Almost 50% of Americans cannot come up with $400 if they needed it urgently. 1 in 3 Americans has $0 saved for retirement. In the U.S. it seems we’re much better at spending money then we are saving.

This spending problem is leaving too many American households living paycheck to paycheck with close to nothing saved for the future.

Americans Have a Problem

The savings rate has been falling for most of the past few decades. Maybe we stopped saving when our income growth flatlined after the recession, maybe it’s because we’re being buried in student loan debt, or maybe consumerism has taken over.

It doesn’t change the cold hard truth that most people are not prepared for retirement at all.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

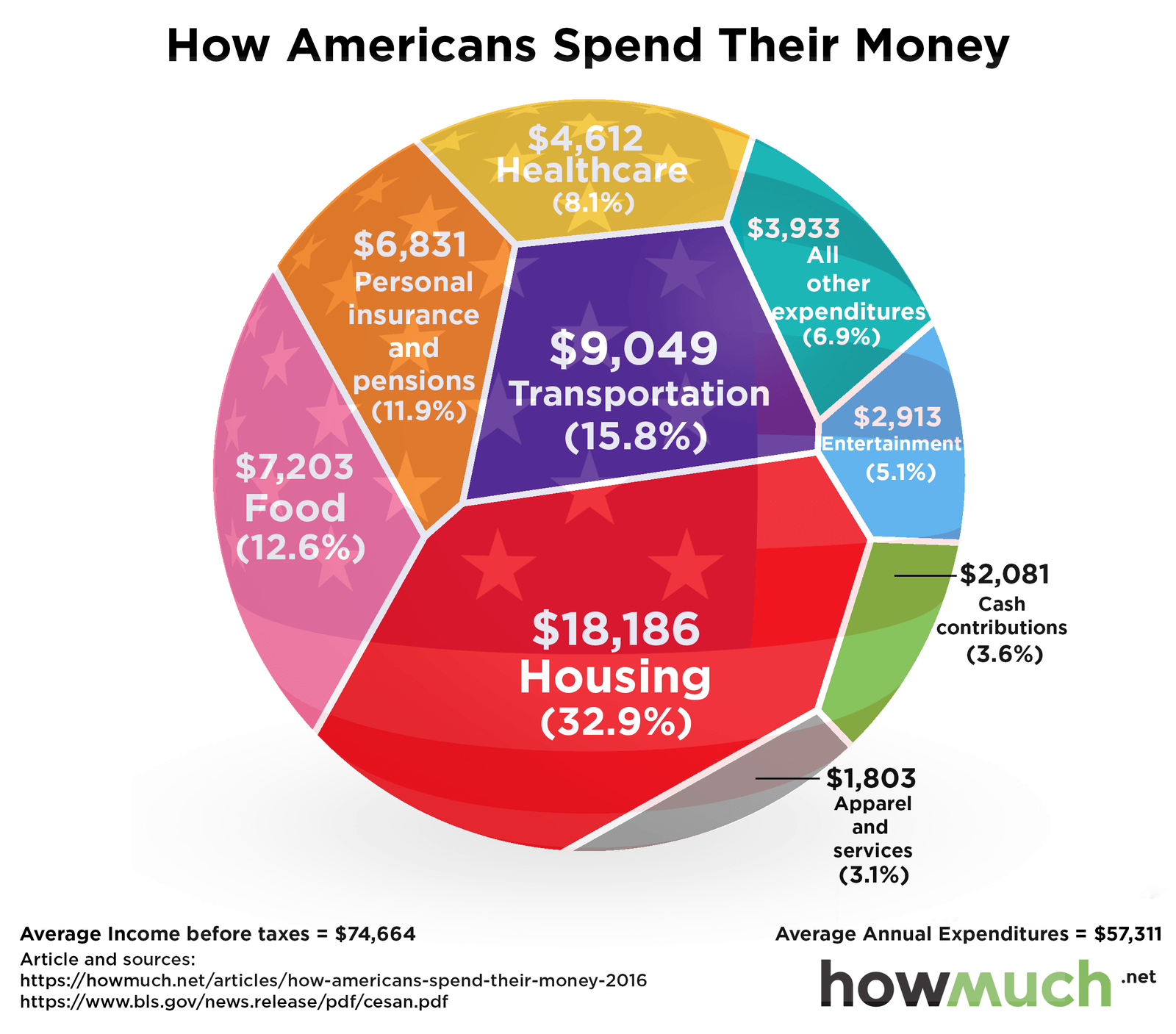

Americans today save a lot less than their parents and grandparents did a generation ago. The average savings rate for our parents was between 7 and 10 percent and two generations ago, Americans saved 10 to 13 percent of their income.

Today the average is 4.8%. Whomp Whomp. So where is it all going?

Chances are, you’re not saving enough

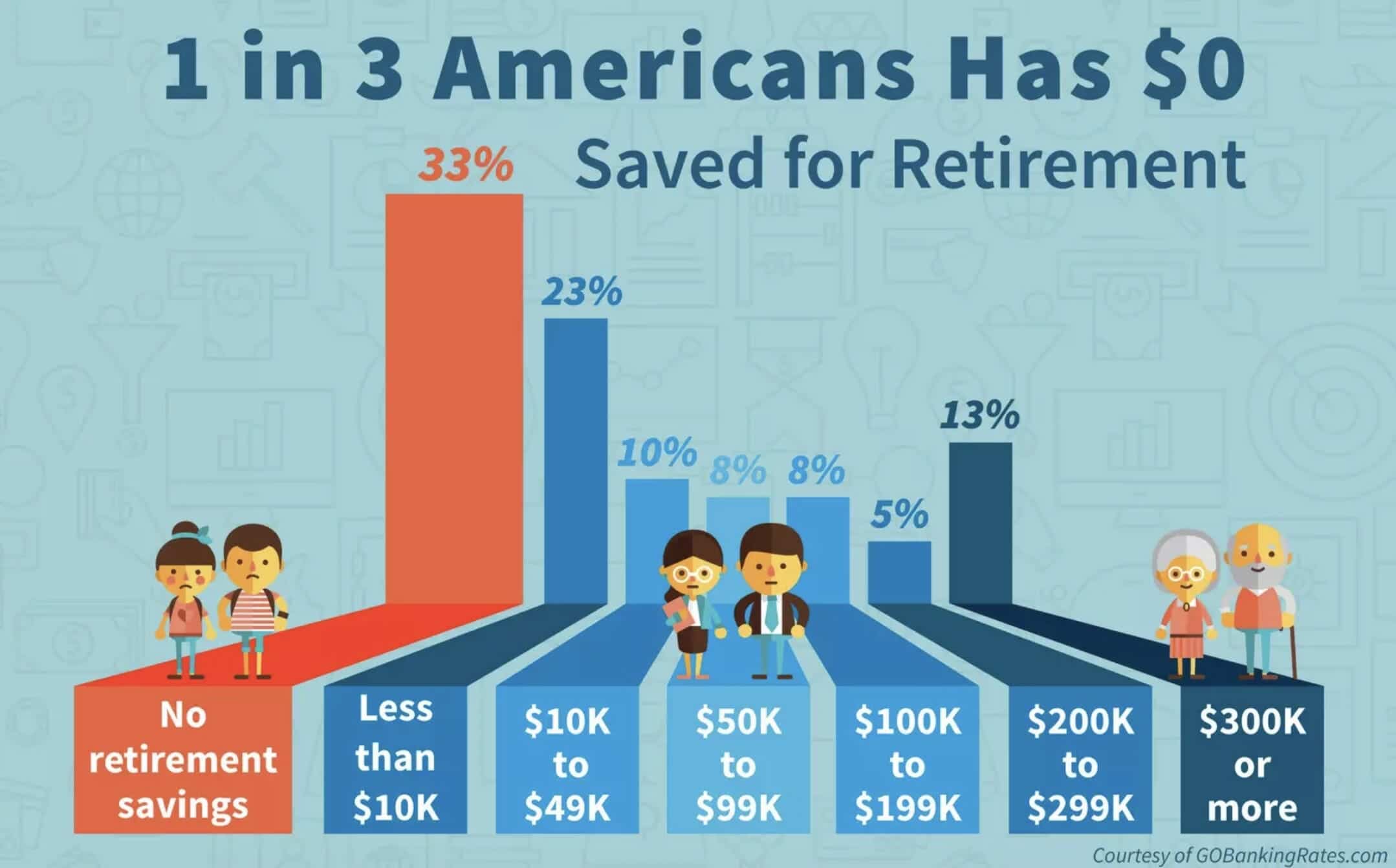

Did you know 1 in 3 Americans has $0 saved for retirement? Yeah, that’s a scary number.

And 56% of Americans have less than $10,000 saved for retirement and 74% have less than $100k saved for retirement. 100k may sound like a lot of money now but it’s nowhere near enough to retire.

If you’re young you still have plenty of time to save for retirement but, you’ll need to figure out how much you will actually need. You can’t just pull a number out of your butt.

And if you are already consistently saving for your future, how do you if you’re saving enough?

A good benchmark to follow is aiming to replace between 70% to 90% of your annual pre-retirement income through savings and Social Security.

For example, if you earn an average of $100,000 per year before retirement should expect to need $70,000 to $90,000 per year in retirement.

Want to know how much you need?

Go ahead, and give it a whirl.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Saving now is easier than saving later

It’s much easier to save money while you are young – you know, before the mortgage, 2.5 kids, and minivan payment. You are also more likely to get consistent raises or big bumps in your salary at the begining of your career.

Instead of upping your lifestyle every time you get a raise or bonus be smarter with the extra money.

Don’t even think of it as “extra money”. Pretend it’s not there.

That means holding out on getting your own place and living with your roommate a little longer.

That means going to your local dive bar with the great happy hour instead of the upscale cocktail lounges. Let us be honest – you’re going to drink the $16 cocktail the just as fast $6 beer.

That means packing your lunch instead of getting a $15 salad every day.

That means driving a beater car for a few more years instead of buying that Tesla. Your retired self will thank you.

Or better yet, move closer to work so you can commute to bike in. If you live in a city, don’t get a car unless you really need one. We use Zipcar, it’s so worth it. We save on car payments, gas, parking, and insurance.

The struggle is real

We get it. You have credit card debt, student loans, you’re overworked and underpaid but it doesn’t mean it’s impossible to save for retirement.

There are plenty of people who live on far less than you.

It isn’t easy to cut your expenses but if you are one of those people who have nothing saved for retirement get off the fancy salad line and start brown bagging your lunch.

We know, cutting a $15 salad or $4 coffee out isn’t going to change your life but you’ve got to start somewhere. It all adds up.

Try opting out 50% of the time.

If your friends meet for Bruch every Sunday opt-out time from to time. By going to brunch two times a month instead of once a week, you could reduce those costs by 50%.

Maybe you can eventually get down to once a month cutting that to 75%. Ok fine, now I’m pushing it.

The point is, you can still have fun in moderation. Plus those times you do go out will be more of treat.

The “It Was Only $20” Syndrome

How many times have you said this? I bet it’s more than you care to admit. If I had a dollar for every time I’ve said it, I would have a lot more than $20.

All those small purchases add up – for some of us (like me) they add up to A TON of money.

“It was only, like, twenty bucks.” – Me

What the problem was for me, when I started making more money, I thought about it differently.

When you are bringing in 2K a week the $5 coffee doesn’t really make a difference to you. Neither the $15 salad for lunch or the $40 for happy hour beers or the $25 for take-out (because let’s be real you’re not cooking after happy hour drinks) and the $15 Uber home.

That’s $100. Let’s say do this once a week. That’s $400 a month.

Think about how your college self would have viewed that $400……..

FOMO is real, real bullshit.

You’re the only one that sees yourself naked in the mirror. You see everyone else with their best foot forward. Few people of real wealth appear like they have wealth.

It’s cliche to mention Warren Buffet and living in his original house or his old car but the millionaire-next-door is very true. Savers save, spenders flaunt, don’t get caught up.

Peer pressure doesn’t end when high school ends; it just grows up. Even if your friends seem to have it together financially, their net worth could be a big fat $0.

You only see the stuff people want you to see, not what’s behind the scenes. What you see is most likely not the whole picture, and it definitely shouldn’t be the standard you live by.

Comparing yourself will lead to debt and dissatisfaction with what you already have.

Just because all your co-workers are going out to a happy hour doesn’t mean you have to. You don’t need to go out for all the birthday fiestas. Plus you work with these people all day, don’t you need a break from them?

Just because all your college friends are buying houses doesn’t mean you’re ready for that yet.

Just because all your friends are shopping for new designer handbags with their end of year bonus doesn’t mean you need to. That vintage Coach bag you found at the thrift store for $20 is way cooler.

You don’t have to keep up with your neighbors, co-workers, and friends. Everyone’s financial situation is different.

The Refrigerator Method

So, if you know you’re spending way more than you should and want to start saving money for retirement, you’ll need to figure out where all your money is going before you create a plan.

There a ton of budgeting apps that can help you see exactly where your money is being spent every month but if you want to go old school like us, try The Refrigerator Method.

Yeah, I know it sounds pretty cool, right?

Unfortunately, taping pieces of notebook paper to your fridge with your handwritten budget on it isn’t as cool as it sounds BUT, it has helped us cut our spending by 30%. Yes, 30%.

Maybe it’s working so well because we have to look at it every day or maybe it’s the task of physically writing down how much we spent that helped us but whatever it is, it’s working.

If you want to try it out, go grab a piece of paper and start by writing down your top spending categories. Leave space in between each so you can list your purchases underneath each category.

Here are ours:

- Groceries

- Restaurants and Take Out (includes coffee shops, lunch)

- Alcohol (wine for home, grabbing drinks with friends)

- Household/Personal Care Items (cleaners, razors, garbage bags, etc)

- Shopping (gifts, clothes, electronics, books, other toys)

- Miscellaneous (Zipcar, Uber)

*Note* We don’t include things like our mortgage and other utilities that are pretty much the same every month.

Next, decide how much you will spend in each category. For example, we allow $150 for groceries, $30 for personal care and $75 for alcohol and bar. Be realistic with your numbers. If you blow your budget in a couple of days you’ll become discouraged.

Now all you have to do is write down everything you spend in the appropriate categories. Simple as that.

One more rule. If you do go over budget in a category gets deducted from the next weeks budget.

So, let’s say you’re eating out budget is $100 and you have dinner with your college friends plus a birthday brunch for your sister in one week and you end up spending $135 on eating out. That -$35 get rolled over to next week so you will only have $65 to spend.

Fair? We think so. Try it for a week to see how you do!

Now for the good news

A significant number, 13%, of Americans’ have retirement savings of $300k.

The fact that so many Americans do have $300,000 or more saved for retirement goes to show just how easily the amount of money in your retirement fund can grow over time if you are dedicated to contributing regularly. -Kristen Bonner, GOBankingRates

You have time on your side when it comes to investing for your future. The earlier you start saving, the easier it is. With the power of compounding, if you start saving, even small amounts, on a consistent basis you could easily have enough for a comfortable retirement.