Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Asset allocation is simple. Buy 2,000 shares of Tesla, 5,000 shares of Amazon, and put the rest in the hot stock tip you got last week. Now, sit back, relax, and watch your portfolio grow forever.

That’s obviously incorrect, but wouldn’t it be nice if it were that simple? But, contrary to popular opinion, asset allocation isn’t that complicated.

It’s not about picking the right stocks. It’s about diversifying your investments so you can make money in different ways.

A favorite allocation of Andrew’s here at Listen Money Matters is the Golden Butterfly Portfolio (more on that below).

Let’s dive in.

Understanding Asset Allocation

Before diving into the different types of portfolios, it’s a good idea to know how the pieces work when putting yours together. And it starts with asset classes.

What Are Asset Classes?

Each of the five categories above is a different asset class. In other words, each is a different type of investment.

Rather than putting all your money into individual stocks, like in the bogus example at the start, you’re spreading your money into multiple investment classes.

And there are plenty of asset classes to choose from. Here are a few examples:

- stocks

- bonds

- money market/cash equivalents

- real estate

- commodities

And each of the categories listed above can be further divided into subcategories. The point is to show you there are many ways to build a diversified portfolio.

What you need to focus on now is how much risk you’re willing to take and your time horizon. It starts with defining your financial goals.

Meet Your Investment Goals with Strategic Asset Allocation

Everyone has their investment objectives, which is why there’s no one perfect asset allocation strategy. But, there is a perfect strategy for you.

One that fits your risk profile and has the right mix of assets to get you out of the rat race at the perfect retirement age.

The best way to do this is to think about your desired time horizon. When do you want to spend your investments?

If you’re 25 years old and investing for retirement, you probably won’t need your investments for the next 40 years.

Because of that, your risk tolerance should be very, very high.

It shouldn’t matter if the market turns sideways now, tomorrow, or in ten years. You have enough time to ride out any volatility. Why?

Because, over the next 40 years, you’ll have generous investment returns. Enough to make up for any downs in the market along the way.

But maybe that’s not you.

If you’re saving up to buy a house, your time horizon is shorter, and your risk tolerance should be smaller.

You don’t want to see your investments cut in half by a market correction days before you close on your new home. You need that money in a safe, short-term investment.

So, what’s your goal? Is it long-term growth or short-term security?

If it’s the latter, you don’t need to diversify your investments; instead, check out a high-yield savings account. It’ll give you a modest return and keep that money safe.

But, if you’re looking for long-term gains, you have plenty of choices.

Fiscal flexibility that’s funny, free and delivered weekly.

What Should My Asset Allocation Be?

If you’re interested in the DIY approach, below are four excellent asset allocation strategies along with an easy way to determine what your allocation should be.

- Jack Bogle’s Stocks and Bonds Portfolio

- Ray Dalio’s All Weather Portfolio

- David Swensen’s Lazy Portfolio

- Tyler’s PinWheel Portfolio

Jack Bogle’s Stocks and Bonds Portfolio

One of THE best investors in history was Jack Bogle, founder, and chief executive officer of The Vanguard Group.

Jack grew up during the Great Depression and saw first hand how the markets could quickly go south. Because of this, he recommended a simple asset allocation to most investors: a mix of stocks and bonds.

To determine the right ratio for you, subtract your age from 110.

The answer is the percentage of your portfolio that should be in stocks and the remainder in bonds.

For example, if you’re 40 years old, the math would be: 110 – 40 = 70.

Your asset allocation could look like this:

- 70% in Vanguard’s Total Stock Market Index Fund (VTSAX)

- 30% in Vanguard’s Total Bond Market Index Fund (VBMFX)

If you’re feeling a bit more conservative, tweak the formula—use 90 instead of 110.

Or, if you want a more aggressive approach, use 130 as your starting point. The idea is to keep it simple.

Worried it’s too simple? Don’t be.

It’s a perfect method for most investors, especially those just starting. If you want more diversification in your portfolio, keep reading.

Asset allocation is easy; follow Jack Bogle's advice and subtract your age from 110.

Tweet ThisRay Dalio’s All-Weather Portfolio

Ray Dalio is the co-chief investment officer of Bridgewater Associates, a hedge fund with a reported 160 billion dollars under management.

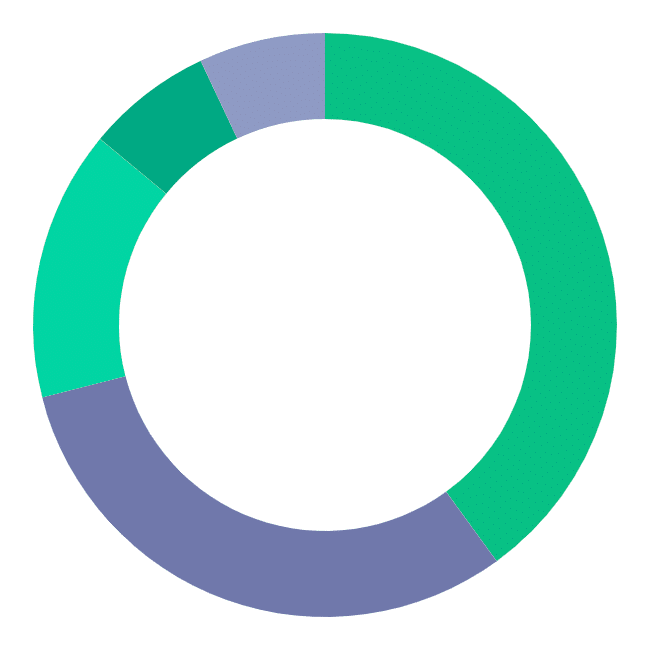

Thankfully, Ray openly shares his investment strategies and believes his All Weather Portfolio is the best asset allocation strategy.

Here’s what it looks like:

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

Commodities are basic goods traded on the open market like grains, gold, beef, oil, and natural gas. The easiest way to invest in commodities is to buy ETFs through a brokerage firm.

Golden Butterfly Portfolio

The Golden Butterfly is a less-pessimistic variation on the All-Weather Portfolio.

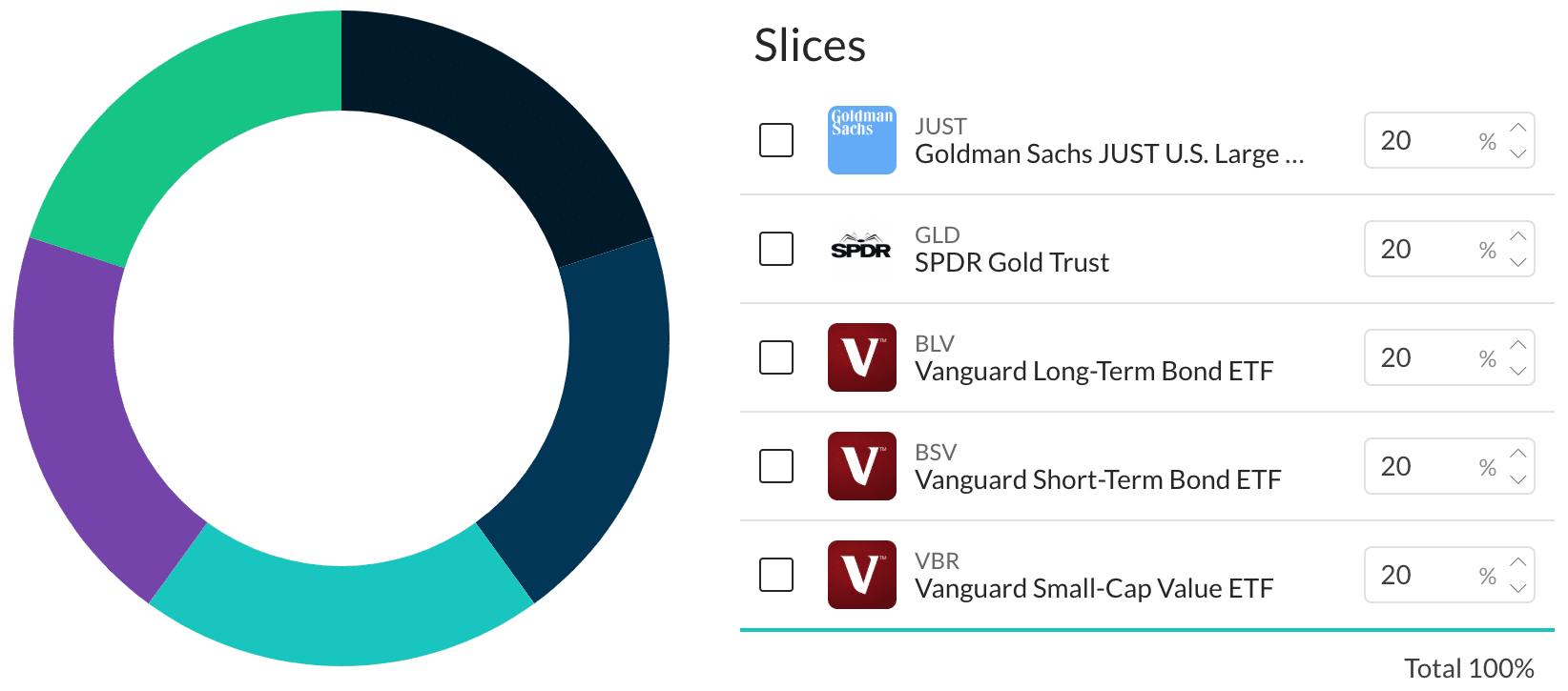

The above model is the Socially Responsible Investing alternative to the Golden Butterfly.

This portfolio is a modified version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

David Swensen’s Lazy Portfolio

Consider David Swensen’s Lazy Portfolio if the All-Weather Portfolio’s five asset classes aren’t enough. And don’t be turned off by its name.

His preferred asset allocation strategy looks like this:

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 30% | Total Stock Market | Stock |

| 15% | International Stock Market | Stock |

| 5% | Emerging Markets | Stock |

| 15% | TIPS | Intermediate Bond |

| 15% | U.S. Treasuries | Intermediate Bond |

| 20% | REITs | Real Estate |

David’s no slouch, he manages Yale University’s 29.4 billion dollar endowment and has been beating the market for years.

A contrarian investment approach that promotes a well-diversified, equity-oriented portfolio that rewards investors who exhibit the courage to stay the course. Swensen, creator of this portfolio is the mastermind behind the Yale Endowment investment strategy.

Treasury Inflation-Protected Securities (TIPS) is a bond issued by the US Government indexed to inflation.

The principal value of a TIP rises as inflation rises, so you’ll never lose your initial investment and pays out interest twice a year.

It’s not a way to get rich, but it is a low-risk way to invest your money.

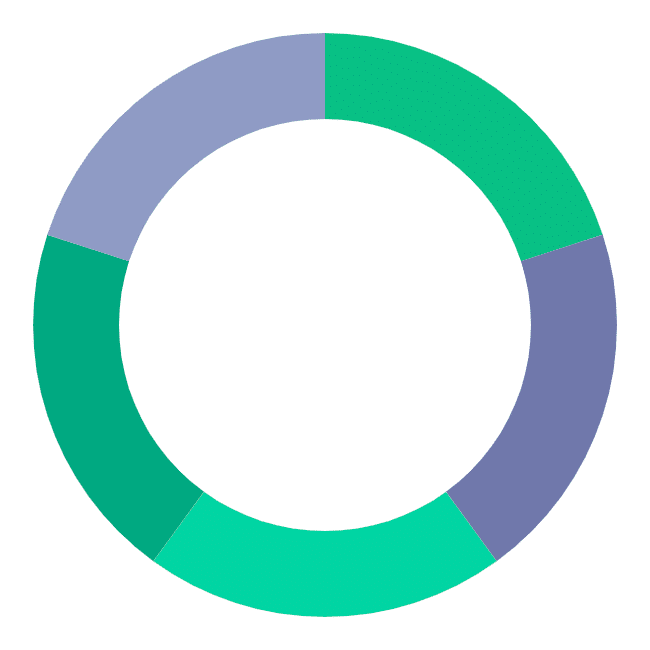

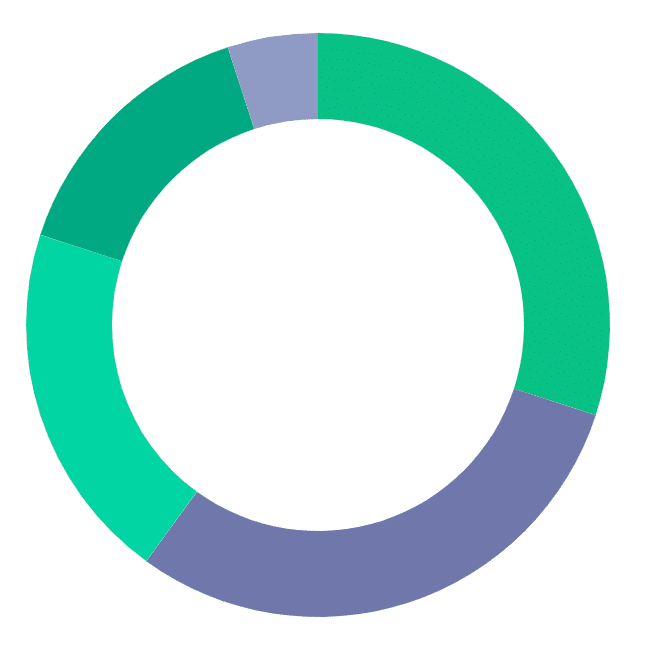

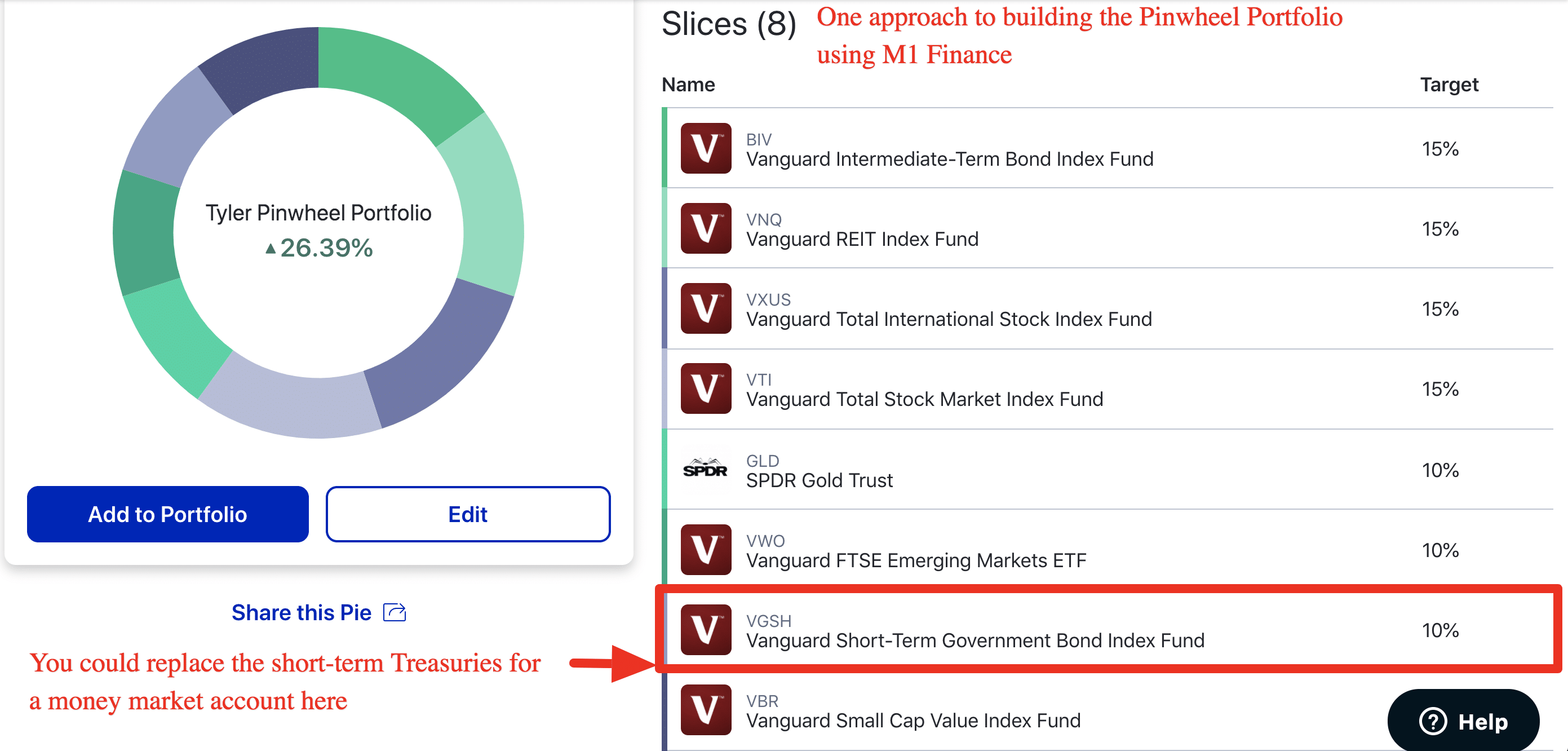

Tyler’s Pinwheel Portfolio

Perhaps six asset classes aren’t enough for you. If that’s the case, consider the Pinwheel Portfolio.

The Pinwheel's approach is to equally hold the four most common asset classes found in professionally-recommended portfolios. It then seeks to complement those four with strategically picked securities to both enhance returns and mitigate risk.

Tyler created this asset allocation strategy over at PortfolioCharts.com, and, if you’re curious, Tyler prefers to remain somewhat anonymous, which is why his last name isn’t widely known.

But his methods are, especially the Pinwheel Portfolio, which looks like this:

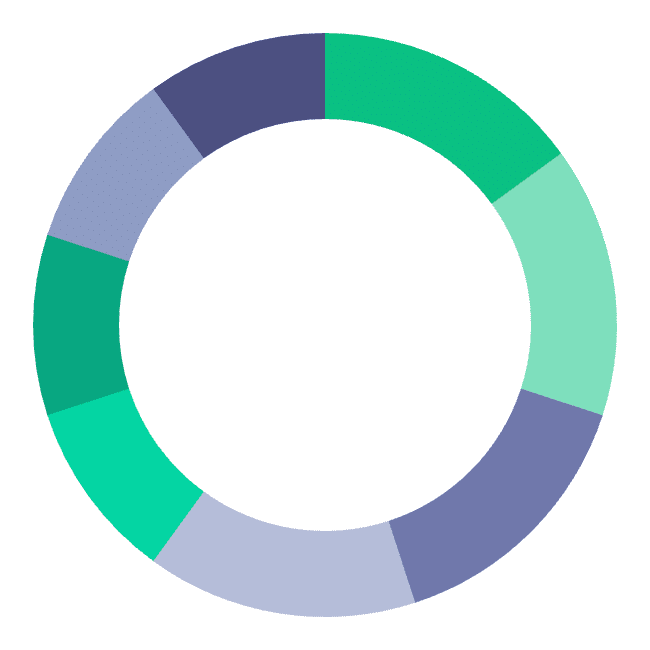

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 15% | Total Market | Stock |

| 10% | Small-Cap Value | Stock |

| 15% | International Developed Market | Stock |

| 10% | Emerging Market | Stock |

| 15% | Intermediate Treasuries | Bond |

| 15% | REITs | Real Estate |

| 10% | Gold | Precious Metals |

| 10% | Money Market | Cash |

Real Estate Investment Trusts (REITs) are like a mutual fund with real estate as its asset rather than stocks and bonds.

Most REITs are publicly traded like stocks purchased through a brokerage firm. Or you can invest directly with a company like Fundrise.

In the asset allocation table, you could choose to use short-term Treasuries (as opposed to a money market account) as your cash-equivalent when building your portfolio.

The idea behind these models is the flexibility the interchangeable components provide to DIY-investors.

Why Asset Allocation Is Important

Mixing asset classes through portfolio diversification is an excellent way to reduce your risk, keep costs low, and avoids market-timing.

What you need to decide is how much risk and diversification you feel comfortable with. Remember, there’s no one best strategy.

Any of the methods listed above will work. There are differences, and each one’s performance will vary depending on economic conditions.

Choosing one over the other isn’t going to make or break you. What will, is failing to choose.

If you’re disciplined and consistent, the market will reward you over time. You can always switch to a different asset allocation strategy in the future.

Maintaining Your Target Asset Allocation

You’ve picked your allocation strategy; now what? You can’t sit back and forget about it, because over time two things will happen:

- You’re going to get older

- Your investments will grow at different rates

Portfolio Rebalancing

Over time your investments will grow. Because you’ve allocated your investments in a wide variety of asset classes, not everything will grow equally.

For example, if the stock market does well, the percentage of your portfolio in stocks will also increase. It might look like this:

| January | April | July | November | |

|---|---|---|---|---|

| Stocks | $7,000 (70%) | $8,500 (73%) | $9,700 (75%) | $11,500 (78%) |

| Bonds | $3,000 (30%) | $3,100 (27%) | $3,200 (25%) | $3,300 (22%) |

| Total | $10,000 | $11,600 | $12,900 | $14,800 |

You’re making money. But, if you planned to keep a 70/30 stock to bond ratio, you’re now out of alignment, and you need to fix it.

To do so, you have two options:

- Sell some stock (your winners) and use the proceeds to buy more bonds (your losers)

- Alter your contributions to put more money into bonds until you’re back at a 70/30 mix

And it might seem wrong to sell off part of an investment that’s doing well, but remember, you have no idea what will happen next week, month, or next year.

Maybe the stock market will tank and bonds will earn more money. The point is you don’t know.

And the last thing you should be doing is stock picking because it’s a recipe for disaster.

Change your perspective. You’ve made money, and that’s fantastic. Now protect your gains by sticking to your plan.

Keep your asset allocation properly aligned.

Take Less Risk with Age

Let’s talk about aging. Like it or not, we’re all getting older. And the older you get, the less risk you want in your investment portfolio. Why?

Because when you retire, you’re going to need that money. And the last thing you want is to run out of it.

You don’t want to be forced to return to work when you’re 80.

Think about it this way; let’s pretend you’re 60 and ready to retire. And you’ve got a million dollars invested

You’re ready to spend it on a sailboat and a life of leisure. You quit your job, buy your boat, and then WAM! The stock market collapses.

If you’re heavily invested in stocks, you’ve lost a ton of your savings. And even if you’re healthy, you probably won’t have enough time to make up the losses.

Plus, since you’re on a fixed income, you have less money to spend on your day-to-day expenses.

But, if you shifted your portfolio from the high-risk stock market into a lower risk investment like bonds, it will protect you from sudden dips; a collapse will have less impact.

Shift from Stocks to Bonds

That’s why most financial advisors recommend you slowly shift your investments from high-risk categories to lower risk categories as you age.

A stock-to-bond ratio is the easiest way. Here’s what it would look like:

| Age | 30 | 35 | 40 | 45 | 50 | 55 | 60 |

| Stocks | 80% | 75% | 70% | 65% | 60% | 55% | 50% |

| Bonds | 20% | 25% | 30% | 35% | 40% | 45% | 50% |

When you’re 30, subtract your age from 110 to determine you should have 80% of your investments in stocks (110 – 30 = 80). But when you’re 60, it should be closer to 50% (110 – 60 = 50).It’s not rocket science. It’s based on the 110 number we used above.

Don’t overthink this.

You’ve worked hard for your money, so protect it. Over time, shift your hard-earned cash into safer asset classes so you’ll have it when you need it.

When Should I Rebalance?

Rebalance every six or twelve months like clockwork. Rebalancing shouldn’t be something you do on a whim. And it shouldn’t be something based on market conditions.

Pick a time frame that works best for you, stick it on your calendar, and do it every single time (without fail).

Otherwise, the market is going to do what it does. It’s going to fluctuate and throw your investments out of alignment.

If you don’t stick to the plan you’ve chosen, what was the point of picking a plan at all? Asset allocation works well when you do the work.

But what if I’m lazy and don’t want to rebalance?

You’ve got two options if you want a hands-off approach to both asset allocation and regular rebalancing:

- Target-date funds

- Robo-advisors

What’s a Target Date Fund?

Target Date Funds are products sold by the major investment companies (Vanguard, Fidelity, Schwab, etc.) that automatically readjusts your investments over time to align with your desired retirement age.

It’s a great option because you only need to purchase a single fund.

You put the money in, and the fund does the work of locating different asset classes for you and properly rebalancing them.

These funds are easy to find. Most have names with your desired retirement year built into the title.

For example, here are a few of Vanguard’s Target Date Funds:

- Vanguard’s Target Retirement 2045 Fund (VTIVX)

- Vanguard Target Retirement 2050 Fund (VFIFX)

- Vanguard Target Retirement 2055 Fund (VFFVX)

If you wanted to retire in 2050, then you’d buy that fund and keep contributing to it over time.

There is a small fee charged by the investment firm to do all the work, but typically, it’s low. Currently, Vanguard charges 0.15% on its 2050 fund.

That’s a small penance compared to hiring a financial advisor (or taking the DIY approach and forgetting to do the work).

What’s a Robo-Advisor ?

Robo-advisors are similar to target-date funds, but instead of a human at the controls, the work is turned over to a computer algorithm.

It means your investments are monitored 24/7 by a machine to maintain the perfect alignment with your goals.

Not all Robo-Advisors are created equal, so you’ll want to do your homework before investing in one.

If you do, take a look at things like:

- minimum balance requirements

- management fees

- tax-optimized portfolios

Tax-loss harvesting sells an investment at a loss to reduce the amount of tax you pay. If you do this well, you can save yourself money each year by claiming your losses and pay less in taxes.

Here are four popular robo-advisors and how they stack up:

Minimum Investment:

$0

Management Fees:

0.25%

Promotion:

Invest free for up to 1 year

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$21 billion

Minimum Investment:

$0

Management Fees:

0.5%

Promotion:

Get your first $10,000 managed free

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$13B

Minimum Investment:

$100,000

Management Fees:

0.49% - 0.89%

Promotion:

Join for Free

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$12B

Minimum Investment:

$0

Management Fees:

$0

Promotion:

Low cost investing

Tax Loss Harvesting:

No

Portfolio Rebalancing:

Yes

Assets Under Management:

$1 billion

Just know that most of these companies are fairly new. For example, M1 Finance opened in 2015.

If that makes you uncomfortable, consider checking out a robo-fund at one of the major investment firms. Here’s three to get you started:

- Fidelity Go

- Charles Schwab Intelligent Portfolios

- Vanguard Personal Advisor Services

What’s Next?

You now know all about asset allocation. Since you read this entire article, you probably know more than 99% of the public.

Now you need to use it.

If you’re not following a specific allocation strategy, you’re not investing as well as you could. So pick a path, open up a new tab in your browser (right now), and get to work.