Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

No one can accurately predict when a recession will happen. 2023 was a recession fire drill if you will (still waiting). When we understand what a recession is, we can take steps to protect ourselves from the fallout of the next recession.

Everyone reading this will remember the 2008 recession. Some of you couldn’t get a job, some of you lost your job, and some of you even lost your homes. We lived through it once, and we don’t care to repeat the experience.

But the majority of economists (and the eminent Ray Dalio) agree that sooner or later we are due for another recession.

If the weather forecaster told you a hurricane was coming, you would take precautions, wouldn’t you? Of course, you would. This is no different. We know a recession is coming even if no one can tell us exactly when.

A recession will impact different age groups in different ways. For Millenials who finally got a regular, well-paying job after years of being underemployed, a recession could mean layoffs.

For the Gen Xers, life is expensive.

They have a mortgage, a couple of car payments, and kids who will be heading off to college in a few years. The Boomers are looking forward to retirement but worrying if they have enough saved and what a recession will do to those savings.

Whatever camp you fall into there are steps you can start taking now, scratch that. There are steps you must start taking right this second to make sure you come out of the next recession relatively unscathed. And if you play your cards right, you might come out of it smelling like a rose.

The Experts Agree

In the most recent Statista.com posting regarding the probability of a recession, they show a 62.94% probability that a recession will occur by December of 2024. Net, net, they are predicting that we’re less than one year from a recession.

Ray Dalio, Andrew’s hero, proclaimed in September 2023 that the U.S. is going to have another debt crisis.

“We’re going to have a debt crisis in this country,” the founder of hedge fund Bridgewater Associates said in an interview with CNBC’s Sara Eisen that aired Thursday. The two were speaking at a fireside chat at the Managed Funds Association. “How fast it transpires, I think, is going to be a function of that supply-demand issue, so I’m watching that very closely.”

You saw what happened to those who weren’t prepared in 2008. We have been preaching to you every week that you have to get your financial house in order.

What is a Recession?

The stock market goes up and down. Sometimes it goes down a lot. Is that a recession? It’s not although you can be forgiven for thinking so because most of the economic news the average person hears is what the market is doing.

But the market is not the economy, and a recession is more than a bear market. A recession happens when the economy as measured by GDP declines for two consecutive quarters or six months.

GDP (Gross Domestic Product) is the total value of everything produced by all of the workers and companies in a country.

Fiscal flexibility that’s funny, free and delivered weekly.

It’s Not a Depression

A recession is not the same thing as a depression.

A recession is when your neighbor loses their job. A depression is when you lose your job.

Tweet ThisA depression, according to Investopedia.com, is defined as “A depression is a severe and prolonged downturn in economic activity. A depression may be defined as an extreme recession that lasts three or more years or which leads to a decline in real gross domestic product (GDP) of at least 10% in a given year.”

What happened in 2008 was not because the market crashed, remember the stock market is not the economy. It was because access to debt and credit was severely curtailed and in many cases, the debt was called in.

That was the case with Lehman Brothers. They had what is essentially a line of credit with JP Morgan Chase and one day JP Morgan Chase decided they weren’t going to lend Lehman anymore.

As a result, Lehman couldn’t meet their obligations. It was infinitely more complicated than that, but this is the spark that ignited the wildfire that consumed the world’s economy.

Debt Cycles Rule the Economy

Economists and Ray Dalio don’t have crystal balls so what are they basing their prediction of a coming debt crisis on?

Debt cycles rule the economy, and because cycles are well, cyclical, we can see them coming.

This is how Ray breaks it down:

- Short-term debt cycles last 5-8 years and are controlled by the central bank lowering and raising interest rates.

- Long-term debt cycles last 75-100 years and can’t be controlled by lowering the interest rates because they are already too low.

- Dalio further breaks down the long-term debt cycle as 50+ years for leveraging, 2-3 years in the depression, and 7-10 years for reflation.

- Dalio says the 75-year debt supercycle is coming to an end.

- We’re not trying to instill fear, nothing good comes from fear. We’re trying to highlight the importance of making smart decisions now.

Check out The Economic Machine at the bottom of the page in the show notes. It’s an animated video created and narrated by Ray Dalio, and it’s 30 of the best minutes you’ll ever spend. He explains how the economy works in a straightforward, easily understandable way.

CLOs are the new CDOs

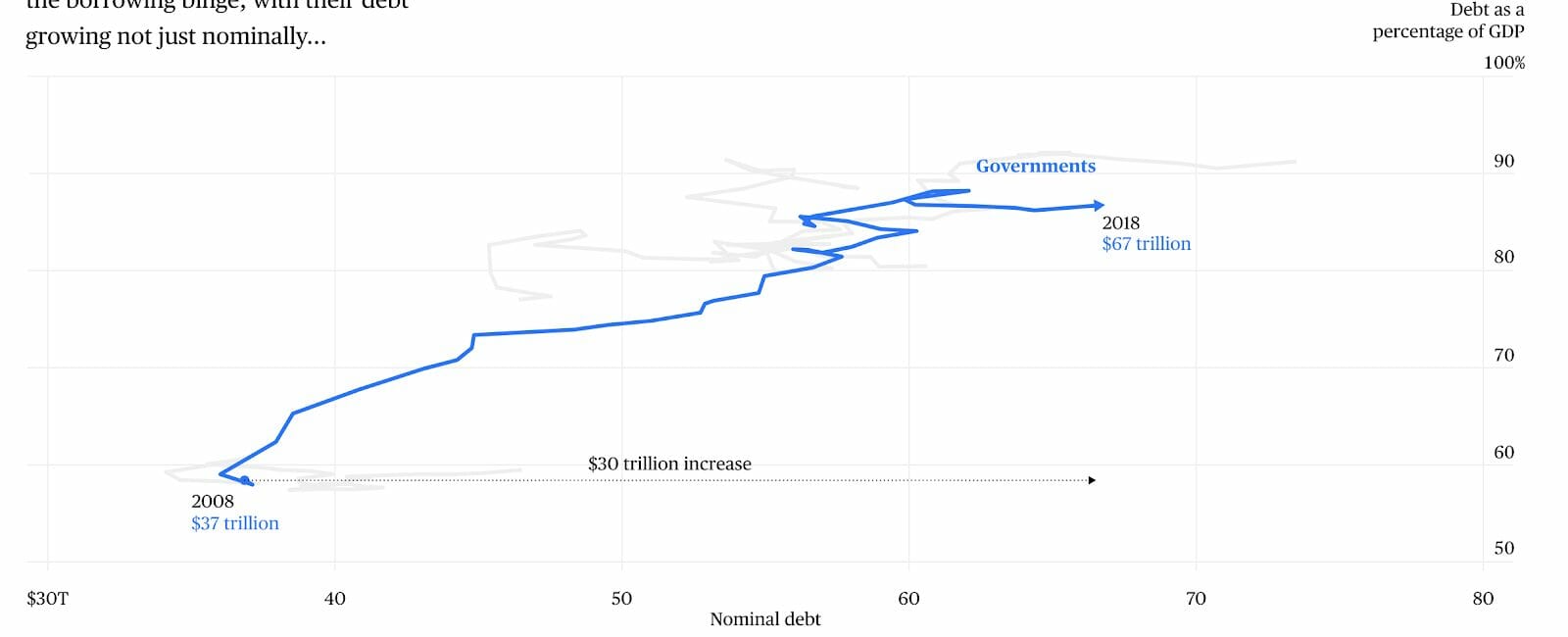

We’ve got a bit of a debt problem at the moment. Global debt has ballooned over the past two decades: from $84 trillion at the turn of the century (2000), to $173 trillion at the time of the 2008 financial crisis, to a staggering $307 trillion in 2023 (according to the World Economic Forum).

That’s 77.45% higher than the last crash in 2008.

According to S&P (spglobal.com), “Global leverage is at a historic high of 349% based upon global debt-to-GDP–more than 25% higher than the 278% in the pre-2008 financial crisis era.”

Non-financial companies have taken over $43.37 trillion in MORE debt or almost 52% more than they had at 2008 levels, and this is the crux of CLOs. CLOs are to business debt as CDOs are to mortgage debt.

- Non-financial businesses gained $28 trillion in debt since 2008 (the big difference is governments can print money and businesses can’t)

- By 2022, global household debt reached $64 trillion, reflecting a 24 percentage point increase compared to 2008 levels.

Recession-Proofing Your Finances by Age

Don’t let the fear of recession push you into making emotional decisions. When have you ever made a good decision when you were deciding based on emotion? We’re going to be ultra-logical here so no knee-jerk reactions.

When you decided to start investing with Betterment, that was a good decision. It was a good decision when you did it, and it’s a good decision now.

Because we have listeners and readers of all ages, let’s break down your career into 15-year segments. There are risks and advantages to each stage.

20s and Early 30s (Early Career)

You’re the new kid on the block which puts you at risk. But you’re a hard worker and have few responsibilities.

Biggest Risk: Job loss

Biggest Advantage: Work Ethic and Time

Damn it! You just got a job, a grown-up job, full-time, good pay, and excellent benefits and the recession will put that job in danger.

Focus on additional income streams. If you lose your job, you want to have money coming in from somewhere because unemployment isn’t going to replace 100% of your income. We know you hate the term side hustle, but you need to get more than one.

Choose one hustle that will start bringing in money immediately like driving for Lyft or renting out your house on Airbnb.

Choose another that could become a full-fledged business. We did a series on how to start an online business that will start making money in one year. If your business does start to make money, wonderful! But don’t be tempted to make a full leap and quit your job to do it full-time.

With the possibility of a recession looming, it’s smarter to hedge your bets. Keep your 9-5 while continuing to work on and hopefully grow your side hustle. It’s too uncertain to leave a (semi) sure thing for a new thing just now.

Increase your working capital. The minimum you want to have as a cash reserve is three months. In the lead-up to what is undoubtedly a coming recession, work on bumping your number up to six months, possibly even nine.

That’s a lot of cash to have sitting around but worst-case scenario, the experts were wrong, the recession doesn’t happen, and hey, you’re sitting on a big pile of cash! There isn’t much downside to this plan.

We know Millennials take a lot of crap from the bitter old Boomers (who raised them), but we know y’all work hard.

The results show that contrary to previous stereotypes, millennials are more likely than other generations to be hooked on work: “More than four in 10 (43%) of work martyrs are millennials, compared to just 29% of overall respondents.”

The study also found that 24% of millennials forfeited vacation last year – meaning they didn’t use holiday days they were entitled to – compared to 19% of generation X and 17% of baby boomers.

Being a hard worker is great, but in a recession, it might not be enough to save you. Rather than working harder, become indispensable at work. Be the person who knows how to do everything and does it without being asked. Be the person they can’t do without.

Because a lot of people in this age group don’t yet have responsibilities like home ownership and family (thanks in part to crushing student loan debt and partly to being the first generation to see those things may not be all they’re cracked up to be), you have a lot of time.

You can take on extra duties at work; you can take classes that will increase your skills. Take advantage of the time you have to become un-layoffable.

But sometimes no matter how good you are, it’s not enough to save you. You lose your job through no fault of your own. You won’t be the only one, and everyone is going to be job hunting at the same time.

The old saying is right though, especially when it comes to getting a job. It’s not what you know; it’s who you know. Start networking, hardcore. Go to Meetups, conferences, and any other type of gathering connected to your industry.

Don’t confine yourself to industry-only events though. Volunteer for a cause you care about, start going to a local trivia night, or join a pickup sports league. It doesn’t matter what you do; it matters that you meet people who could hook you up with a job.

Mid-30s to Late 40s (Mid Career)

You’re spending and making big money.

Biggest Risk: Overinflated lifestyle

Biggest Advantage: Work experience and a strong network

This is for most people, the most expensive period of their lives. They started making more and more money as their careers progressed and spent accordingly. Every raise came with a nice lifestyle upgrade; lifestyle creep crept in.

Life might be good but it’s expensive. Some people in this bracket not only have credit card debt but still have student loan debt. Get a consolidation loan to pay off the credit card debt and refinance the student loan debt to a better interest rate.

This is a dangerous trend at any time, but it’s even worse when a recession is on the horizon.

If this sounds familiar, you must become ruthlessly efficient with your expenses. Start making cuts now.

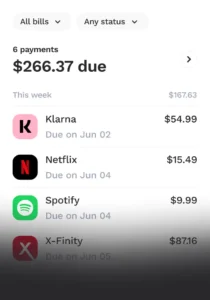

Cushion will find recurring monthly expenses like the gym membership you never use or that trial offer period for insert thing you didn’t need here. When Cushion finds these expenses, they’ll ask if you want to cancel them. If you do, Cushion will handle the rest. It’s that easy.

Cushion is the easiest way to organize, pay, and build credit with your existing bills and Buy Now Pay Later. All your recurring payments — one dashboard, complete control.

We know you have a budget (please tell us you have a budget). Move from budgeting for the month to budgeting for the week. It’s easier to see where your spending leaks are and plug them when you micro-budget.

And listen to the Refrigerator Episode we did a couple of months ago.

You also need to revisit your asset allocation and reduce your risk. This means more bonds than stocks. It’s also an excellent time to start an opportunity fund so you can score some bargains in the next bear market.

Start hoarding an opportunity fund in an Upgrade High-Yield Savings Account so you can snatch up some bargains during the next Bear market.

You’re in the most expensive period of your life, but you’re in your highest earning period. You’ve been around for a while and you know your job and industry intimately. But are you being paid what you’re worth?

If you’ve been getting the standard 3% raise each year and you’ve been with your company for several years, probably not. Start researching to find out what you’re worth. Go to your boss with a solid argument as to why you should be making what others in similar jobs in your industry are making.

Did you get the raise? If you didn’t, don’t worry. The big jump doesn’t come from getting a raise; it comes from changing jobs. And you have a strong network to mine for a better opportunity.

50s and 60s (Retired and Almost Retired)

You’re looking forward to winding things down but on your schedule and not because of economic conditions. But if you must go, you’re at least somewhat prepared.

Biggest Risk: A big loss this late can seriously affect your retirement lifestyle or even your ability to retire.

Older workers are among the first to go when the layoffs start because they’re expensive. And it can be harder for them to find employment for the same reason. It’s cheaper to employ and hire younger people.

If you’re offered a buyout package to retire early, take it. Getting paid to leave is better than getting laid off or fired. Unemployment is not going to pay as well as a buyout package.

Biggest Advantage: You’re likely prepared to retire so you won’t be in a time-critical money crunch.

You might decide to cut back your hours as you wind down your career. Even if you don’t, you are probably an empty nester by now, so you don’t have the demands of raising kids. Translate any extra time into gently converting a hobby or activity into a casual stream of income.

If there is a market crash, it will affect your retirement in later years so you can probably use small levels of income to resolve any draws you need to take at a market low-water point.

Shift some of your investments towards income-producing assets. You don’t have to incur the risk stocks represent anymore, nor should you. You don’t have enough time to ride out the ups and downs of the market anymore.

Your portfolio should include things like Dividend Aristocrats, Rental Property, Fundrise, REITs, or interest-paying bonds.

Scared Straight

We don’t want to frighten you, but there is very good reason to be scared. A recession is coming; automation is going to eliminate millions of jobs, and wages have been stagnant for decades. So we don’t necessarily want you to be scared, but we do want you to understand the consequences of these things.

If you don’t take steps now to prepare yourself and your finances, you’re going to be caught out. But the steps you have to take aren’t particularly hard or complicated. And you still have time, probably not much but still time. Start now.

Show Notes

SingleCut: From Beersmiths

Brunch: Matt’s brew