We are in an unprecedented situation. The coronavirus (or COVID-19) is going to significantly impact the world economy, just how bad things are going to be, we can only speculate. But right now, things are already dire for some of you. If you need help paying bills or other forms of financial assistance, this post has a comprehensive list of resources.

Millions of Americans are out of a job in record numbers.

A record 3.3 million people filed claims for unemployment in the US last week as the Covid-19 pandemic shut down large parts of America’s economy. The figure is the highest ever reported, beating the previous record of 695,000 claims filed the week ending 2 October 1982.

Many of you reading this may be among that 3.3 million. A stimulus plan is coming, but we don’t know when. Unemployment benefits and stimulus checks could be weeks away.

While we wait for Washington to finish wrangling, we have mortgage payments, rent payments, utility bills, phone bills, the list goes on, that we have to pay.

To say nothing of our credit card bills and student loan debt.

But if you need help paying bills, support is available. We’ve made this list as exhaustive, comprehensive, and up to date as we could.

If you know of some resources we missed, national or local, head over to the Listen Money Matters Facebook page and share.

We have also written an article that will give you some personal finance tips to get through this.

Unemployment

The coronavirus relief package, which is expected to fully pass in late March, greatly expands unemployment insurance. The first thing you should do is apply for unemployment benefits in your state if you’re eligible.

Getting unemployment may mean you don’t need help paying bills, or at least will need a lot less.

Federal Benefits

There are two main categories of government assistance benefits. Pandemic Unemployment Assistance will cover those who can’t work because of the outbreak, and that includes those in the gig economy, independent contractors, those who are ill, and those caring for an ill loved one.

The second part is an extra $600 a week for the next four months for those who have lost their jobs and are getting unemployment benefits in their state.

The $1,200 stimulus checks aren’t going to do much to help people pay their bills over the coming months, but the unemployment benefits will.

Once you’re receiving unemployment insurance in your state, you will be eligible for the $600 per week the federal emergency plan provides through July 31, 2020, on top of your state benefits.

And the $600 is across the board, it doesn’t matter how much you were making.

State Benefits

The weekly state benefits vary by state, and you can find a complete list here. Massachusettes leads with a maximum benefit of $742 per week while Mississippi is bringing up the rear with a max of $235 per week.

The number of weeks benefits are available also varies and is available on the linked chart.

Editor's Note

Note: Most states provide up to 26 weeks, but this new bill provides an additional 13 weeks.

After that, an extended benefits program could be triggered, which will give an additional 13 to 20 weeks of state unemployment benefits.

You can find your state and learn how to apply here.

Part-Time Benefits

If you worked part-time before this or your hours were cut because of it, your benefits will vary by state. Some provide unemployment benefits for part-time workers, and some don’t.

The bill provides funding to states that want to extend benefits to those who lost hours but were not laid off, but not all states will participate, and it’s up to each state to decide that.

Local Financial Assitance Programs

While there are assistance programs available through the federal government, they often involve a lot of red tape. They’re also general, meant to serve a broad range of people across a geographically diverse country.

But there are local resources that know their people, their communities, and what they need. They can also likely get help to you faster than the feds because they have less or no red tape. So start here.

And you thought it was just for funny cat pictures! No, most cities of any size and some of almost no size have their own subReddits. If your city has one, check it out.

I have seen some fantastic, generous offers from local community groups, churches, businesses, and regular Redditors on my local page.

You can also ask where you can find specific help and offer help to your fellow Redditors.

Nextdoor

Nextdoor is a message board broken down into small neighborhoods. It’s another great, hyper-local resource to find all manner of help from child care to affordable housing (many “mom and pop” landlords post their rentals here) to help wanted posts.

Like Reddit, you can offer or ask for help from your community on Nextdoor.

Facebook Groups

You probably have no idea how many different Facebook groups there are in your local area. You can find groups about homes and apartments for rent, bartering goods and services, exchanging things like clothes and toys.

Because of current events, there are more and more pages popping up to deal with the specific issues people are having.

Community Action Organizations

Google the name of your city, followed by “community action organizations.” In my area, New Orleans, there are five pages of results.

There are organizations dedicated to things, including education, housing, health, mental health, food, and more.

Family, Friends, Neighbors

Don’t overlook the people closest to you if you need help. In the past, maybe your pride kept you from asking people in your life for help, but all bets are off now, and it’s either sink or swim.

Let them help you swim.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

National Charities

United Way

The United Way is the best of both worlds. It’s a substantial charitable organization with a presence in 95% of American communities. If you’re struggling, they’re providing crucial information and services

Specialists answer requests by phone, text, chat, and email to connect people with disaster, food, housing, utility, health care resources and more.

In New Orleans for example, the United Way is providing nearly $500,000 to the Hospitality Cares Pandemic Fund which will provide grants to hospitality workers (New Orleans primary industry is hospitality so those workers have been hit especially hard).

The fund provides aid to those who are unable to afford basic financial needs during the COVID-19 outbreak. The United Way knows what the locals need! You can find your local chapter here.

Feeding America

There are 200 Feeding America Food Banks across the United States. If the organization isn’t available in your area, Feeding America will help you find one.

Feeding America distributes food and non-food items like cleaning supplies, diapers, and personal care products.

Salvation Army

The Salvation Army has chapters across the United States, and services vary by location.

Some of the services include:

- Emergency Financial Assistance

- Food & Nutrition Programs

- Emergency Shelter

- Latchkey Programs

You can find your nearest chapter here.

Housing

Housing is the most significant expense for most of us. Here are ways to get help and relief if you’re worried about covering your housing expenses.

Temporary Mortgage Assistance

The federal government, via Fannie Mae and Freddie Mac, is telling associated mortgage lenders to reduce or suspend homeowner’s mortgage payments for up to 12 months if they’ve lost income due to the Covid-19 pandemic.

Fannie and Freddie are also not charging penalties, late fees, and delinquent payments will not be reported to credit bureaus (so it won’t impact your credit score).

Editor's Note

Note: If you’re under foreclosure currently, that action will be suspended for at least 60 days.

Federal regulators expect that most private lenders and servicers will adopt the same policies soon. As of this writing, JP Morgan Chase, US Bank, Wells Fargo, and Citibank have agreed to defer mortgage payments for 90 days.

If you are unsure of your lender’s policy, call them to clarify. No matter who your lender is, do not just stop making payments.

You have to contact your lender and let them know you can’t make your payments and then follow whatever steps are required to participate in the program.

Rental Assistance

The federal stimulus package bill includes a national moratorium on some residential evictions. This is a summary of the protections.

Some cities and states are taking steps to help too. This is a list of places that have instituted eviction moratoriums.

The number of cities and states doing this continues to grow, so if your location is not listed, check your local news sources.

Rentassistance.us

This organization is a comprehensive resource for thousands of local agencies and non-profit organizations that can help those struggling with housing costs pay their rent or find more affordable housing.

You can search Rentassistance.us by state and then the city.

In Louisiana, for example, there are 33 assistance resources across 32 cities. Some resources include Catholic Charities, Hope House, and Unity of Greater New Orleans.

Utilities

There are already several government programs in place to help low-income individuals and low-income families with their utility bills. In the wake of COVID-19, there is even more help available.

Shutoff Freezes

Many states and cities are requiring that local utility companies freeze shutoffs in the wake of the pandemic.

In fact, one governor, Charlie Baker of Massachusettes, threatened utility companies that shut off gas, electric, or water services to customers during the state of emergency with $1 million fines.

Check your local policies for similar freezes. You want to know how long the freeze is in place and if there any steps you have to take, i.e., calling your providers to let them know you’ve lost your job or part of your income to be included under the policy.

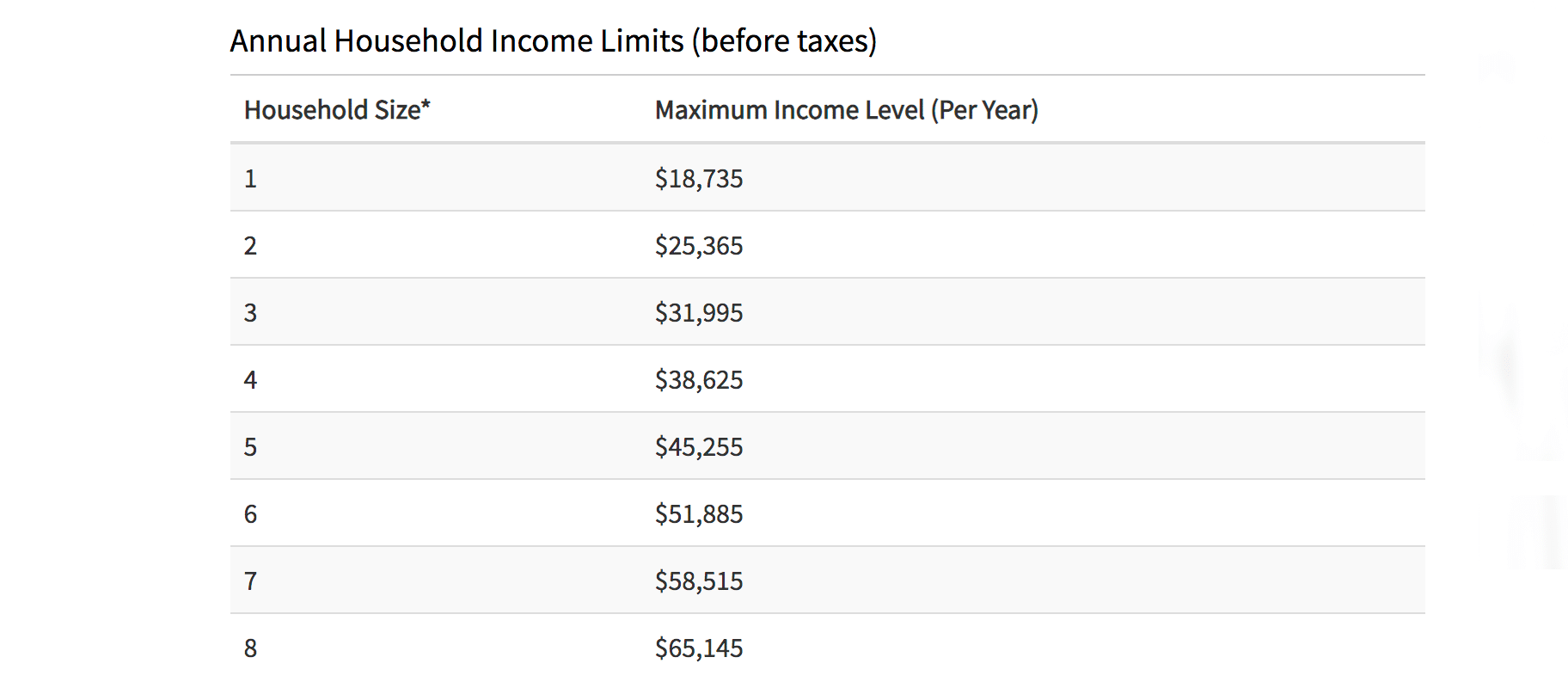

Low-Income Home Energy Assistance Program

This program, also known as LIHEAP, helps those in low-income households with their energy bills, weatherization, and energy-related home repairs.

To qualify, you must have an annual household income (before taxes) that is less than or equal to the following amounts:

You can go here to see if you meet the eligibility requirements.

Lifeline Program

This is the FCC’s (Federal Communications Commission) program created to help low-income households afford communication services.

It provides a discount for telephone and internet service when purchased from participating providers.

To apply, you can go here to the verification system.

State Programs

Many states have programs that help people pay their utility bills. Local charities and non-profits administer some, some are state-run, and some utility companies have and operate their own utility assistance programs.

You can search by state here.

Medical Help & Human Services

If your health insurance is tied to your job and you lose your job, replacing it is a must. We all know the dire state of medical care, medical costs, and the health system in this country, and the middle of a pandemic is no time to have absolutely no coverage and end up with medical bills that reach six figures.

If you do come through this with medical bills, keep in mind that for 2019 you can deduct medical expenses for the year that exceed 7.5% of your AGI, and for 2020, the threshold amount increases to 10%.

Hospitals also frequently have a patient financial services department to help with medical expenses.

Your Spouse or Partner

If your spouse or partner has health insurance, have them contact their HR department to see if you can get on their policy. Whether or not domestic partners can join a plan varies by state.

COBRA

If you lose your job, you may be legally allowed to buy into your former employer’s health insurance for up to 18 months.

This option is available for most companies that have 20 or more employees. Your former employer is obligated to notify you of this option.

COBRA is not ideal, it’s expensive, but it is an option and a perfect reason to deploy your emergency fund.

Affordable Care Act

This is the open marketplace where consumers can buy their own insurance coverage. Usually, these marketplaces are only open for enrollment during certain times or under certain circumstances.

Some states have opened their registration to deal with this crisis. If your state is not among them, you may be able to get coverage under what is known as a qualifying event, which includes losing your job.

Depending on your financial situation, you may be able to get free or subsidized coverage. You can apply here.

Medicaid

Medicaid is funded through a partnership between states and the federal government. Under the ACA, 37 states and the District of Columbia expanded Medicaid to expand coverage to more residents.

The plan is free or very low cost. There are two ways to apply for Medicaid, through your state or through the Health Insurance Marketplace.

There is no open enrollment period for Medicaid; you can apply anytime.

Children’s Health Insurance Program

The Children’s Health Insurance Program (CHIP) is administered by the U.S. Department of Health and Human Services. It provides matching funds to states for health insurance to families with children.

CHIP provides low-cost health insurance to children whose families make too much money to be eligible for Medicaid. In some states, the program covers pregnant women also.

There is no open enrollment period for CHIP; you can apply anytime. You can apply by calling 1-800-318-2596 or through HealthCare.gov.

Prescription Help

If your insurance plan doesn’t cover your prescriptions, you lose coverage, or you need help paying for your medication, there are lots of resources including government, non-profits, and from drug companies.

Hill-Burton Hospitals

This program was started in 1946, and while it ended in 1997, some 140 health care facilities across the country remain obligated to provide free or reduced-cost care.

Editor's Note

To be eligible to apply, your income must be at or below the Federal Poverty Guidelines.

Health services at a Hill-Burton facility are not automatically free or reduced-cost. You have to apply at the facility and be deemed eligible for care.

You can apply before or after you receive care and can even apply after a bill has gone to collections. Only facility costs are covered, not bills from your private doctor.

There are dozens of these facilities across the country.

Food

While, for the most part, no one in America is starving to death, food insecurity exists, and the pandemic could worsen it.

In 2018, 11.1 percent of households were food insecure at least sometime during the year., including 4.3 percent (5.6 million households) that had very low food security.

If you need help with food, there are lots of resources.

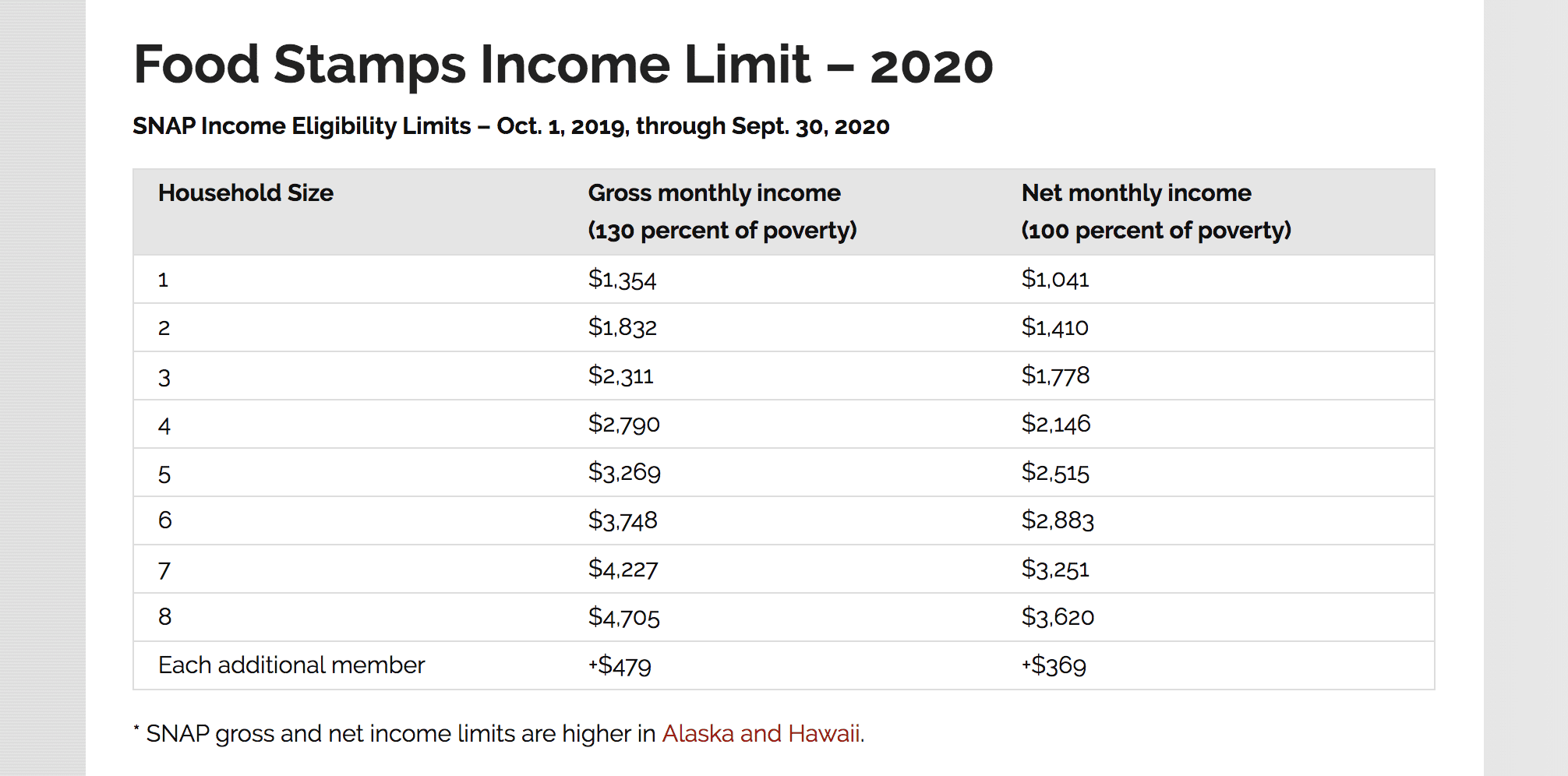

Supplemental Nutrition Assistance Program

Also called SNAP, this is what used to be called food stamps. It’s the most extensive federal nutrition assistance program. You must apply through your state’s program, and there are income limits.

Typically, applications are processed, and you’re informed of your eligibility within 30 days, but it may take longer under current conditions.

You must complete an eligibility interview and provide proof of the information you provided in your application. The interview can usually be done over the phone, and almost certainly will be during the pandemic.

You can find your state’s application here.

Women, Infants, & Children

The WIC program provides federal grants to states for supplemental foods, health care referrals, and nutrition information for low-income pregnant, breastfeeding and non-breastfeeding women, infants, and children up to age five who are at risk of malnutrition.

WIC has income and other limits. Recipients must have an income at or below an income level set by the state agency they’re applying through.

You can apply through your local office. At the time of this writing, several of the state’s whose sites I checked were still requiring in-person appointments to apply.

That may change, so be sure to check the requirements of your state.

WIC has restrictions on what items can be bought, brand, size, etc. We all know the situation in the grocery stores.

If you’re shopping, please be mindful not to buy WIC approved items if you have other options.

Leave them for those on the program who have fewer choices. The tag above shows what to look for.

Child Nutrition Programs

This program includes several options, including free school breakfast and lunch. Schools are closed across the country, but many areas are still providing meals on a take-away basis.

Check with your child’s school to see what arrangements are being made.

Your Community

There are so many community options for free groceries or meals; community groups, restaurants, and religious organizations.

I can name a dozen locally-owned restaurants in New Orleans that are offering free meals, some to anyone who needs one, and some to hospitality employees since they’re so severely impacted.

Check the local resources we mentioned above to find out where you can get groceries or a meal.

Cook at Home

We can’t go out to eat but we can still get take out or delivery in most places. If you’re in a position to support the locally-owned restaurants in your area, by all means, do so.

But cooking at home is a lot cheaper. We’ve done a few articles on how to cook cheap meals at home when you’re on a budget.

Government Relief

Benefits.gov helps you locate qualifying federal assistance in the U.S. The site can help you with healthcare, housing, family and children services, and more. It’s become the official benefits website of the U.S. government.

Temporary Assistance for Needy Families

Also known as TANF, this program provides temporary financial assistance to pregnant women and families with one or more dependent children. It provides monthly cash benefits and may help with housing costs.

Apply through your state here. You can check your eligibility here.

Child Care

Not everyone can work from home, and with schools closed, it’s a struggle for parents to find child care. These resources can help.

State Resources

This site lists child care closure status and emergency child care provisions for each state.

Winnie

This site has listings for emergency child care options around the country. You can search by city or zip code.

Komae

This site is a cooperative, babysitting app. Families can swap care, and the app is working with some healthcare organizations to arrange child care for essential workers.

Education

At the time of this writing, it seems very unlikely that K-12 schools are going to resume before the end of the school year. Here are some resources to help your kids keep learning.

New York Department of Education

This is a 10-day curriculum that covers a variety of subjects for every grade from pre-K to 12. There are curriculums for Phys ed, special ed, multilanguage and more.

Outschool

Your students’ age 3-18 can find more than 10,000 classes live and online for subjects including English, math, social studies, science, coding, music, languages, and more.

Varsity Tutors

Varsity Tutors is offering Virtual School Day, a free program for K-12 students. It includes live, online classes taught by tutors experienced in the course subject and with remote teaching.

Topics include math, reading, writing, and science.

Practical Lessons

Not everything worth knowing is taught in a classroom. If you’re home with your kids, why not incorporate some practical lessons into your day?

Teach them some essential personal finance habits, how to cook, sew on a button, change the oil in a car, or a million other things that will be more useful than diagramming sentences ever was.

Loans

If you need cash, a personal loan is an option, especially if you have a good credit score. The better your score, the lower the interest rate you’ll be offered. You can get a personal loan from:

- Your bank

- Your credit union

- An online lender

- A peer-to-peer lender

Upgrade offers personal Loans up to $50,000 with competitive and low fixed rates and fast funding. A personal loan can help you eliminate high-interest credit card debt, streamline your credit or upgrade your life with a fixed-rate loan instead of a high-interest credit card.

Credit Cards

If you didn’t have credit card debt going into all this, you might have it coming out.

What Will Happen?

You have a bit of a grace period for late credit card payments, at least 21 days for new purchases. There is often no grace period on cash advances or balance transfers.

So you have a bit of breathing room here before things go south.

How Fast Will It Happen?

Late charges can start racking up fast. If you’re even a day late, you might be charged a late fee ranging from $25-35.

Your card may also be canceled, and you might only find out when you try to use it. Closing an account is at the discretion of the credit card company.

What Can You Do?

Call as soon as you know you won’t be able to pay and ask what is typically done in this situation.

The rep may be able to extend your due date, which will give you some time to come up with the minimum payment. You can keep your credit cards out of default by paying a minimum.

While you have someone on the phone, ask if they can lower your interest rate.

Or you can have someone negotiate it for you. National Debt Relief specializes in debt settlement and will negotiate settlements for thousands of creditors and collection accounts.

Credit card companies will forgive some of your debt if you’re in trouble. Get a $10,000 bill reduced to $4,000 just by asking. National Debt Relief negotiates on your behalf.

You can also refinance your debt to a lower rate and immediately drop your monthly payments.

What Are The Consequences?

You’ll get the usual late charges. After 60 days, your interest rate may increase to the default or penalty rate; the late payment will be reported to the credit bureaus lowering your score and leaving a black mark on your credit report.

After 6-7 months of non-payment, your debt may be charged off and sold to a third party debt collection agency.

These kinds of collectors are much more aggressive than dealing with a credit card company. You have certain rights, but not everyone is aware of them, and these bottom feeders know that and will push the envelope.

It will be a much less unpleasant experience if you can keep the debt with the originator.

Student Loans

Forty million of us have them, and more than five million of us are in default, so if you get behind, you’re in good, or at least plentiful company.

It’s nearly impossible to discharge student loans in bankruptcy, and if you have federal loans, the government can hold your tax refund and garnish your wages if you default.

What Will Happen?

I am guilty of being late on student loan payments a looooong time ago. I don’t ever remember getting a call.

It may be a case of giving us the rope to hang ourselves because student loan lenders are rarely going to end up on the hook for a bad debt.

If we’re feeling charitable, it could be because loans are passed from one service to another, and sometimes things get lost in the shuffle.

So if you aren’t organized, it might not be that you didn’t have the money to pay but that you sent the payment to the wrong place and don’t know it.

How Fast Will It Happen?

A loan is considered delinquent the day after the due date. Most federal loans are in default when 270 days late.

What Can You Do?

So many of us have student loan debt that it is probably the easiest on this list to get help with. They can’t throw all forty million of us into debtor’s prison if things go wrong, so there are lots of assistance programs to help us if we get into trouble.

And that was the case before COVID-19. Because of the pandemic, there are some new options in place to help.

What Are The Consequences?

You’ll have the usual late fees and ding on your credit report. But a defaulted student loan probably has the worst real long-term consequences.

Unlike most consumer debt, student loans cannot be discharged in bankruptcy in all but a very small set of circumstances. So defaulted student loans can literally haunt you to the grave.

Federal Suspension

As part of legislation passed in late March, federal student loans are suspended until September 30, 2020. Allegedly, you don’t need to take any action, don’t need to contact your loan servicer.

I believe it’s still a good idea to contact your loan servicer and ask if there are any steps you need to take to ensure your loan payments have been suspended.

Because frankly, I don’t trust the current Secretary of Education at all.

Private Student Loans

Private student loans are not included in the suspension. And some federal loans under the Federal Family Education Loan (FFEL) Program are held by private lenders, and some Perkins Loans are held by the college or university you attended.

These loans are also not included in the suspension.

Federal loans held by private lenders offer income-driven repayment plans. You might be able to enroll online rather than calling your servicer.

If you just need a short-term pause on payments, you might be able to get a forbearance or deferment.

For regular, private loans, you’ll need to contact the bank or credit union to see what if any programs they have to help those struggling with their payments.

Car Payment

Some of us depend on our cars to get to and from work. Missing even one car payment can have swift consequences, including the inability to get to work to make money during an already dire situation.

What Will Happen?

You’ll start getting calls from the lender. Why are you late? When can you pay? This is the time to explain the situation and see if they are willing to work with you.

How Fast Will It Happen?

A missed car payment may have more immediate consequences than a missed mortgage payment. Some lenders will repossess your car after just one missed payment, so it’s especially important to call them when you know you can’t pay.

What Can You Do?

You may be able to refinance the loan if you have good credit. Ask for a modified payment, to lower the amount you owe monthly or get a short-term so that you won’t have a monthly payment for an agreed-upon time.

Try to sell the car or turn it over to the lender. You will still be responsible for the difference between what the car is worth and what you still owe on the loan.

If the worst happens and the car is repossessed, you still have the right to any personal belongings that were left in it.

What Are The Consequences?

You may be assessed the late fees and costs of repossession, and the delinquency will likely be reported to the credit bureaus, damaging your credit score.

The loss of the car can start a chain reaction.

If you can’t get to work, you can’t make any money, and you might be fired. If you can’t make money, you can’t pay your other bills either.

While the specter of a home foreclosure seems scarier, losing your car may be the worst thing on this list.

Public Transit

We know that no one is eager to get on public transit during an epidemic, but because so few people are out and about, it’s less crowded than usual.

Cities are making some forms of transit free; buses in New York City for example.

What Not To Do

We know it’s scary to need help paying bills or to need financial assistance, but there are some things you definitely don’t want to do as they will almost certainly make a bad situation worse.

Take Out a Payday Loan

We know when you need money, a payday loan can seem appealing. There is usually no credit check, and you can get the cash fast. But beware.

Payday loans have become the face of predatory lending in America for one reason: The average interest rate on the average payday loan is 391%.

Payday loans can start a neverending cycle of very high-interest debt. Exhaust every other avenue for financial help before even considering taking out a payday loan.

Take a Credit Card Cash Advance

The average interest rate on a credit card is about 15%, while the average rate on a cash advance taken against your card is about 21%.

Not only that, but there is no grace period on a cash advance as there is when you buy or pay something using your card. The second you take the cash out, the interest starts to accrue.

Cash advances typically come with fees too. Some cards charge a flat fee, usually $5 to $10, while others charge a percentage of the amount of the advance, which can be as much as 5%.

That said, if your only choice is between a payday loan and a cash advance, the cash advance is the least worst option.

Ignore Bills

Listen, two months ago, if you were having a lot of these problems, they were your problems. But now there will be millions of us facing these problems, and that makes it the problem of the entities we owe money to that we can’t pay.

If you owe the bank $100, you have a problem. If you owe the bank $10 million, the bank has a problem.

Tweet ThisAs you can see, some entities have moved to help people deal with these problems or the government, be it on the federal, state, or local level, has forced them to do so.

It’s in the interest of anyone you owe money to, to work with you, be that your landlord, your hospital, or your credit card company.

Because if they refuse, thousands of people will be forced into bankruptcy, which means most of these creditors won’t get any money at all.

You do need to call creditors and explain your situation to them and ask them how they’ll work with you be that a payment plan, interest-only payments, a discount, or temporary forbearance.

Don’t just let bills pile up and ignore them. It’s in everyone’s best interest to work together.

More Help Is Available

Please don’t be scared. There is so much help out there! Way more than I ever imagined when I started writing this.

Our goal was to make this as comprehensive as we could and relevant to the greatest number of people while still getting it up as quickly as we could so people who need help can find it.

Researching this showed me how much local help is available. We couldn’t list every single resource available in America; no one can.

We did our best to choose the best resources that would help the most people, but you should also mine the resources local to you.

The best way to find them is to do a simple Google search.

Type in the kind of help you need, followed by the name of your city or state. Here’s an example: “Rental assistance Charlotte.”

It also helps to add COVID-19 at the end of the search. Many more programs have popped up to help with the extraordinary circumstances this pandemic has caused.

An example search might look like this, “Rental assistance Charlotte COVID-19.”

None of us knows what’s going to happen, when this will be over, and what the world will look like when it is. So all we can do is our best to take care of ourselves, our families, and our communities. Good luck and be well.