You already know how important finances are to your overall well-being. A large part of that is the biggest purchase you will ever make: a home.

Because this is such a large purchase, most people elect to partner with a lender to help them make the purchase. Unless you’re this guy…

As a rule, if you own diamond-rimmed glasses, then you can clearly pay cash for a crib.

Most of us, however, do not own bejewelled headgear, and need the help of a bank. But what if you don’t qualify for a bank loan? What then?

To help overcome the challenges associated with conventional loans, many people have turned to hard money lenders to finance investments and home purchases.

But, what the fuck are hard money lenders?

Good question! But first, what is hard money?

In essence, hard money is a short-term loan that provides a borrower money that’s secured by property. Even though a lot of people don’t quite understand the mechanics of hard money lending, most have a negative view of hard money loans and hard money lenders.

Hard money is lent out privately outside of traditional banking institutions, oftentimes by private individuals.

With hard money loans, a borrower must go through a private lender and usually has a 12-month loan term. Most people pursue hard money loans to finance things quickly or to secure a loan that would not be approved by a conventional borrower or financial institution.

With hard money, you can pay for a home, home renovation, or other expenses quickly with borrowed capital. The amount you are able to borrow through a hard money loan will vary depending on the value the home, the collateral you can put up, and your credit history.

You can also use hard money loans for real estate investments. If you acquire a home through a foreclosure or a short sale, you may need financing immediately that you cannot obtain through conventional mortgage options.

Hard money vs. soft money

A soft loan has a more traditional structure than a hard loan. Let’s say you want to buy a car and finance it with a soft loan. After being approved, you would be awarded a below-market interest rate and given several years to pay off the loan.

These loans are offered by lending and financing institutions, such as banks and credit unions, and you must have solid credit and suitable proof of income to be approved.

A hard money loan, on the other hand, is granted to a borrower who offers property as collateral. A hard money lender does not rely on credit checks to insulate itself from risk. Instead, it accepts a property to back the loan and will pursue the value in the asset should the borrower default.

One of the primary differences between hard money vs. soft money is that soft loans tend to have much lower interest rates. You may even be given an interest holiday that postpones adding any annual interest rate to the loan for a certain period of time.

With a hard money loan, the interest rate—along with the loan term—is much higher. In most cases, you may have a relatively reasonable interest rate for your loan term, but you will be subject to exorbitant rates if you fail to complete repayment within the designated period.

You also must consider the application process when you’re thinking about hard money vs. soft money.

Securing a soft loan is usually a much more extensive process, as your credit score and credit history are taken into account. Soft money loans can be used to pay for properties with a loan-to-value ratio of up to 90 percent, but you may have to prove that you have between three and six months worth of payments in reserve.

Hard money loan requirements are much less stringent. You don’t need to prove that you have a reserve to cover future payments and your financial history will not be as closely scrutinized. This is because the loan is entirely backed by a physical asset: most often your home.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

What can hard money be used for?

Despite its risks and drawbacks, there are several useful applications for hard money loans. From hard money personal loans to hard money for real estate investors, you can leverage this financing tool to make profitable investment choices and finance large expenses quickly.

Or, to buy those diamond glasses you’ve always been dreaming about!

The most important thing to keep in mind is that hard money loans are specifically suited for investments that will turn a profit quickly, so that you can pay back the loan in a shorter amount of time than you would a conventional loan.

House flipping

For regular readers of Listen Money Matters, you know how much we love real estate.

“Real estate investing even on a very small scale, remains a tried and true means of building an individual’s wealth” – Robert Kiyosaki

For this reason, many creative real estate investors use hard money to help with the short-term funding of deals.

For investors who are interested in purchasing a home and flipping it for profit, hard money is often employed to finance the purchase of commercial and residential properties. The idea is that the property buyer can pay off his or her hard money loan with the profit made from flipping and selling the property.

Imagine a property is sold after a foreclosure or through a short sale. In this scenario, an investor may not have the time necessary to go through the conventional mortgage process and receive funds from a traditional lender.

Hard money loans make it possible for an investor to make this purchase and then take care of any planned upgrades and renovations. Investors can make significant profits off these deals, which enables them to pay their loan without breaking a sweat.

In these case, it’s extremely important you conduct your due diligence.

However, these deals can and do go wrong, leaving investors with a mountain of debt. You have to run the numbers on a property flip before investing in one. Make sure you know as much as possible about a property and what the real cost will be to fix it up.

If you are unsure about an investment property and you have a lot of unanswered questions about its condition, you’re likely better off looking at other investment options.

Property development

Another way that hard money loans can be used is for the development of a property. If an investor purchases a property and is able to build a home in six months, he or she can sell the home for much more than the original purchase price.

However, it’s vital to exercise caution when using hard money for property development and construction, as construction timelines can be unpredictable. If you take on a major development and the timeline is extended by several months in the midst of the project, you may exceed your loan term before the property is completed and can bring in a profit.

Personal loans

In other cases, people are looking for hard money personal loans. These loans may be used to finance a renovation or repair to a home, or pay for an unexpected cost that cannot be financed through a conventional soft money loan.

Even though the people who take out hard money loans are often those who need that capital the most, they are also more likely to struggle with repayment. Be sure to budget properly, and keep track of your finances on a daily basis.

Perhaps you want to take out a hard money loan so that you can improve your home and then refinance it with an improved value.

In this case, you must be certain that the work you have done with your hard money loan is sufficient to raise your property value and give you enough equity that you could pay off the loan after refinancing. A home equity loan would also allow you to tap some of the equity you’ve built up.

Speaking with a local real estate appraiser or broker is a good choice in this scenario.

Even if you simply want to purchase a home, you may turn to hard money to finance your purchase because of less-than-ideal credit history. Foreclosures, defaults, and bankruptcies remain on your credit report for years, and they can come back to haunt you.

If a bank denies your mortgage application, a hard money lender may be your only choice for financing. The rapid turnaround for hard money loans may be tempting, especially if you cannot get approved for a conventional loan with your credit history.

But! They can also be financially hazardous if they are not used wisely.

Pros and cons of using hard money

Below are several factors to consider when it comes to using hard money loans for real estate investors or personal needs:

Interest

The interest rates tacked on to hard money loans are one of the most unappealing aspects of this financing tool. Traditional bank loans are usually offered to financial candidates at low-interest rates, while hard money lenders simply don’t operate this way. By offering to finance for situations that other institutions would deny, a hard money lender justifies interest rates upwards of 10 percent.

Turnaround time

Nobody wants to wait around for financing before they can make a purchase or investment. Hard money loans are processed quickly, and you can receive funds in as little as three or four days. This gives you the freedom to respond to investment opportunities quickly so that you can make the best deals possible.

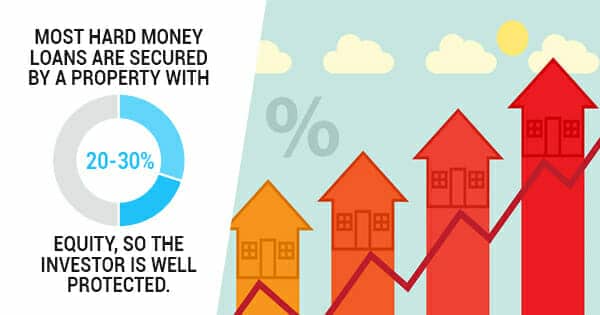

Equity requirements

One of the issues that’s important to be aware of is the standard equity requirement for hard money loans. In most cases, you must prove that you paid a down payment of between 25 percent and 30 percent—or that you have that much equity in the property you are offering up for collateral.

Avoidance of banking limitations

Banks have an obligation to their shareholders to make sound investments and issue loans that have a high probability of bringing in a return. This limits much of what banks can do in terms of financing things like property flips and major renovations. In these cases, it’s nice to work with a hard money lender who will provide capital for many different situations.

Shorter terms

The short terms that hard money loans come with can be brutal if you don’t have sufficient capital for repayment. You have to be sure that you will be able to pay back the loan in time with whatever capital or profits to which you have access.

Fewer requirements

Because of the limited requirements associated with hard money loans, you are much more likely to be approved. By pursuing a hard money loan, you are much less likely to experience the stress and setback of loan denial.

Although there are plenty of hard money success stories, these loans are not for everyone. The most important thing you can do before applying for a hard money loan is to understand as much as you can about this financing tool.

Consult a financial advisor and determine whether hard money loans are truly the right financial option for your needs, goals, and circumstances.

How do hard money lenders work?

In essence, a hard money lender is a private investor who offers rapid loans with property used as collateral. In other words, a hard money lender does not finance loans with money from deposits, like banks and other financial institutions do.

Instead, a hard money lender is an individual or group that uses private money to quickly finance loans. Because hard money lenders use private funds, you can bypass much of the regulatory hurdles that are part of the conventional loan application process.

As far as hard money lender fees, requirements, and interest rates go, it’s difficult to know what to expect.

To give you an idea of the structure of hard money loans, typical terms might include a 5 percent origination fee and a 13 percent interest rate on a loan. These interest rates have more to do with the local loan market than they do with your specific credit score and financial history.

Because a lender has access to such a valuable asset as collateral, it can insulate itself from a lot of risk in the event that you default on your payments.

On average, you will receive the funds from your hard money loan within just a couple weeks of your initial application. It’s this quick funding process and the bypass of strenuous loan applications that make hard money so appealing to so many different people.

When you apply for a hard money loan, you are working with an individual rather than an institution. Having a personal relationship with a lender is important to a lot of people, which is another reason why hard money can be such an attractive option.