Personal finance has many facets, among which investing is perhaps the most daunting. Investing has its own specialized vocabulary and includes various types and methods of investments. Professionals often manage these investments, earning significant fees for their services. Perhaps the most intimidating aspect of personal finance is that investing directly impacts our financial security and future, highlighting the critical importance of informed and thoughtful financial strategies.

Investing is essential if you aim to increase your wealth, achieve financial goals, and ensure a comfortable retirement. Merely saving money is insufficient as it does not grow your funds to the same extent as investing can. Additionally, relying solely on Social Security for retirement is risky and likely inadequate to cover all expenses. Thus, proactive investment is crucial to securing your financial future.

While the government assures us that Social Security will be around when it’s time to retire, it’s best not to rely too heavily on others when planning how to live out some of the most vulnerable years of our lives. The average retirement benefit for a retired worker is roughly $22,884 per year as of January 2024.

Do you think you could live on less than $25,000 a year?

Anyone can learn the basics of investing. While it is possible to delve deeply into the subject, understanding the basics is sufficient to become a successful investor.

By the time you finish reading “Investing for Beginners”, you should have the knowledge you need to begin your investing journey. Don’t worry if you think that you don’t have enough money to start. The good news is, you can start investing with even a small amount of money. Some platforms allow you to invest with just $1 in fractional shares.

Ready? Good! Let’s get investing.

Why You Must Start Investing

Maybe you are a super saver. You are frugal and don’t live beyond your means. At the end of every month, you have a hefty sum left in your checking account which you promptly transfer to your savings account. Good for you! This puts you ahead of many other people.

According to Bankrate.com, only 44 percent of Americans would pay an unexpected $1,000 expense, such as a car repair or emergency room visit, from savings. That figure is consistent with the range of 37 to 43 percent seen in surveys from 2014 through 2023.

But saving money is not the same thing as investing money, and if you’re only saving and not investing, you’re making a big mistake. Don’t believe it? Let’s do a little math using an online calculator.

Examples of the Power of Compounding Returns

- An initial amount of $1,000 goes into a savings account and an additional $200 a month is added. The money earns 2% interest (which is low given current interest rates) and we leave it for 30 years.

- For the second calculation, the same numbers were used except for the interest rate which changed to 7%, the conservative average return you might expect over a long time horizon invested in the stock market.

This was the outcome:

- Savings account $100,366

- Investment account $252,111

That is the power of investing when it comes to growing your money.

What to Do Before You Invest

Create an Emergency Fund

If you’re not a super saver and are dealing with debt without any savings, there are essential steps to take before diving into investing. First, establish an emergency fund.

Ideally, this fund should cover three to six months’ worth of basic expenses. Building this can take time, so if you’re starting from scratch, aim first to accumulate $1,000. This amount will create a buffer between you and potential financial crises, providing peace of mind as you begin to navigate your investment journey.

By failing to prepare you are preparing to fail.

Tweet ThisFocus on cutting spending and making additional income until you save at least that first $1,000.

Accelerate your journey towards your financial aspirations with Premier Savings. Tailored to align with both your ambitions and lifestyle, this savings account offers an exceptional APY of 4.81% on balances exceeding $1,000. They value your hard-earned money by eliminating any monthly or annual account fees.

Manage Your Debt

We get this question a lot, “Should I invest if I have debt?” It’s a good question but there isn’t a “one size fits all” answer.

The first consideration is what kind of debt you have. If it’s high-interest debt like credit card debt, you should focus on paying that off first.

If you’re carrying a credit card balance, the high-interest rates can significantly eat into your finances. Since the average credit card interest rate is much higher than the potential return on conservative long-term investments (around 7%), paying off your credit cards should be a priority.

Consider a debt consolidation loan with a lower interest rate (depending on your credit score) to free up money for faster repayment. However, if you have a long time horizon, investing might be an option for future financial goals, but it carries some risk. It’s important to consult with a financial advisor to determine the best strategy for your situation.

Get your rate from every platform, for free, and it doesn't affect your credit. Rates as low as 3...

The exception to this rule is for those of you who can invest in an employer-sponsored 401k retirement account that offers to match. If you do, invest the minimum amount to get the matching because that is free money.

If you have low-interest debt like federal student loan debt (current rates are 5.50% to 8.05%), you should start investing while paying the monthly minimum on your student loans. Your interest rate is likely lower than the rate of return you can expect when investing, so the math does work out in favor of investing.

If your rate is higher, consider refinancing for a lower rate. And the same rule applies. If the new rate is under 5.5%, go ahead and invest while paying the minimum loan repayment amount.

Student Loan Refinancing Made Easy

Experience the freedom that comes with saving on your student loans and refinance today.

✔ Fast & simple application. Get pre-approved instantly.

✔ No fees. No origination fees or pre-payment fees.

✔ Lower your monthly payment. Multiple repayment options to fit your budget.

Fiscal flexibility that’s funny, free and delivered weekly.

Things You Can Invest In

This isn’t a comprehensive list but the basic things you can invest in as a new investor without doing a ton of learning.

- A stock is a small share of ownership in a company. Companies issue stock in order to raise money or pay off debt. The price of a stock depends on several factors, including a company’s performance and economic conditions.

- A bond is like a loan to a company or government entity. You’re paid back for the loan in a certain number of years and in the meantime, you earn interest. Bonds are less risky than stocks but less lucrative.

- Mutual funds are a variety of investments under the management of a company. You don’t choose the investments within the fund; the fund manager does that for you. This mix of investments provides diversity within your portfolio making mutual funds less risky than investing in individual stocks.

- ETF stands for exchange-traded funds, they are index funds, a basket of investments which can include stocks, bonds, and commodities. ETFs are bought and sold through a broker. An ETF provides diversification similar to a mutual fund and is easy to trade like stocks. Many people choose ETFs over mutual funds because the fees are usually lower.

- eREIT (electronic real estate investment trust) Looking to invest in real estate? eREITs allow you to start with as little as $500, unlike traditional methods that often require a much larger investment.

Retirement Accounts

- 401(k)– A 401(k) is an employer-sponsored retirement account that offers tax advantages. These plans typically allow you to choose from a variety of investment options, including mutual funds, stocks, and bonds.

- IRAs – (Traditional & Roth) offer tax benefits and let you invest in a variety of assets.

If you’d like to see how it all comes together, here’s one example of how you can build an investment portfolio using the above asset classes.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes.

This is a straightforward allocation that splits equally in five ways. Or, to see how diversified you can get, have a look at the Ivy 10 Portfolio.

How to Choose an Investment

Choosing investments depends on your time horizon, and how long before you need the money you’re investing.

- Short Term: This is the money you’ll need within the next five years for planned expenses like a vacation or a wedding. An emergency fund is also considered short-term because you need the money to be liquid, but it’s specifically set aside for unexpected events, not planned ones.

- Medium Term: This is the money you expect to need for goals like a down payment on a home or to purchase a rental property. You can generally invest with a slightly higher risk tolerance in this timeframe compared to short-term goals, but the specific risk you take might depend on your exact goal (e.g., down payment vs. other goals) and when you’ll need the money.

- Long Term: This is money you won’t need for at least a decade. Common long-term goals include retirement savings and college savings for your children. If you have access to a tax-advantaged retirement account like a 401(k) or IRA, prioritizing contributions to these accounts is a smart strategy to maximize your retirement savings. For college savings, there are various options to consider, including 529 plans that offer tax advantages for education expenses.

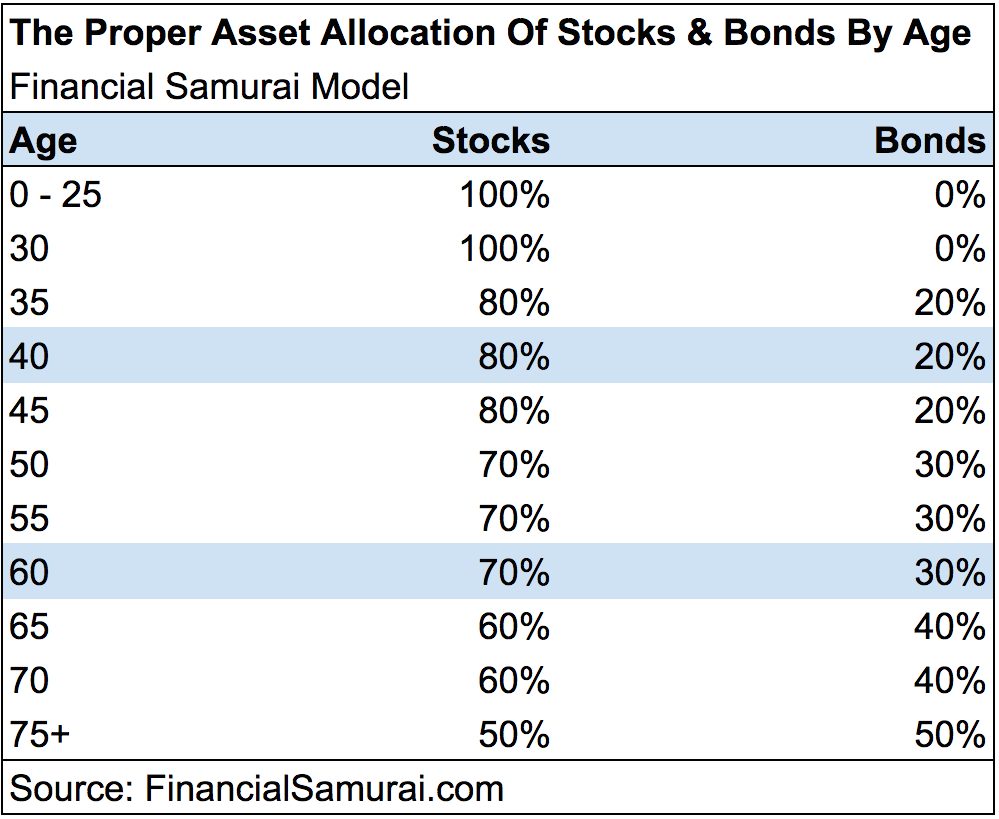

This money can also be invested in taxable accounts like an M1 or Vanguard account. This is a good rule of thumb allocation.

Real estate is another investment option for long-term money.

How Much To Invest

Well, the flippant answer is as much as you can, but that’s not realistic and not much fun either. Like so many things in the realm of personal finance, there is no definitive answer. But there are rules of thumb and tools to help you determine how much you should invest.

A rule of thumb is that the minimum you should invest is 10% of your net (after tax) income. We feel that 10% is an excellent start, but up to 30% of your net income is even better. Part of your decision will be goal-based too.

If you want to buy a home in an area with expensive housing prices, saving and investing 10% of your income may not be enough for a 20% down payment. You can play around with a calculator to get a ballpark number and base your saving and investing numbers on that.

The same is true for your retirement plan. It’s hard to predict decades out, but there are plenty of theories and calculators to help you plan. We like the 4% rule which is very straightforward, easy to understand, and according to its creator, a way to make sure you don’t outlive your money for at least 30 years.

Where to Invest Your Money

Great, you’re ready to start investing. These are the places to do it.

- Brokerage Account: If you want to buy stock in individual companies, you’ll need to open a brokerage account. You can do that with companies like Robinhood, Charles Schwab, or Fidelity. You need to do some research before buying stock in individual companies.

- Mutual Funds: You can buy a mutual fund directly from a mutual fund company like Dimensional Funds, BlackRock, or T.Rowe Price. They can also be purchased through some banks or brokerage firm.

ETFs: You can buy ETFs through companies like M1, Wealthfront, and Empower.

Investing for Beginners: Priorities

This list is not exhaustive, but it provides a foundation for those new to investing. The vast array of investment options can be overwhelming for beginners. However, it’s crucial to recognize the importance of starting your investment journey as early as possible, armed with the best available information.

Max out your 401k, especially if your employer offers to match. That match is free money. Do be mindful of the high fees some 401ks charge. If the fees are outrageous or your employer doesn’t offer a 401k, open an IRA.

This can help you choose between a Traditional IRA and a Roth IRA. For those who are self-employed, you can open a SEP IRA. These numbers change slightly sometimes, but the 2024 maximum you can invest in a 401k is $23,000, an IRA is $7,000, and a SEP IRA up to 25% of total compensation or $69,000 (whichever is less).

If you’ve done that and still have money to invest, open an

LMM Covers it All

We wrote Investing for Beginners to attract, you guessed it, beginning investors. We know how intimidating investing can seem, but we also know investing is essential if you want to build wealth. This article is a good appetizer and gives you enough information to get started investing.

But we have so much more, not just on investing but on pretty much any other aspect of personal finance you could think of. We cover budgeting, making more money, finding a job, dealing with debt, and every subject covered in this article but in much greater detail.

We want to teach people to take control of their finances on their own with no need to pay an expensive financial advisor. If you’re just finding us, join us. We want to be your financial friend for many years to come.

Show Notes

Andrew’s

Mint: The easy way to track your spending.

Legendary mutual fund pioneer John C. Bogle reveals his key to getting more out of investing: low-cost index funds. Bogle describes the simplest and most effective investment strategy for building wealth over the long term