We’re all creatures of habit, sticking to routines that can be good or bad for us. The good ones help us grow, but the bad ones? They can trap us in a rut, especially when it comes to money. Bad financial habits can have serious consequences if we’re not careful.

Financial strain has been found to reduce relationship satisfaction, worsen depression, and lead to emotional problems, health difficulties, and poor work performance.

Your financial life is your whole life. That’s not to say that money is everything, but when you’re under financial stress, it impacts every area of your life. The financial decisions you make don’t happen in a vacuum. In many ways, overall well-being is closely tied to your financial well-being. To move forward with your goals and plans that aren’t financial, you have to get financially unstuck first.

You’re familiar with Einstein’s definition of insanity, aren’t you?

The definition of insanity is doing the same thing over and over again, but expecting different results.

Tweet ThisWhen you approach things differently, more effectively, and correctly, the results improve significantly. It’s astonishing how life unfolds when you move away from your usual patterns and embrace new strategies. If you find yourself stuck in a financial rut, there are small, manageable steps you can take to break free. Importantly, you don’t need to spend on an expensive financial advisor to make these changes.

Financial Ruts

Some financial ruts are severe; you find yourself in a challenging personal financial situation, acutely aware of it as you rely on ramen for meals and ponder which utility you can forego. However, not everyone facing financial difficulties is necessarily broke or experiencing short-term troubles. These financial ruts can lead to long-term repercussions that may not be immediately apparent.

Whatever kind of financial rut you find yourself in, these are some of the solutions.

You Live Paycheck To Paycheck

Many people find their finances teetering on a knife’s edge, lacking any form of emergency savings. They operate within such narrow margins that trimming expenses further is simply not an option.

According to a 2023 survey by Payroll.org, 78% of Americans live paycheck to paycheck, meaning their income barely covers their expenses.

While some splurge on big-ticket items, many Americans struggle to save due to a hidden culprit: small, frequent purchases. Daily coffees, subscriptions, and impulse buys can unknowingly drain accounts. Combined with rising living costs or stagnant wages, these “little things” add up, making saving, investing, and financial security a challenge for a significant portion of the US population.

The solution is to pay yourself first. A percentage of every paycheck, ideally 20% goes first into savings or investments.

One strategy is to prioritize saving by paying yourself first. Allocate 20% of each paycheck directly into savings or investments before handling any other financial obligations. If you’re questioning where this 20% will come from, the answer lies in adjusting your budget. By reducing expenditures on non-essential items, you can easily free up the required 20%. This straightforward approach ensures consistent saving and investing towards your future, all without the complexity of financial expertise.

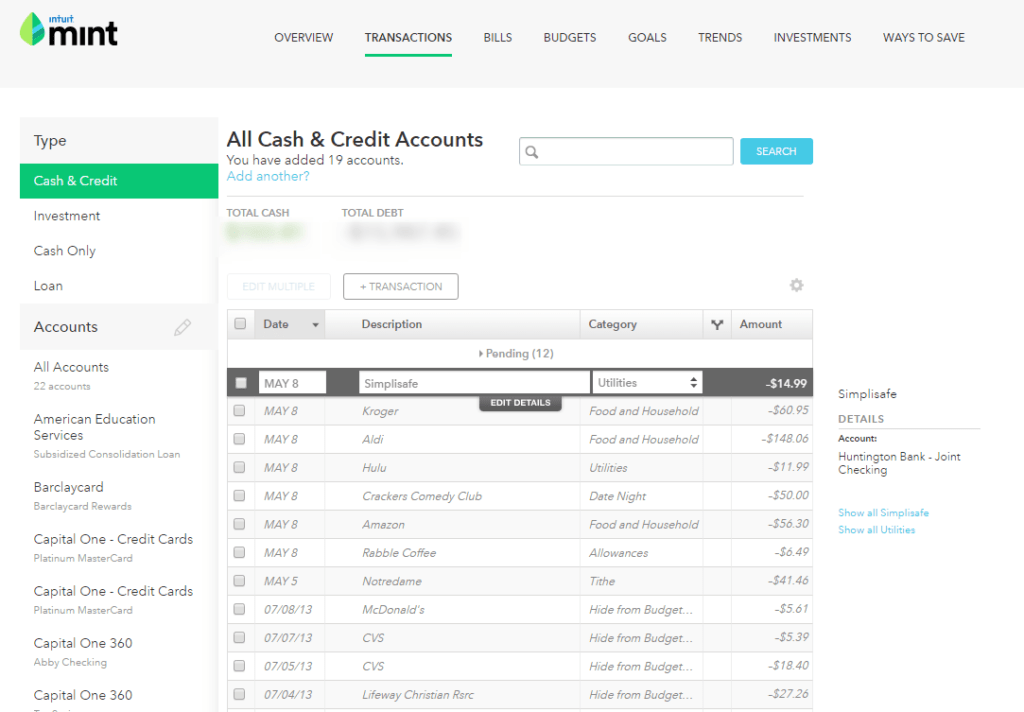

You’re going to find that money by creating a Mint account.

Mint is our favorite budgeting tool because it’s free and easy to use. Connect your financial accounts and Mint will pull the transactions and categorize them although you may have to recategorize some of them.

Mint will tell the tale.

An excellent free budgeting tool. I use it, and if you're getting started, you should too. If you don't track your spending, you'll never know where you're wasting money.

You Overspend

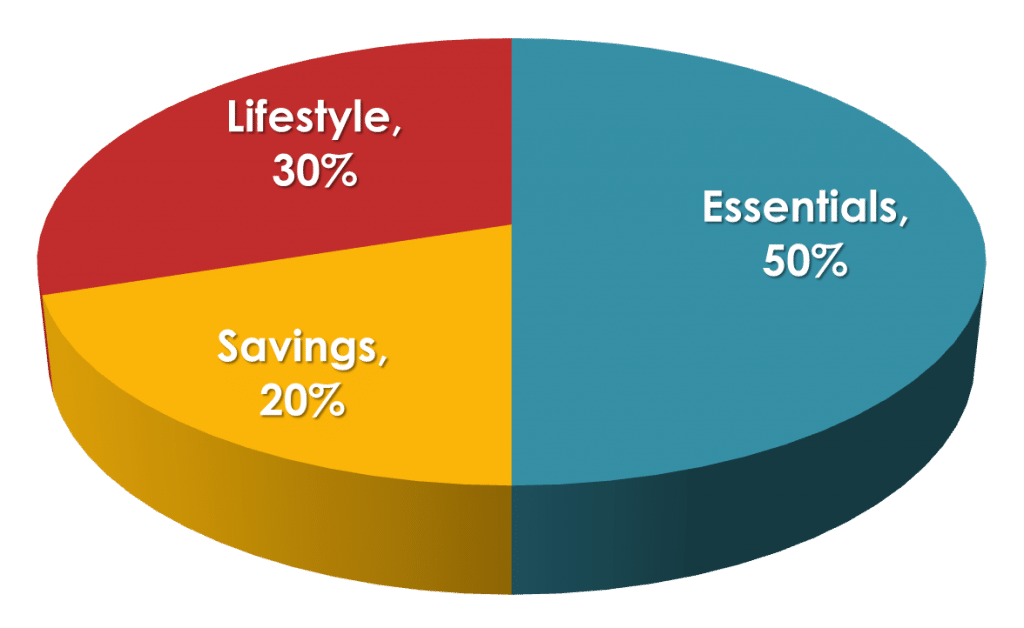

Mint will give you a new perspective on your spending, but understanding where your money will go is just the beginning. To maximize its benefits and escape the paycheck-to-paycheck cycle, you will need to also use it for budgeting. We recommend the 50/30/20 method for its simplicity.

It can take time to get into the habit of staying on budget, especially if your overspending is not just a mindless thing but rooted in something more profound. But there are a few easy things you can do right now to cut spending pretty painlessly.

Cushion is like having your own financial, personal assistant. The Cushion app automates the process of identifying and negotiating refunds for bank and credit card fees, such as overdraft, late, and monthly service charges. Using artificial intelligence, Cushion seeks to recover disputable fees on behalf of users, aiming to save them money and enhance their financial management through insights into their spending habits.

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Services like Billshark, BillTrim, and Hiatus can negotiate better rates on your cable, cell phone, satellite TV and radio, internet, and home security systems. No comparison shopping and no waiting on hold trying to get through to a human on the phone.

You Don’t Invest

Maybe you don’t live paycheck to paycheck. Maybe you have a 12-month emergency fund and coffee cans loaded with cash buried in strategic locations. You don’t spend more than you make, you don’t have credit card debt, and you paid off your student loan years ago. Sounds great, but you are not done.

If you keep all of your money in cash, you have two problems. Inflation is working against you, and compounding interest isn’t working for you. Do you know how you can fix that? By investing.

Starting to invest might feel like a huge deal, especially if you’re pretty good with money but find the whole thing a bit complicated. Don’t let that scare you off, though. There are tons of resources out there to help you figure it all out. Sure, some pros might charge you for their advice, but there are also plenty who offer tips for free. And don’t forget about all the great books and workshops that can give you the lowdown on investing smartly.

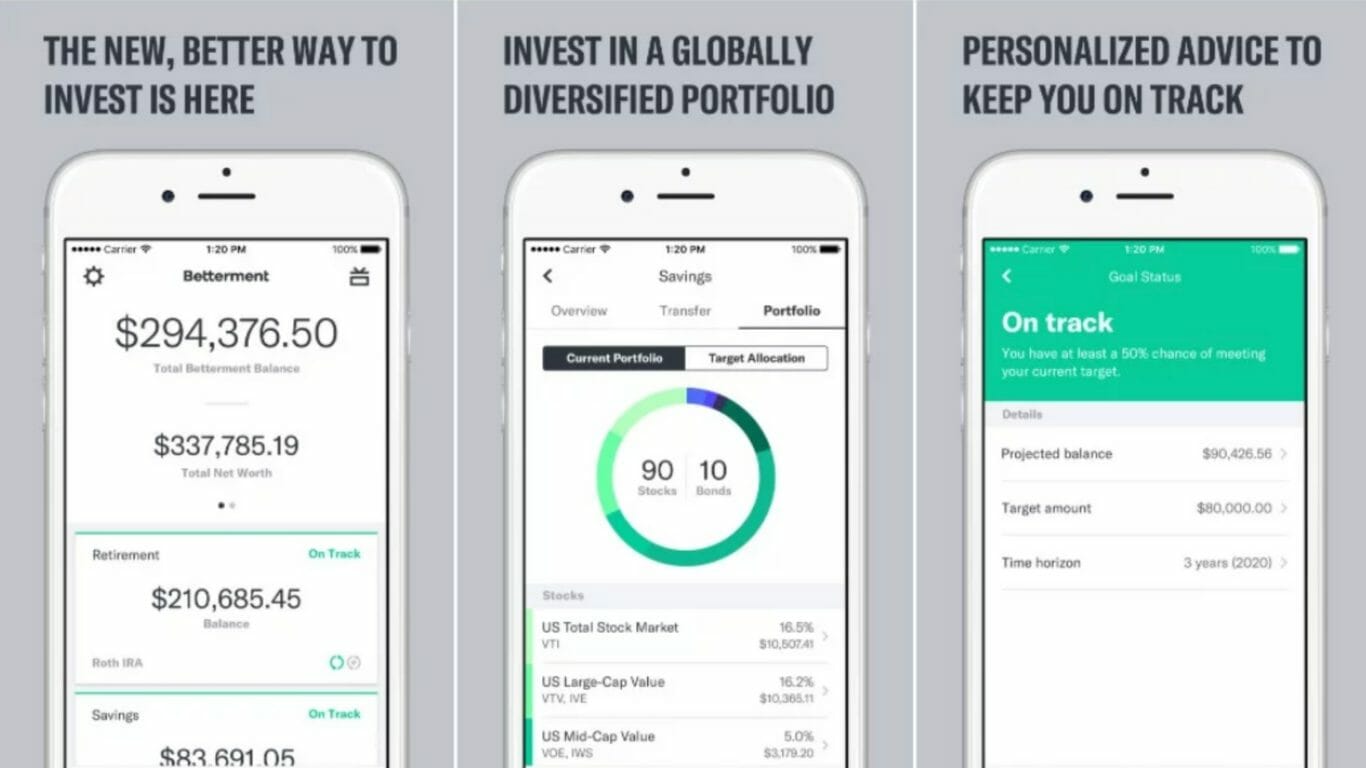

Investing for the long term can be a profitable endeavor. You don’t require extensive financial education, insider knowledge, or a large sum of money to become a successful investor. With just $1, five minutes, and an Internet connection, you can open an account with

For those of us without high six-figure incomes or trust funds, regular and long-term investing is the key to building wealth and achieving financial security. There’s just no other way around it – investing is a must.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

You Don’t Ask For More

When was the last time you had a raise? After the blood bath caused by the Great Recession hit the United States and much of the world, people who still had jobs were not about to rock the boat by asking for a raise.

While acknowledging your worth is crucial, navigating a salary increase requires planning and preparation.

- Know Your Worth: Go on comparison sites like Glassdoor and PayScale to see what those in your area, field, or job in similar-sized companies are making. You could be grossly underpaid or making about what you should. Either way, you need to know.

- Sing Your Praises: What have you done to deserve a raise? Come armed with a list of your achievements since your last raise, even better if these achievements can be expressed numerically, ie, “I brought in $X in new business”, “I saved X% on the firm’s travel expenses”, etc.

- Negotiate: The ability to negotiate doesn’t come naturally for all of us, but you can fake it til you make it. One of the best episodes we ever did, was on how to negotiate.

- Be Ready To Walk: If you don’t get what you want (within reason) and you know the company is in a position to give it to you but won’t, you have to be ready to move on. That brings us to our next point.

You Love Your Comfort Zone

You can step out of your comfort zone and embark on a job search to find a better gig. And finding a better job is the way to improve your financial situation, more so than asking for a raise.

We interviewed a guest about the FIRE movement, and she talked about how geographic arbitrage was a big part of achieving FIRE and allowing her to live the kind of life she wanted, a life not so focused on money.

You Don’t Hustle

Everyone should do something that brings in some side income, yes the infamous side hustle. Few of us are so busy that we don’t have enough time to do some hustling. If you want to stop being stuck in a rut, a new hobby that brings in some money is an excellent way to do it.

There are all kinds of side hustles, so there is something that will fit everyone’s skills and free time. You can answer surveys on mobile apps like Survey Junkie and InboxDollars. You can start a blog or a podcast. Drive for Lyft, and rent out your place (or someone else’s) on Airbnb.

The right side hustle can give you a sense of purpose, help pay healthcare costs and student debt, and pad your retirement savings.

There is no bigger rut than going to work for someone else, coming home and watching TV, going to bed and then getting up the next day and the next and the next to do the exact same thing.

Take a break from that and do something for yourself.

You Never Learn

Some people scrape and claw their way out of thousands of dollars of credit card debt and then start charging up their balances again. Some people file for bankruptcy more than once. We all make mistakes, so there’s no need to feel bad.

Failing to learn from your mistakes, particularly those that are financially painful, goes beyond merely being stuck in a rut; it amounts to self-sabotage. This issue cannot be rectified simply through financial literacy or coaching. Often, the issue isn’t the credit cards we carry, but the mindset and behaviors driving our financial decisions.

A Sticky Situation

Being stuck in a rut is a temporary state, yet it’s possible to remain there for an extended period. Ruts are peculiarly comfortable; they might not represent the ideal situation, but their familiarity is what truly defines being stuck. It’s the comfort found in the known that keeps us there.

Sometimes attaining the deepest familiarity with a question is our best substitute for actually having the answer.

Be someone for whom familiarity isn’t good enough. Be someone who searches for the answer. Curiosity may have killed the cat, but the cat died knowing.

In “Unshakeable: Your Financial Freedom Playbook”, Tony Robbins shares tips from financial gurus like Warren Buffett, Alan Greenspan and David Swensen, on the rules of the financial game, the key players and their agenda, and how the average person can ride the financial storm to build your financial freedom.