If you have debt, you want to pay it off as quickly as you can. To do that, you may be considering debt consolidation. Not so fast. Don’t make any decisions until you read our complete guide.

We have always emphasized that if you have debt, you need a plan to pay it off. Attacking debt with a plan means you will pay it off more quickly and it will cost you less. Debt consolidation seems like it would be a useful facet of that plan. But is it, or will it cost you more in the long run?

Editor's Note

What is Debt Consolidation?

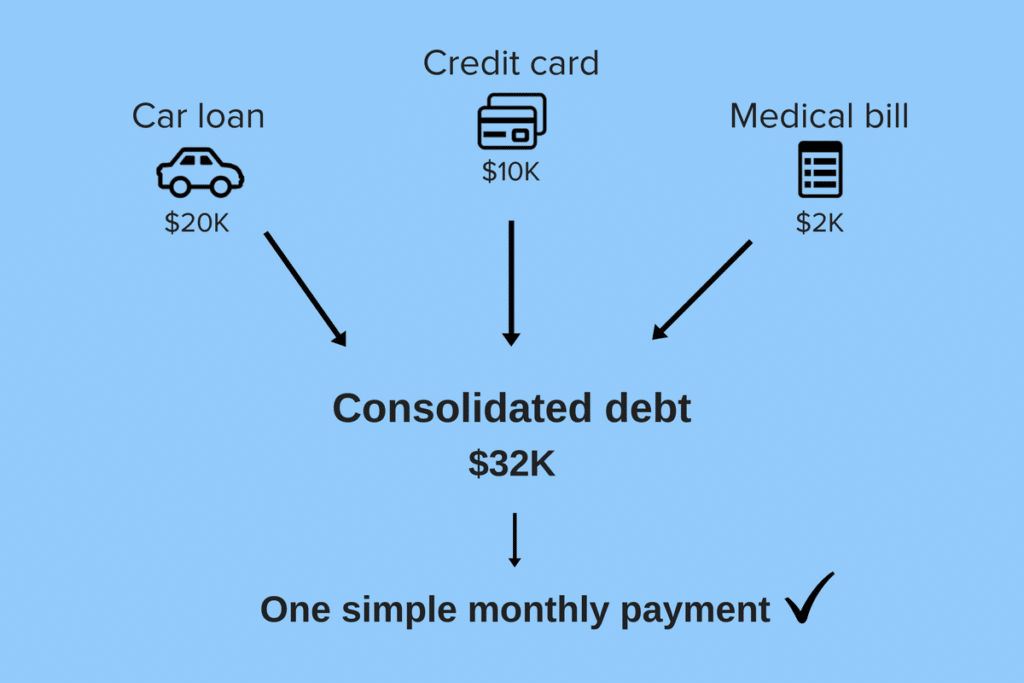

Debt consolidation combines all of your debt into a single monthly bill. It’s a strategy used to pay off unsecured debt including credit card balances, student loans, personal loans, and medical debt.

A debt consolidation loan simplifies your financing. Rather than making multiple payments to multiple creditors, you just make a single payment to the company holding the new loan.

What to Consolidate

Credit card debt is a prime example of the kind of debt you want to consolidate because it has a high rate of interest. The average interest rate on a credit card is 24.61% When your interest rate is so high, it can take years to pay off debt especially if you are only making the monthly minimum payments.

Bankrate.com’s Credit Card calculator can help you figure out how long it will take to pay off a credit card. As an example, if your credit card balance was $1,000 and you paid $30 per month at 24.00%, it would take you 4.67 years to pay off your balance! You would have paid $664 in interest on your $1,000 balance (so a total of $1,664).

Forty-three million Americans have student loan debt, and that debt is often spread out over multiple loans and multiple lenders making the payments hard to manage. The numbers vary by disbursement dates, but the federal student loan interest rate is currently between 5.50%-8.05%.

For private student loans, it can run over 14%. Even if your interest rate is manageable, your monthly payments may not be manageable, so you might consider consolidating your loans to lower that monthly payment.

If you have medical debt, you’re not alone. One in four Americans faces challenges in paying their medical bills while this study expects national health spending to reach $6 trillion by 2027.

Medical facilities often use debt collectors to recoup this money, and if you’ve ever been on the receiving end of a phone call from these collection companies, you know how aggressive they can be and how distressing it is.

Unsettled medical debt may result in wage garnishment or even a lien on your home, underscoring the serious consequences of unpaid healthcare bills.

Types of Debt

Debt falls into two categories: secured and unsecured. Secured debt is protected by an asset, which serves as collateral in the event you cannot repay the loan. An example of secured debt is a mortgage on your home.

Unsecured loans don’t have any assets backing them up, so they usually have higher interest rates. Things like credit card debt, student loans, and medical bills are all unsecured debt.

Debt Consolidation Options

The four primary methods of debt consolidation include:

Debt Consolidation Loans: You get one big loan to cover all your smaller debts. This way, you’re left with just one payment to make every month, hopefully at a lower interest rate.

Balance Transfer Credit Cards: Move all your different credit card debts onto one card that has a low-interest rate at the start. If you play your cards right and pay them off fast, you can save on interest.

Home Equity Loans or HELOC: If you own a home, you can borrow against its value to pay off your debts. You could get a lump sum with a home equity loan or a credit line you can tap into with a HELOC. They usually have lower interest rates, but your house is on the line if you can’t pay it back.

401(k) Loans: Borrowing from your 401(k) to pay off debt is like giving yourself a loan. You have to pay it back with interest, but that money goes back into your retirement pot. Be careful, though—if you bail on your job, you might have to pay it all back fast. Plus, you’re missing out on growing that retirement stash while the money’s out on loan.

There are plenty of companies that prey on those looking to consolidate debt. But plenty of reputable companies do it too, some of whom we’ve interviewed and reviewed here at LMM.

Credit Card Debt

If you have credit card debt, consider getting credit consolidation loans at Prosper.

If you’re considering consolidating debt, you may be concerned about not having a high enough credit rating to secure a low-interest rate. However, it’s worthwhile to visit the site and check your rate, as this process won’t impact your credit score.

You may also be eligible for a credit card balance transfer. These cards have an introductory interest rate of 0%. You transfer the balance from your current high-interest credit card to the new card. During the 0% APR period, you can tackle the balance without accruing more interest.

Be cautious, however. After the introductory period ends, the standard interest rate will apply, which might be higher than the rates on your previous cards. To ensure a balance transfer card effectively addresses your credit card debt, it’s crucial to pay off the total balance before the new interest rate takes effect.

Also, be mindful of any balance transfer fees that may be included. Some companies charge between 3% to 5% of the total amount transferred.

Student Loan Debt

If student loan debt is what you struggle with, you can refinance through Lendkey. LendKey’s student loan refinancing program connects borrowers with a network of community banks and credit unions, offering competitive interest rates. Its streamlined platform simplifies the refinancing process, enabling easy comparison of rates and terms from various lenders with just one application.

Medical Debt

If you have medical debt, you can consider a loan with a peer-to-peer lender like

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

What Loan Terms to Look For

The terms are the essential parts of choosing consolidation loans. Consolidating debt does not automatically mean you will get a lower rate of interest than what you currently have. Nor does it mean that you are guaranteed to save money.

The interest rates on consolidation loans can range from 5%-36%! Interest rates on consolidation loans are influenced by factors such as credit score, loan type, and loan term. Higher credit scores typically lead to lower interest rates, whereas poor credit scores may result in higher rates approaching 36%.

When considering debt consolidation, your primary focus should not be on lowering your monthly payments but on minimizing the total interest paid and accelerating the repayment of the loan amount. Treat your debt as an emergency that you want resolved as swiftly as possible.

Is It Smart to Consolidate Debt

The promise of a lower monthly payment can be seductive if you are struggling with debt, but the reason the monthly payment is reduced is that the life of the loan is increased. When that happens, you haven’t saved any money at all, you’ve spent more.

If the number of loan payments increases, you’re paying more money (in interest) because you’re taking longer to repay it.

In this instance, consolidating doesn’t make sense.

While some considering debt consolidation face financial challenges, their reasons can vary. For some, it’s a proactive step to regain control of their debt by potentially lowering interest and simplifying payments. Seeking professional guidance is crucial before making any major financial decisions related to debt consolidation.

Beware of debt consolidation companies making unrealistic promises or requiring upfront fees, as these are signs of potential scams. Genuine lenders will assess your financial background first. Also, be cautious of firms pushing debt settlement plans over consolidation loans, as it could negatively impact your credit score. Always research thoroughly to ensure you’re dealing with a reputable company.

Beware of Fees

Consolidation loans might have start-up fees, origination fees, or charges if you pay them off early. These extra costs can eat into the savings you thought you’d get from a lower interest rate. Always check the fine print and do the math to make sure the loan saves you money.

Debt Settlement

Debt settlement aims to negotiate lower lump sum payments with creditors but comes with risks like no success guarantee, credit score damage, and high fees. It’s a last resort option, best pursued after exploring other debt relief methods. Before engaging with a debt settlement company, ensure they’re accredited and transparent about their fees and success rates.

At worst, some debt settlement companies might just take your money and run. Even in the best-case scenario, your credit score could take a huge hit. Creditors usually only think about settling when your debt is late. These companies collect your cash for a while, then try to make a deal with your creditors using that pile of money.

Credit Cards and Debit Cards

Credit cards provide certain protections that debit cards lack, and activities such as renting a car or booking a hotel room often necessitate a credit card. If your debit card or bank account is compromised, resolving the issue can take several days. During this period, access to your funds will be blocked. Without a credit card, you may find yourself in the position of needing to borrow money from friends or family to cover necessities such as food and fuel.

Do Consolidation Loans Hurt Your Credit?

Debt consolidation can temporarily impact your credit score due to the closing of older accounts and the opening of a new, single account, which might lower the average age of your credit accounts.

Additionally, applying for a debt consolidation loan involves a hard inquiry on your credit report, leading to a slight and temporary drop in your credit score. These factors combined can result in a short-term decrease in your score.

In the long term, debt consolidation can boost your credit score by enabling better debt management and timely payments. Decreasing your total debt and keeping up with payments can gradually improve your score. Despite initial drawbacks, strategic debt consolidation can benefit your credit health over time.

If you’re consistently making late payments or defaulting, the impact on your credit score will be more severe. However, if you’re managing your debts adequately and are considering credit consolidation merely to streamline your finances, it may not be worth the potential drawbacks.

Don’t Take On New Debt

Avoid accruing new debt after consolidating your existing obligations. This might seem obvious, but the act of debt consolidation can have an unexpected psychological impact on some individuals. It creates a false sense of resolution, leading them to believe their financial emergency has passed and their debt is settled.

There is scarcely anything that drags a person down like debt.

Tweet ThisThe debt has not been paid off; at most, it has been managed. There is still outstanding debt. It’s important not to increase it.

Ways to Eliminate Debt

To eliminate debt without consolidation, try a few simple tricks. First, slash your spending and save every penny you can. Consider the snowball method, knocking out small debts first for quick wins, or the avalanche method, targeting those high-interest debts.

Extra cash? Get a side gig or sell stuff you don’t need. Also, chat with your creditors to see if they’ll cut you a deal on interest rates. If things get tough, a non-profit credit counselor can help set you straight without combining your debts.

Make More

Here’s a startling statistic: on average, Americans spend five hours daily watching television. While this leisure time might seem harmless, it’s crucial to reconsider if you’re struggling with debt. Instead, channel some of that time into activities that can generate additional income, helping you tackle your financial challenges more effectively.

Drive for Lyft, babysit with Sittercity, and sell stuff on eBay or Poshmark. Even taking surveys on Survey Junkie can make you some extra money, certainly more than watching television. Check out our list of ways to make money fast.

Ask a Raise

Request a raise from your boss, providing ample evidence to support why you deserve one. Consider working overtime or taking on a part-time job in retail or hospitality during evenings and weekends to increase your income. Additionally, begin exploring opportunities for a new job that offers higher pay.

And all of that extra money goes toward paying back your debt.

Spend Less

Every cent you earn should be accounted for, and you do that by making and sticking to a budget. Our favorite budgeting tool is Mint because it’s easy to use and free. We can help too.

We have episodes and articles on all kinds of ways to save money; saving on food, on fun, on moving, on your apartment. Listen to and read them and follow the advice.

Use tools like Cushion and Rocket Money to save you money. Rocket Money will go through your expenses and find recurring charges like your subscriptions or gym membership.

Improve Your Credit Score

You can actively work on improving your credit score, tracking your progress through platforms like Credit Karma. As your score increases, you can consider revisiting the option of consolidating your debt. Even if debt consolidation isn’t currently on your radar, aiming for a strong credit score is a worthwhile goal.

You can work on improving your credit score. You can watch your progress at Credit Karma. When your score improves, you can try again to consolidate your debt. Even if you are not interested in doing so, having a good credit score is something to aspire to.

“Bad credit can suggest you’re a risky bet. While bad credit may only show the details of how you deal with debt, some will extrapolate the characteristics from your financial life to other situations and assume that your bad credit implies that you may be just as irresponsible driving a car, taking care of an apartment or showing up for a job”, Weston notes.

Spending Habits

Assuming you opt for a reputable company, debt consolidation loans can serve as a valuable resource for climbing out of debt. However, it’s essential to reflect on the circumstances that led to needing this assistance in the first place. For instance, if your debt stemmed from student loans, it might be a one-time occurrence, especially if you don’t plan on pursuing further education.

Before you jump into consolidating that credit card debt, take a moment to figure out how you got there in the first place. Was it unexpected stuff like a job loss or medical bills that maxed out your cards? Or was it more like, those extra shopping sprees or dream vacations that just weren’t in the budget? Figuring out the why can help you avoid a similar situation down the road.

Debt Relief

There is credit counseling available to help you if you feel your financial situation spinning out of control. The National Foundation for Credit Counseling and Debt.Org are worth a look.

The mentioned companies, along with similar ones, can assist in determining the most suitable debt management plan for your needs.

If you don’t control your spending, you’ll remain in debt regardless of your income. We can assist you in mastering money management, building wealth, and attaining financial freedom. You hold the ability to transform these detrimental habits.

Utilize your debt consolidation journey as a catalyst to transform your financial situation. While we all make mistakes, we have the power to learn from them and avoid repeating them. LMM is here to support you every step of the way.

If you’re afraid to open your bills, if you’ve never added up how much you owe, if you can’t even imagine being debt-free, it’s time to join the thousands of people Gail Vaz-Oxlade has helped.

![A Good Credit Score Saves You Money and Here’s How [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2014/07/LMM-Cover-Images-29-768x432.jpg)