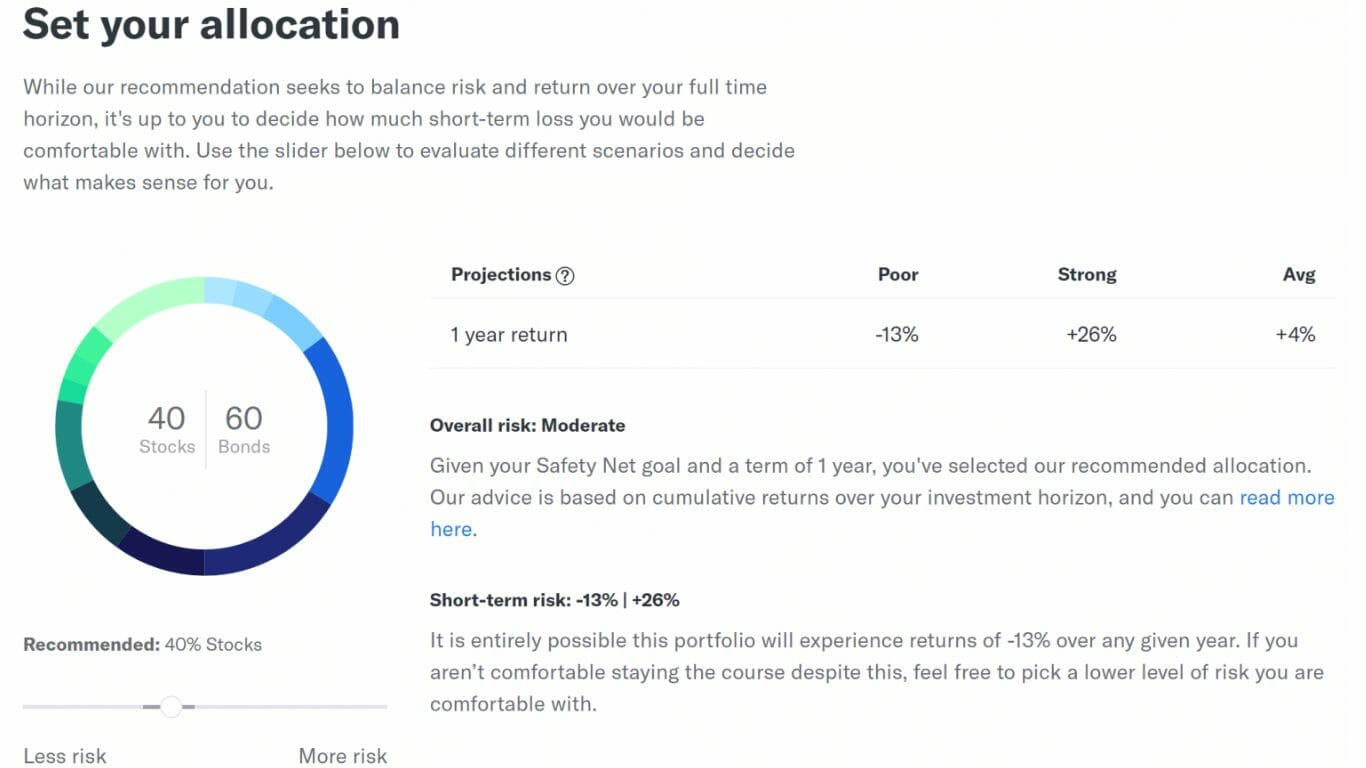

Since you’re opening an IRA, you’d answer long-term with extended withdrawals. Next, they’ll crunch the numbers based off of your time horizon, goals, and risk tolerance.

Once you’ve completed these steps,

Betterment selects your globally-diversified portfolio of ETFs from a combination of twelve asset classes.

If you require a more personal touch, you can schedule a call with

Account balances of $100,000 or higher grant you access to

Betterment’s Current Fee Structure

- Digital Plan: Charges an annual fee of 0.25% of assets under management for accounts with balances of $20,000 or more, or for those with recurring deposits of at least $250 per month.

- Premium Plan: Available for accounts with a minimum balance of $100,000, this plan charges an annual fee of 0.65% and offers unlimited access to Certified Financial Planner™ professionals.

- Fee Discount: Both plans offer a 0.10% fee discount on balances over $2 million.

Compared to Vanguard and Schwab

- Vanguard Personal Advisor Services: Requires a minimum investment of $50,000 and charges an annual advisory fee of 0.30%.

- Schwab Intelligent Portfolios: Requires a $5,000 minimum investment and charges no advisory fees; however, it maintains a higher cash allocation in portfolios, which may impact overall returns.

While

Betterment’s Tax-coordinated Portfolio Strategy (TCP) aims to optimize tax efficiency by putting assets taxed at higher rates into tax-advantaged accounts like your IRA.

Betterment’s Premium Services for High-Balance Account Holders

- Tax-Smart Withdrawal Strategies: Optimizes the tax efficiency of your withdrawals to help you keep more of your money.

- Unlimited Access to CFP® Professionals: Offers personalized financial advice tailored to your goals and needs.

- Management Fee Discount: Provides a 0.10% discount on management fees for account balances over $2 million.

These features are designed to appeal to investors with higher balances who seek comprehensive financial planning and tax-efficient strategies.

Wealthfront

If you’re not looking for human advisors and prefer a “set it and forget it” approach, Wealthfront is an excellent choice. They’re a top-tier

Wealthfront uses advanced algorithms to handle your investments, making it perfect for those who want a hands-off, automated solution. Their impressive growth highlights their position as one of the leading robo-advisors in the industr

What they offer:

- Hands-off, globally diversified portfolio of ETFs spanning across various asset classes

- No trading commissions for automated investing accounts

- Automatic rebalancing of your portfolio

- Low 0.25% management fee on assets under management

- No account opening, withdrawal, or transfer fees

Wealthfront requires a minimum investment of $500 to start investing. For accounts with at least $25,000, you can access features like a Portfolio Line of Credit. They also offer a Cash Account with competitive APY and additional financial planning tools.

You can use their free Path Tool to stay on track for retirement. Just sync your other accounts and let Wealthfront handle the rest. They’ll analyze your data and spending habits while running future projections on how much you’ll need to live on in your golden years.

Wealthfront’s paltry $500 account minimum still makes it appealing to both low-net-worth and high-net-worth investors alike. This gains you access to their suite of PassivePlus investment options.

It’s for hands-off investors who aren’t concerned with the human element.

Why Invest with Wealthfront:

- Integration with TurboTax for seamless account setup and tax data import.

- Comprehensive financial planning available through their app and online platform; no need for scheduled calls.

- Flat 0.25% annual advisory fee on all account balances.

- Low $500 minimum investment requirement.

- Ideal for hands-off investors seeking automated portfolio management without direct human interaction.

Reason not to Invest:

- It’s missing the human element as Wealthfront is entirely digital. For investors whose needs extend beyond 100% digital, a

Robo-Advisor paired with a financial advisor may be the better option.

Their Chief Investment Officer is Burton Malkiel, Professor of Economics, Emeritus, and Senior Economist at Princeton University, and author of the finance classic, A Random Walk Down Wall Street.

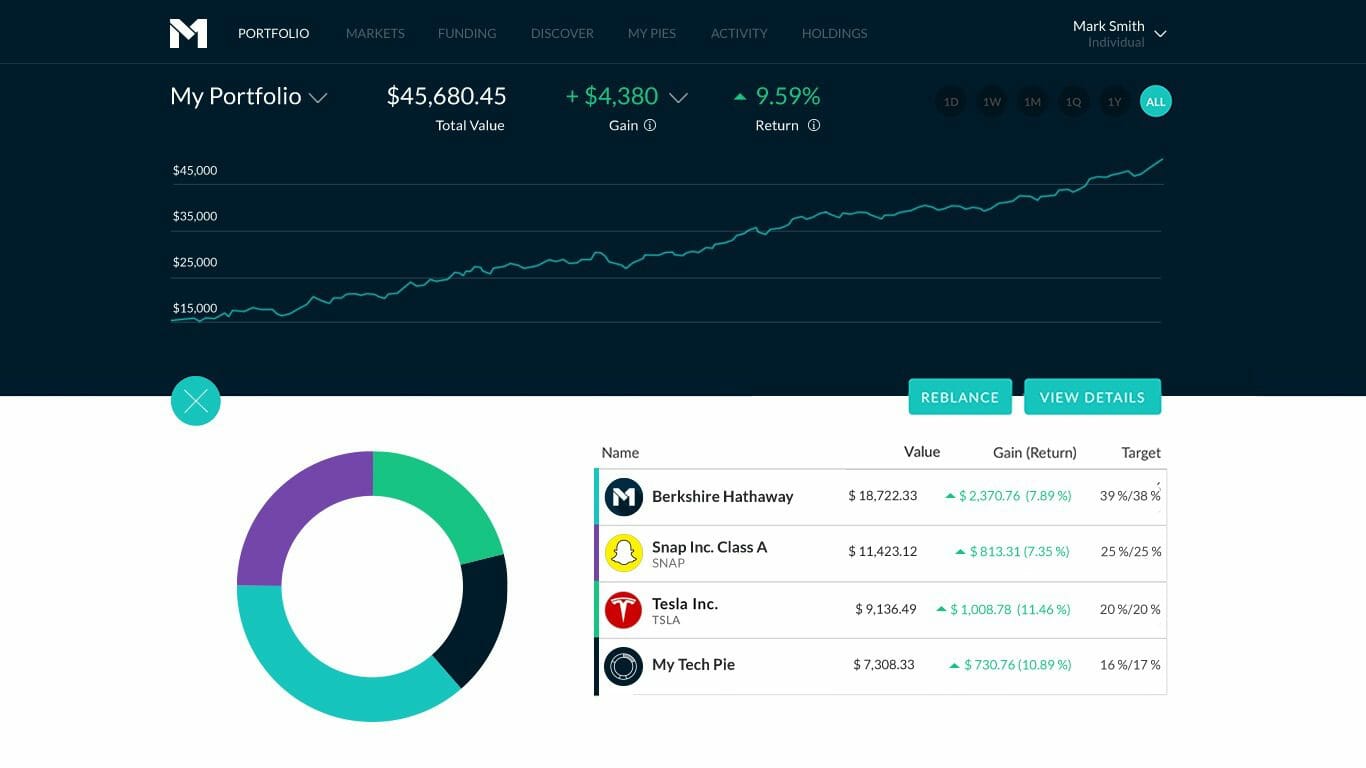

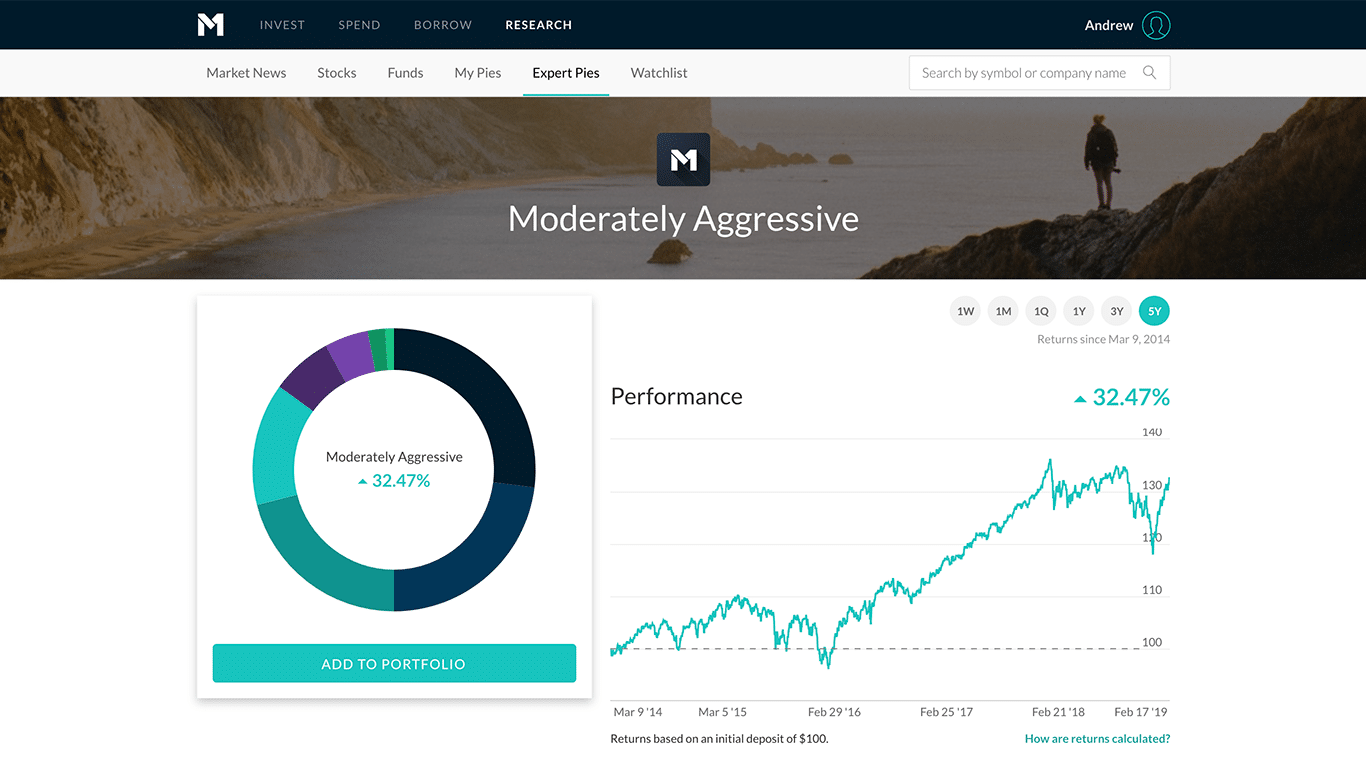

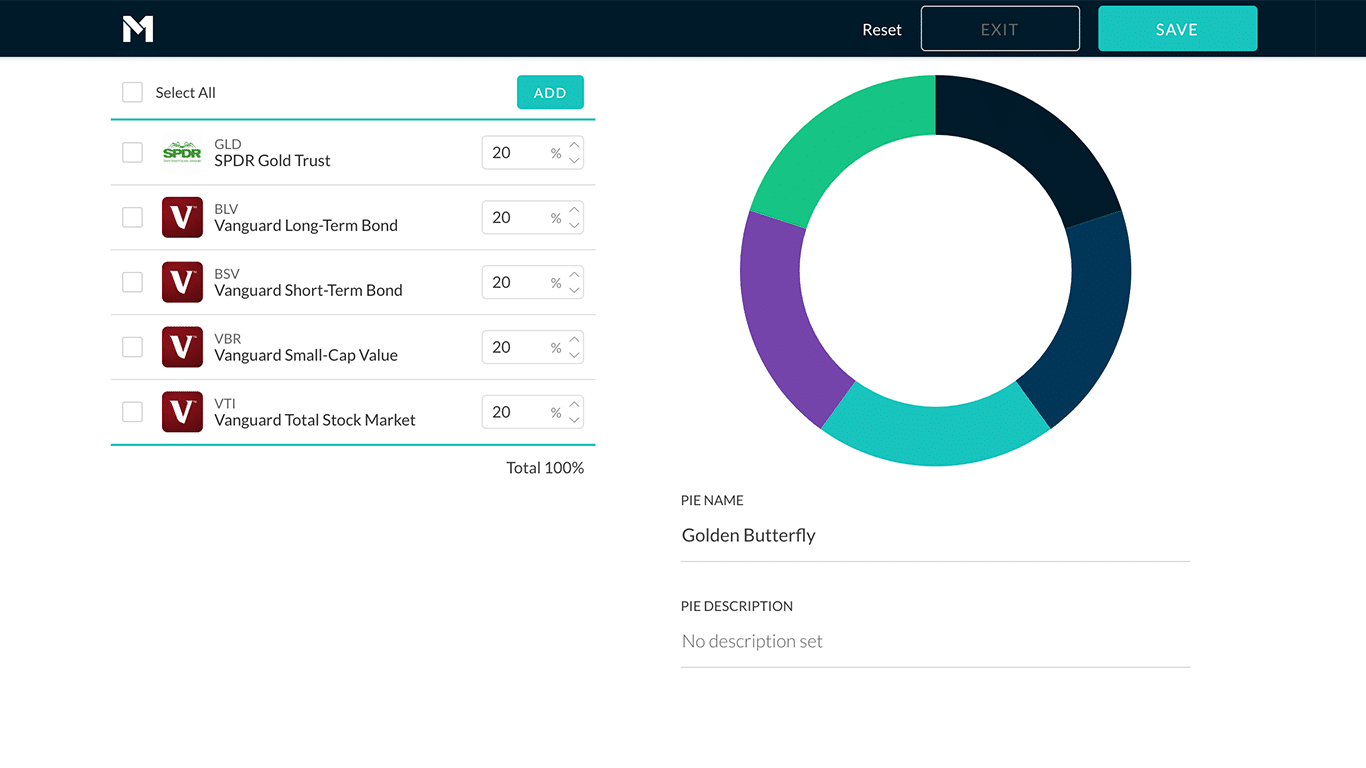

M1 Finance

Unlike traditional robo-advisors such as

M1 Finance lets you create a custom portfolio from a combination of stocks and ETFs of your choosing, incorporating a Pie Model (like you’re looking at slices of a pie graph when viewing your asset allocations).

Who’s hungry?

M1 Finance makes investing simple by offering nearly 100 pre-made portfolios called Expert Pies. You can mix these with your own Custom Pies to create a portfolio that fits your needs, whether you’re new to investing or have experience.

Their platform is easy to use, with no trading fees or commissions. They also use fractional shares, so every dollar you invest is put to work, leaving no money sitting idle. While there are no fees for basic accounts, some small charges, like regulatory or platform fees, may apply.

M1 Finance automatically adjusts your investment portfolio to keep it balanced as you add or take out money. Before you start, they ask you some questions to understand how much risk you’re comfortable with and what your investment goals are. Once everything is set up, you can set your deposits to happen automatically, so you don’t have to worry about managing your investments all the time.

M1 Finance IRA Features

- Diverse Investment Options: Choose from Expert Pies focusing on socially responsible investing, specific sectors, or hedge-fund-inspired strategies.

- IRA Minimum Balance: Requires a $500 initial deposit to open an IRA, with subsequent contributions allowed at $10 or more.

- Beginner and Hands-Off Friendly: Designed for those seeking automated investing without commission or management fees, making it ideal for investors with smaller budgets.

- No External Account Integration: M1 does not support viewing or managing external accounts like employer-sponsored 401(k) plans. However, you can transfer existing brokerage accounts or IRAs into M1.

Who’s it for:

- Passive investors

- Beginner investors

- Investors on a budget (their platform is free to use)

- Investors specifically looking for individual shares and ETFs

Reasons Not to Invest:

- Active traders may not find M1’s platform ideal for day trading.

- Investors who aren’t interested in robo-advisors.

- Investors seeking mutual funds (only stocks and ETFs are available).

Ally Invest

Ally Invest Features and Fees

- Trading Fees: Ally Invest offers commission-free trading for U.S. stocks and ETFs priced above $2. Stocks under $2 incur a $4.95 commission plus $0.01 per share. Options trades cost $0.50 per contract with no additional exercise or assignment fees.

- IRA Fees: There is no fee to open an IRA. Closing an IRA account incurs a $25 termination fee, and transferring the account to another institution costs $50. Partial transfers also have a $50 fee.

- Investment Options: Ally Invest provides access to stocks, ETFs, mutual funds, bonds, and options. Mutual funds are available but do not include no-transaction-fee (NTF) funds.

- Commission-Free ETFs: Ally Invest offers a selection of commission-free ETFs, including options from WisdomTree and iShares.

- Account Minimums: No minimum balance is required to open a trading account.

When you open an IRA with Ally Invest, you can also add savings options like their IRA High Yield CD and IRA Online Savings Account to earn more interest. The High Yield CD offers good rates and is insured, with no monthly fees. There’s no minimum deposit needed to start, making it easy for anyone to get going. Plus, Ally’s app lets you manage everything easily from your phone.

Ally offers both banking and investing services, making it easy to manage all your finances in one place. They currently provide a $100 bonus for new investing accounts with specific conditions.

For hands-off investors, Ally’s Robo Portfolios manage and rebalance investments automatically with a $100 minimum.

However, if you prefer a completely “set it and forget it” experience, other platforms may be more tailored to your needs.

Why Invest with Ally?

- Commission-free trading for U.S. stocks and ETFs, eliminating the previous $4.95 per trade fee.

- Comprehensive financial services, including banking and investment options, for managing your finances in one place.

- Robo Portfolios available with no advisory fees, ideal for hands-off investors.

Reason Not to Invest:

- Investors seeking a fully passive, “set it and forget it” approach with no interest in active trading may find Ally Invest’s platform less suitable for their needs.

Final words

If you’re still confused by what options are available to you, speak with a fiduciary, financial advisor. They’re required by law to put your interests ahead of theirs while offering you sound advice. Now, go pour yourself a bourbon and think about how much you’re going to enjoy your retirement. It’s been a hell of a day.

![M1 Finance: A Comprehensive Review [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2018/08/LMM-Cover-Images-2-768x432.jpg)