Did you know that Harvard has a 37 billion dollar endowment? That’s a crazy amount of money. And to be clear, that’s billion with a capital ‘B.’

Harvard isn’t alone. All of the eight Ivy League Schools have multi-billion-dollar endowments at their disposal and they’ve generated some impressive returns over the years.

Take Harvard for example. In 2018 its endowment earned a 10% annual return. That’s 3.7 billion dollars!

Why they still charge tuition is beyond me.

The world’s top investment advisors actively manage Harvard’s endowment (and the rest of the Ivy League’s).

So it’s worth looking at the moves they make to learn from their successes (and failures).

Thankfully, schools like Harvard openly share their investment strategies. And while you and I may not be able to invest like they do (more on this below), the Ivy Portfolio creates an asset allocation strategy you can implement right now.

What Is The Ivy Portfolio?

The Ivy Portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds.

It’s a way for individual investors to emulate the asset allocation strategies used by Ivy League Universities. The Ivy Portfolio doesn’t attempt to mirror every move the endowment fund makes.

That’s impossible.

What’s possible is to copy their asset allocation strategies.

And using a diverse set of asset classes is the backbone of the endowment’s methodology. Because they’re not looking for huge gains.

They don’t need them!

They’ve already got billions of dollars at their disposal. What they need are safe, reliable returns, with minimal risk.

That’s what The Ivy Portfolio attempts to do. It’s focused on protecting your money and earning steady returns in both bear and bull markets.

To do that, you have a choice between two different versions of the portfolio: (1) the Ivy 5; and (2) the Ivy 10.

Both have the same overall diversification, but Ivy 10 breaks things further into more specific asset classes.

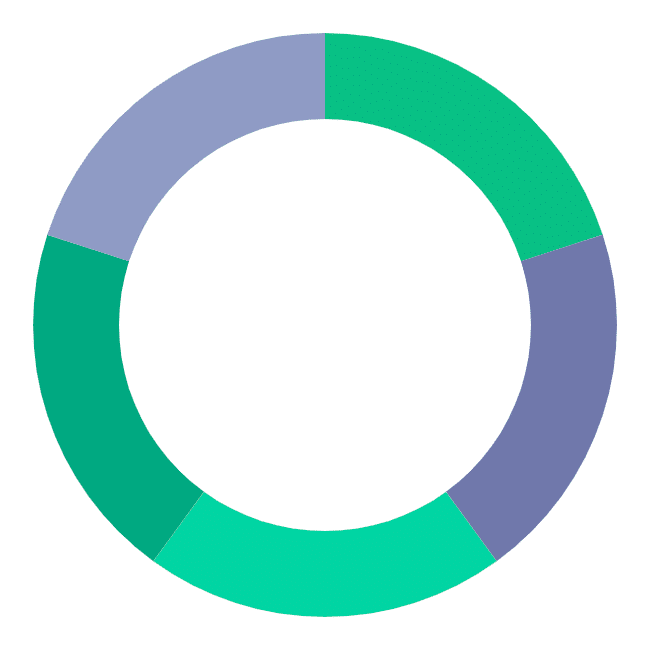

The Ivy 5’s Asset Allocation

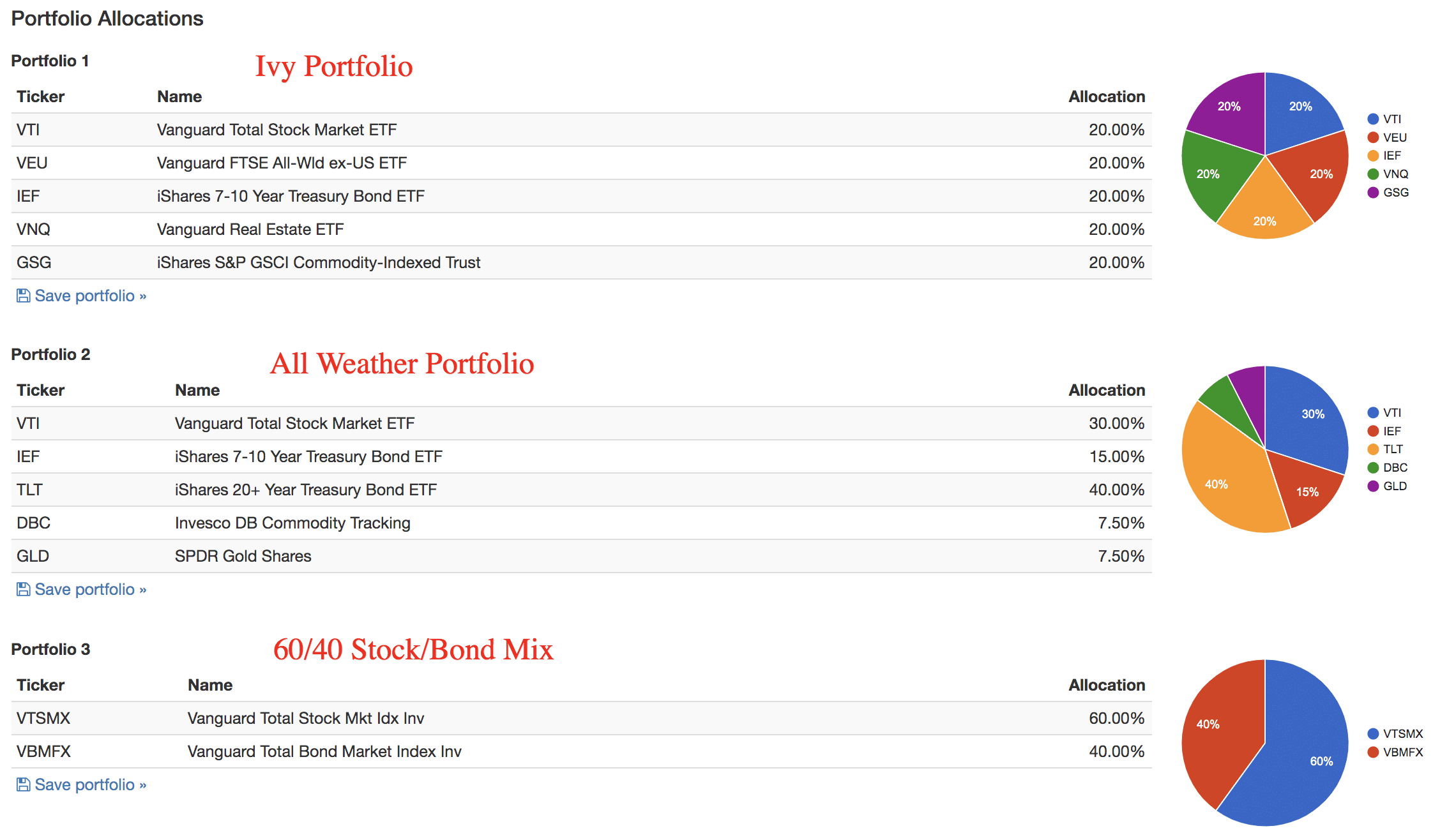

Here’s a breakdown of what the allocation looks like for the Ivy 5.

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 20% | U.S. Total Stock Market | Stock |

| 20% | Global International Stock Market Fund ex U.S. | Stock |

| 20% | U.S. Total Bond Market | Bond |

| 20% | Diversified Commodities | Commodity |

| 20% | U.S. REITs | Real Estate |

The Ivy 5 splits its allocation evenly five ways using two stock funds, bonds, commodities, and real estate.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes.

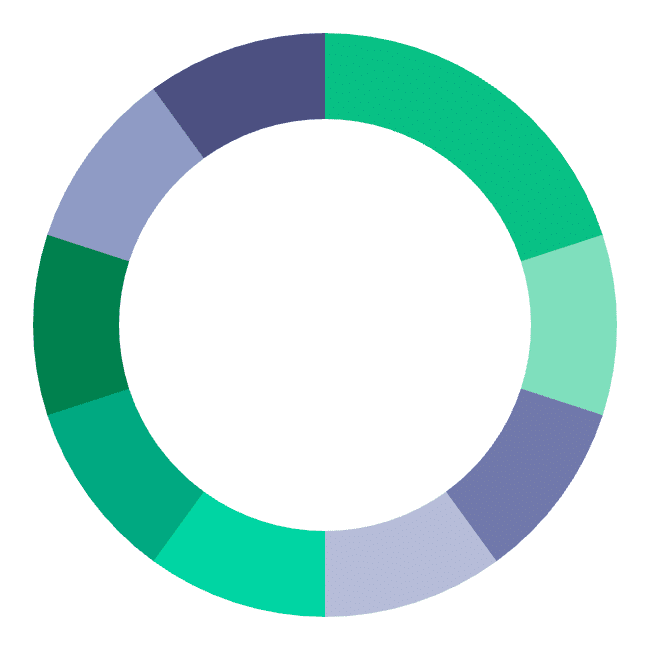

The Ivy 10’s Asset Allocation

The Ivy 10 gets more granular with its construction as it further divides the stocks, bonds, and real estate into several pieces.

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 10% | U.S. Large Cap | Stock |

| 10% | U.S. Small Cap | Stock |

| 10% | International Developed Blend | Stock |

| 10% | Emerging Markets | Stock |

| 10% | Total U.S. Bond Fund | Bond |

| 10% | TIPS | Bond |

| 20% | Commodities | Commodities |

| 10% | REITs | Real Estate |

| 10% | International REITs | Real Estate |

The Ivy 10 really should be called the Ivy 9, since it only has nine asset classes. But, who are we to judge.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes. This is more specific than the Ivy 5.

Who Created The Ivy Portfolio?

Mebane T. Faber and Eric W. Richardson created the portfolio in the book, The Ivy Portfolio: How to Invest Like the Top Endowments and Avoid Bear Markets.

Meb Faber is the driving force behind this strategy.

He’s the co-founder and chief investment officer at Cambria Investment Management, an independent, privately-owned investment firm focused on quantitative asset management (more on that in a minute).

He’s also the author of half a dozen investing books.

A word of warning, The Ivy Portfolio book is a great resource, but it’s not a light read. It dives heavily into the math behind the portfolio filled with graphics, charts, and tables.

If that sounds appealing, pick up a copy!

But if you’re not keen on reading 200+ pages on mathematical algorithms, consider Meb’s podcast or his YouTube Channel to learn about his investment philosophy.

What Is Quantitative Asset Management?

Quants (“quant” for short) use mathematical algorithms, modeling, and data analysis in making all their trading decisions.

They take the same types of data any investor sees, whether its earnings, book values, cash flows, but look at it in a systematic way to make reliable, research-backed decisions.

When done well, the data should lead to the same investment decision every single time.

Meb describes the principles behind quant investing in his books, but it’s not something you can pick up before a bedtime read.

Quant investing takes some serious know-how and a strong background in applied mathematics. But, if you’re willing to put in the work, it might be worth it.

A decent preform quant on Wall Street can pull down over a million dollars a year. Whether you read Meb’s book or take in his content online, you’ll quickly learn that he’s a big fan of quantitative asset management.

Fiscal flexibility that’s funny, free and delivered weekly.

How You Can Build The Ivy Portfolio

All you need to do is purchase investments that mirror the asset allocation in the Ivy 5 or Ivy 10. There are a few examples below, but don’t be scared to venture out on your own.

The idea here is that you’re imitating the diversification used by the Ivy League endowments, not buy the exact ETFs or index funds suggested below.

Vanguard

Vanguard offers low-cost index funds which are an excellent option for most investors.

If you want to learn more about Vanguard, consider our deep dive into their best funds. To build The Ivy 5 Portfolio with Vanguard, you could try the following equally split five ways:

- Vanguard Total Stock Market Index (VTSAX)

- Vanguard Total International Stock Market Index (VTIAX)

- Vanguard’s Intermediate-Term Bond Index (VBILX)

- Vanguard Commodity Strategy (VCMDX)

- Vanguard Real Estate Index (VGSLX)

While Vanguard funds are known for being low cost, their minimums can be steep. For example, the commodity strategy fund carries a $50,000 minimum and the remaining funds cost $3,000.

One way around this obstacle is to buy the ETF equivalent. However, there is no Vanguard ETF equivalent for the commodity fund.

If you’re getting started investing with little money, attempting to replicate the Ivy Portfolio with Vanguard funds may be out of reach.

One cost-friendly solution is to use a

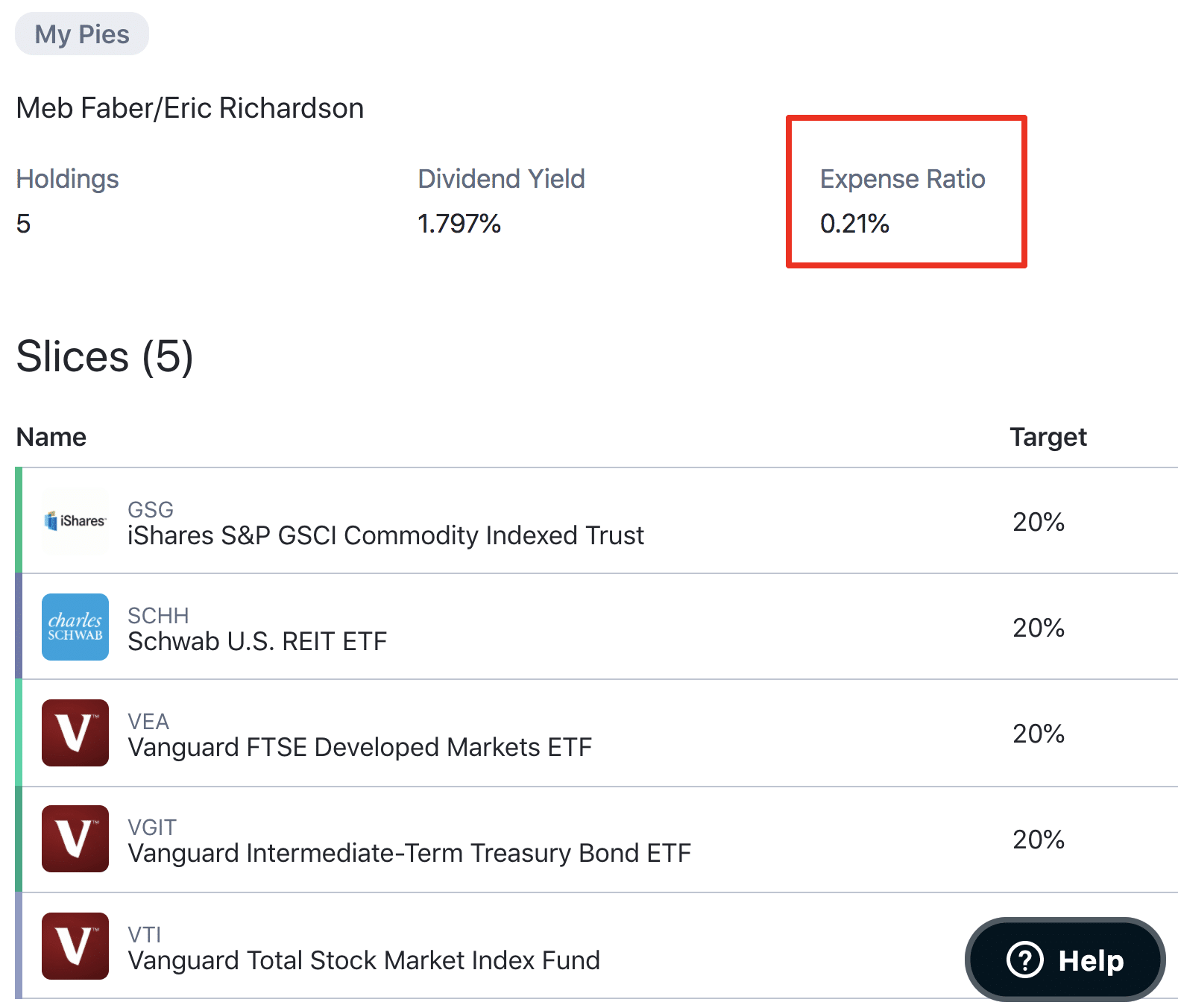

M1 Finance

M1 lets you build The Ivy Portfolio using an inexpensive mix of Vanguard, iShares, and Charles Schwab funds. You can also invest in single stocks or model world-class investor portfolios using their Expert Pie models.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes.

We went ahead and pre-built these portfolios but you can further customize them on your own if you like. If you use M1 Finance it will make automating these strategies easier.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes. This is more specific than the Ivy 5.

Here’s one option of how you could build a custom version of your own.

Currently, the ETF commodity alternative offered by iShares trades at $10.66 per share. Compare that to a $50,000 minimum needed to invest with Vanguard.

All you have to do is select the investments you want in your portfolio and set each investment’s target weight. Their software automatically aligns your portfolio to follow your desired target asset allocation.

M1 Finance is a great choice for individual investors because they charge zero transaction fees and dynamically rebalance your portfolio.

And you will have to rebalance with The Ivy Portfolio, especially the Ivy 10.

Your asset allocation drifts out of alignment over time.

Tweet ThisWhen that happens, you’ll need to move funds from one asset class to another to keep the ratios of your investments on target.

Most investment professionals recommend rebalancing at least once a year. If you decide not to use M1 Finance, then pick a date each year (or twice a year), stick it on your calendar, and commit to rebalancing your portfolio like clockwork.

If you decide to go with M1 Finance, you don’t have to worry about it.

Harvard’s Version

Although The Ivy Portfolio emulates the investment strategies followed by Havard and Yale’s endowments, it doesn’t copy them exactly.

If you find that disappointing, consider this, the Harvard Endowment is run by the Harvard Management Company which employs over 120 people and manages 13,000 different funds.

Don’t get me wrong, I love investing, but there’s no way I’m attempting to manage that kind of complexity on my own. And you shouldn’t either!

That’s the beauty behind these asset allocation strategies, it takes Harvard and Yale’s complicated methodologies, and makes them something you and I can implement.

But, that doesn’t mean we can’t learn from what the big boys do.

Let’s take a look at Harvard’s allocation. And this is taken directly from their 2019 Performance Report, which you can read for free online.

| Asset Class | Allocation | Return |

|---|---|---|

| Public Equity | 26% | 5.9% |

| Private Equity | 20% | 16% |

| Hedge Funds | 33% | 5.5% |

| Real Estate | 8% | 9.3% |

| Natural Resources | 4% | -12.4% |

| Bonds/TIPs | 6% | 5.7% |

| Other Real Assets | 2% | -8.3% |

| Cash | 2% | --- |

| Endowment | 100% | 6.5% |

Like it or not, you’ll be unable to invest in many of these asset classes. Private equity and Hedge Funds, for example, typically require being an accredited investor.

What's Accredited Mean?

It means you’ll need to have an income exceeding $200,000 for the last two years and a net worth of over one million dollars.

Ivy Portfolio Performance

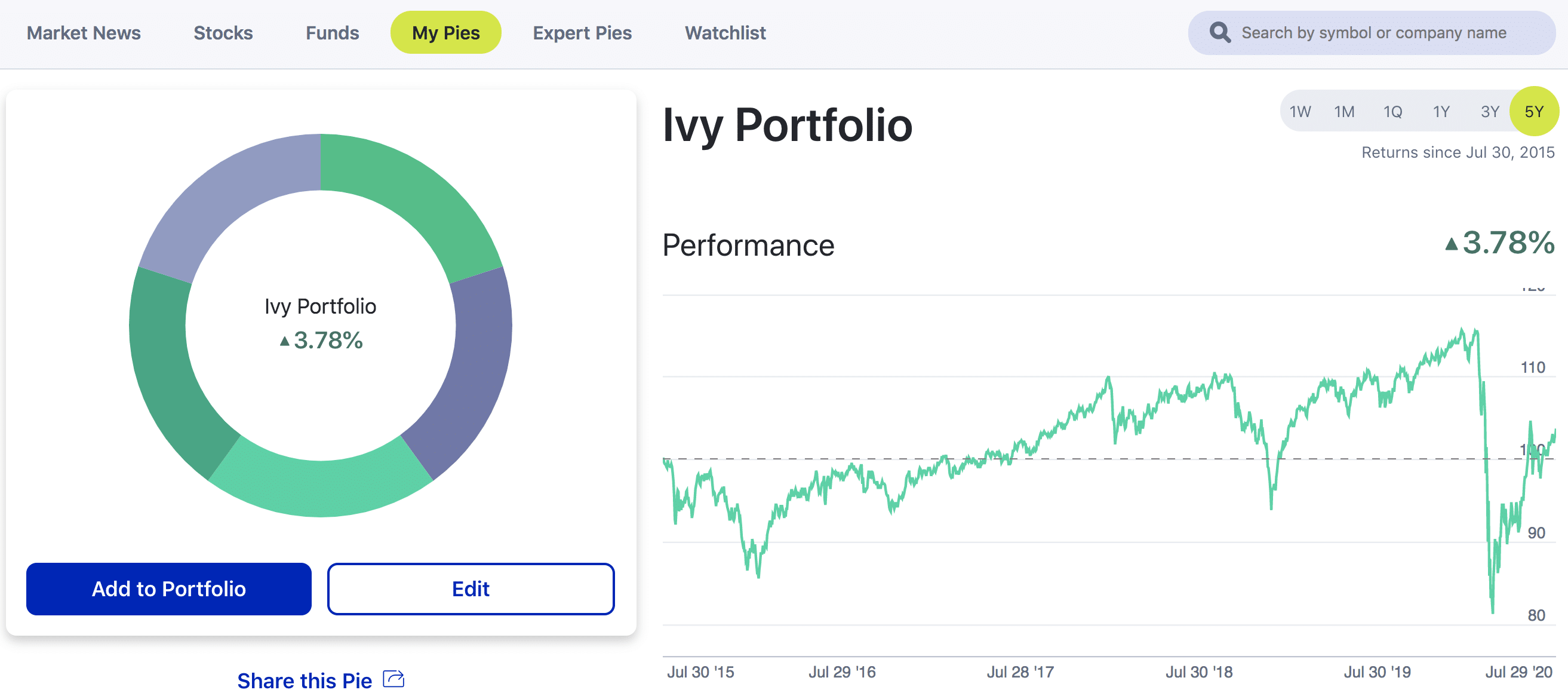

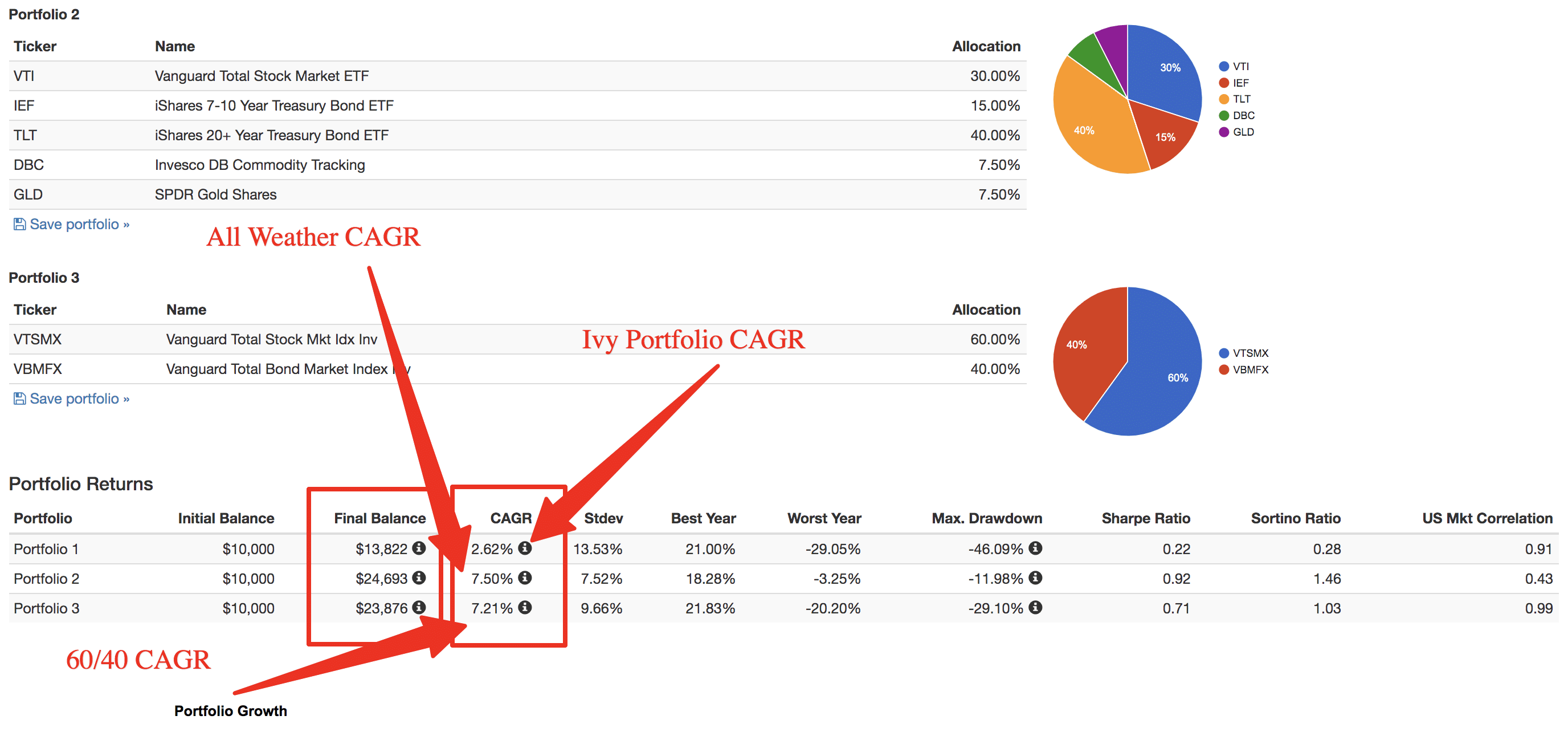

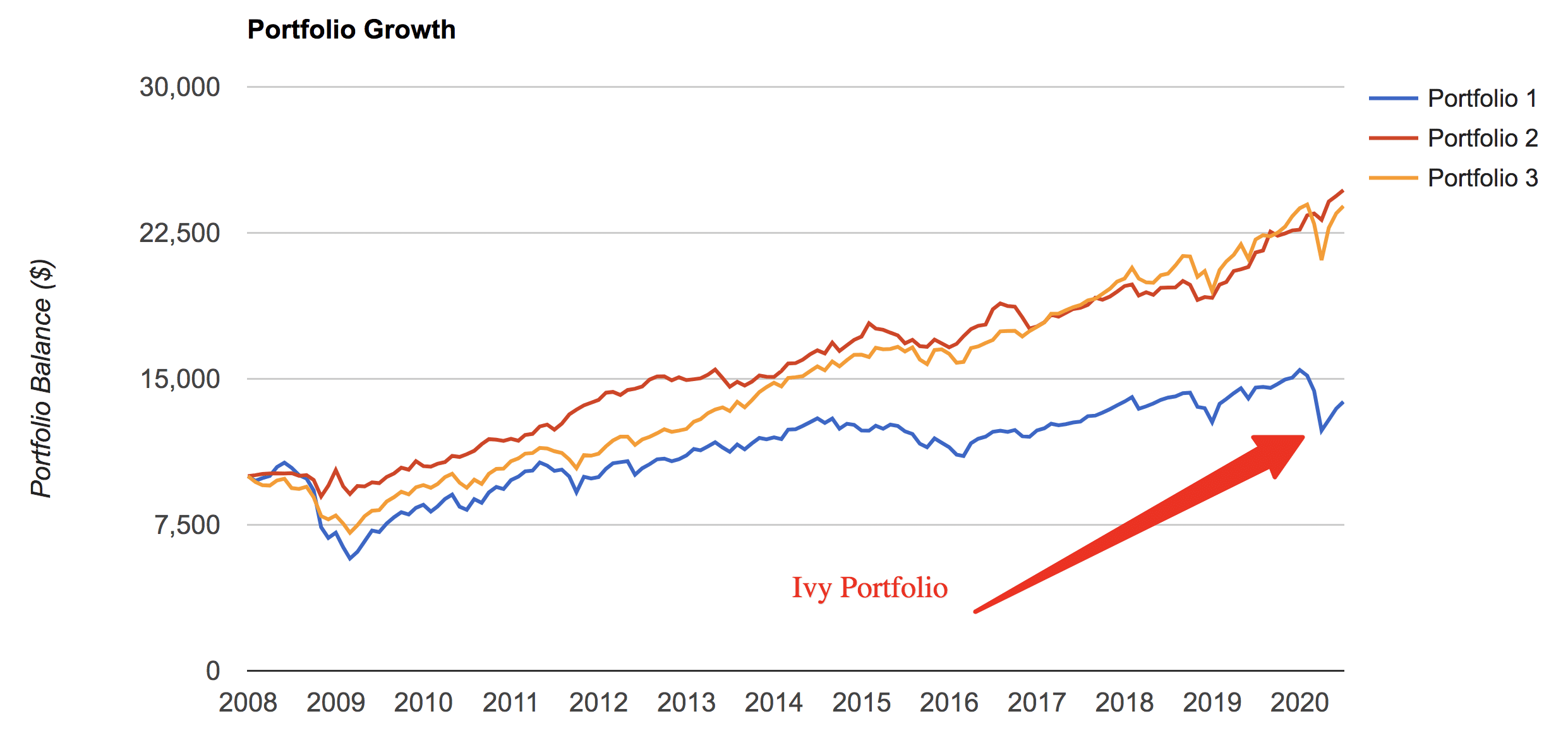

We backtested the portfolio using PortfolioVisualizer to run a scenario and the below represents the allocations, funds used, and performance of each.

However, you can’t look at a portfolio in a vacuum, so let’s compare it with two other investment allocations.

To look at The Ivy Portfolio’s performance, let’s pretend it’s 2007 (as far back as these results went due to the funds chosen) and you have $30,000 to invest equally in:

- The Ivy Portfolio

- Ray Dalio’s All Weather

- 60/40 Stock/Bond split

In other words, you hedged your bets and invested $10,000 in each of the three. Which would win?

Well, here’s the answer.

Below, the results displaying the Compound Annual Growth Rate (CAGR).

Not exactly a screaming endorsement for this strategy, is it at 2.62%? The All Weather and 60/40 portfolios more than doubled their money while the Ivy gained just over $3,000.

But, before you completely write off the Ivy Portfolio, remember two things.

First, past performance is no guarantee of future results. Who knows what will happen in the next decade.

And second, schools like Harvard and Yale aren’t looking for huge returns. They want to protect their endowments from significant losses and slowly grow their money over time.

There’s no retirement age for an endowment. The goal is to keep them safe, forever.

Put another way, this is a fantastic portfolio for someone who already has a lot of money and wants to protect it.

Is that you? If not, consider an alternative. We’ve written about several model portfolios along with the All Weather including:

What’s Next?

If you’ve read this far, you’ll likely know more about the Ivy Portfolio than 99% of the public. Still have questions?

Consider reading our post on asset allocation to learn more about the mechanics of building a portfolio to align with your financial goals.