When I started investing, I didn’t have a clue. I’d never heard of words like tax-loss harvesting, rebalancing, or mutual funds. I thought it was completely reasonable to pay my financial advisor a 1% annual fee. Someone had to rebalance my portfolio, right?

And brokerage firms? I couldn’t have told you who Vanguard was let alone John C. Bogle.

But then I got curious. I started reading about personal finance. Now I’m startled by some of the words escaping my lips:

“Vanguard funds have some of the lowest expense ratios in the industry.” “Betterment offers investment accounts using low-cost exchange-traded funds.”

Who had I become? Life is an evolution. Enjoy the change.

Speaking of

An Executive Summary

Minimum Investment:

$500

Management Fees:

0.25%

Promotion:

Invest your first $5,000 free, for life

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$10 billion

Minimum Investment:

$1,000

Management Fees:

0.04% - 0.30% advisory fee

Promotion:

Invest

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$5.3 trillion

Betterment vs. Vanguard: What’s the Difference?

The main difference between

Vanguard

Vanguard was founded in 1975 by John Bogle. Mr. Bogle championed low-cost, buy-and-hold investing, scoffed at Wall Street, and fought tooth and nail to lower costs for ordinary investors.

Instead of having investors try to pick winning stocks, he thought it would be more advantageous if investors owned every stock in the index and mirrored the returns of the market.

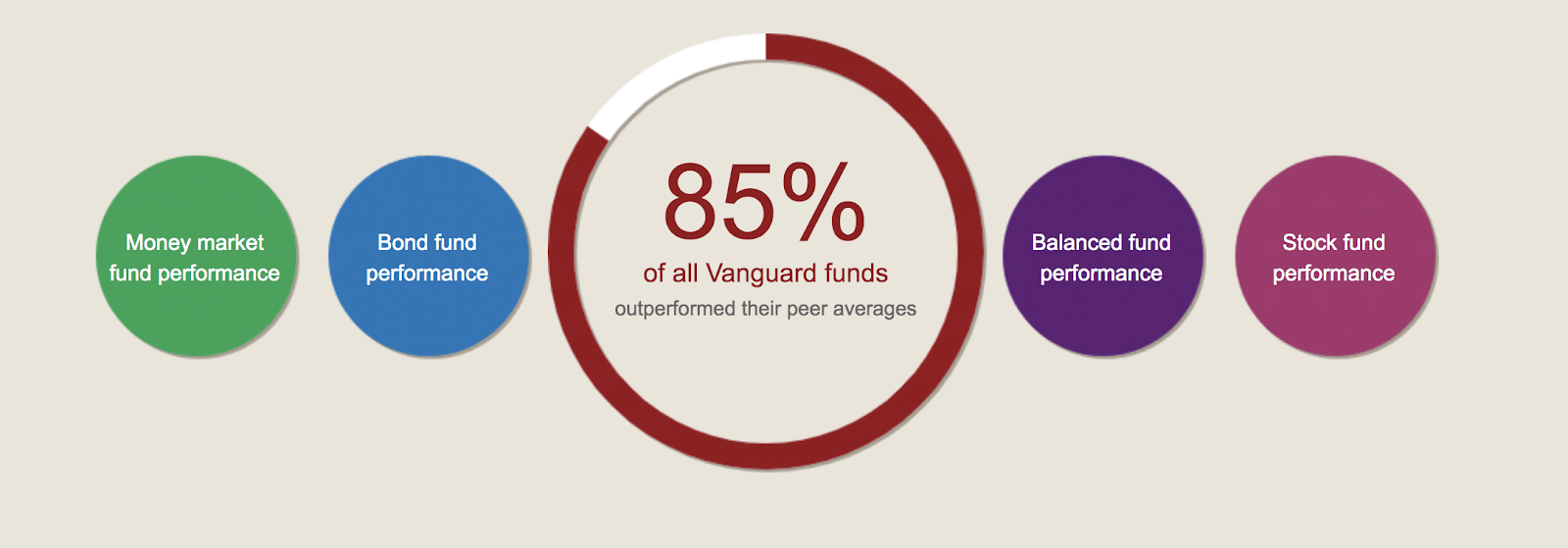

Mr. Bogle saw the correlation between low management fees and exceptional investment returns with a buy-and-hold-own-every-stock-in-the-index approach.

Andrew wrote a detailed article on why mirroring an index for an “average market return” is superior to market timing or picking individual stocks.

Vanguard is also client-owned. You, a shareholder of Vanguard funds, own a piece of the company (spoiler alert: it’s how they can keep costs so low).

Holding a contrarian position to how other mutual fund companies operate, Vanguard operates at cost: you only pay for the costs to manage the fund – nothing else. As Mr. Bogle said in this article from Market Watch:

This business is all about simplicity and low cost. I’m not into all these market strategies and theories and cost-benefit analyses – all the bureaucracy that goes with business. In investing, strip all the baloney out of it, and give people what you promise.

Vanguard has grown to $5.3 trillion in assets under management (AUM), is the largest provider of mutual funds, and the second-largest provider of ETFs in the world.

Vanguard is owned by their funds so they are uniquely aligned with the interest of their investors. As a result, Vanguard funds usually have the lowest fee rate in their category. Mind you, signing up is more work and requires more decisions than Betterment.

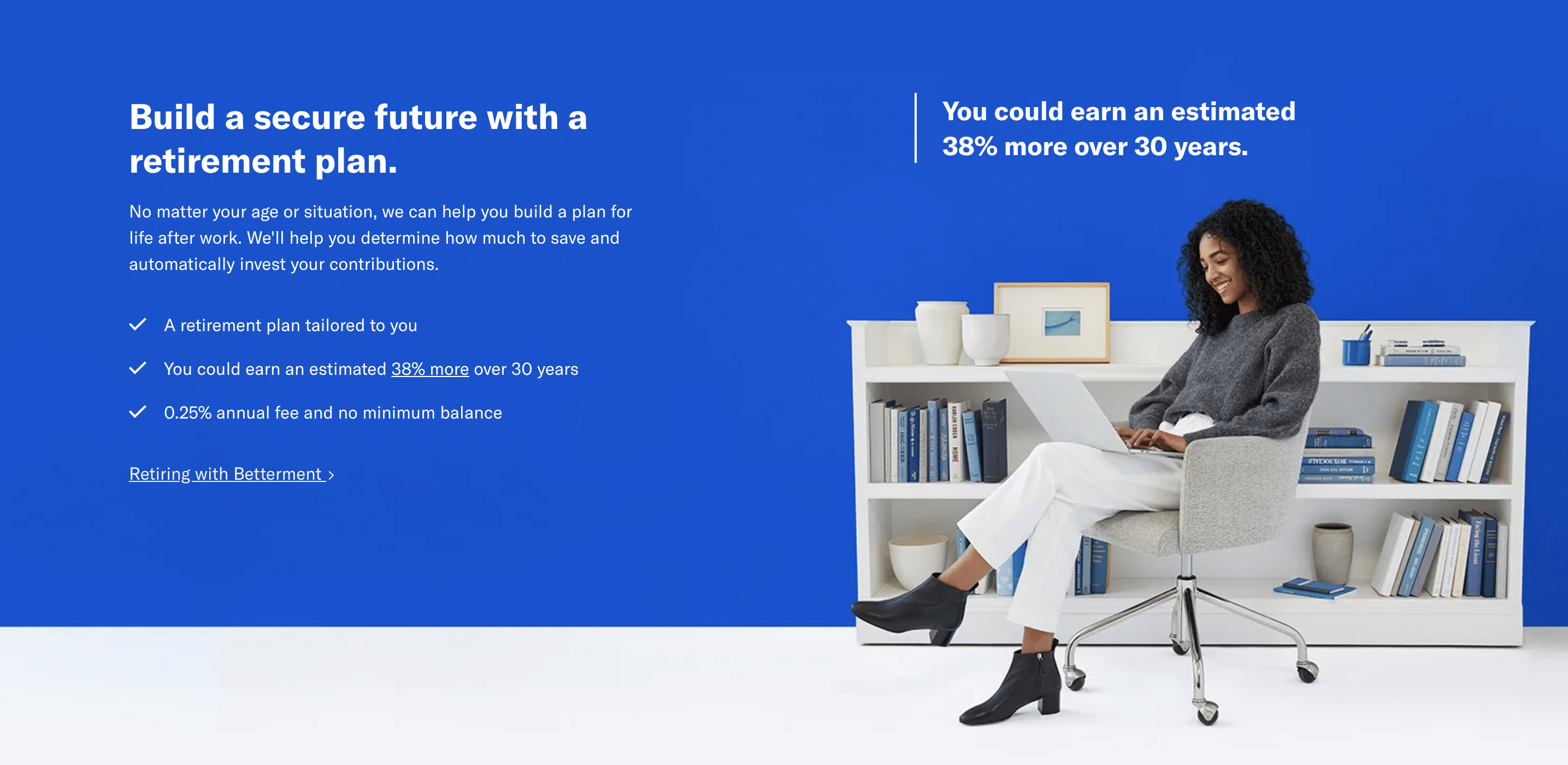

Betterment

Founded in 2008,

Their mission statement:

We’re building smarter, more efficient money management for everyone… By pushing the bounds of what technology can do, by bringing together the best software and analytic thinking of diverse, cutting-edge industries, we’re able to ensure that more get the advice that they deserve.

Stein took inspiration from John Bogle and the Vanguard group. The two met briefly in 2009, while Bogle was on campus to promote his book, Enough.

Jon feverishly pitched his ideas while Bogle listened attentively, asking questions, until finally saying to Stein, “You’re going to help a lot of people. Stay the course!”

They’re an SEC-Registered Investment Advisor, an SEC-registered broker-dealer regulated by FINRA, and a member of SIPC (which means your money is insured up to $500,000).

They’re now one of the biggest robo-advisors in the country.

We even had Jon Stein on our podcast for a chat. Have a listen!

Fiscal flexibility that’s funny, free and delivered weekly.

Costs

Expense Ratios

Whether you want to open a

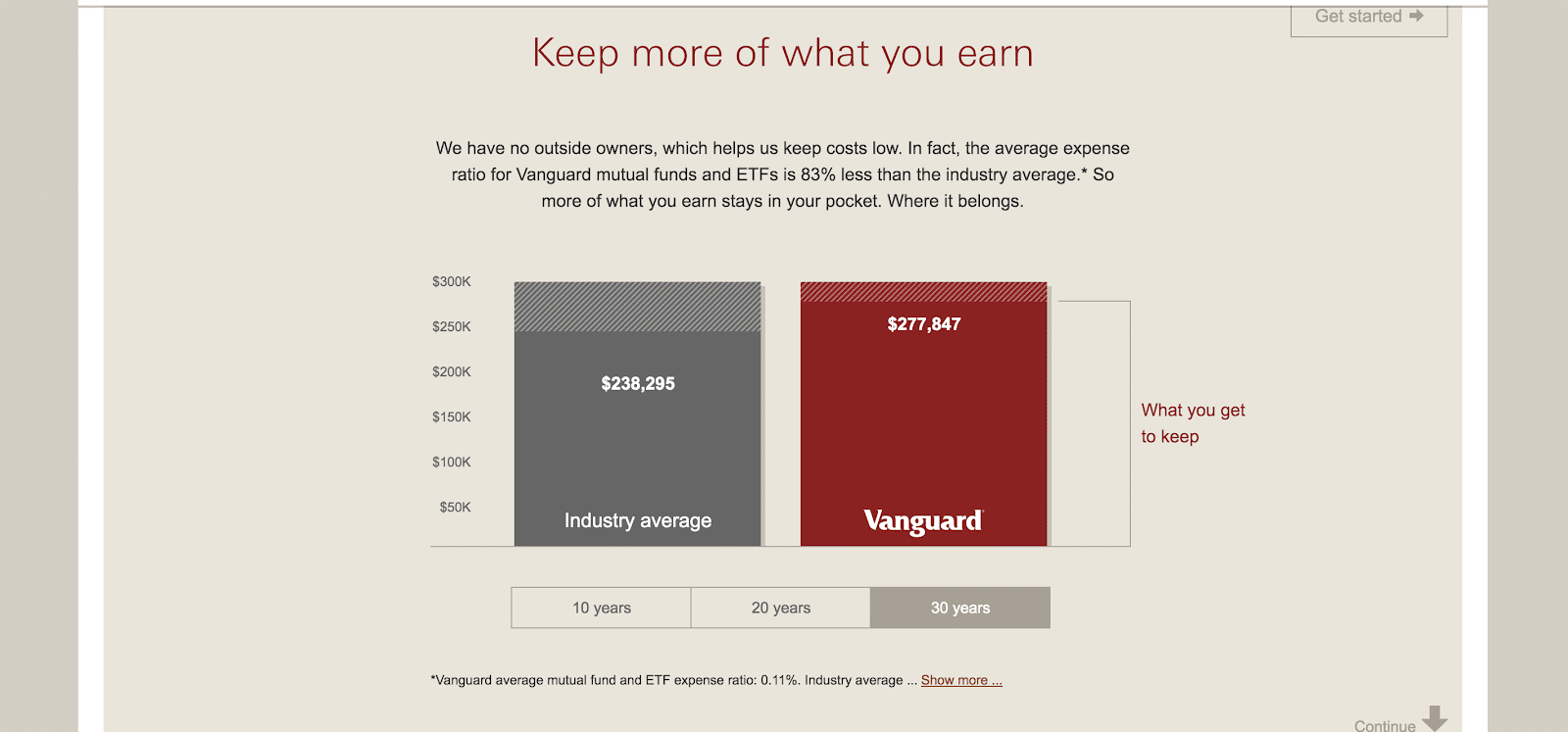

Vanguard is the low-cost leader. Their funds are 83% less expensive than the industry average.

The average expense ratio (operating cost) of a Vanguard fund is 0.1%. Their total U.S. stock index fund and ETF equivalent are even lower at 0.04%. That’s $4 annually on a $10,000 account balance.

Compare that to a 0.58% industry average.

Keeping up with Vanguard’s low prices has led to a phenomenon: the Vanguard Effect. Mutual fund companies are forced to offer similar-priced products to compete with their low costs.

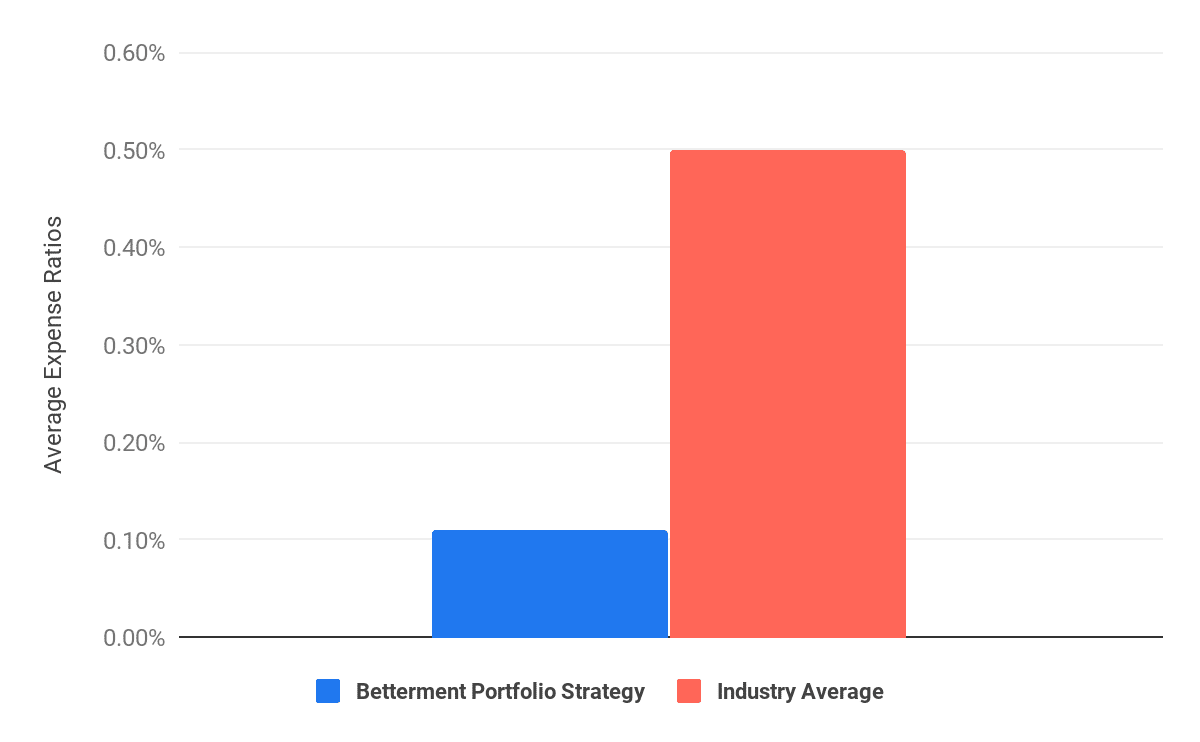

Betterment is also a superior, low-cost alternative to other brokerage firms with an average ETF expense ratio varying between 0.07% and 0.15%.

It’s no secret

Account Minimums

Vanguard has several investment options, each with its own account minimum. If you want to access their catalog of over 3,000 no-transaction-fee mutual funds, you’ll need at least $1,000.

Their Target Date Retirement Funds and Star Funds both have a $1,000 minimum, while their Admiral Shares cost $3,000. ETFs, stocks, CDs, and bonds all cost the price of one share.

If you’re looking for that personal touch only an advisor can give, you’ll need a $50,000 minimum to take advantage of the Vanguard Personal Advisor Service.

Betterment has no minimum, which makes it very attractive to investors with low account balances. If you’re getting started and prefer someone to manage your money for a small fee,

Management Fees

Both

Beware of little expenses. A small leak will sink a great ship. – Ben Franklin

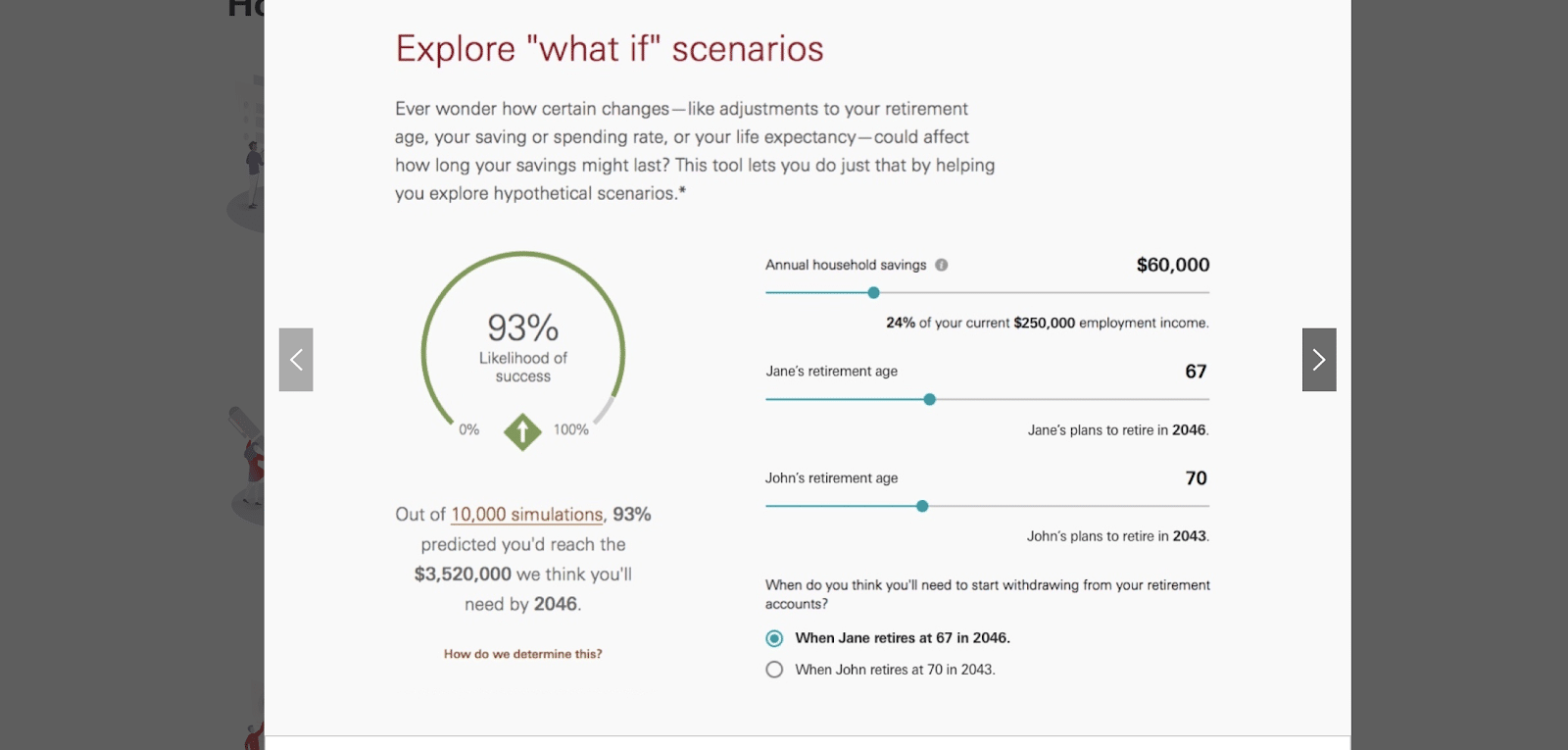

Vanguard’s advisory service costs 0.30% on assets below $5 million (don’t forget about that $50,000 minimum too). Portfolios are constructed on a client-by-client basis, depending on your investment strategy.

***The above is an example of Vanguard’s advisory service portfolio playing out “what-if” scenarios***

However, the higher your account balance, the lower your fee. For example:

- Your fee drops to 0.20% on assets between $5-$10 million

- Assets between $10 million and $25 million carry a 0.10% management fee

- $25 million and above cost you 0.05%.

Betterment has two tiers: its Digital Plan and Premium Plan.

- The Digital Plan has an annual 0.25% management fee and has no account minimum

- Premium Plan carries a 0.40% fee and has a $100,000 minimum account balance requirement

You can stay with the Digital Plan forever, or when you hit $100,000, you can upgrade to Premium.

Vanguard can supplement its management fee by using its own funds, which is an advantage

Financial Advice: Schedule A Call

- Getting Started Package ($199)

- Financial Checkup ($299)

- College Planning ($299)

- Marriage or Retirement Planning package ($299)

If you decide to upgrade to the 0.40% Premium plan, you’ll have unlimited access to a team of certified financial planners while retaining all of the benefits of the Digital Plan.

You also have the option to get matched with a pre-vetted CFP through

What Do Your Management Fees Pay For?

The Vanguard Personal Advisor Service manages IRAs, Individual accounts (mutual fund or brokerage), Trusts, and Vanguard Variable Annuity accounts.

Accounts excluded from their advisory services (and don’t count toward the $50,000 minimum balance):

- 401(k) & 403(b) accounts

- i401(k) accounts

- 529 accounts

- UGMA/UTMA accounts

- Accounts held outside of Vanguard

Betterment offers investors Individual and Joint taxable accounts, Traditional IRAs, Roth IRAs and SEP IRAs, 401(k) and 403(b) Rollovers, and Trusts.

Accounts excluded from

- 529 accounts

- Custodial accounts

- HSAs

- Solo 401(k)s

- Self-directed accounts (you can’t choose your own funds or stocks)

Depending on what your investment strategy is will determine what you choose.

Investment Options

Vanguard’s product offerings outnumber

Vanguard’s shortlist of product offerings:

- Traditional and Roth IRAs

- Annuities

- 529 College Savings plans

- SEP, i401k, and SIMPLE IRAs

- 403b services

- Individual and Joint accounts

- 401k Rollovers

- Mutual Funds & ETFs

- Individual Stocks, Bonds, CDs, and Options

- Factor-based Investing (smart beta)

- Sector Investing

- ESG (environmental, social, and governance) Investing

If DIY investing appeals to you, Vanguard might be a better fit. They have the edge over

Betterment

However, if you’re looking for a more hands-off approach and prefer to invest in

With their guidance, you’ll construct a globally diversified investment portfolio across 12 asset classes using pre-selected, low-cost ETFs (most notably Vanguard, Charles Schwab, and iShares).

It’s for this reason that DIYers might be turned off by

The flip side to this argument:

Betterment account. They also use fractional shares, so you’re fully invested at all times.

You do have three additional portfolio options:

- Socially Responsible Investing (SRI) puts your money in companies meeting specific social, environmental, and governance criteria

- Goldman Sachs Smart Beta is a multi-factor modeled portfolio (as opposed to a traditional market-cap-weighting) looking to take an even greater calculated risk for potentially higher returns

- BlackRock Target Income is a 100% bond portfolio and lets you choose between short-term and long-term fixed-income securities

Enhanced Suite of Automated Tools

It’s a beast of a service equipped with a Retirement Planning Suite, automatic rebalancing, tax-loss harvesting, goal-based investing, and tax-coordinated portfolios.

While

General rule-of-thumb: the higher your tax bracket, the more you’ll benefit from tax-loss harvesting.

Here’s where the edge tilts to

A Target Date Fund Alternative to Betterment?

Rebalancing

This is what matters most to all investors, especially the DIYers. You want your portfolio to remain optimized for taxes (so you’re not paying unnecessary costs to Uncle Sam), and you want to stay the course with your asset allocation (i.e., all portfolios drift outside of their target asset allocation and will need to be rebalanced).

If you’re not sold on

- Vanguard Target Date Retirement Funds

- Vanguard LifeStrategy Funds

Target Date Funds rebalance your portfolio automatically, so you’re still mostly hands-off. These funds start with a high stock-to-bond allocation then gradually shift away from stocks and add more bonds as you near retirement.

Vanguard puts it this way:

The funds’ managers gradually shift each fund’s asset allocation to fewer stocks and more bonds so the fund becomes more conservative the closer you get to retirement.

Ideal for the Lazy

Personal finance whiz Ramit Sethi is a big fan of these and even talks about them in his book, I Will Teach You To Be Rich:

“That’s why target-date funds are great: They’re designed to appeal to people who are lazy. In other words, for many people, the ease of use of these funds far outweighs any minor loss of returns that might occur…”

Vanguard’s average expense ratio for target-date funds is 0.12%. That’s 81% less expensive than the competition.

Or, if you prefer a static asset allocation, consider Vanguard’s LifeStrategy Funds. These are similar to target-date funds with one exception:

They rebalance to ensure your correct allocation stays the course as Mr. Bogle would say. For example, if you got their growth fund with an asset allocation of 80% stocks and 20% bonds, the fund manager would rebalance to maintain that stock-to-bond ratio.

Vanguard LifeStrategy Funds carry an average expense ratio of 0.13%.

Tweet ThisTaxes

This approach does have its critics. Betterment argues that target-date funds are out of date for a few reasons:

- Lacks sophistication of tax coordinated portfolios

- Target date funds aren’t tailor-made to the individual

- Exact years are more efficient than a broad date

There is no “one size fits all” approach when it comes to investing. Every person’s situation is different. It’s a good idea to know what’s available before making a decision.

Educational Resources

Both

Mobile App

You’ll find

Final Thoughts

Who’s better? I use both. I have a Big Purchase investing goal through

My Roth and taxable brokerage accounts live at Vanguard. I’ve yet to have a bad experience with either company.

If you’re going the DIY route, use Vanguard to build a portfolio of low-cost index funds or ETFs and rebalance at least once a year. Be mindful of optimizing your portfolio for taxes and put the right assets in the right investment buckets.

If rebalancing once a year doesn’t sound like enough, try it twice a year or quarterly.

If you’re going the “hands-off” route, use

What’s important is that you get started.