Feeling lost trying to manage your money is terrible. For many, budgeting carries a steep learning curve that turns would-be budgeters off. You think you’ll never save enough, it’ll require too much of your time, and you never seem to know what to track or categorize.

In this Mint review, I’ll examine how this budgeting app can help manage your money. I looked at some of its notable features, including how it works, bill tracking, credit score, and more.

Be sure to read through to the end to decide if Mint is right for you. I’ll also address concerns regarding its safety, alternatives, and what it does with your data.

Let’s get started!

What Is Mint?

Mint is a free, online personal finance app that syncs all of your credit cards, bank accounts, and investment accounts.

Its money management service focuses on budgeting by monitoring your cash flow.

The Mint app categorizes transactions, analyzes your spending trends, and oversees all account information on your financial dashboard.

It’s brought to you by Intuit (owners of

- Fortune 100 Best Companies to Work

- People Magazine Companies That Care

- Forbes America’s Best Employers for Diversity.

Intuit has grown to over $6 billion in revenue, while the Mint app has over 20 million users.

How Mint Works

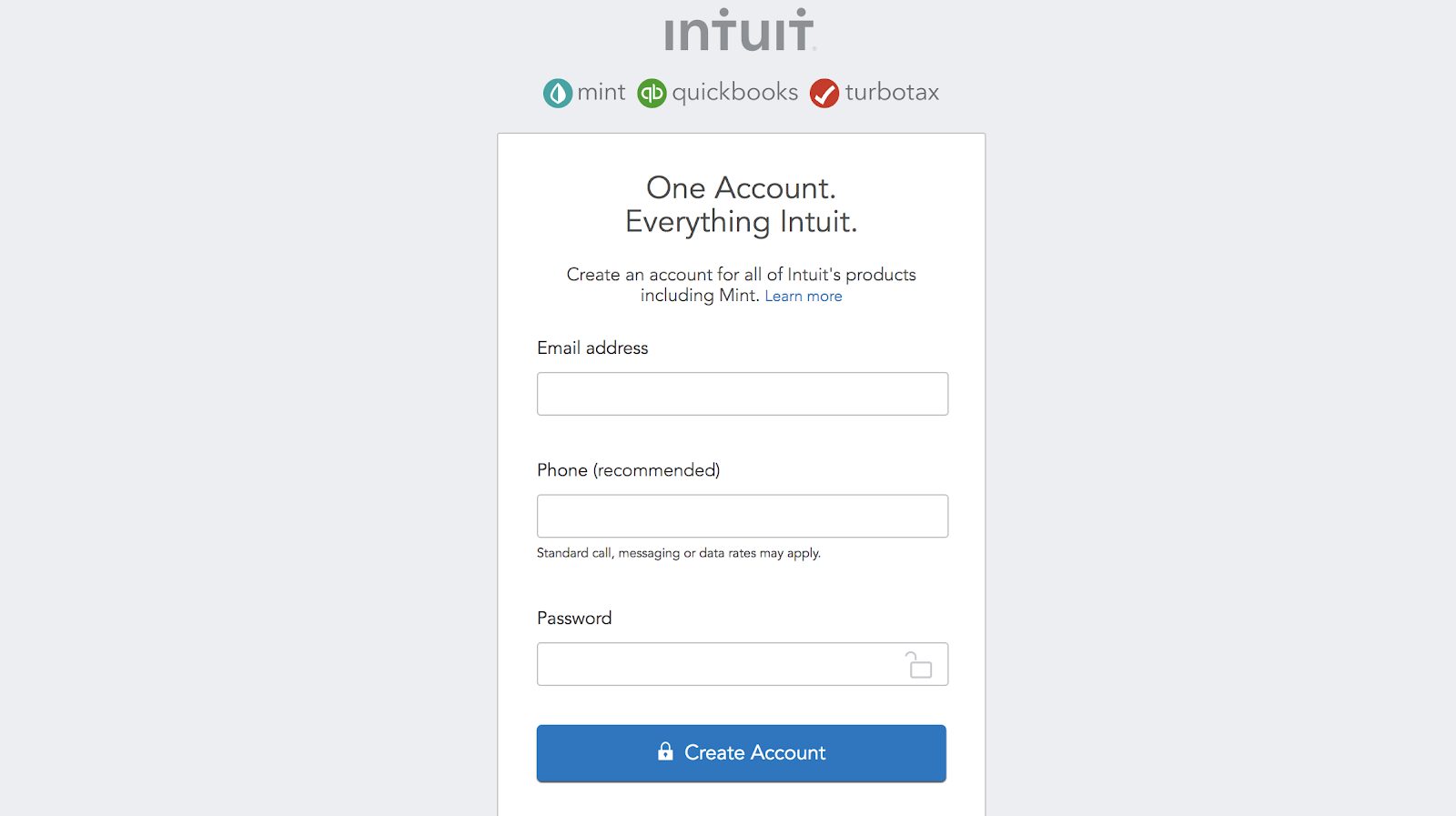

Mint offers a one-stop-shop for all of your money-tracking needs. Creating an account is simple and straightforward. Sign up with an email address, create a password, and start adding your bank accounts.

I recommend completing your user profile once creating your Mint account. Fill in your address, age, income status, rental status, education, and other additional information. Why?

Because Mint uses that information to look for ways to optimize your situation.

It connects to virtually every financial institution on the web. Link all financial accounts: IRAs, real estate, checking accounts, savings accounts, 401(k), loans — everything.

Mint scans thousands of credit cards, banks, and brokerage offers to find ones matching your spending patterns.

Perhaps you spend most of your money at Trader Joe’s. Mint will recommend a credit card that gives 5% cashback on grocery purchases.

The more accounts you link, the more recommendations you’ll get. Once Mint has all of your account information, it determines your net worth.

This metric is critical to achieving financial success. Now you’ve got a starting point to track your spending, set goals, and create budget categories.

Your information displays in real-time.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Mint Features

Here’s a snapshot of Mint’s features with detailed explanations of each below. We cover essential budgeting features, including whether it has bill tracking, mobile app accessibility, a free credit score, and more.

| Cost | Free |

| Accessibility | iOS and Android devices, desktop |

| Bill Tracking | Yes |

| Free Credit Score | Yes |

| Goal Setting | Yes |

| Spending Trend Analyzation | Yes |

| Investment Tracking | Yes |

| Alerts and Reminders | Yes |

| Retirement Planning | No |

| Bill Payment | No |

Bill Tracking

While you can’t pay your bills through the app, you can monitor them.

Some folks are disappointed Mint no longer offers bill pay, but that’s an easy fix – set up automatic deposits through your bank and track them through the app.

Schedule alerts to notify you about upcoming bills and set due dates, so you know ahead of time.

Mint stores your bills in one place, which makes it easy. Some you’ll have to manually enter if not found in Mint’s database like rent or music lessons, but they’re mostly all there.

Reminders & Alerts

Set up notifications that alert you when your account balance falls too low. This way, you’re never hit with an overdraft fee. You can request Mint to notify you of not only upcoming bills and low account balances, but unusual spending.

Need to know when you’re over budget? That ATM fee? What about suspicious activity?

Mint has a suite of alerts you can activate that will track all of them. Enable weekly reports and quickly scan your data.

These are some (but not all) of the alerts found in the app:

- Low Balance. Set a dollar amount that will trigger this alert and if your balance dips below it, Mint notifies you

- Bill Reminders. Combine this with autopay through your bank, and your bill payments will be seamless

- Unusual Spending. I find this useful when tracking specific categories. If your spending in any category is above average by a dollar amount, you’ll see

- Over Budget. If you’ve created a budget in the app and exceed your allowance, this will tell you it’s time to reel it in

- Bank Fees. Never pay bank fees. Set this to the lowest amount (which is $1)

- Large Purchases. I recommend setting it between $100 and $200. I don’t have too many of these, but I’d want to know about it if I did.

- Goal Notification. If you’re tackling a savings goal, activate this alert. It’s fun to observe your progress.

- Weekly or Monthly Reports. Choose how often you want to get progress reports. Weekly might be a better idea if you’re trying to control your spending.

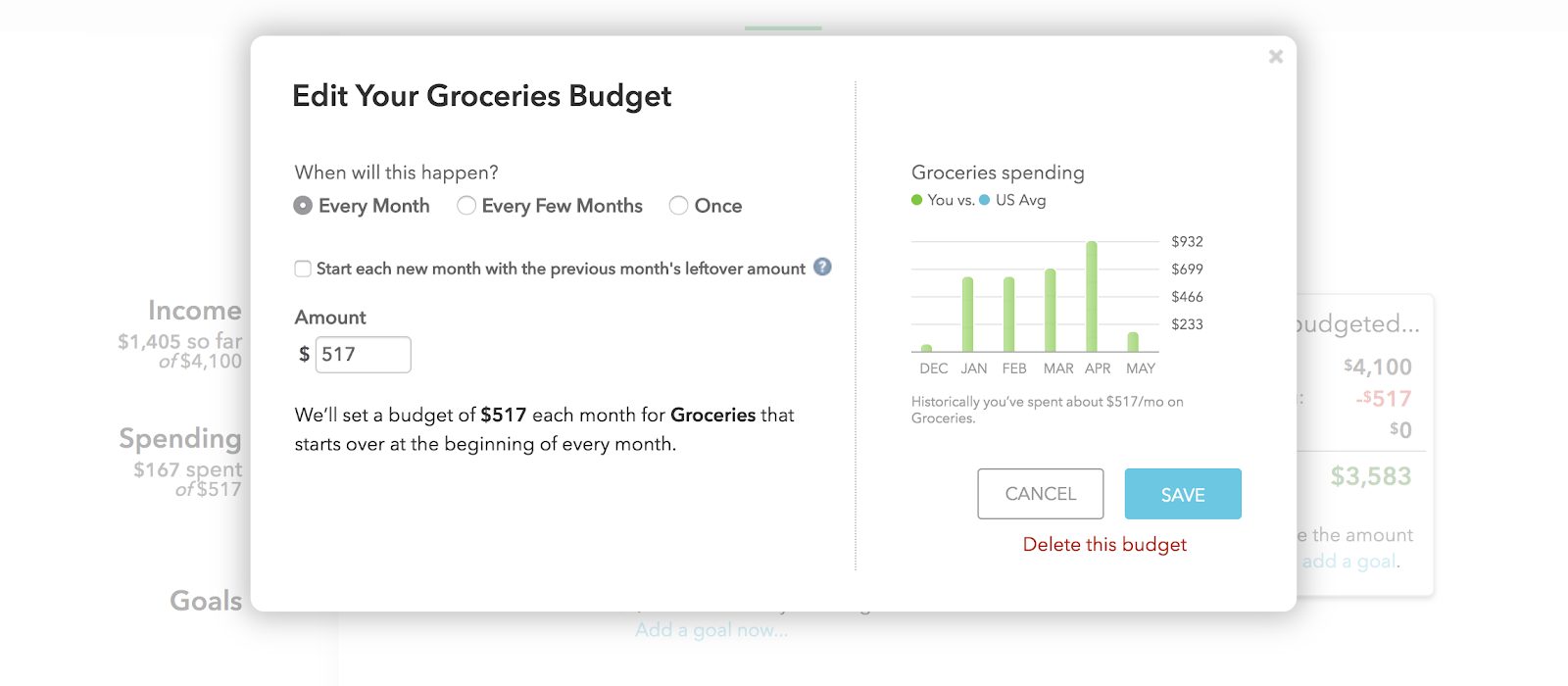

Budgets

Create a budget based on last month’s earned income. If you’ve got a steady paycheck, this should be easy. If you’re a freelancer with adjustable income, use last month’s earnings as your benchmark.

If you don’t know what you earned last month, you must figure that out before creating your budget categories.

The budgeting tool compares your spending in specific categories and lets you see how you’re doing monthly or annually.

Mint will suggest budgets for you based on your spending, or you can create your own. Categorize income and expenses as bi-weekly, monthly, recurring, or one time.

Helpful Tip

Budgeting by category makes it easy to see your progress. For example, if you’re trying to cut down your grocery bill, you’d pull up your grocery budget to see if you’re on track.

Mint will also show you how your spending is affecting your savings. Are you overspending on dining? Can you cut back in that area to free up cash to meet your financial goal?

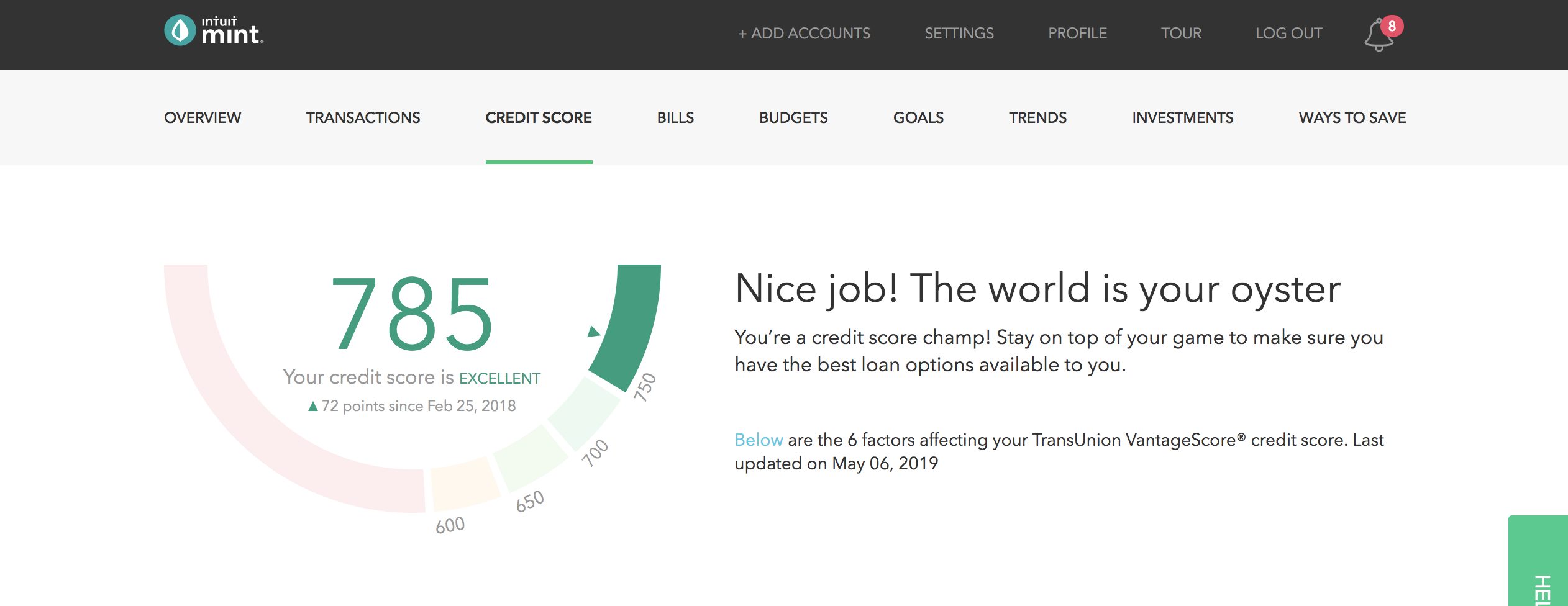

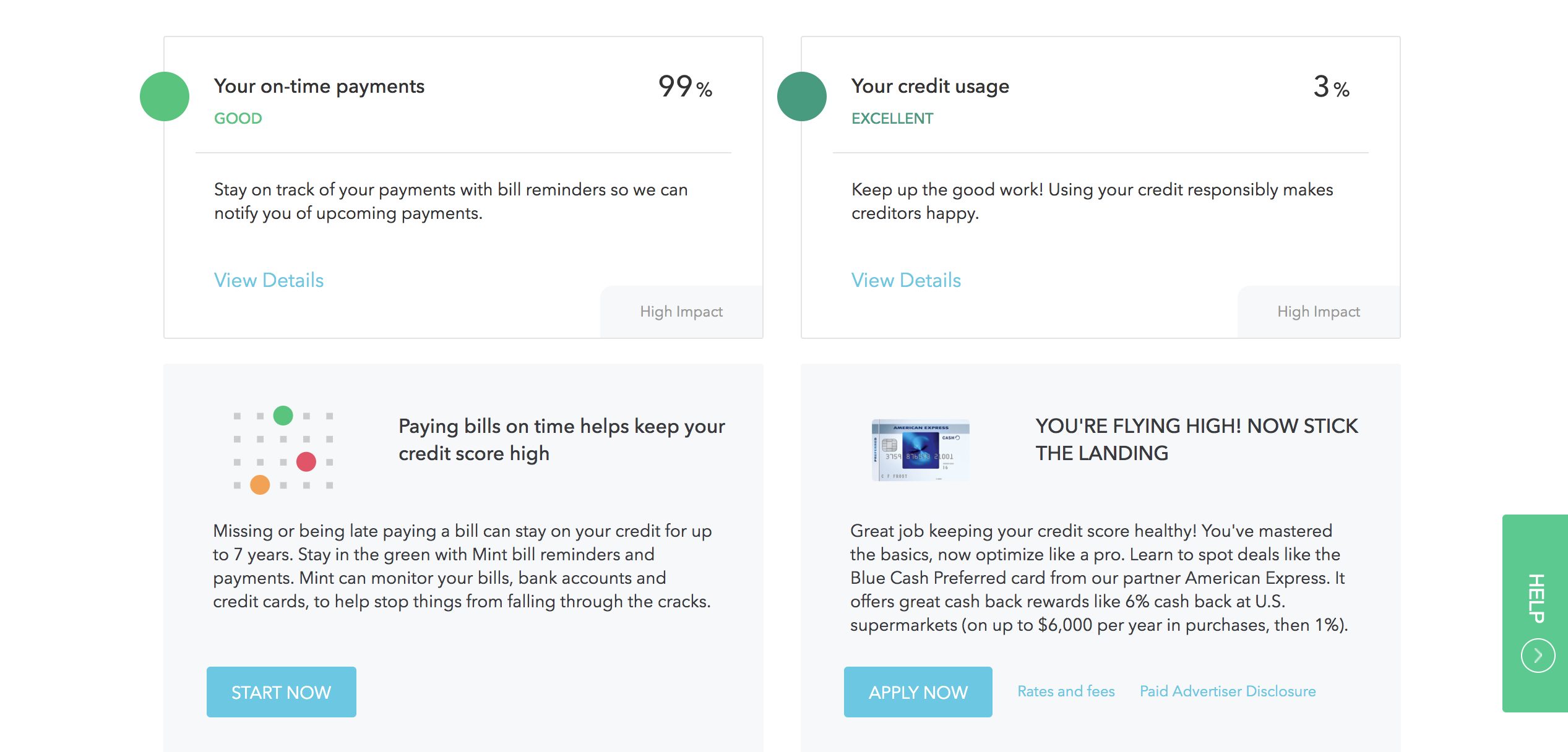

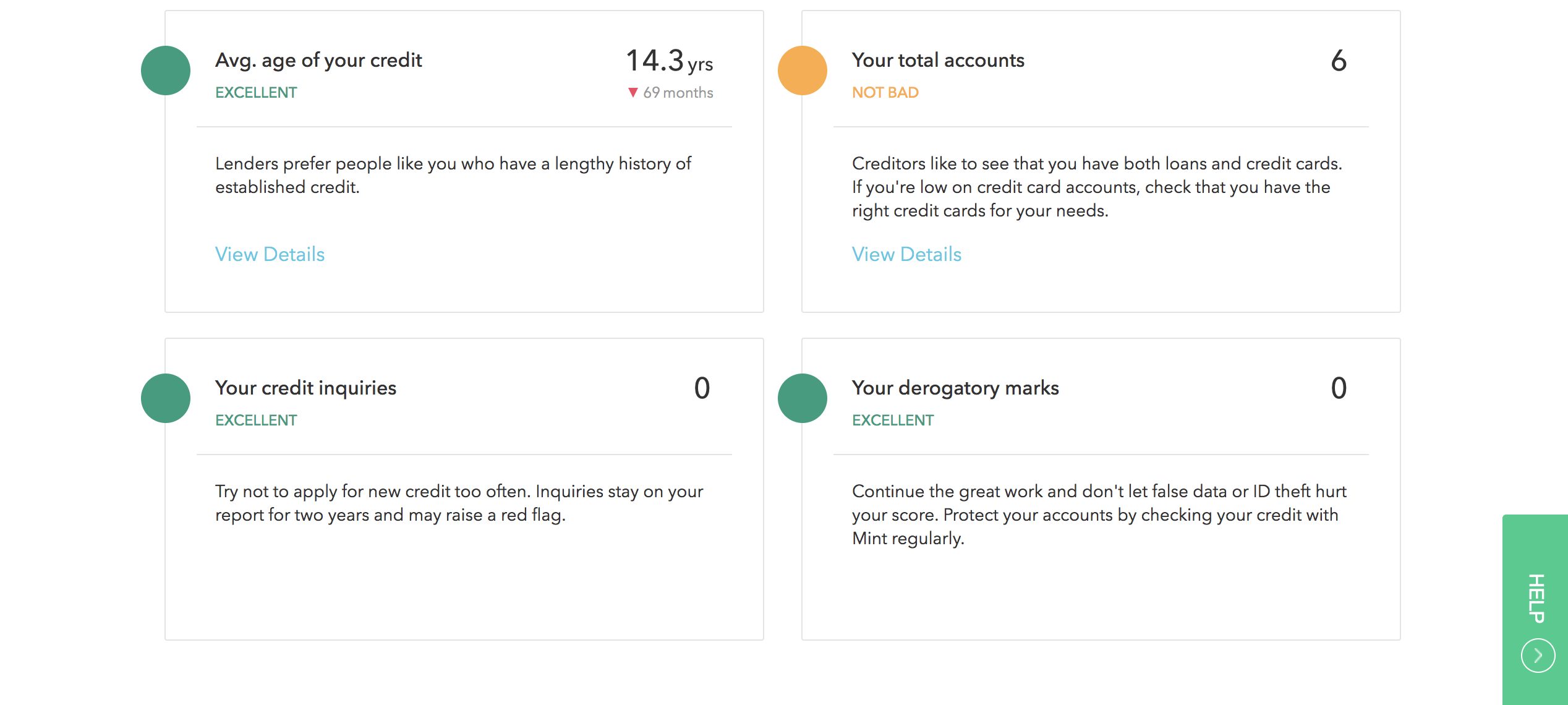

Credit Score & Monitoring

If you’re looking to increase your credit score, this feature will help. It’s great for folks who are applying for a loan. TransUnion powers your free credit score and shows you:

- Your on-time payments

- Your credit usage (aka credit utilization)

- The average age of your credit

- The total number of existing accounts.

- Your credit inquiries.

- Any derogatory remarks.

If your score isn’t the best, Mint provides feedback on why it’s so and then steps for improvement.

Your credit score affects interest rates offered on loans, insurance, and credit cards. Aim for a score of 700 or higher to secure lower rates.

TransUnion notifies you through the app whenever there’s an update.

An excellent free budgeting tool. I use it, and if you're getting started, you should too. If you don't track your spending, you'll never know where you're wasting money.

Easily Categorize Your Transactions

Mint has several default categories, so you may not have to do much work. However, it’s important to scroll through your transactions to determine their accuracy.

Choose from their default selection or create custom categories.

You can also train Mint to remember purchases under the Rules category. For example, if you always buy coffee through Amazon, the transaction will appear as shopping.

If you go into Rules and list that specific transaction as Groceries, it will start showing up as groceries. Over time, every future purchase will be in the right category.

Mint lets you get as detailed as you want, but remember to keep it simple. Getting too granular defeats the purpose.

You can create tags as well, like Eating Out or Online Rentals. Any kind of purchase you make regularly will be easier to find through tags.

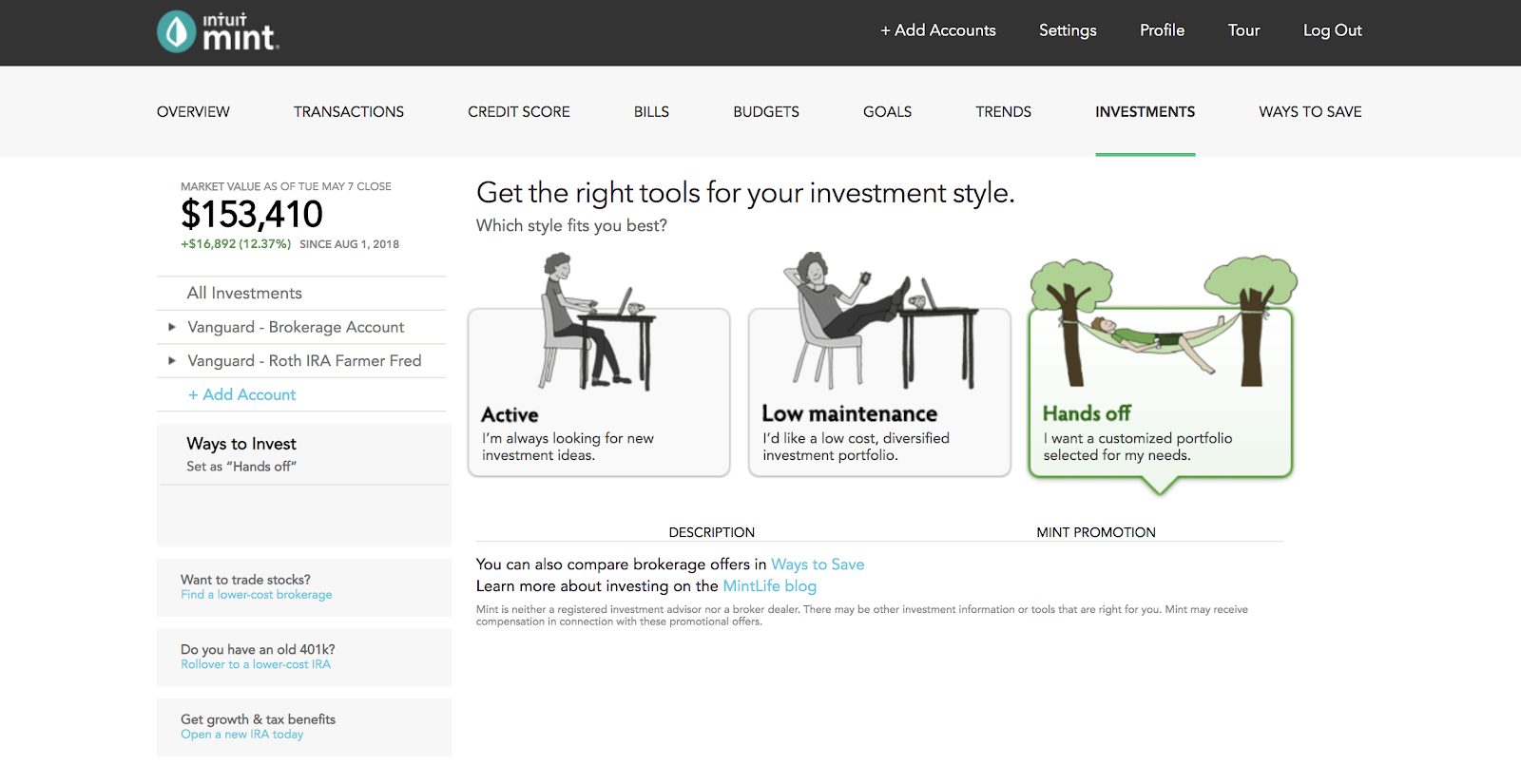

Investment Tracking

How does your portfolio measure against market benchmarks? See your asset allocations along with your portfolio’s overall performance.

Park your 401(k), mutual funds, IRAs, and any other brokerage accounts here. Mint will offer recommendations based on your investing style.

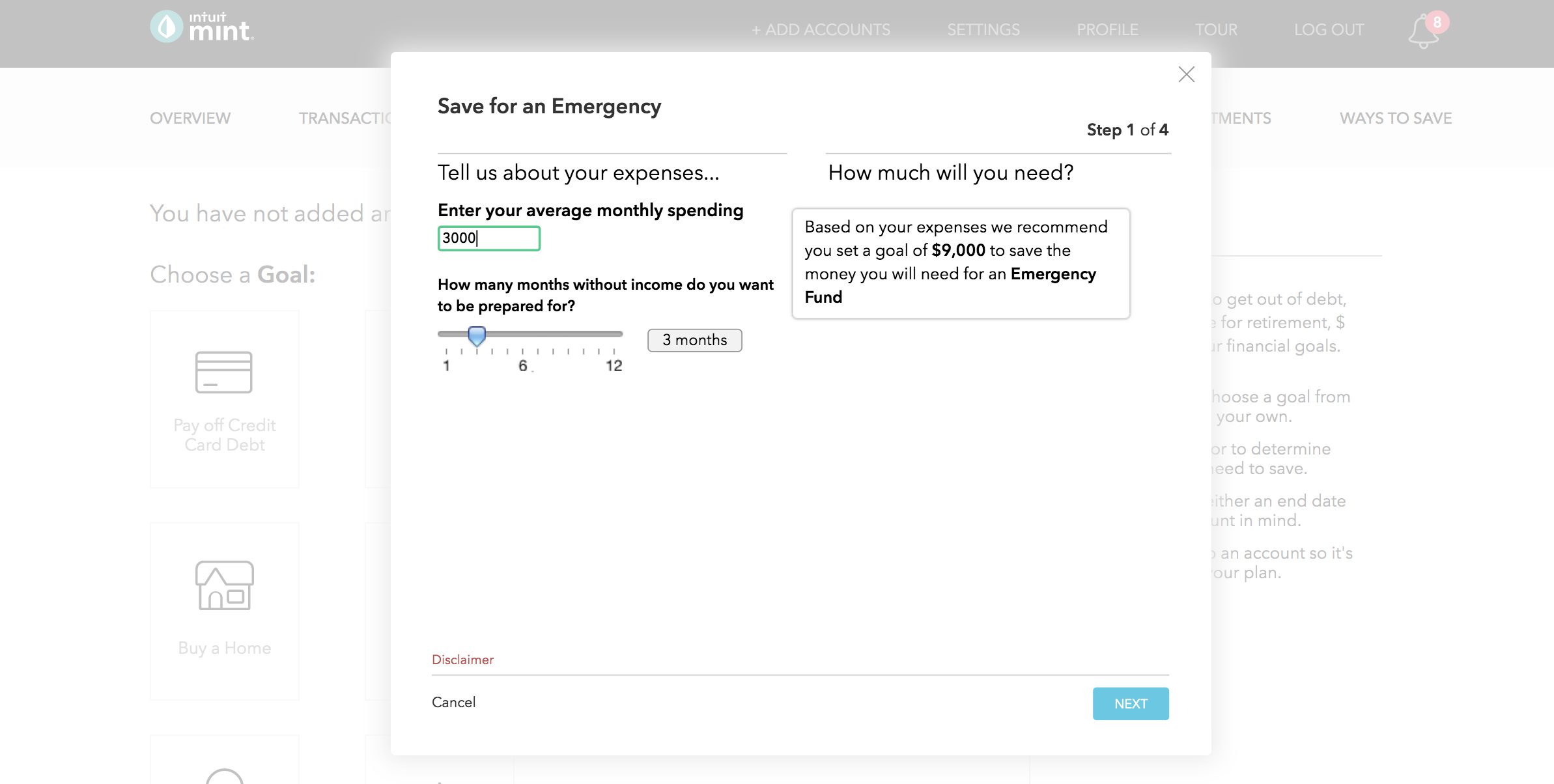

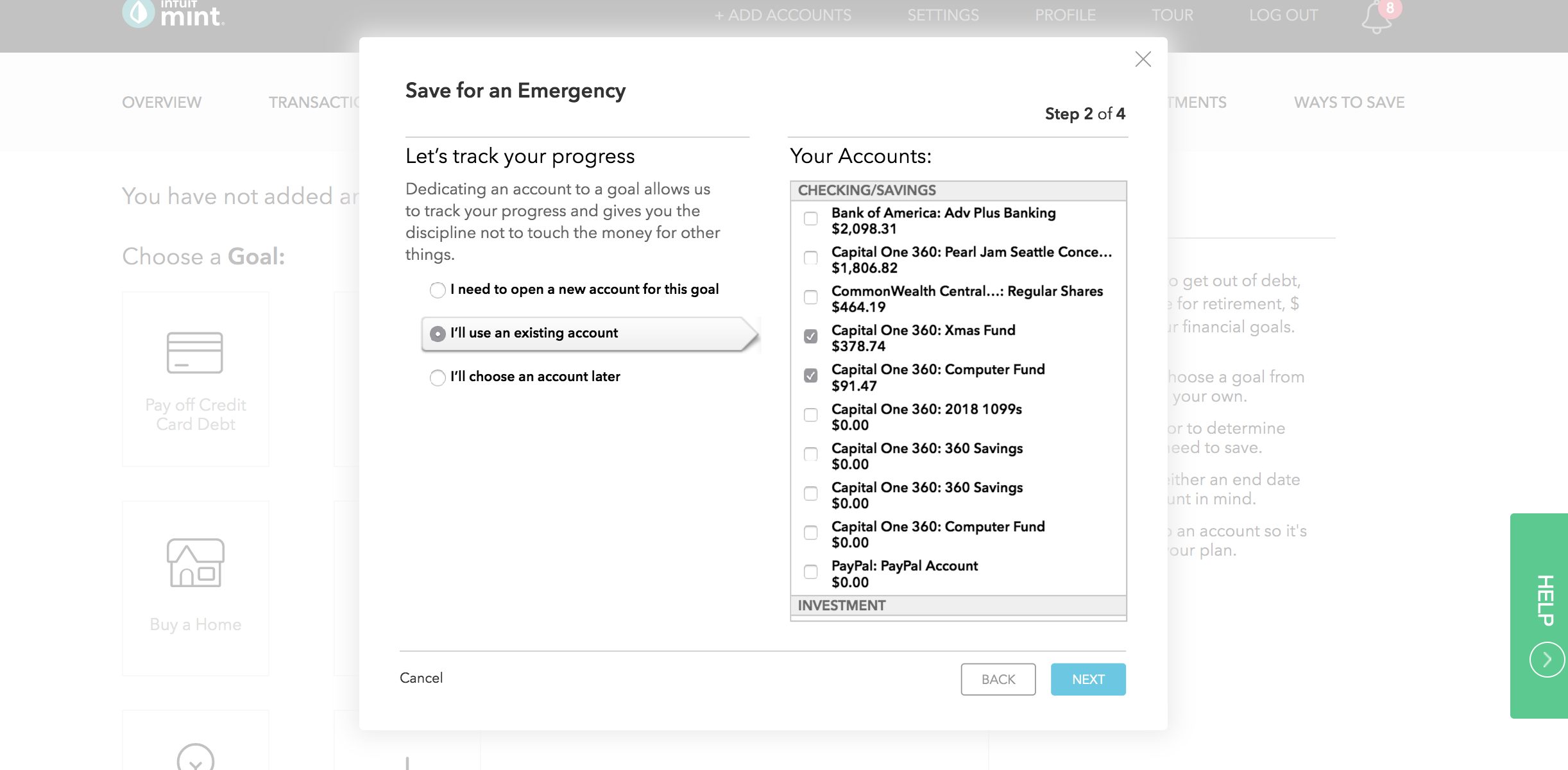

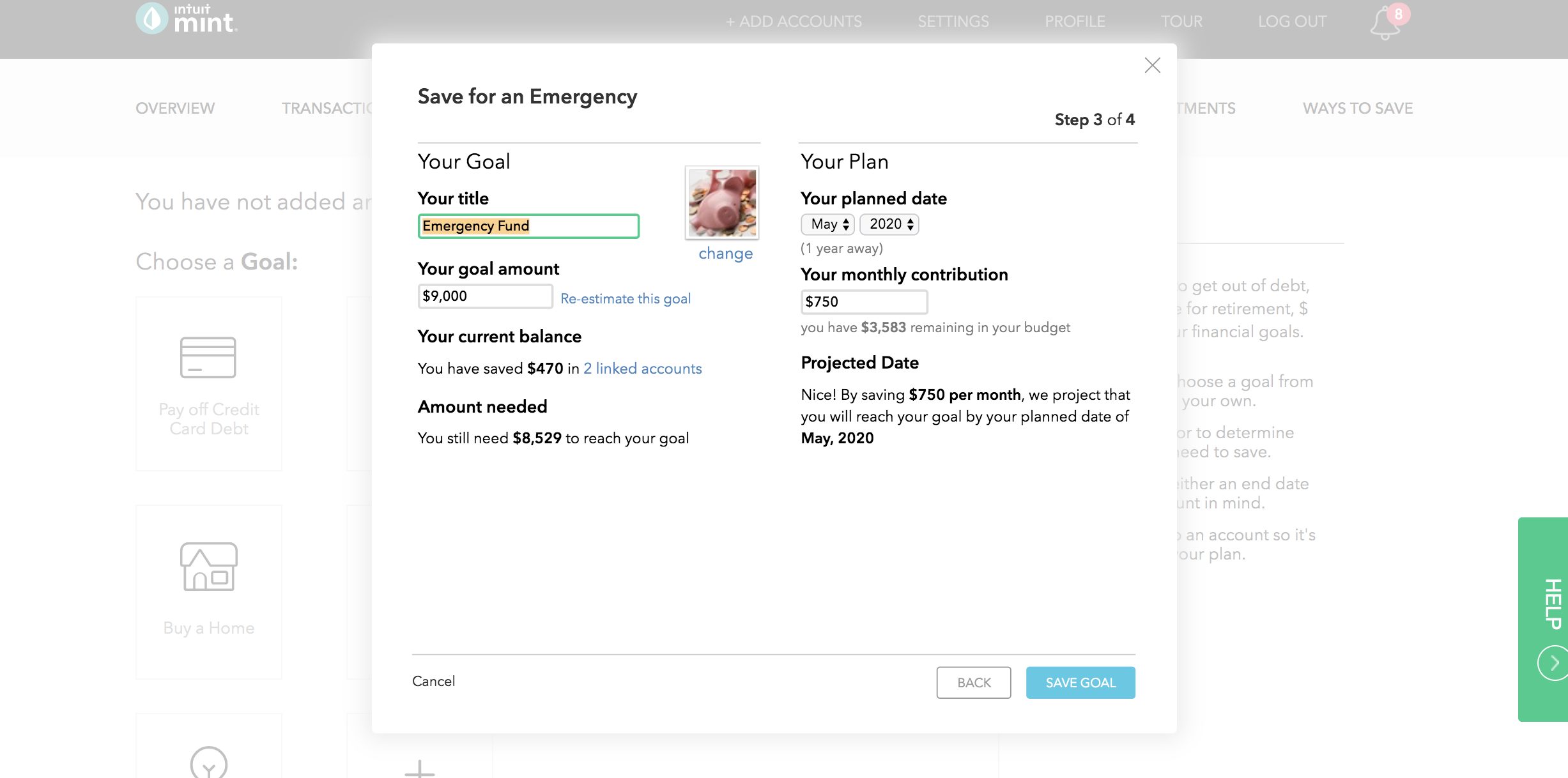

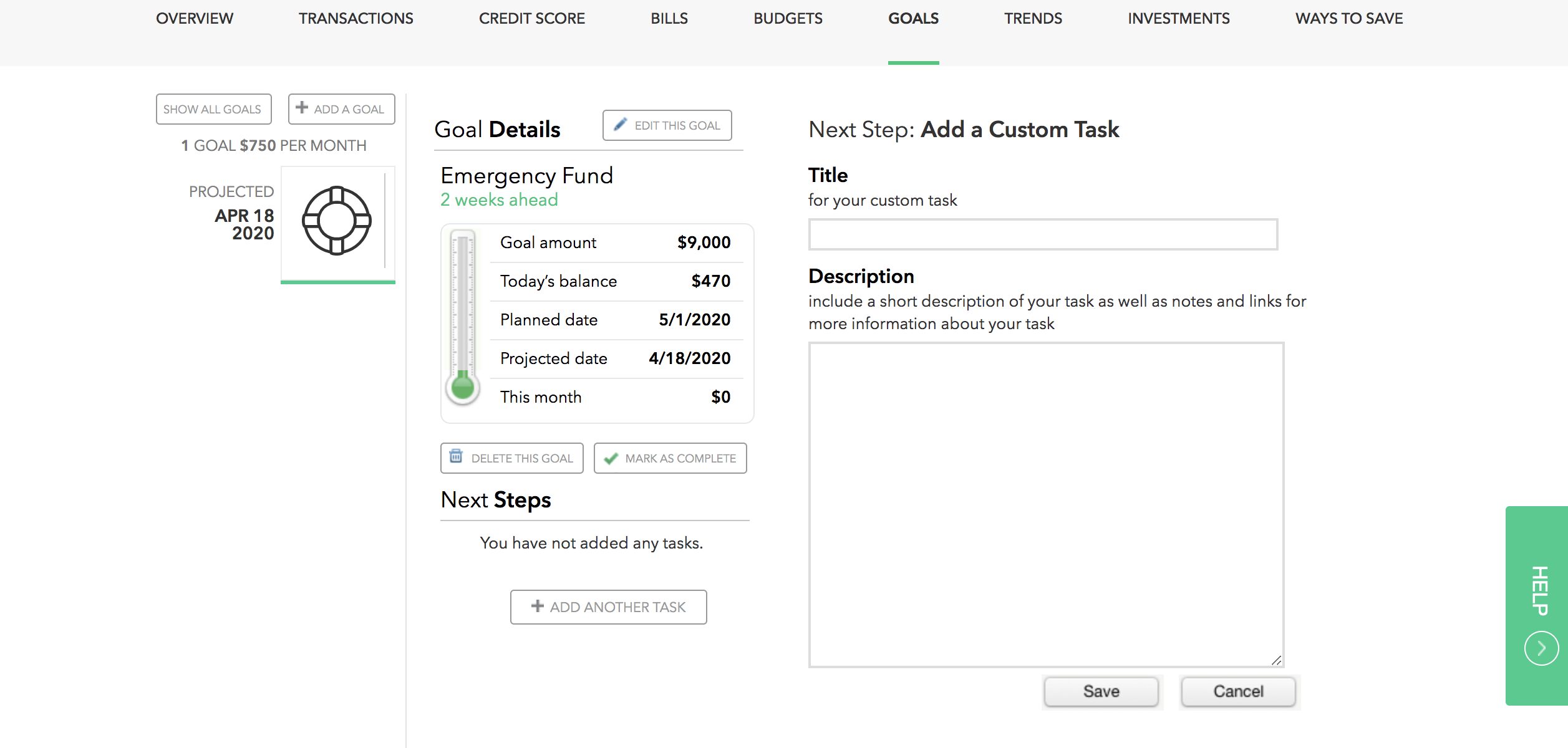

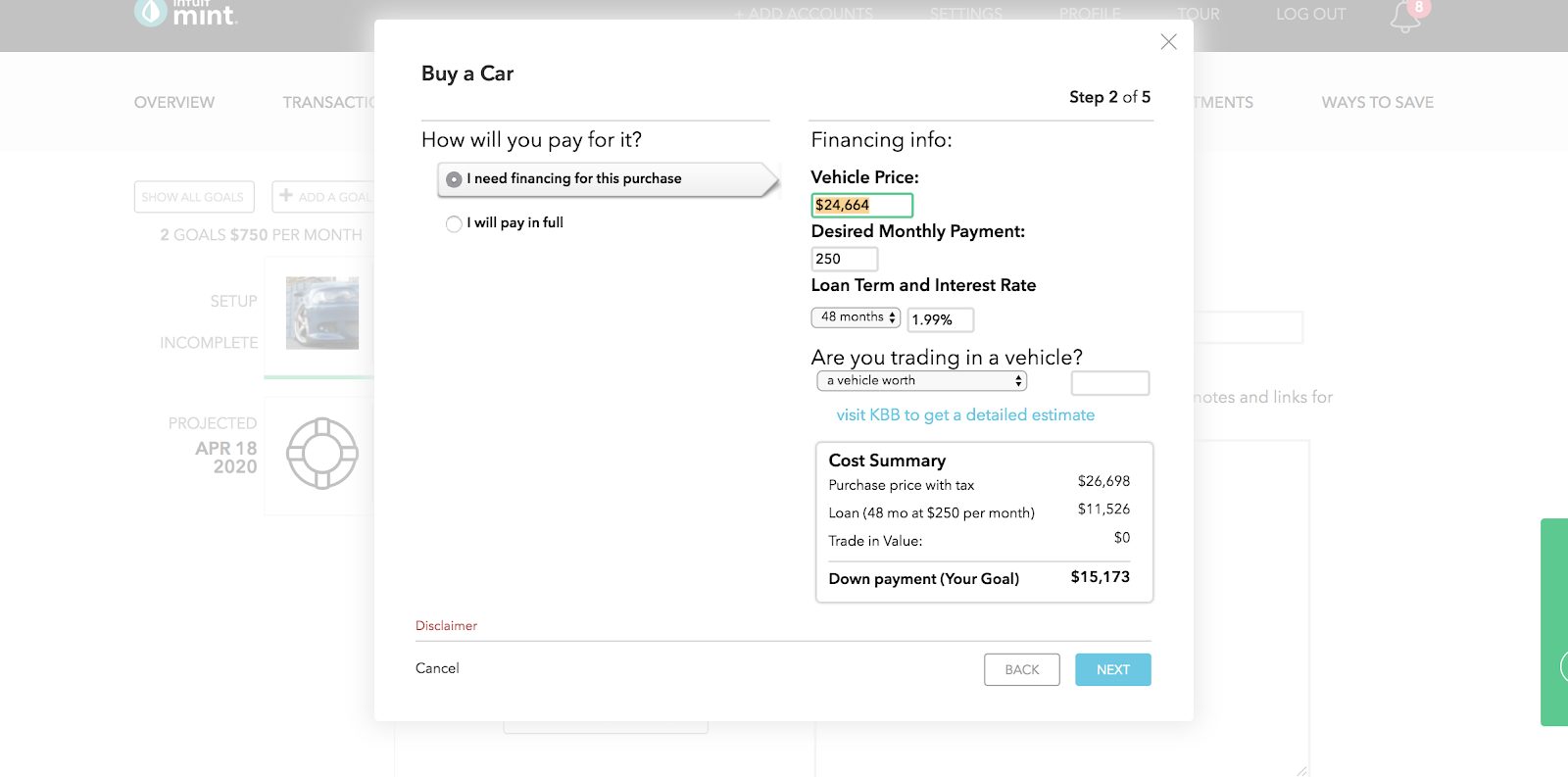

Setting Financial Goals

The type of goal depends on how Mint helps you prepare. For example, saving for a car will look different than building an emergency fund.

The car scenario will ask how you’ll pay for it, the desired monthly payment, loan term, and interest rate. The emergency fund only asks for a target amount and time horizon.

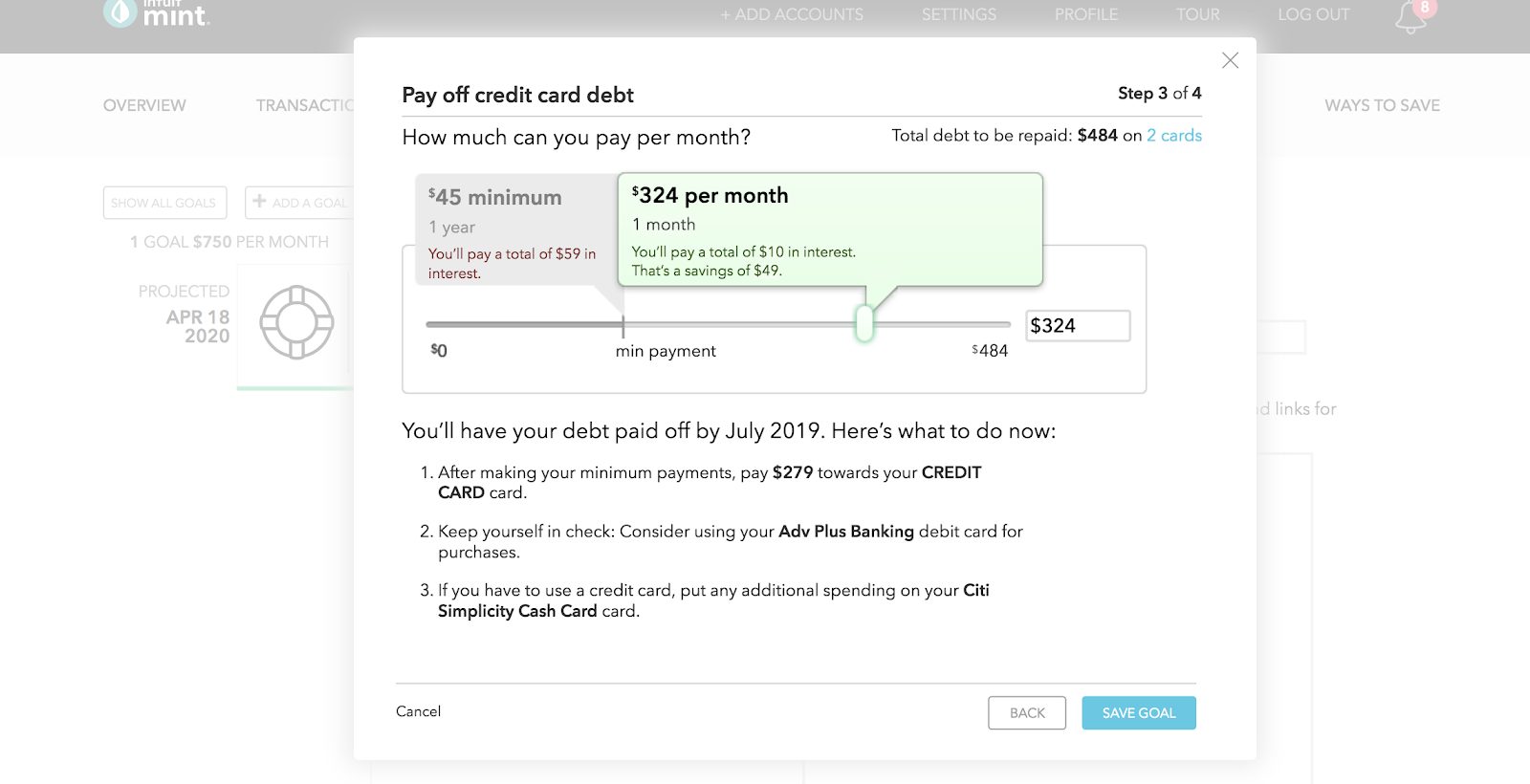

The same holds when paying off credit card debt. Mint runs multiple scenarios on a sliding scale.

See how much interest you’re charged by paying only the minimum due versus a larger monthly payment.

It’s where Mint shines – calculating the interest payments. It’s eye-opening to see how much extra you’ll pay in interest.

Mint realizes each goal is different and integrates these features into their app.

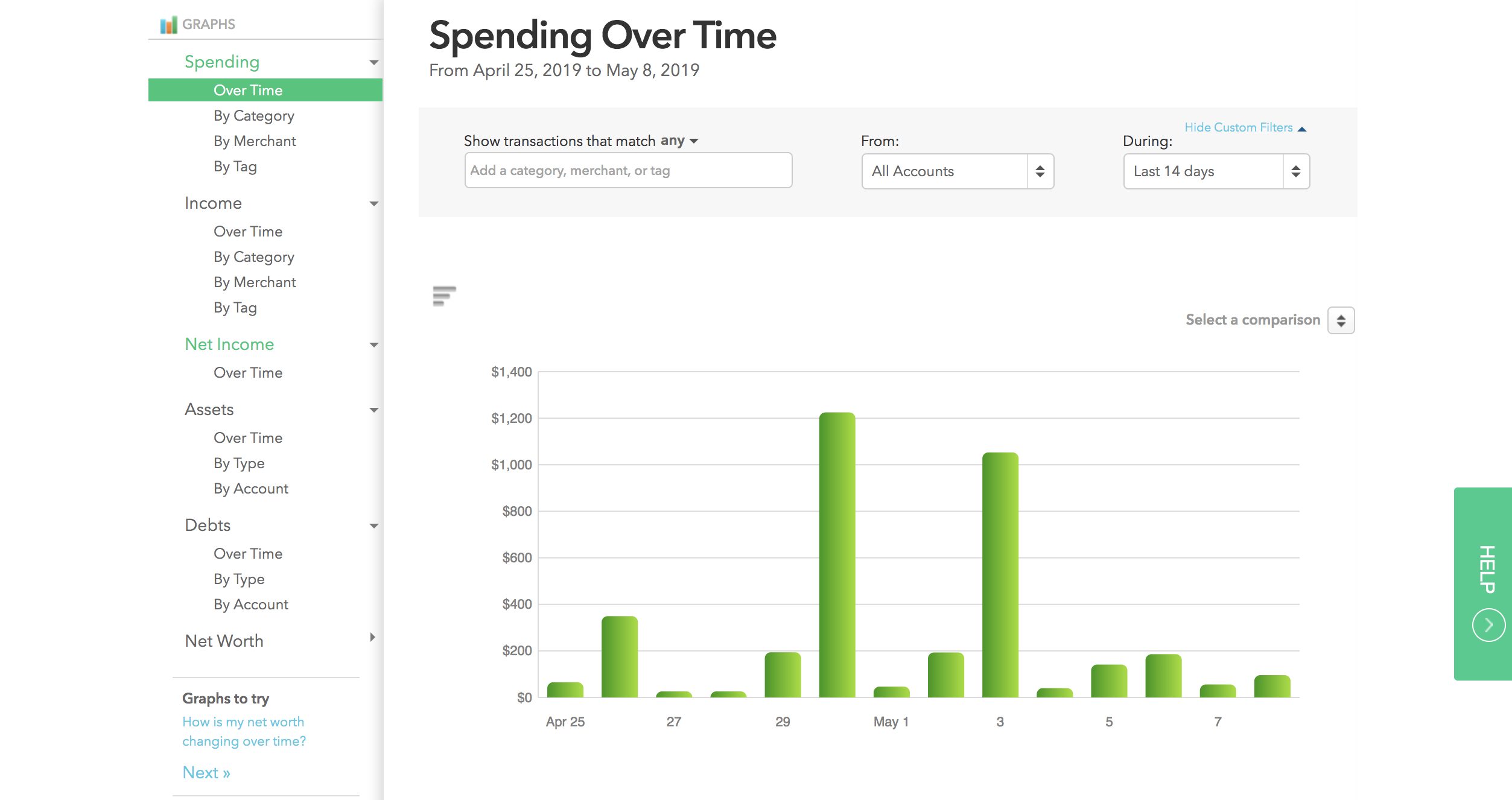

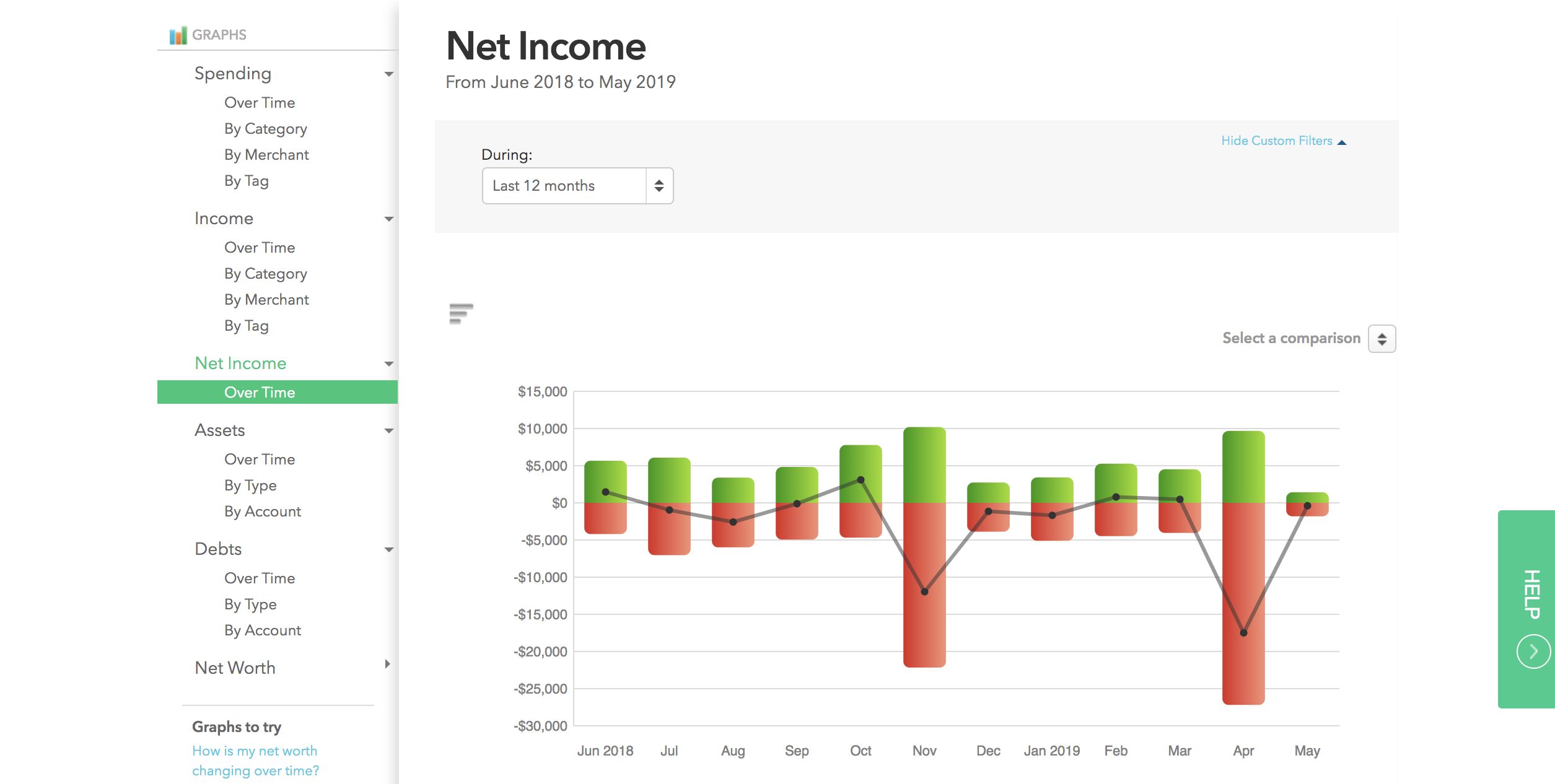

Trend Analyzing

Once your transaction data is in the proper categories, you can dig into where your money goes every month. Trends lets you crunch the numbers on your spending habits, income, assets, and more.

Mint divides Trends in six ways:

- Spending

- Income

- Net Income

- Assets

- Debts

- Net Worth

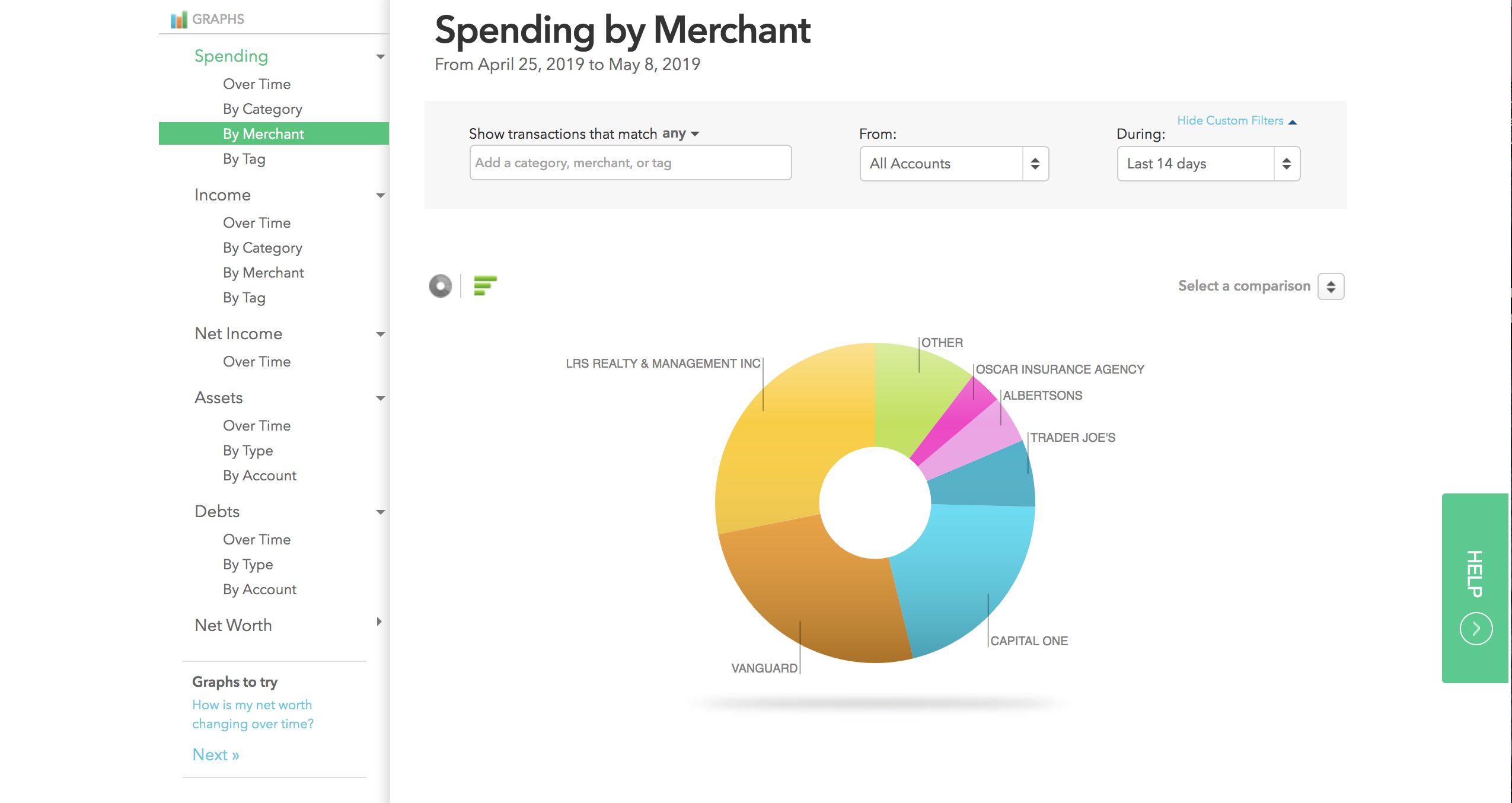

For example, starting with your spending, you can track your purchases over time, by category, by the merchant, or by tags. You set the time frame too.

If you want to see how much you’ve spent in three months dining out, you’ll choose that as your time frame and select category (or merchant if you’re singling out a specific restaurant).

If you think dining out for $300 a month is too much, you can curb your future spending. Perhaps you’d feel better only spending $150 a month and socking away the extra towards retirement.

It’s another area where Mint excels. You can run the numbers on your spending and make adjustments aligned with your goals.

You can track your income the same way. Is it trending up or down? Were you planning on building your client base over the past six months while increasing your income?

Select that time frame and check your progress. Your net income is your income minus your expenses.

This feature is excellent at spotting areas needing improvement (or areas where you’re on track)

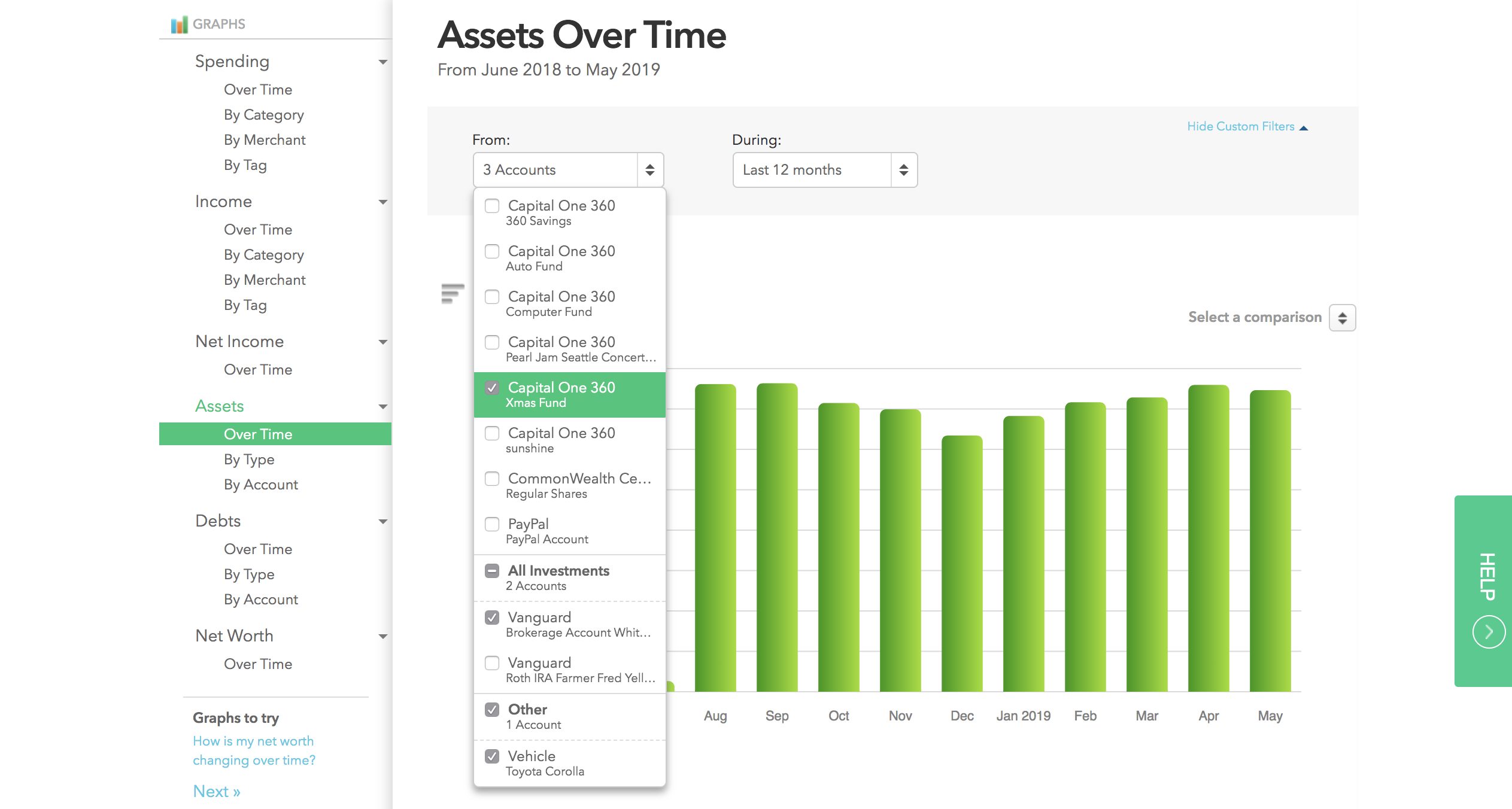

Assets are everything of value you own. Mint will ask you to list any property including homes and cars, brokerage accounts, and other investments.

You can select one account or several to track its performance over time and see if your assets are trending up or down.

Worth Noting

What I like about this feature is the ability to filter by account. You have the option to see the aggregate of all your data or specific accounts.

For example, if you only want to see data from the last six months, you’d tick that box, and Mint will show you a report from that period.

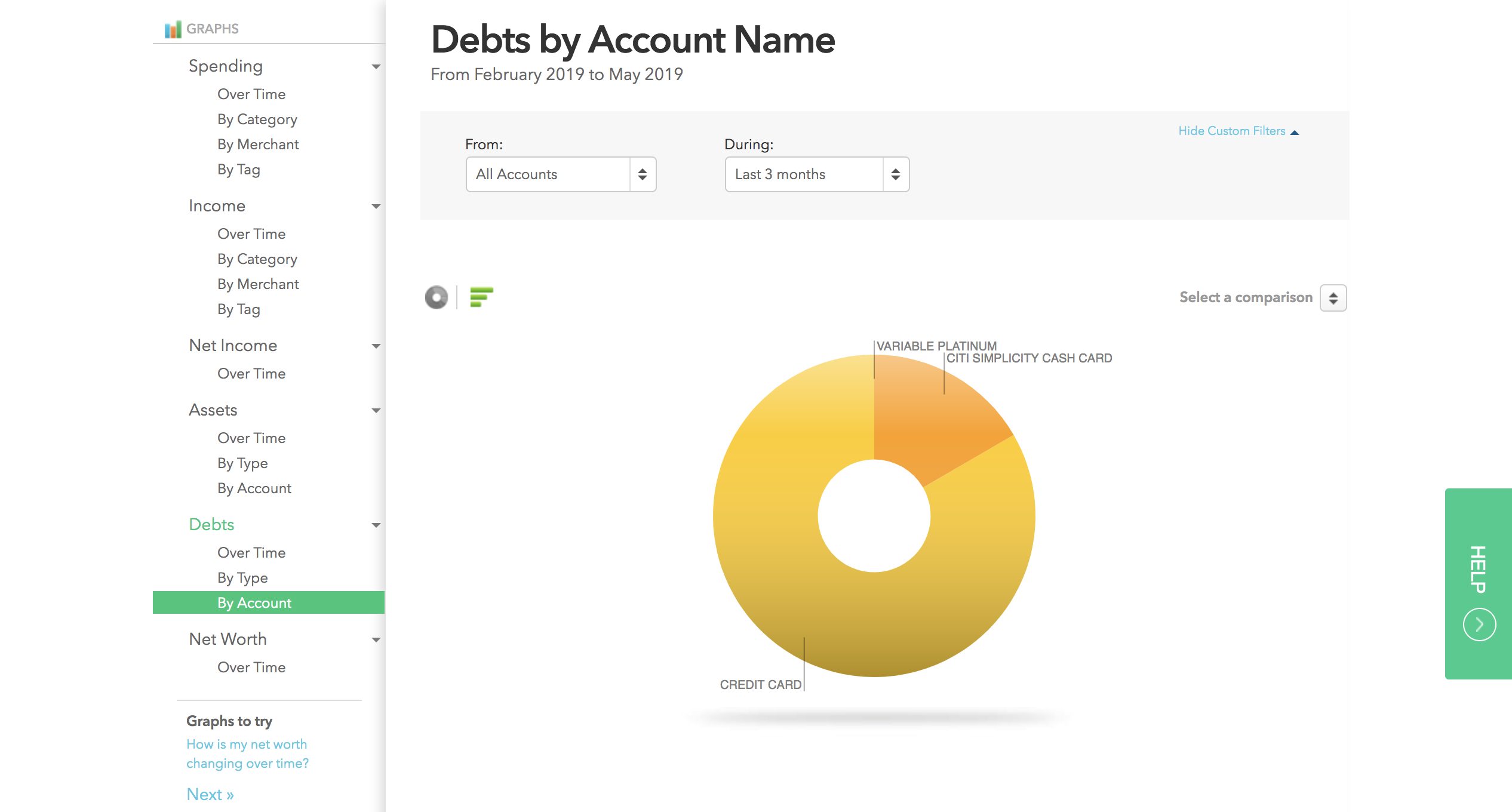

Debts and Net Worth work the same way.

If you’ve got a lot of debt (student loans, credit cards, mortgage), you can divide it up by account, type (loan, credit card), or overtime.

Net Worth is what you want trending up. If it’s not, Mint points out areas needing improvement. It’s an indicator of how well you’re growing your wealth.

Ways to Save

Mint isn’t shy about offering ways to save. You’ll find them either through your spending habits or an entire selection of ideas at the upper right-hand corner of their page.

Will all of their suggestions be appropriate for you? No.

However, it serves as a great starting point. Click on any one of the categories at the top. Find ways to save in the following areas:

- Credit Cards

- Personal Loans

- Investments

- Banking

- Student Loans

- Auto

- Home

- Life Insurance

One drawback here is Mint only offers suggestions through their partners. For example, in the Investments category under Brokerage, you’ll only see a few suggestions.

And there’s no mention of top

It pays to do your homework when exploring their recommendations. They won’t always be a perfect fit.

Mint Resources & Tools

The one area where Mint is lacking is with Customer Support. It’s only available in the form of a chat window, and they have no phone number.

There is a brief customer support page containing the answers to common questions, but not much else.

Helpful Tool

Its Loan Repayment calculator helps determine your monthly payments for various loan types. If you want to learn more about paying off your debts, it’s easy to use.

You’ll enter your loan amount, term, interest rate, and Mint tells you how long it’ll take you to repay along with the final amount.

Blog

However, their blog does provide users with many articles covering wide-ranging topics, from saving to money etiquette to investing advice.

Mint’s robust selection of reading materials has plenty to offer the curious. I think providing users with personal finance education should be a staple of any money-related site.

Security

Mint is a product of Intuit (the folks behind TurboTax and

Ample security features, including:

- Multi-factor authentication

- Receive codes via text and email confirming your identity

- Create your security questions

- Receive notification of account changes

The mobile app has a four-digit code and is touch-ID capable. You also can either remove mobile access or delete your account in case your smartphone is lost or stolen.

Did You Know?

Mint is “read-only.” There’s no transferring of money. Because there’s no money exchanged, all Mint can do is download your transactions.

A hacker would only be able to view your transactions without withdrawing.

Mobile App & 3rd-Party Integration

Mint does have mobile app access through both iOS (including Apple Watch) and Android devices.

You can also integrate your Amazon store card with Mint by signing into your Amazon account and register your card to connect.

Is There Anything Better Than Mint?

Mint isn’t the only budgeting app on the market. I’m a fan of anything that helps improve your financial situation. If you find their offerings disagreeable, there are alternatives.

Cost

Free

Apps

iOS/Android

Budgeting Style

Category Tracking

Reporting

Spending, Income, Debts, Assets, Net Worth

Investing Tools

Performance Analyzation, Allocation, Value, and Stock Market Comparisons

Alerts and Reminders:

Email Reminders and Alerts, Goal Reminders within the App

Security:

Encryption, MFA

Cost

Free

Apps

iOS/Android

Budgeting Style

Business Style

Reporting

Income, Expenses, Investment Performance, Holdings, Allocation, Net Worth

Investing Tools

Retirement Planner, Retirement Fee Analyzer, Investment Checkup

Alerts and Reminders:

Email Alerts

Security:

Encryption, MFA

YNAB vs. Mint

You Need A Budget is an award-winning digital budgeting tool, has an excellent user experience, and a Four Rules budgeting method that works.

Users pay an annual subscription fee, but they offer you a 34-day trial to test drive their software.

You can visit

Mint vs. Quicken

Quicken is another application that lets you see your entire financial picture in one place. You can categorize your expenses, manage bills, and track your investments.

It’s a bit more robust as it lets you do things like pay bills and provides retirement planning advice, which Mint doesn’t do.

Like

Check out our detailed article comparing Mint vs YNAB vs Personal Capital vs Quicken.

Personal Capital vs Mint

While Mint focuses heavily on budgeting, Personal Capital focuses on investment optimization.

You can still monitor your budget through Personal Capital, but I’d recommend it as a service to use when you’re ready to move beyond only budgeting.

Visit Personal Capital here. Or read our Personal Capital review.

Mint FAQs

Before getting any product, I’m always curious to learn the common questions people had before buying (or downloading the free app). The most talked-about related to Mint’s safety, costs, and data.

Is the Mint App Safe?

As mentioned earlier, the Mint app is secure. It features multi-factor authentication, a four-digit code, and is touch-ID capable, making it extremely difficult to access your information.

And, because Mint is “read-only,” a hacker couldn’t access your bank account to make withdrawals.

Is Mint Really Free?

Mint is free to use (which is why it has millions of users). You only have to download the app through the Apple store, Google Play, or create an account using your desktop computer.

Does Mint Sell Your Data?

Yes, Mint sells your data. However, it’s an anonymous pool, so it protects your identity. Mint is in a unique position to observe consumer trends which is how it can generate revenue from interested third parties.

Because Mint makes money through referrals to its partners on the site, advertisements, and account upgrades (as well as selling your data), it lets them keep the app free to use.

Is Mint Right for You?

Your financial goals and needs should dictate which type of budgeting tool you’ll need. If your interest is strictly focused on budgets and tracking income and expenses, Mint will work fine.

Consider the following before creating your account.

What’s to Like

- Free to Use: For the number of features included in the app, you’re getting a wealth of financial information at no cost. If you’re a beginner and want to get a clearer understanding of where your money goes, it’s a solid service.

- Free Credit Score: It’s an excellent way to monitor your credit with an explanation of how and why you earned your number. If you’re in the process of rebuilding credit or searching for a low-interest rate loan, tracking your score will serve you.

- Budgets & Goal Setting: When saving for any goal, it’s good to know the numbers. Mint breaks everything down for you and differentiates between goals. For example, if paying off debt, it calculates your interest rate and shows you the varying levels of how long it will take to pay it off, paying the minimum versus increasing your monthly payment. It also lets you set spending goals in different budget categories to monitor your cash flow.

- Trend Analyzing: Mint analyzes your data to help you make decisions based on your spending patterns. This feature can help you cut out frivolous spending.

What’s Not to Like

- Syncing Issues between Accounts: There are instances when Mint doesn’t remain connected, and you’ll have to re-sync. It seems to be a constant annoyance for Mint users, myself included.

- Recommendations Limited to Mint’s Partners: You won’t find an exhaustive list of companies covering every category using Mint’s Ways to Save. I’d suggest exploring outside of Mint to find companies that are a better fit for you if you don’t like its recommendations.

- Limited Customer Support: Clicking “Support” on their site gets you a list of troubleshooting articles and accesses their Live Chat window. However, Mint has no phone number or email.

Bottom Line

Will Mint help you save money? It’s a great budget app to have in your toolbox. It includes many first-rate features, like the ability to analyze trends, enhanced goal setting, and bill tracking.

When you coordinate Mint with its provided financial information, your monthly budget may do better. Is it the only app available?

No. You Need A Budget and Personal Capital are two top competitors worth exploring.

Having a holistic financial picture makes managing your money effortless. Mint’s powers primarily lie in the budgeting arena.

Even though you can park your investment accounts with Mint.com, its features are no match for Personal Capital’s wealth management tool.

Something to think about for investors with more extensive portfolios.

However, if you’re looking for an optimal way to track your money, Mint is a solid choice. It’s important to remember that it’s only as powerful as its user.

Merely downloading this personal finance app alone isn’t going to solve your money problems. You’ve got to put in the work. A healthy financial life starts with knowing where you stand.

If you’d like to get your hands on our detailed user’s guide to Mastering Mint and discover more about using it exclusively to manage your finances, click here.