Throughout history, examining past economic downturns has provided valuable insights into potential outcomes of future recessions. Reflecting on these patterns can offer some indication of what we might expect when the next downturn occurs.

Even in the face of adversity, opportunities can arise from chaos. The best chances for growth often sprout from the most challenging conditions, both personally and economically.

Many of us were not in a position to take advantage of the opportunities revealed during the last recession, the Great Recession.

The Great Recession began when the U.S. housing market went from boom to bust in 2007, and large amounts of mortgage-backed securities (MBS’s) and derivatives lost significant value.

Interest rates during a recession are typically lowered, the stock market drops and real estate prices slump. All of these things create opportunities for us to make money or save money.

Naturally, during a recession, there are abundant opportunities for missteps, frequently driven by fear, leading to hasty decisions without proper foresight.

So let’s take a look at a few dos and don’ts during a recession.

What Is a Recession?

The textbook definition of a recession is:

Two consecutive quarters of negative economic growth as measured by the GDP or gross domestic product.

Gross domestic product is the total monetary value of all the goods and services produced by a country over a set period. GDP represents the health and size of the economy.

Other factors can be indications that a country is in a recession, including a high unemployment rate, trade wars, the stock market, industrial output, and credit availability.

Since 1900, America has averaged a recession every four years, and since World War II, the average recession has lasted about eleven months.

Eleven months is a misleading number. It’s skewed high due to the Great Recession, which lasted 18 months.

Are We In a Recession?

We are not yet in a recession, but according to ycharts.com, the probability of a recession by May of 2024 is 70.85%.

Like recessions, corrections are not uncommon. There have been 36 corrections in the S&P 500 since 1950 of at least 10%, or about one every two years.

Are we headed toward a recession? Probably. And even before the pandemic, there were signs a recession was looming.

But we’ve been through recessions before and come out the other side, so there is no need to panic. Expansionary monetary policy can help us through the coming recession.

Expansionary Monetary Policy To the Rescue

We know the government is often inept, but when it comes to something it cares about, the economy, it can get things right through fiscal policy.

What is Expansionary Monetary Policy?

Expansionary monetary policy (EMP) occurs when a central bank uses its available monetary policy tools to stimulate a country’s economy. Doing so increases the supply of money, lowers interest rates, and increases aggregate demand.

Aggregate demand, also called domestic final demand, is the total demand for goods and services in an economy, the demand for a country’s real GDP.

EMP increases growth as measured by GDP. It devalues currency, which decreases the exchange rate.

This is the opposite of a contractionary monetary policy. Expansionary monetary policy curbs the contractionary phase of the business cycle.

But because central bankers don’t have a crystal ball, EMP is put into place only after a recession has started it; it’s a reaction, not a preemptive measure.

How Expansionary Monetary Policy Works

In the United States, the central bank is the Federal Reserve. One EMP tool that the Fed employs is open market operations.

It buys U.S. Treasury notes from member banks with credit created out of thin air. The Fed is increasing the money supply, by essentially printing money.

Replacing the banks’ Treasury notes with credit means the Fed has given the banks more money to lend out. To lend out the excess cash, banks lower interest rates.

Borrowing money for a mortgage, a car, or a student loan is now cheaper. The interest rates on credit cards are also reduced. These lower interest rates increase consumer spending and economic activity.

Business loans are cheaper, too, so companies can afford to hire additional employees, which lowers unemployment and puts money into these employee’s pockets, allowing them to spend more.

This tactic helps stimulate demand for goods and services and can increase economic growth.

The Federal Open Market Committee can also lower the fed funds rate, which is the rate banks charge one another for overnight deposits.

Banks are required by the Fed to hold a certain amount of their deposits in reserve at the local branch of their Federal Reserve office every night. Banks with more cash than they need to lend the excess cash to banks that don’t have enough and charge the fed funds rate.

When the Fed lowers the target rate, it’s cheaper for banks to maintain their reserves, so they have more money to lend out. The result is lower interest rates for customers.

The Discount Rate

The next tool in the tool belt is the discount rate; the interest rate the Fed charges banks that borrow from its discount window. Banks don’t like to use the discount window.

Banks primarily use the discount window as a safety net to address temporary cash shortages and support central bank policy, but its higher cost and potential negative signal make it a last resort option.

The fourth of the monetary policy tools is lowering the reserve requirement. This does increase liquidity immediately, but member banks must adhere to a lot of additional policies and procedures.

We can expect to see some of these tools deployed to prop up the economy and spur economic growth during a recession that is potentially headed our way. That’s what the Fed can do for us, let’s see what we can do for ourselves.

Fiscal flexibility that’s funny, free and delivered weekly.

Recession Dos

Some of us are scared to make any money moves when we’re in an economic downturn, but doing nothing can be the wrong decision if it means failing to take advantage of an opportunity.

Refinance

The Federal Reserve last raised the Fed Funds Rate of interest rate to 5.50% in July 2023, the 11th time during 2022-2023. Post-pandemic, inflation soared, prompting the Federal Reserve to raise interest rates to mitigate inflation.

During a recession, when interest rates are typically lower, it’s cheaper to borrow money, even money you’ve already borrowed. You can take advantage of lower interest rates by refinancing your mortgage rates, auto loans, and student loans.

When should you consider refinancing? If the rate you can get is half a point to one point lower than your current rate is the rule of thumb.

It might not sound like much, but when you’re talking about thousands of dollars over decades in the case of a mortgage, a 0.5% or 1% cut in your interest rate can save you thousands of dollars over time.

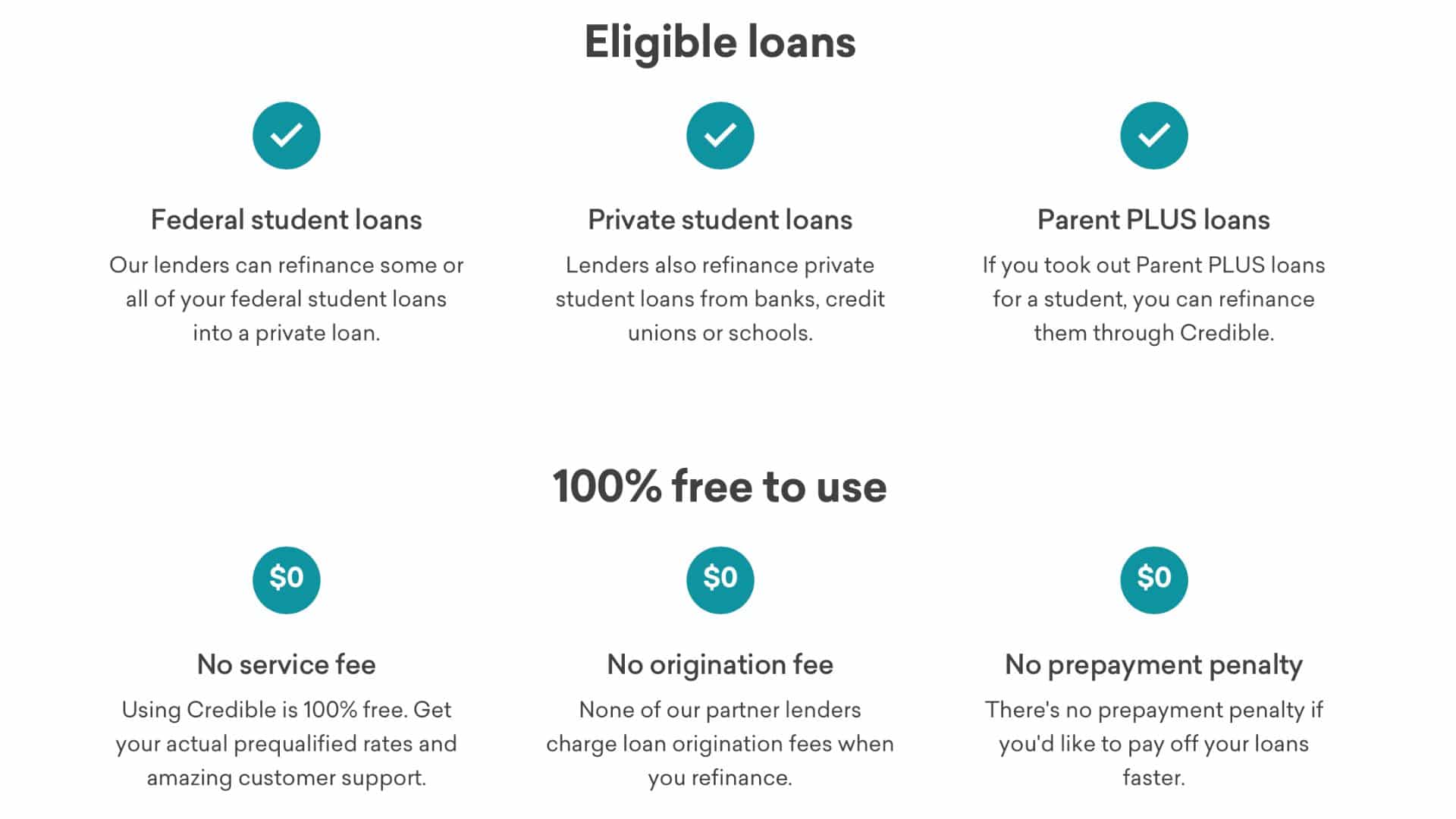

How do you know your new rate – If you’re considering refinancing your student loans, Credible allows you to enter in some basic information and check your rate without impacting your credit score.

Credible allows you to shop for rates from several different lenders who will refinance your student loans and mortgage without impacting your credit score.

Upgrade offers personal loans and auto loan refinancing, and you can check your rate with no effect on your credit score.

There can be costs associated with some types of refinancing, so be sure to look at more than just the interest rates when you’re shopping around.

Pay Down Credit Card Debt

The annual percentage rate, APR on credit cards, is not expected to decrease until the Federal Reserve begins to lower interest rates. Rates drop because most cards are variable rates and follow the prime rate. The prime rate follows the Fed’s rates.

As of the end of 2023, the average credit card rate was 20.74%. According to Bankrate.com, there is an expectation that the Fed will implement two quarter-point rate cuts in 2024 and the average rate on credit cards will decrease slightly more than that (so 0.50% or more). How aggressive should you be in paying off credit card debt to take advantage of these lower rates once available?

While carrying a credit card balance generally isn’t advisable due to interest and credit score impacts, it might be acceptable for short-term financing with 0% APR offers or during unforeseen emergencies, but only with a solid plan for swift repayment.

Given today’s high-interest rates, if you have some measure of job security, now is the time to get aggressive with your credit card debt. At the very least, take the money you’re saving by not being able to go out and put it towards the credit card debt.

Invest

What does master investor Warren Buffett tell us about investing?

Be fearful when others are greedy and greedy when others are fearful.

Tweet ThisWhen the U. S. economy starts to tank, unwise investors panic and start selling their stocks. It’s a mistake because the only rule when it comes to investing is “buy low, sell high.”

- When to Invest – You can’t time the market, but you can invest set amounts at regular intervals. This is called dollar-cost averaging and it can help you manage marketing timing risk and stick to your investment plan.

- What should you invest in – For new investors, index ETFs (exchange-traded funds) make sense. When you invest in an index ETF, you are investing in a specific market index, offering broad diversification.

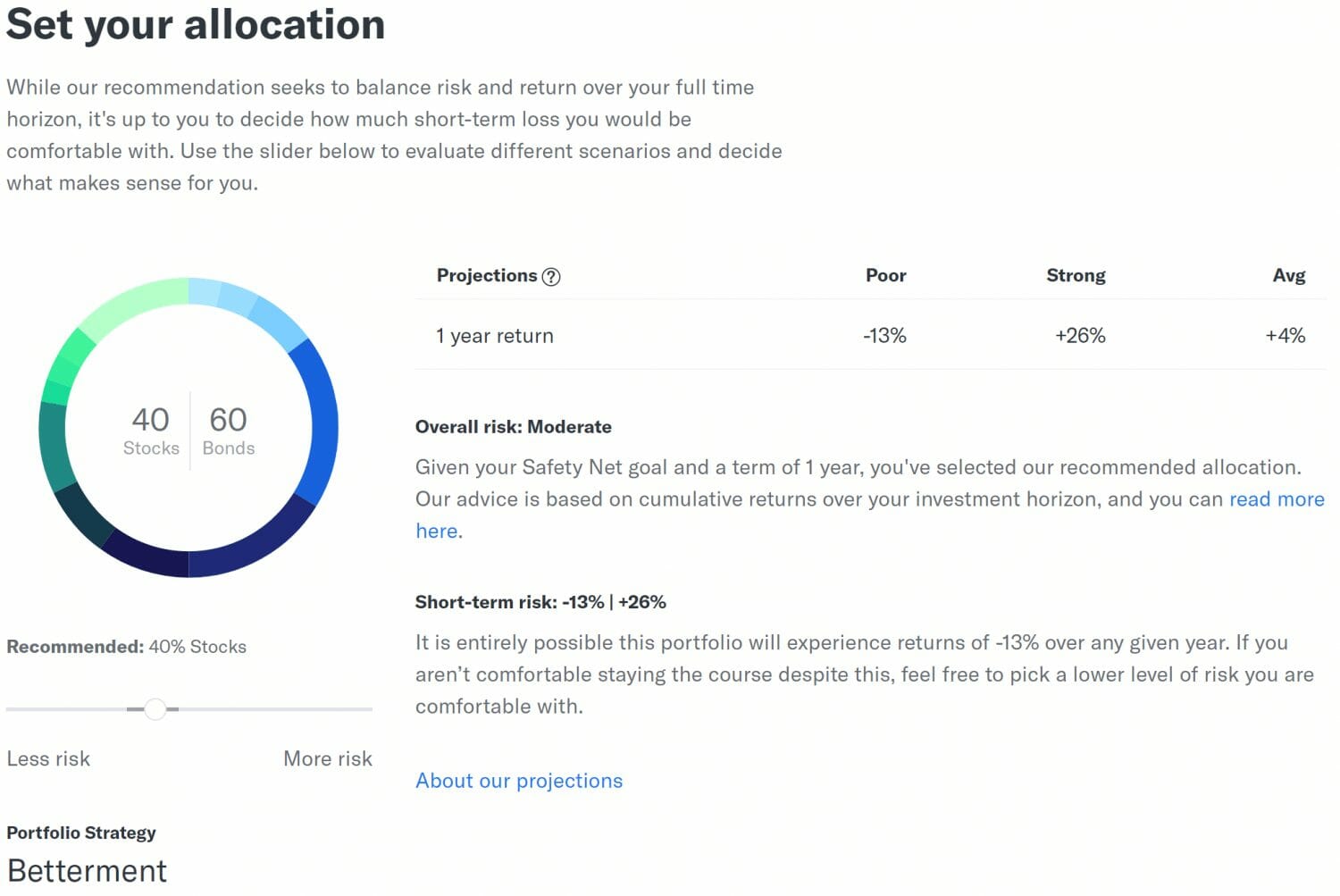

- Set your asset allocation – An asset allocation is a mix of investments (stocks, bonds, cash, etc.) and risks (aggressive to safest).

Cut Back

Recessions can hit your wallet hard. Whether you’re saving for a house, or just need a rainy day fund, you might need to trim the fat from your budget. Look for ways to cut back on unnecessary spending, like that daily latte habit.

Regularly checking your budget helps you catch these little leaks before they sink your ship. This way, you’ll be more prepared to weather any financial storm.

A few ideas to save money

- Minimize how many times you go out to dinner, out for drinks, or to the movies.

- Scale back on your vacations.

- Change your shopping habits.

- Are you still getting a fun subscription box or boxes?

- How many streaming services are you subscribed to?

- Try comparison shopping for major purchases like rental insurance or cell phone plans.

Cushion can help you simplify your bills. Cushion is the easiest way to organize, pay, and build credit with your existing bills and Buy Now Pay Later. Use that extra money to invest.

Update Your Resume

Updating your resume during a recession is important for staying competitive in a challenging job market. Even if you still have your job, it could change. An updated resume ensures you’re ready to seize new opportunities and allows you to quickly respond if you lose your job.

A recession is an excellent time to update your resume and reconnect with the professional contacts that you might have lost touch with.

And it works both ways; when you reconnect, you might find that you’re in a position to help someone who needs it.

Recession Don’ts

While recessions can be daunting, proactive steps can significantly improve your financial well-being. Here are some crucial don’ts to keep in mind during an economic downturn:

Opt for Adjustable Rate Loans

What goes up must come down and vice versa. Interest rates are not going to stay this high forever. If you’re borrowing money or refinancing debt, now is not the time to start thinking about how you refinance your debt.

Now, every rule has a workaround. If you do take a calculated risk and choose an adjustable-rate mortgage and rates go up, you could refinance or refinance again.

Take On Debt

Low-interest rates are an excellent reason to refinance existing debt, but a high-interest rate environment is not the time.

Avoid accumulating high-interest debt, such as credit card debt, as it can become a significant burden during challenging economic times. Prioritize paying off existing debt and be cautious about taking on new loans.

Whatever plans you had, just hold on a little longer. You can buy a house or a car after the recession.

Stay on top of your credit score, a personal loan will have a much lower interest rate than credit cards.

Neglecting Your Emergency Fund

Having a well-funded emergency fund is even more crucial during a recession. This provides a safety net in case of job loss or unexpected expenses, helping you weather financial difficulties.

Ignoring Your Budget

Regularly reviewing and adjusting your budget is essential during a recession. Identify areas where you can cut back on spending, and prioritize essential needs over wants.

Your investments

Selling – Sit tight. This is why we always preach long-term investing. Unless you are near retirement, your money has time to ride this out. Don’t sell!

Investing – A recession might seem like an excellent time to invest in the stock market, and researching stocks will give you something productive to do, but don’t risk your rent money.

Don’t Panic

There is much within your control, and your focus should be on those aspects. Being wise with our finances and health is essential. Avoid making impulsive decisions fueled by fear.

Be Smart, Be Safe

Personal finance and health have a lot of parallels. Neither is easy, but both are simple. Motivation is not enough; you need discipline. It’s (almost) never too late to change bad habits and undo their damage.

Designed to provide a workable, sensible framework for investors, The Five Mistakes Every Investor Makes and How to Avoid Them encourages investors to refrain from certain negative actions