Debt affects your credit score and makes life more expensive. We’ll show you the cost of debt and the reasons you need a good credit score.

A good credit score saves you money in many ways. You don’t have to achieve the “perfect” score but having a score above 700 will go a long way towards making life cheaper.

What Is a Credit Score?

A credit score is a three-digit number based on several factors that represent your creditworthiness. Lenders use this number to determine whether or not to lend you money and what your interest rate will be. The higher scores earn the best rates.

Editor's Note

What Makes Up a Credit Score?

Six major components make up your credit score. They are:

- Payment History: If you pay your bills on time.

- Credit Utilization: How much of your available credit are you using.

- Derogatory Marks: Do you have delinquent accounts, past bankruptcies, judgments against you, etc

- Length of Credit History: How long you have had a credit file.

- Total Accounts: How many credit accounts you have open and how many types (credit card, mortgage, student loan, personal loan, car loan, etc.)

- Credit Inquiries: The number of times lenders check your credit.

We wrote an in-depth article on it too.

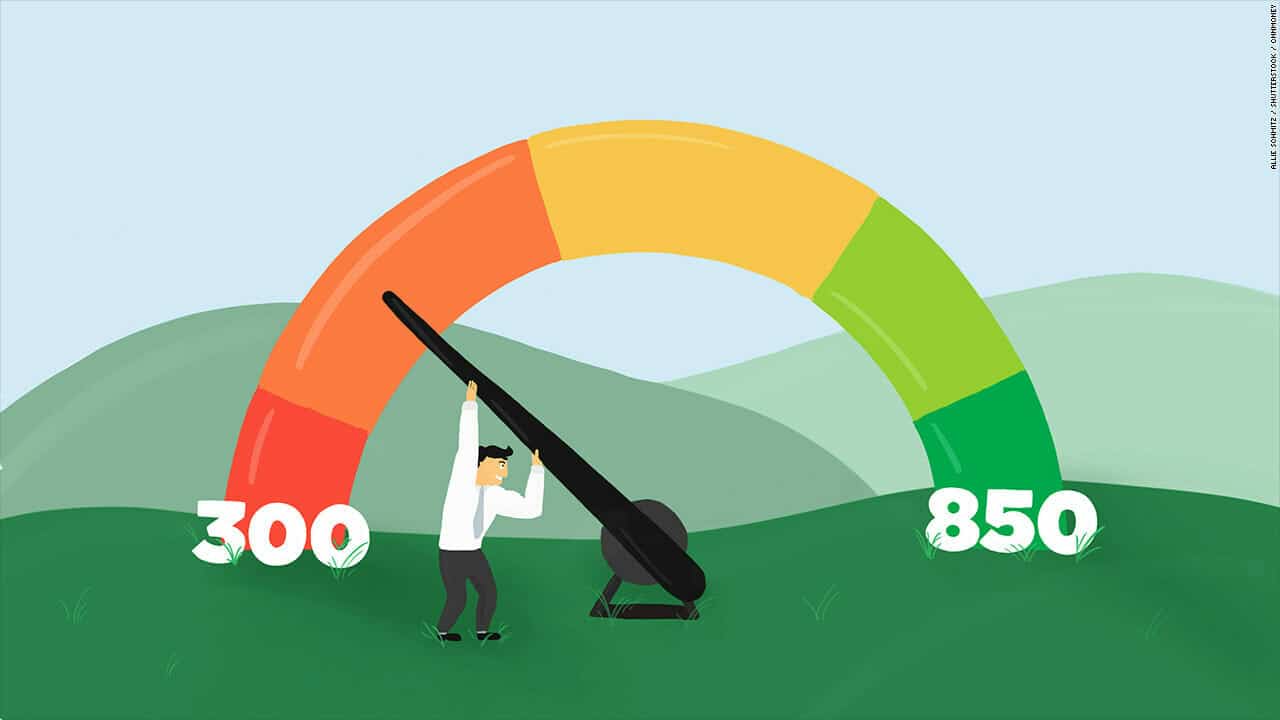

What is a Good Credit Score?

A good credit score is typically 700 and up. Scores range between 300-850. Anything above 800 is excellent. Here’s a FICO credit scoring model:

- 300-579 is bad.

- 580-669 is fair.

- 670-739 is good.

- 740-799 is very good.

- 800+ is excellent.

Either end of those is pretty hard to achieve, and some people obsess over their credit score way more than necessary. There are lots of reasons you need a one, but a good score starts at 700. So if you are there, you’re set.

The most well-known types of credit scores are FICO Scores, created by the Fair Isaac Corporation, and scores from Vantagescore. The three major credit bureaus that run your score are Experian, Equifax, and TransUnion.

Remember, with the Fair Credit Reporting Act (FCRA); you’re entitled to get a free credit report annually.

Free credit scores can be found on the government website AnnualCreditReport.com. You can also get your score through your credit card issuer. Know what your score is so you can improve it.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

Reasons You Need a Good Credit Score

If you don’t have a good score, here are some reasons to get one.

Interest Rates

The two most expensive things in life are taxes and interest, and if you can avoid them, you will reach financial independence much faster.

If you want to buy a home, take out an auto loan, or borrow money for anything from starting a business to renovating your house, a good credit score will determine the rate of interest the lender sets for the loan.

What’s a point here and a point there? A lot when we’re talking about interest rates. If you buy a $300,000 house with a 20% ($60,000) down payment and a 30-year fixed-rate mortgage at 4.5% rather than 5.5%, over the life of that loan, you will save $52,794.

Your monthly payment at 4.5% will be $1,216 versus $1,363 at 5.5%. That’s an extra $147 per month. If you invested that $147 every month at an average return of 7% a year and did that for 30 years, the same length of your mortgage, you would have $180,381.86.

A one percent difference means over $200,000.

Job Search

Employers may pull your credit report as part of a background check. It’s most likely to happen if the job involves handling cash, access to personnel files, or a senior-level position that requires a lot of decision making.

You can see why a potential employer would want this information in those circumstances; people who have poor credit could be thought of as more likely to steal either money or the identity of another employee that could be used to open credit accounts.

If your decisions led to an unsatisfactory credit report, they could lead to bad decisions for the company.

These kinds of checks are usually not done early in the process. They come when the employer is almost ready to offer the candidate a job. If it comes down to a choice between two equally qualified candidates, a bad credit report could be the difference.

![A Good Credit Score Saves You Money and Here’s How [UPDATED]](https://www.listenmoneymatters.com/wp-content/uploads/2014/07/LMM-Cover-Images-29-768x432.jpg)

Better Credit Rating Means Better Options

Having an excellent credit score gives you more options. If you want to buy a home or car, you will have more lenders willing to loan you money. You can choose the best offer.

If you are renting an apartment, you can choose between nicer neighborhoods. Residences that don’t do credit checks or have low requirements are not going to be in agreeable areas.

If you want to leave your job and start a business, good credit will increase your chances of getting a business loan.

Save Money on Bills

Most landlords and management companies will do a credit check before renting an apartment. If your credit isn’t favorable, they may not rent to you.

Some still rent to people with bad credit but require a substantial security deposit or a guarantor.

If you have poor credit, utility companies may require a deposit to turn on the electricity, phone service, water, and gas.

Moving is already expensive, and when you have to pay more to have the utilities turned on, coupled with paying a bigger deposit on the apartment you’re moving into, it gets challenging.

Good Credit Cards

Not all credit cards are created equal, and not everyone who applies for a card will qualify. To get good cards, you have to have satisfactory credit.

A sound credit card comes with all sorts of perks; free hotel stays and flights, airport lounge access, reimbursement when you pay for Global Entry and TSA Pre-Check, concierge services, consumer protections, and cashback.

Insurance

Insurance companies, whether home, auto, health, or life, are in the business of taking risks. They want the price you pay to reflect how much risk they are taking by insuring you.

To do this, many companies compile an insurance score, similar to a credit score. Part of what they use to come to the insurance score is information from your credit report.

Companies use the number to determine how likely you are to file a claim, miss or make late payments, or file a fraudulent claim. Home insurance rates for those with poor credit are two times higher on average than those with excellent credit.

Health insurance companies want to know if you have a good payment history, but you only need to worry about this if you pay privately for insurance.

If your employer covers you, they won’t check your credit score because the payments are automatically deducted from your paycheck.

Credit scores can correlate to behavior. People who are responsible for their money tend to be responsible for their health. You can see why health and life insurers find your credit score relevant.

How to Build Your Credit Score

There are lots of ways to build a good credit score if you have what’s called a “thin file.” If you don’t have enough history to be approved for a regular credit card, you can apply for a secured credit card. You provide a deposit, and that amount is your credit limit.

After a time, if you have used the card responsibly, you can apply or sometimes be upgraded with the same company that issued the secured credit card, to a traditional card.

If you’re in college, you can apply for a student card. The bar to be approved is lower than for a traditional card. The same is true of some retailer-issued credit cards. Some landlords and utility companies report payment history to the credit bureaus.

You can become an authorized user on someone else’s card. You have access to credit, but the person the card was initially issued to is responsible for paying the bill.

Using a card this way can build credit, but not all cards report authorized user activity to the credit reporting bureaus, so check first.

You can get a credit builder loan. You borrow money, but it’s held by the lender and only released to you after you have paid the loan back.

Fix Bad Credit

If you need to improve bad credit, you can follow the same advice for building credit, but there are a lot of new things you can do as well.

If your score is low due to late payments, set up phone alerts a few days before the due date, and schedule it to go off at a time you know you will be in front of a computer to pay the bill.

There is no point if an alert goes off when you’re driving to work; you might forget once you arrive.

Some credit card companies allow you to choose your payment date. If you have that option, select dates that are easy to remember. For example, the first or 15th of the month, or a lucky number.

That way, you have fewer dates to monitor. Just be sure you don’t cluster so many payment dates that you don’t have enough to pay all your bills at once.

If you still have new credit cards, ask for an increase in your spending limit. You may be turned down, but it doesn’t hurt to ask, and if you’re approved, it lowers your utilization, one of the factors making up your score.

For the same reason and for the length of history, don’t close credit accounts once you’ve paid them off. Many people close paid accounts, thinking it improves their score, but it hurts you.

If you’ve been haphazardly paying off your cards, just throwing money at the credit card balances randomly, have a plan. Use the stacking or snowball method so you can pay the debts off more quickly and increase your score.

You Lose Benefits by Not Using Credit

You might decide this is too much hassle, and you’re not going to play the game. You’re going to pay cash for everything, so it doesn’t matter what your credit score is.

And you can do that, but it means you lose some of the benefits of a good credit score, like lower insurance rates.

It hurts your cash flow. You can pay cash for a home, but that’s a lot of money tied up in a non-liquid asset, cash that you can’t use to invest and cash that you don’t have in case of an emergency.

You lose the buyer protections credit cards provide like extended warranties when you buy things with cash.

Having a credit score doesn’t have to mean drowning in debt. You can have one or multiple credit cards and pay them off in full every month with no debt.

You can take your time paying down student loans or mortgage debt because the money you invest instead is giving you a higher return than the rate of interest on those debts.

Using credit in a way that adds up to a good credit score makes life cheaper.

Show Notes

E Credit Attorney: A company that can help clean up mistakes on your credit report.

Maxed Out: A documentary about credit practices.

Ready For Zero: A service to help you track and pay off your debts faster.