You’ve heard the term diversification, but you might not know what it means. It’s more complicated than merely owning stocks and bonds. Portfolio diversification isn’t just a financial advisor’s fancy term; it’s an integral part of any long-term investment strategy.

You don’t have to have a Ph.D. in finance or spend hours researching a single stock to understand the basics of portfolio diversification.

While diversifying your investment portfolio is a little more complex than only owning two types of assets, it’s by no means difficult for individual investors to do themselves.

Understanding diversification may also help alleviate the fear that people have around investing in the stock market. That fear prevents millions of people from investing at all.

In the U.S., fewer than 52% of households own stock. Of the top 10% of income earners, nearly all of the 94.7% own stock. Of the bottom 19.9%, only 11.6%.

Most of us are not going to earn enough from our jobs to grow our wealth. Some of us won’t even make enough from our jobs to ever be able to retire.

That is the real risk, not investing. Investing is the only way most of us can achieve our financial goals and retire with enough money to last us for the rest of our lives.

So whether you don’t understand portfolio diversification or you’re afraid to invest, this article is just what you need.

What Is Portfolio Diversification?

Diversification simply means having a wide variety of assets in your portfolio. Owning stock in a single company means you have zero diversification.

It’s the riskiest thing you can do with your portfolio. It’s even more precarious if that stock is in the company you work for.

If the company were to go under, you’d lose your job, and the stock would be worthless.

A diversified portfolio would contain stocks across different sectors and economies, bonds, real estate, alternative investments, and cash or cash equivalents.

Diversification Benefits

Part of successful investing is risk management. Generally, you can expect higher returns from stocks than other asset classes.

Still, a portfolio containing only stocks or too heavily weighted towards stocks puts an investor at tremendous risk during a stock market crash and significant market volatility.

When you have the right diversification strategy, you are at a lower risk of having your portfolio wiped out.

Returns are the name of the game; diversification exposes you to more profit potential. Lack of diversification means you lose out on the growth opportunities available when you hold various asset classes.

Into Every Portfolio Some Risk Must Fall

If you aren’t willing to accept some risk when it comes to investing, you aren’t going to make any money. So how do you determine how much risk to take?

Goal-Based Investing

The longer your money is going to be invested, the more risk you can afford to take. An investment started to help you save money to buy a home is going to look very different from one meant to fund your retirement.

The home investment will have a shorter timeline, and all the money will be used in one fell swoop. The retirement investment will be invested for many years and spent down over a long period.

The further away from your goal, the more risk you can take.

Weathering Storms

When the stock market and economy take a downturn, people get nervous, especially when thinking back to 2008-2009.

With home prices tanking, the report estimates a $7 trillion loss in the real estate industry. The stock market decline has brought another $11 trillion in losses, and retirement accounts have lost $3.4 trillion.

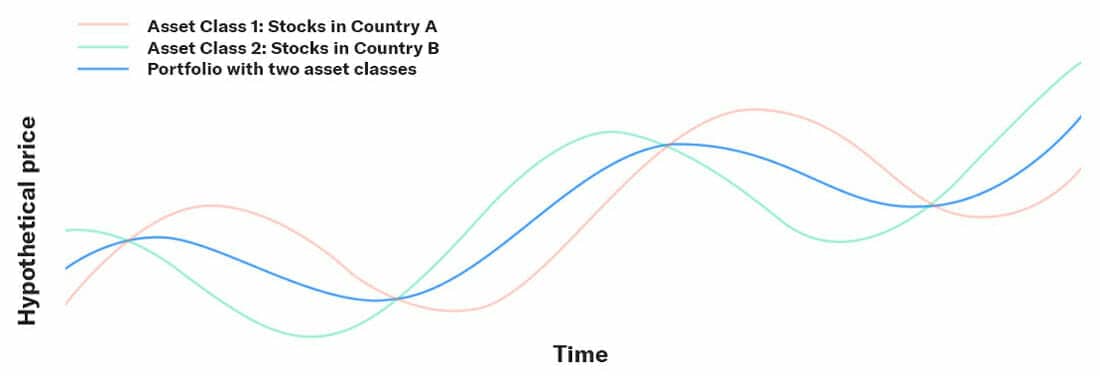

You can weather the inevitable storms by being diversified among asset classes, sectors, and countries. While the last significant recession impacted most sectors and most of the world, not all sectors and economies move in lockstep.

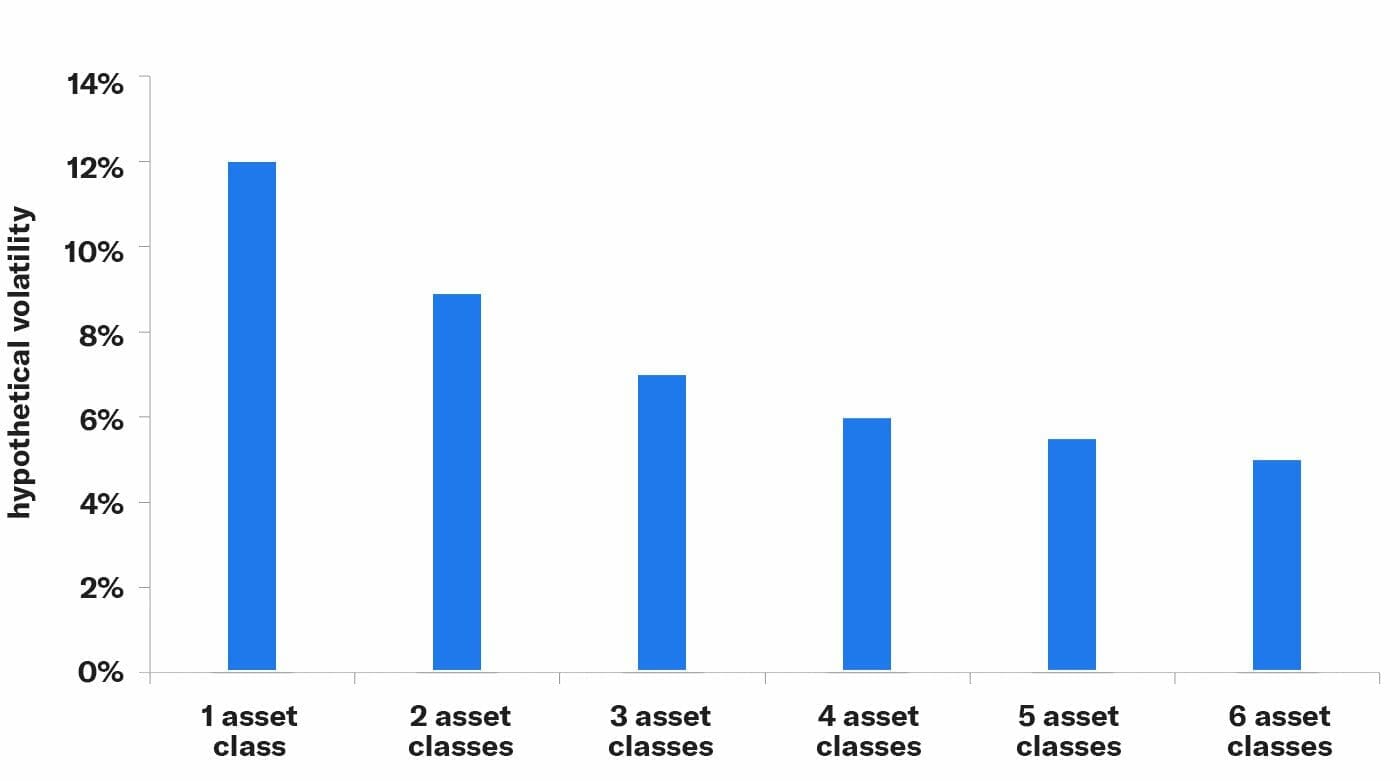

The volatility of a portfolio reduces as you increase the number of asset classes.

Another way to protect your portfolio is by rebalancing.

Your portfolio has a specific asset allocation. An example would be 50% stocks and 50% bonds. That allocation can change. If bonds are doing well and stocks are doing poorly, your allocation is no longer 50/50.

To rebalance, you need to sell off some of your assets and buy some others to bring your portfolio back into balance.

If you have $500 in stocks and $500 in bonds and you lose $100 in stock value, you take $100 from your bonds and buy stock. Why would you take money from something doing well and put it into something doing poorly?!

Rule #1 of investing is to buy low and sell high.

Stocks are low, so now is the time to buy. Bonds are high, so now is the time to sell. Allow periodic rebalancing to account for “drift” in your portfolio.

Maintain the goal-based asset allocation you started with (adjusting based on a diminishing time frame) and don’t let losses and gains determine your allocation.

Fiscal flexibility that’s funny, free and delivered weekly.

How Diversified Should My Portfolio Be?

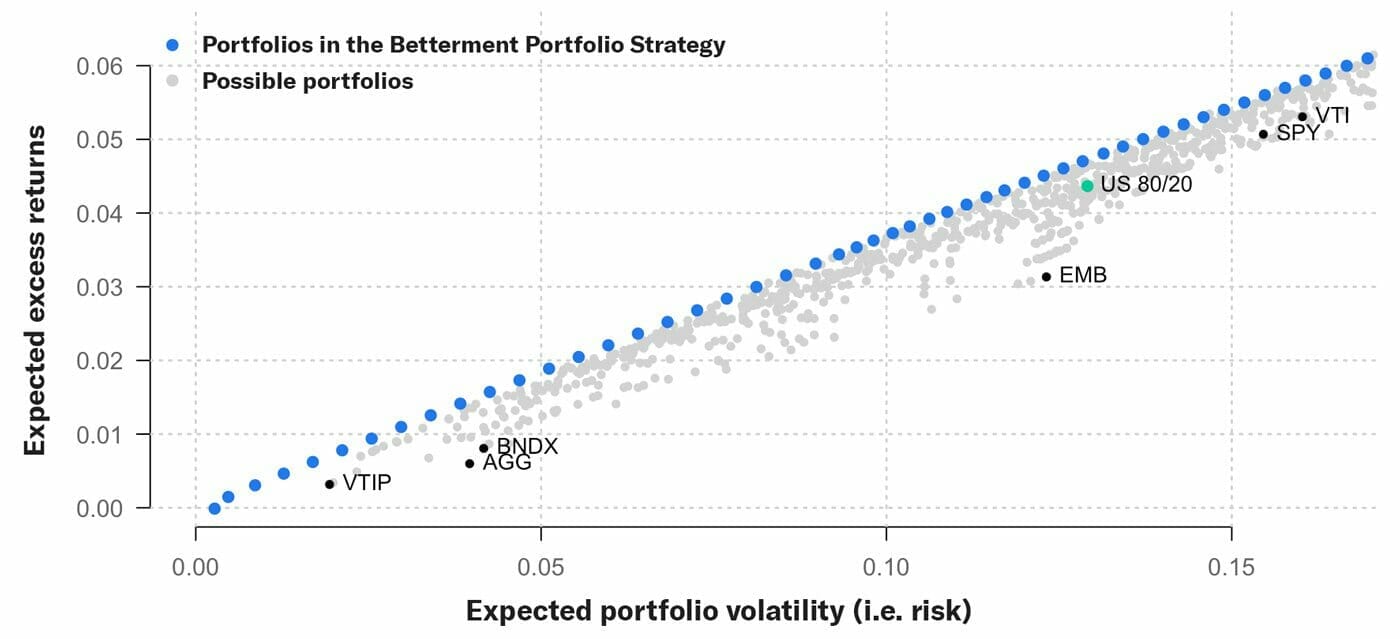

The Efficient Frontier

The efficient frontier starts with the concept that risk and return are related, that risk is bad, and returns are good. Then as we mix assets that don’t entirely move in lockstep, we can reduce risk without adversely impacting returns.

The efficient frontier is the outer boundary of how much return you can get for any level of risk. U.S. stocks and bonds, when mixed, have less risk.

How much extra stuff can you add before you reach the limit of a healthy mix of risk and return? Ideally, your portfolio is at or near the efficient frontier.

Staying on the efficient frontier allows you both to take advantage of that volatility and insulate from it.

Finding the Frontier

How is this calculated? When investing, future risk and returns are what’s important. This next part gets technical and is from the

To compute forward-looking returns, we use the Capital Asset Pricing Model (CAPM), which assumes all investors aim to maximize their returns and minimize volatility while holding the same information.

Under CAPM assumptions, the global market portfolio is the optimal portfolio. We know the weights of the global market portfolio and can reasonably estimate the covariance of those assets, we can recover the returns implied by the market.

This relationship gives rise to the equation for reverse optimization:

μ = λ Σ ωmarket

Where μ is the return vector, λ is the risk aversion parameter, Σ is the covariance matrix, ωmarket is the weights of the assets in the global market portfolio.

By using CAPM, the expected return is determined to be proportional to the asset’s contribution to the overall risk.

It’s called reverse optimization because the weights are taken as a given, which implies returns the investors expect.

CAPM does rely on several limiting assumptions: e.g., a one-period model, a frictionless and efficient market, and the assumption that all investors are rational mean-variance optimizers.9

To complete the equation and compute the expected returns using reverse optimization, we need the covariance matrix as an input. Let’s walk through how we arrive at an estimated covariance matrix.

The covariance matrix mathematically describes the relationships of every asset with each other and the volatility risk of the assets.

Our process for estimating the covariance matrix aims to avoid skewed analysis of the conventional historical sample covariance matrix and instead employs Ledoit and Wolf’s shrinkage methodology.

It uses a linear combination of a target matrix with the sample covariance to pull the most extreme coefficients toward the center, which helps reduce estimation error.10

Thank you, Adam!

The Uncompensated Risk Gap

You need to take enough risk when you invest to grow your wealth without taking so much risk that you put that wealth into an unnecessary amount of jeopardy.

As we wrote earlier, into every portfolio, some risk must fall. But there is a difference between compensated and uncompensated risk. A compensated risk is one that, when taken, will increase your returns (although nothing is guaranteed when it comes to investing).

An uncompensated risk is one that won’t increase and can even decrease your expected returns. No one should knowingly take an uncompensated risk. So how do you avoid them? By diversifying.

How to Diversify Your Portfolio

I promise all of the above is the complicated part, and frankly, you don’t have to understand any of it to create a diversification strategy. That information was to explain the importance of diversification and how it helps lower risk for investors.

Now let’s go into the much more straightforward explanation of how you can diversify your portfolio.

Multi-Layer Portfolio Diversification

One layer of diversification is to buy stock in more than one company but in the same sector. You only had stock in Apple, so you decide to buy stock in Microsoft. That is one layer. You have stock in more than one company but the same industry.

But both those companies are in the same sector, technology and the tech sector is not doing well. You’re still not diversified enough.

A second layer of diversification would be to buy stock in a different sector, so you purchase stock in Pfizer and Novo Nordisk, those are in the healthcare sector. Tech is not doing well, but healthcare is.

Great, you are more diversified. But where are all those companies based? In America so your portfolio only contains U.S. stocks. In fact, 40% of all stock dollars invested are invested in U.S. companies.

To further diversify, you need investments outside of the U.S. in foreign stocks from international developed and emerging markets.

Real Estate

Investing in real estate is a great way to add diversity to your portfolio.

When the value of stocks and other traditional assets decline, the value of real estate investments may actually rise.

Rental property is a great way to invest in real estate, but not everyone wants to get into the landlord business, and not everyone has the money to buy a

If that’s true for you, you can still add real estate to your portfolio with a REIT. REITs are Real Estate Investment Trusts.

A REIT is a company that owns, operates, or finances income-generating real estate. They’re similar to mutual funds in that they pool money from lots of investors.

Exchange-Traded Funds and Mutual Funds

Exchange-traded funds or ETFs and mutual funds are an easy way for investors to achieve diversification.

An index fund, be it an ETF or mutual fund that tracks a broad market index, can lower risk when compared to buying individual stocks because the money is being invested in a broad swath of the entire market.

No invention has been more disruptive to the asset-management industry in the last quarter-century than the exchange-traded fund.

Tweet ThisWhen you invest with an ETF like

An appropriate and diversified portfolio will be recommended to you.

Alternative Assets

Alternative asset classes are things outside the things most of us think about when we think of investments (typically stocks and bonds).

Different assets that can be classed as alternative assets include private equity funds, venture capital investments, intellectual property, precious metals, collectibles, and cryptocurrencies.

Diversified Portfolio Examples

If you don’t feel confident enough to cobble together your own diversified portfolio, good news! The work has been done for you.

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

The All-Weather Portfolio was created by legendary hedge fund manager Ray Dalio and introduced to the wider public by Tony Robbins’ personal finance book Money Master the Game.

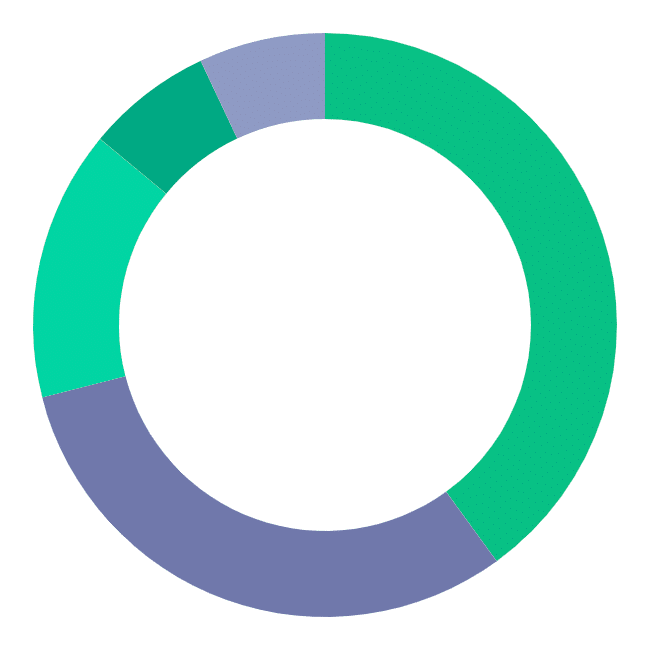

The portfolio is a diversified asset mix meant to weather any kind of economic climate. The asset allocation looks like this:

- 40% Long Term Bonds

- 30% Stocks

- 15% Intermediate-Term Bonds

- 7.5% Gold

- 7.5% Commodities

Bridgewater Associates offers an All-Weather Fund that is based on risk parity strategy. Because stocks are three times more volatile than bonds, the amount of risk in a portfolio is determined by that 3:1 ration.

Each asset class contributes an equal amount in risk terms, not dollar terms.

This portfolio is a modified version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

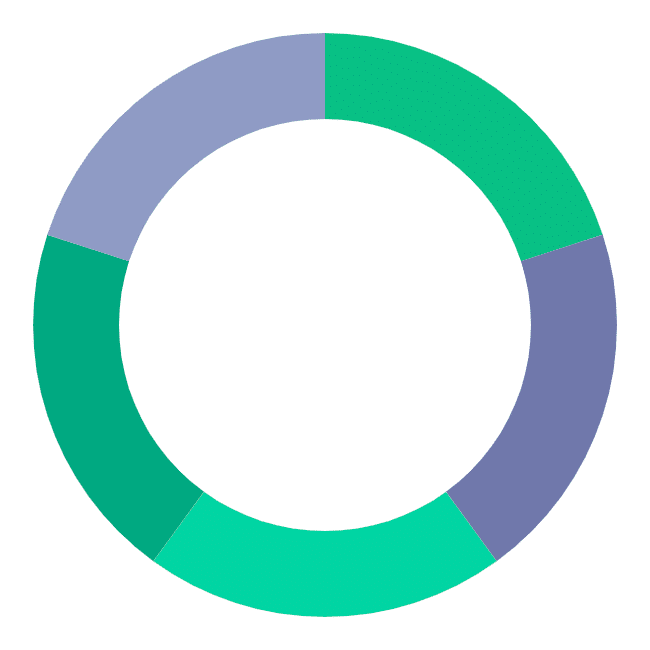

Tyler of PortfolioCharts.com created the Golden Butterfly Portfolio.

He describes it this way:

The Golden Butterfly is essentially a modified Permanent Portfolio with one additional asset class that incorporates some of the characteristics of a few other notable lazy portfolios.

The All-Weather Portfolio is agnostic about the stock market, but the Golden Butterfly is more optimistic.

And over time, we have had more periods of economic growth than periods of decline and recession.

This is the asset breakdown for the Golden Butterfly:

- 20% Domestic Large Cap Fund

- 20% Domestic Small Cap Value

- 20% Long Term Bonds

- 20% Short Term Bonds

- 20% Gold

Diversity Is Always a Good Thing

You should diversify lots of areas of your life; friends, interests, hobbies, and of course, your portfolio. Whether you want to create your own from the ground up or just assemble one that’s already been created, portfolio diversification isn’t as hard as you think.