Having a good credit score makes life easier and cheaper. Even if you’ve tanked your credit, we’ll give you some ways to bring the number back up. You don’t have to wait seven years to start improving your credit score. There are a few tricks to get that number out of the red.

Having a good credit score can save you thousands of dollars over a lifetime. It makes you eligible for lower interest rates for car loans and mortgages. Some jobs even require a credit check.

Understanding Your Credit and FICO Score

Your credit score is a number that shows how reliable you are when it comes to borrowing money—and not all credit scores are the same. One of the most important types is your FICO score, which most lenders use when deciding whether to approve a loan, credit card, or mortgage. Knowing the difference between your general credit score and your FICO score can help you make smarter financial decisions and improve your chances of getting approved.

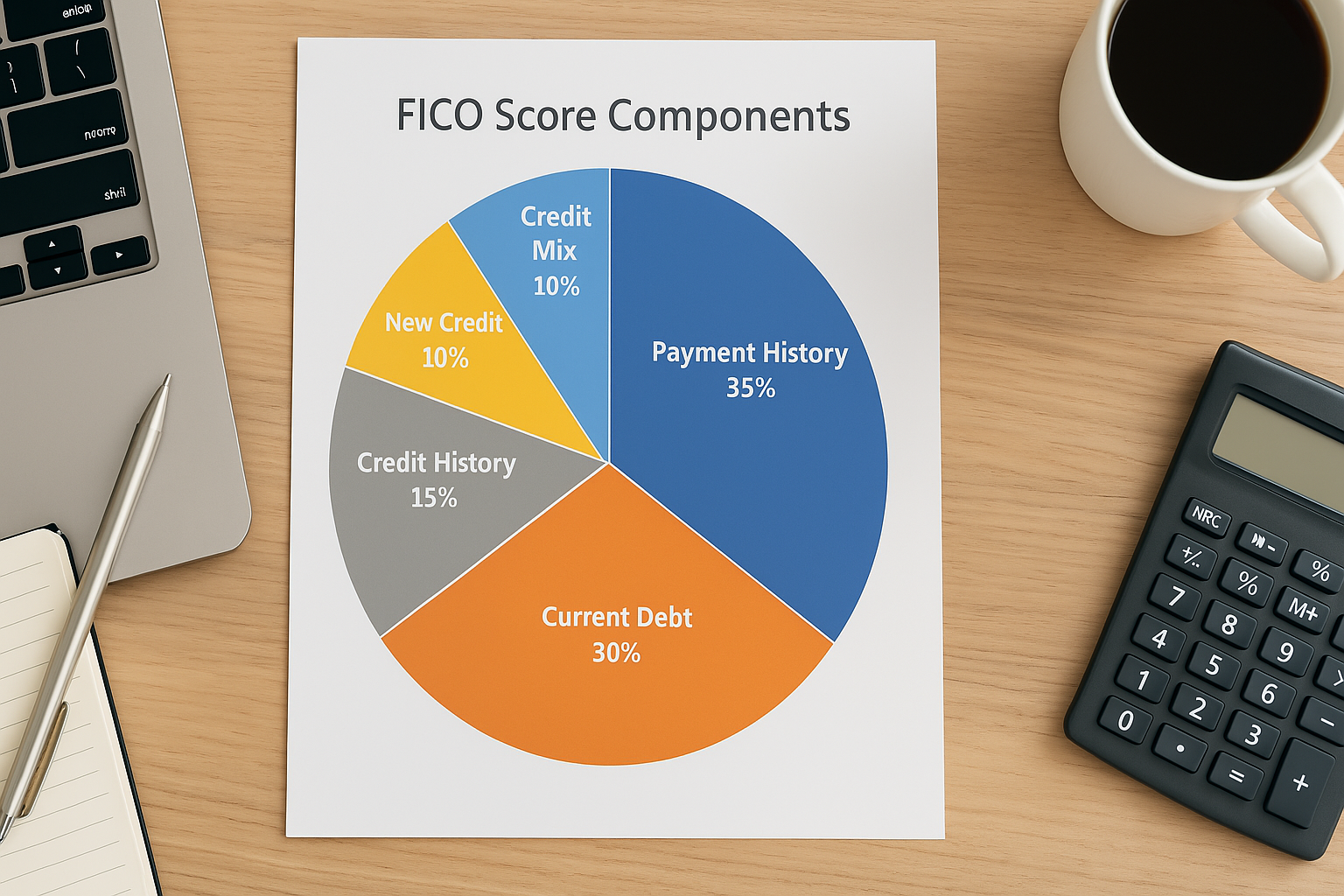

Key Components of Your Credit Score:

- Paying your credit card and loan bills on time, which accounts for 35% of your FICO score.

- Keeping your credit utilization below 30% of your total credit line, which accounts for 30% of your FICO score.

- Avoiding mistakes that result in bad marks on your score, such as late payments or collections.

- Maintaining a long credit history, which accounts for 15% of your FICO score.

- Having a diverse mix of credit types (e.g., credit cards, loans), which accounts for 10% of your FICO score.

- Managing new credit inquiries and accounts responsibly, which accounts for 10% of your FICO score.

Simple Steps to Improve Your Credit Score

Improving your credit score doesn’t have to be overwhelming. With a few smart habits and consistent action, you can boost your score and build a stronger financial foundation. Whether rebuilding from past mistakes or starting from scratch, these tips can help you make steady progress.

- Lower your credit utilization: Request a higher credit limit or spread small charges across multiple cards to keep usage low.

- Keep accounts open: Avoid closing old cards, as this shortens your credit history and increases utilization.

- Use automatic payments: Set up auto-pay on recurring bills to ensure you never miss a due date.

- Always pay on time: Even partial payments help—on-time payment history makes up 35% of your score.

- Start with a secured card: If you have poor or no credit, a secured card can help you build a solid history.

By building your credit now, you will have an easier time being approved for loans and credit cards in the future. Working on your credit allows you to invest in your future, which will lead to tangible benefits.

Getting Your Credit Under Control

Before you can improve your credit score, you’ve got to clean up what’s hurting it. If you’ve got late payments, unpaid debts, or things like liens, start by dealing with those head-on. These issues can seriously drag down your score if left unchecked.

Take a hard look at your finances, figure out where things went wrong, and build a plan to move forward. Getting organized and cutting down on debt will put you on the right track. Start focusing on the path to manageable debt and a stronger credit future.

Assess Your Score

You can’t fix your credit if you don’t know exactly what’s wrong. A lot of people realize their credit isn’t great, but they don’t understand how bad it really is or why it’s low. That’s why your first step should be pulling a copy of your credit report.

There are a few free tools that make this easy. For example, Credit Karma offers free access to your credit reports. Once you have it, go through it line by line to check your score and spot any errors or outdated info that might be dragging you down.

Order a free copy and read through it carefully to check your score thoroughly and scan for any errors that may affect your credit score.

Many people realize that their credit is actually being brought down by clerical mistakes or mistakenly reported factors present in their reports. If you see any of these issues, you can report them to the credit agency and work on getting them amended.

With this report, you will better understand how to improve your credit score.

Stop paying with credit temporarily

Here are some key reasons why overusing credit cards can be problematic:

- High Credit Utilization: Keeping high balances increases your credit utilization ratio, which can lower your credit score.

- Payment History Issues: Missing or making late payments can harm your credit score, as payment history is a significant factor.

- Increased Debt: Overusing credit cards often leads to more debt, straining your financial health and affecting your credit score.

A simple rule is only to buy things with a credit card if you can afford them without it. If you find yourself overspending, try keeping your cards at home or even freezing them to avoid impulse buys.

You can take the first steps towards a healthier credit score by controlling your spending and reducing debt.

Get Organized

Once you’ve reviewed your credit report and paused credit card spending, it’s time to get your finances in order. Start by writing down everything you owe—credit cards, loans, and any other debt. Include balances, due dates, and interest rates so you can see the full picture.

Focus on paying off the debts with the highest interest first. These cost you the most over time. To make real progress, create a budget that minimizes your spending and puts more money toward paying off those high-interest balances.

Automate Payments

Between bills, credit cards, and loans, it’s easy to lose track of due dates—which can lead to missed payments and hurt your credit score. Use a calendar or budgeting app to keep payment deadlines front and center.

Even better, automate your payments. Most banks and lenders let you set up auto-pay for minimum or full balances. With payment reminders and auto-pay tools, you can stay on track without the stress of manual tracking.

Here are some tools that can help you manage and automate your payments:

- YNAB (You Need a Budget): Helps you plan every dollar and stay ahead of upcoming bills.

- Monarch Money: Offers budget tracking, calendar views, and recurring bill alerts.

- Credit Karma: Provides free credit monitoring and payment reminders for linked accounts.

- Your Bank’s App: Most banking apps support auto-pay, alerts, and due date notifications.

This free course outlines a proven framework that thousands of people have used to eliminate their debt, develop better money habits, and start building a secure financial future.

How to Build Credit Fast

While you won’t go from poor credit to perfect overnight, there are smart ways to speed up the process. Taking the right steps now can make a big difference over time. If you’re serious about improving your credit, start by making a few changes and sticking to the basics. Here are some tips to help you expedite the credit-building process and boost your score.

Be Disciplined

You won’t fix your credit without changing how you spend and use credit. That means building a budget—and actually sticking to it. Take a close look at your current spending and cut back where you can. Skipping dinners out or impulse buys now will pay off when your debt is under control and your score starts climbing.

Be Consistent

Pay on time—every time. Set calendar alerts, use mobile banking reminders, or automate payments to avoid missing due dates. If auto-pay isn’t an option, pick one day a month to knock out all your bills at once. Consistency is key to building trust with lenders and raising your score.

Seek Professional Help

Not sure where to start? Talk to a financial advisor or credit counselor. There are professionals who can help you build a personalized plan to get out of debt and improve your credit score. You don’t have to figure it out alone.

Simplify Your Finances

Don’t overcomplicate things. Instead of opening more accounts, focus on managing the ones you already have. Keeping it simple helps you stay on top of payments, avoid mistakes, and build a solid credit history.

What You Can Expect

The great thing about working on your credit score is that you can start seeing results in just a few months. But keep in mind that some parts of your credit history take longer to recover from, no matter what you do.

Here are a few things to expect while improving your credit:

- Delinquent payments: These can stay on your credit report for up to seven years, even after you’ve paid them off.

- Bankruptcies and liens: Depending on the type and reporting agency, these may remain visible for up to ten years.

- Hard inquiries: Any time a lender checks your credit for a loan or credit card, that inquiry can stay on your report for two years.

Stay realistic and don’t let your credit score stress you out. Create a plan, track your progress, and focus on making steady improvements. The sooner you take action, the sooner you’ll enjoy the perks of better credit.

Final Words

Improving your credit is a journey, not a sprint. Some changes take effect quickly, while others require patience and persistence. Focus on what you can control—pay on time, manage your debt, and check your credit reports regularly. With the right habits and tools, your score will start to climb, opening the door to better financial opportunities down the road.

Show Notes:

Credit Karma: A free, ball park credit score. A soft check so it won’t ding your score.

Mint: Track your spending.

What Makes Up Your Credit Score: Read more in depth about what goes into a credit score.