Dollar-cost averaging is a simple yet effective strategy to help you grow wealth. The best part is, you can put your money on autopilot. Dollar-cost averaging takes the fear out of investing.

Do you have a lump sum of money that you want to invest, but you’re waiting until the exact right time to invest it? You don’t just want to dump a pile, especially a big pile of money, into the market at the wrong time and watch it evaporate. There are two ways you can avoid that happening; one is the wrong way, and one is the right way.

All investors have two major concerns when they invest, making money and limiting risk. We all want big profits fast with no risk. But that’s not the reality of investing. To make money while limiting risk, we have to employ a good investing strategy.

Dollar cost averaging is just such a strategy; it’s good for all investors but especially for those new to investing.

Some Good Days and Some Bad Days

On September 29, 2008, the Dow Jones Industrial Average suffered one of the worst losses in Wall Street history. Upon the news that the House had rejected the $700 billion bank bailout plan, the Dow plunged 778 points. This decline marked one of the largest single-day point losses in Wall Street history.

In an instant, $1.2 trillion dollars in market value evaporated. If you had been a wary investor but finally decided to take the plunge on that day, you would have had a very bad day indeed.

Just two weeks later, Wall Street saw its biggest one-day gain in history. The Dow added 936 points, and a record $1.2 trillion dollars surged back into the market. If you had invested that morning, you would have had a very good day indeed.

Timing the Market

If you had known to pull your money out before that big crash and known to put it back in the day of the big gain, you would have timed the market perfectly. But how would you know the crash and the rebound were coming?

Some people think they can predict such things by timing the market.

Market timing means trying to predict the direction of the financial market by analyzing the stock market and economic data. It’s a good idea in theory because like we explained above, you would hate to invest your money right before a big drop in the market and love to invest it before a big gain.

Do you have a Magic Eight Ball?

Because if you do, give it a shake and ask it when you should invest. That will give you about as good a result as trying to time the market will.

Professional fund managers can’t time the market with much success and not only do they have reams more data than you have, but they also have the time to pour over all of it and understand what that data tells them. And they still do worse than the market more than 89% of the time!

Even if you did have the time and understanding to go over all that data, why would you want to? It’s boring!

This is the wrong way to go about investing money into the market if you want to protect yourself from unnecessary market risk. But there is a way to do that.

The key component of dollar cost averaging is NOT timing the market.

Fiscal flexibility that’s funny, free and delivered weekly.

What is Dollar Cost Averaging?

The term dollar cost averaging sounds more complicated than it is. It simply means that you determine a set dollar amount that you want to invest. Then you invest that fixed dollar amount on a set schedule without regard to the share price instead of putting one lump sum investment in all at once.

Here’s an example of a dollar-cost average strategy. You have $1000 you want to invest.

You invest $100 a month over the course of ten months. Using this method, you will average out the cost per share so that you don’t have to worry about timing the market.

Now let’s look at a more specific example; we aim to get as many shares as possible for the lowest price without making life too complicated.

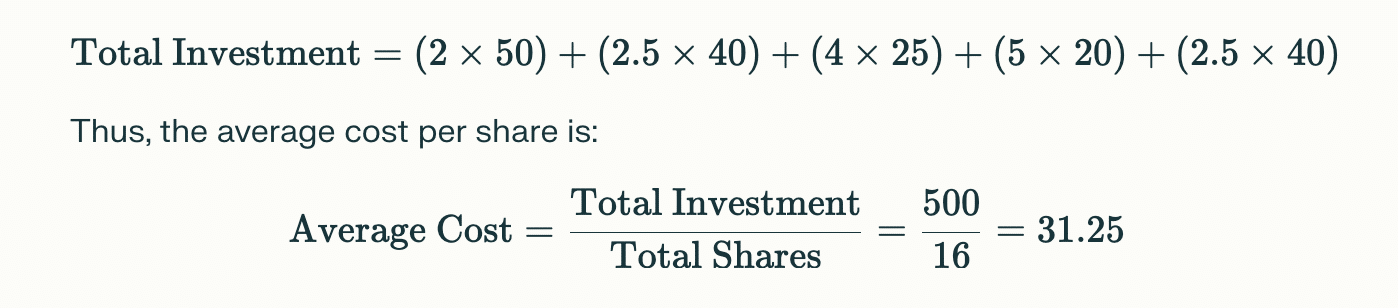

You have $500 to invest in Nike.

The first month each share is a purchase price of $50, so you buy two. The second month each share is $40, so you buy two and a half. The third month they are $25, and you buy four. The fourth month they are $20, and you buy five. The fifth month they are $40, and you buy two and a half.

At the end of five months, you have purchased sixteen shares at an average cost per share of $31.25.

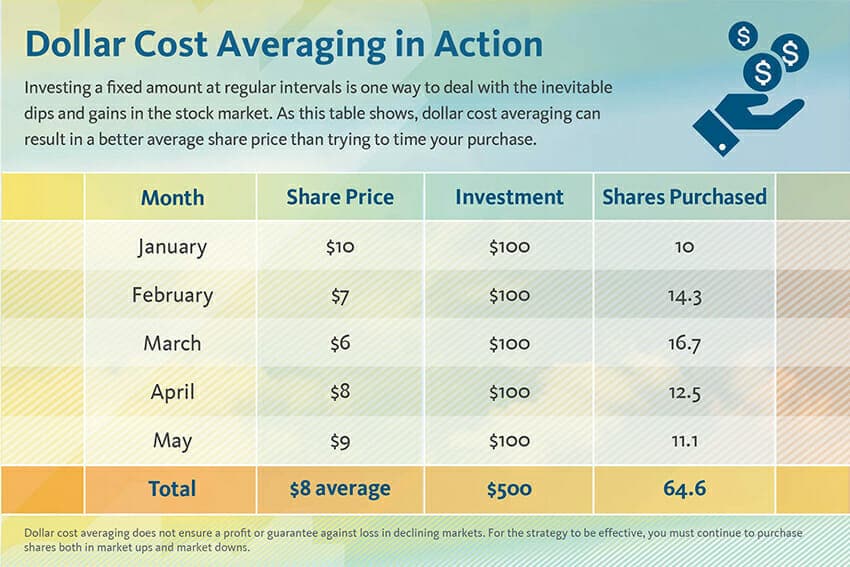

Now, what would happen if you took your $500 and bought as much Nike stock as you could at once? You buy ten shares for equal amounts of $50 each. Your $500 bought you fewer shares for more money average price per share.

You’re Probably Already Doing It

The examples we showed were for buying individual shares of stock which we don’t generally recommend, especially not for investing newcomers. You can use DCA for any kind of investment, bonds, mutual funds, and ETF’s (exchange-traded fund).

You might even already be using dollar cost averaging without realizing it. Do you participate in an employer-sponsored 401k via automatic payroll deductions?

That’s dollar cost averaging. A set amount of money goes into an investment account at regular intervals making an automatic contribution.

Your Dollar Cost Averaging Plan

Dollar cost averaging is so simple! You only have to make three decisions. First, decide how much you have to invest. Make sure this is money you don’t need for other things, constantly pulling money out of the market because you overspent on restaurants and can’t make rent is a bad investment strategy!

Next, decide how often you will invest.

Once a month is nice and simple. It doesn’t have to be once a month; it could be a longer or shorter time frame but we like to keep things simple and investing each month is nice and simple.

Lastly, choose your investment vehicle.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

We like M1 Finance for their low fees and simplicity, but it could be a 401k through your employer or bonds if you’re nearing retirement and have a lower risk tolerance.

Take the Fear Out of Investing

Dollar-cost averaging is a risk management tool. It minimizes the effects of market fluctuations on your investments.

There are many questionable investment strategies out there, but dollar cost averaging is a reliable approach. It helps reduce the fear and anxiety that often come with investing. When you’re feeling uncertain, it’s common to hesitate before making an investment.

Make your investing time agnostic.

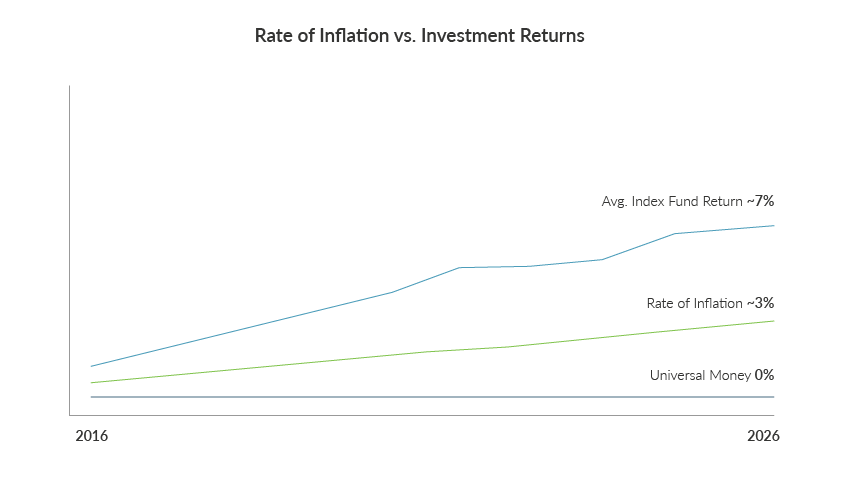

Tweet ThisThat hesitation can be risky because keeping your money in a low-interest savings or checking account doesn’t help it grow. Most of these accounts pay less than one percent interest, which means your money isn’t just sitting still—it’s actually losing value over time.

Inflation averages about 2.7% as of November 2024, so keeping your money in low-yield accounts means losing buying power. A dollar today won’t be worth as much ten years from now unless it’s invested in something that earns more than inflation.

Essentially, leaving your money in a savings account with minimal interest leads to a loss of value over time.

When it comes to investing, time is more important than timing. The longer your time horizon for investing, the more money you will make. The longer you sit by afraid to invest, the further away you are from retirement.

Dollar Cost Averaging (DCA) is a great way to develop a regular investing habit. It involves setting aside a fixed amount of money to invest on a consistent basis, which can easily fit into your budget. This approach not only helps you stay on track with your investments but also supports your retirement plans over time.

When you use DCA, you can ignore the loud headlines about market ups and downs. Since you’re investing steadily over time, short-term dips don’t matter as much. By regularly putting in your money, you let it grow gradually. Just remember, investing is a marathon, not a sprint.

If the market is up, you will be buying fewer shares. If the market is down, that just means you get to buy more shares at a lower price! Remember what Warren Buffett tells us, “Be fearful when others are greedy and greedy when others are fearful.”

The Downside of Dollar Cost Averaging

One downside of Dollar Cost Averaging (DCA) is that you might have cash just sitting around, waiting to be invested. This can feel frustrating, especially if the market goes up while you’re waiting, and you miss out on gains.

But as Warren Buffett suggests, having some extra cash during a bear market can actually be a good thing. It gives you a chance to scoop up stocks at lower prices when others are panicking and selling off their shares.

Dollar Cost Averaging during a bear market is a smart move. It helps you invest consistently at lower prices while reducing emotional stress. To minimize risk, consider diversifying through mutual funds or ETFs, which spread your money across various assets and protect your portfolio from individual stock volatility.

As with any investment strategy, you have to do your own due diligence to mitigate risk.

Variations on Dollar Cost Averaging

If you like the concept of dollar cost averaging but it sounds a little too restrictive, there are variations that incorporate short-term trends.

Value DCA

Instead of investing the same amount each time, you put in more money when prices drop and less when they rise, based on your goals. While this can help you take advantage of lower prices.

While Value DCA lets you invest more when prices drop and less when they rise, you might miss out on gains if the market keeps going up. Plus, any cash you hold while waiting to invest isn’t earning anything, which can lead to higher costs later if prices rise. So, while Value DCA can help manage risk, it can also create new challenges for your investments.

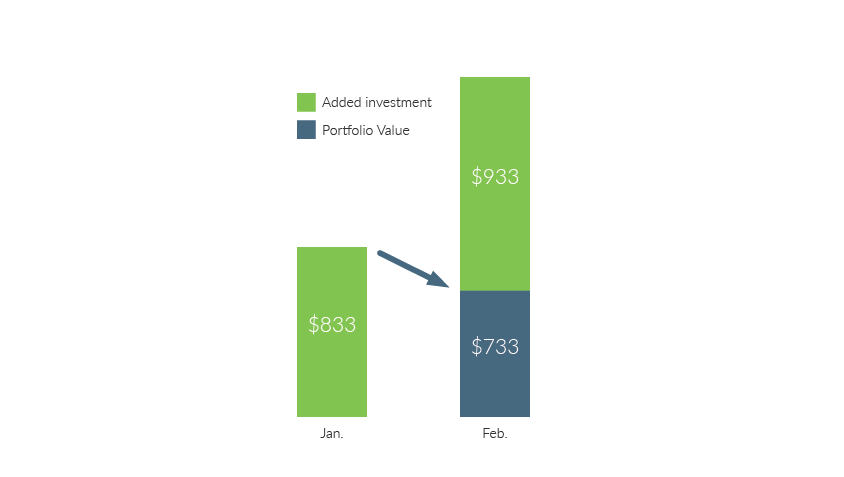

Value DCA Example: Let’s say you want your portfolio to reach $10,000 by the end of the year, investing once a month.

You’d start by planning to invest about $833 each month ($10,000 divided by 12 months). If your portfolio loses $100 in February, you might decide to invest $933 that month to help get back on track toward your goal. This way, you’re putting in more when prices drop, which is the essence of Value DCA.

If your portfolio gains in a month, you’ll invest less to stay on track for that $10,000 goal by year-end. This method requires more monitoring and math than some people may want to deal with, but if you enjoy being hands-on with your investments, Value DCA could be a good option for you.

Momentum DCA

Momentum DCA is different from traditional DCA. In this strategy, you look at data from the past 3-12 months and invest more when the market is rising, paying higher prices per share, and less when it’s falling. This approach assumes that upward trends will continue, aiming for quick gains.

While it can be effective in the short term, it requires careful monitoring and carries significant risks if market trends reverse. We mention this for informational purposes, so be cautious if you consider using it!

Reverse Dollar Cost Averaging

Most people think of dollar cost averaging as a buying strategy, but it can also apply when selling, especially during retirement when your investments become your income. This is known as reverse dollar cost averaging. Instead of investing a set amount regularly, you withdraw money from your investments on a schedule. Rather than selling all at once, you cash out incrementally over a set timeframe.

This approach can lead to selling more shares when prices are low and fewer when they’re high, so it requires careful monitoring to avoid negatively impacting your portfolio.

This can be risky because when share prices are low, you end up having to sell more shares to hit your withdrawal amount. That can really eat into your investment over time. To help balance out these risks, it’s smart to have other income sources, like rental properties or annuities, so you’re not relying solely on your investments during tough market times.

Invest with a Plan

The biggest mistake in personal finance is sitting on the sidelines and not investing at all. The second biggest mistake is jumping in without a plan. Having a solid investment plan helps reduce risk and gives you peace of mind.

Dollar cost averaging should definitely be part of your strategy. Just decide how much you want to invest and how often, and start getting into the market today!Show Notes