Finding the perfect portfolio is debatable. Everybody has an opinion. There is no single portfolio that rules all. There is only the one that lets you accomplish your financial goals with minimal anxiety.

This post explores the Larry Portfolio. We’ll take a look at his approach to building it, his methodology, core components, and if it makes sense for you. Simply put, if you’re looking for a portfolio to let you sleep well at night, keep reading.

Economic Conditions

We’ve talked about portfolio diversification before and why it matters. The idea is not to leave yourself vulnerable to market swings by diversifying away risk as much as possible.

Asset classes in portfolios react differently to market conditions. During economic expansion, times are prosperous and stock prices soar.

Perhaps you hit an inflationary period and everyone says to invest in gold. Or you’re in a deflationary period and long-term Treasurys are the way to go.

Your portfolio should be like a well-balanced cocktail. You want all of the ingredients to intermingle without one overpowering the others. How does Larry accomplish this?

Who’s Larry?

The Larry Portfolio (LP) is named after Larry Swedroe. He’s the Chief Research Officer at Buckingham Strategic Partners (formerly the BAM Alliance).

He’s authored 16 books including, The Only Guide to a Winning Investment Strategy You’ll Ever Need, which was one of the first books to explain evidence-based investing to ordinary investors.

Larry is also a contributor at MutualFunds.com and ETF.com. He holds an MBA in finance and investment from NYU and a bachelor’s in finance from Baruch College.

Fiscal flexibility that’s funny, free and delivered weekly.

What Is the Larry Portfolio?

The Larry Portfolio is featured in the book he co-authored with Kevin Grogan called Reducing the Risk of Black Swans.

Mr. Swedroe suggests by tilting your portfolio to higher-risk asset classes that generate superior returns, you could hold less in stocks and more in safer investments (e.g., bonds).

Larry refers to it as a low-beta/high tilt portfolio.

Buy riskier stock funds, reduce your equity exposure, and decrease portfolio volatility. How?

The Larry Portfolio Asset Allocation

Take a look at the core components of the Larry Portfolio. How does a portfolio holding 70% bonds sound to you?

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 15% | U.S. Small-Cap Value | Stock |

| 7.5% | International Small-Cap Value | Stock |

| 7.5% | Emerging Market Value | Stock |

| 70% | Intermediate Treasuries | Bond |

For some investors, 70% is the perfect mix, while others feel it’s too conservative.

This portfolio's goal is to be both high performance and low volatility. It achieves its performance by tilting your portfolio to higher-risk stocks that are underpriced. Its low volatility is due to only holding 30% in stocks while 70% goes to bonds.

It’s a bit like a barbell strategy where you invest in two market extremes, both high and low-risk while avoiding the middle.

Larry sees small value stocks as having a higher expected return than the stock portion of a portfolio only invested in a total stock fund (e.g.,Vanguard’s Total Stock Market fund).

Because the equity portion of your portfolio is smaller, you’re taking less risk while maximizing expected returns. Your left tail risk is also reduced due to the lower stock allocation.

Tail risk is the possibility of suffering a loss due to an uncommon event.

Larry Portfolio Components

Small Cap Value

Small-cap value stocks combine two factors into one: size and value. Small-cap stocks have more volatility with expected higher returns. They occupy the U.S. stock market’s bottom 10% of the capitalization ladder.

Small-cap market capitalization typically falls between $300 million and $2 billion. Market capitalization is the number of a company’s outstanding shares multiplied by price per share.

Value stocks trade below their book value and are often viewed as bargains. Many investors, including Warren Buffett, take this approach when evaluating worthwhile businesses.

There’s nothing sexy about value stocks – they’re not flashy or popular compared to growth stocks. A value stock’s merit is based on whether it can turn a profit (aka its intrinsic value).

The two distinguishing metrics when analyzing small-cap value are stock trading below its book value with a market cap below $1 billion.

International Small Cap Value

Small-cap stocks are less correlated to the market as a whole because large caps occupy a substantial piece of the pie.

The same holds true for international small-cap value stocks. They add a layer of diversification in the form of developed markets overseas.

These stocks follow similar rules as U.S. small-cap value stocks while not as correlated to U.S. markets.

Investing outside your home market exposes you to differing economic conditions and can reduce your portfolio’s total volatility. With exposure to international stocks, you’re investing in whichever country is outperforming.

Emerging Market Value

Emerging markets are up-and-coming, foreign economies, experiencing high growth and a rising GDP. They don’t qualify as “developed” markets compared to countries like Germany or the United States.

Investing in this asset class carries multiple risks of currency devaluation, inflation, political turmoil, and liquidity. There is also a tendency to have a higher concentration of only a few products (e.g., oil in Saudi Arabia).

Emerging markets typically produce higher returns but carry a larger downside risk.

However, emerging markets tend to be uncorrelated across countries, which makes investing in a fund more attractive.

Intermediate Bonds

Intermediate bonds have maturity dates between two and ten years. They typically have better yields than short term bonds with less volatility of long-term debt.

Long terms are the most sensitive to interest rates.

Medium-term debt lands in the middle, letting investors earn more for their money without sacrificing overall returns. The sweet spot for many investors are bonds with maturity dates below ten years (and are good enough for a portfolio).

Larry Portfolio Investment Strategy: Factor Tilts

What Is Factor Investing?

Factor investing is choosing securities based on certain characteristics that could lead to enhanced returns.

The first definition of risk as it relates to returns (and asset pricing model) was the Capital Asset Pricing Model (CAPM) developed in the 1960s.

As Burton Malkiel put it, the CAPM determined what part of a security’s risk could be eliminated through diversification and what part could not.

Fama – French

In 1992, Eugene Fama and Kenneth French said the CAPM was limited because you’re seeing risk and returns based only on a single factor, market risk (aka beta).

Fama and French suggested a 3-factor asset pricing model which became known as the Fama-French 3-factor model. It measures risk and returns through:

- Market beta

- Size

- Value

Exposure to size and value explained 90% of risk-adjusted, expected returns in a portfolio. Small-cap and value stocks carry both market and unique risk.

It led to the creation of factor-based funds. These were funds tilting in a specific direction.

Calculating Size and Value

Fama and French calculated the size factor through what’s called SMB (small minus big) and the value factor through HML (high minus low).

Simply put, SMB measures the returns of small-cap companies minus large-cap companies.

HMB measures high book-to-market companies (value stocks) minus low book-to-market companies (growth stocks).

It’s similar to calculating your net worth: assets minus liabilities. You want the number to be net positive.

It’s the same with SMB and HML, excess returns in small-cap and value stocks reveal a net positive exposure to size and value factors in a portfolio.

That’s what the SMB and HML calculated. If small and value stocks produced returns superior to the total stock market, investors should tilt their portfolios to those factors.

The significance of the Fama-French 3 Factor Model was that it explained over 90% of portfolio returns.

Know the Identifying Features

Small-cap and small-cap value stocks are different. The two identifying features of small-cap value are 1) a stock trading below its book value 2) with a market cap below $1 billion.

Larry Portfolio Risk Factors

Why Size Matters

Smaller companies are riskier because they have fewer resources and may experience difficulties during a recession or with GDP fluctuations.

Small is scrappy but exhibits short term volatility and underperformance. Investors should prepare for a bumpy ride.

Historically, small stocks deliver higher, long-term returns.

Value

Value stocks typically outperform growth stocks because of their ability to turn a profit, are sustainable, and aren’t a ‘flash in the pan.’

Low price-to-book ratios (or high book-to-market) mean you’re getting a bargain, but may also reveal the company is financially distressed and explain why it’s trading below its book value.

But because they’re not sexy, investors aren’t as attracted to them. There is a correlation between overpriced growth stocks and an investor’s overconfidence and willingness to pay.

Also, stocks trading below their book values tend to provide higher future returns.

Beta

Beta is the risk you assume when putting your money in the stock market. It’s the risk you can’t diversify away.

For example, you can diversify away from a single company’s bankruptcy, fraud, or scandal by investing in multiple businesses (e.g., an index fund).

One company's misfortune won’t break the stock market.

Tweet ThisThat’s what beta measures – the risk of the entire market.

Term Risk

The longer you hold a bond, the greater its chances interest rates will fluctuate. Long-term bonds hold the highest volatility and interest rates sensitivity.

A bond’s value holds an inverse relationship to interest rates: when interest rates rise, bond values fall.

Term risk is the amount of time you hold the bond until it matures. You assume greater term risk the longer the maturity date.

Intermediate bonds carry a form of term risk, though not nearly as much as long-term bonds.

The Larry Portfolio Investing Methodology: Putting It All Together

Critics of the Larry Portfolio argue it’s not well-diversified. It only holds 30% in equities with U.S. and international limited to small value stocks and emerging markets only investing in value stocks.

How can you expect to build long-term wealth in a portfolio that’s mostly bonds?

There’s another way to think about diversification. Don’t think about it as it relates to asset classes and portfolio weightings.

As Larry put it, consider diversification “by the exposure to factors that determine the risk and return of a portfolio.” Those being beta, size, and value.

He examines the exposure to the three factor tilts of the Fama-French model of a total stock market fund.

A total stock market fund (TSM) is exposed to only a single factor: beta (market risk). It isn’t as diversified when looking at it related to factor exposure.

Diversification Through Risk-Factors

The LP portfolio diversifies its risks across multiple factors: beta, size, value, and term risk of the bond holdings.

A total stock market fund has both small-cap and value stocks but has no exposure to the size and value factors. Why?

Because size is measured by the excess returns of small companies minus large companies (SMB). Value is calculated by the excess returns of high book-to-market companies minus low book-to-market companies (HML).

Exposure to large companies brings the net small factor exposure to zero in a total stock market fund.

Value stocks provide positive exposure to the value factor but growth stocks provide negative exposure. Another net-zero effect.

Having both small and large, value and growth stocks (like a total stock market fund) cancel each other out.

Implementing the strategy depends on which funds provide greater exposure to the value and size factors.

The easiest way to do this is to buy small-cap and value stock weighted mutual funds or ETFs.

Larry warns of tracking error regret when implementing this strategy because there will be times when other benchmarks (e.g., a total stock market index fund) are doing significantly better than the LP.

It’s those times you’ll be tempted to move your money into the funds that are currently leading the pack.

Larry Portfolio Returns

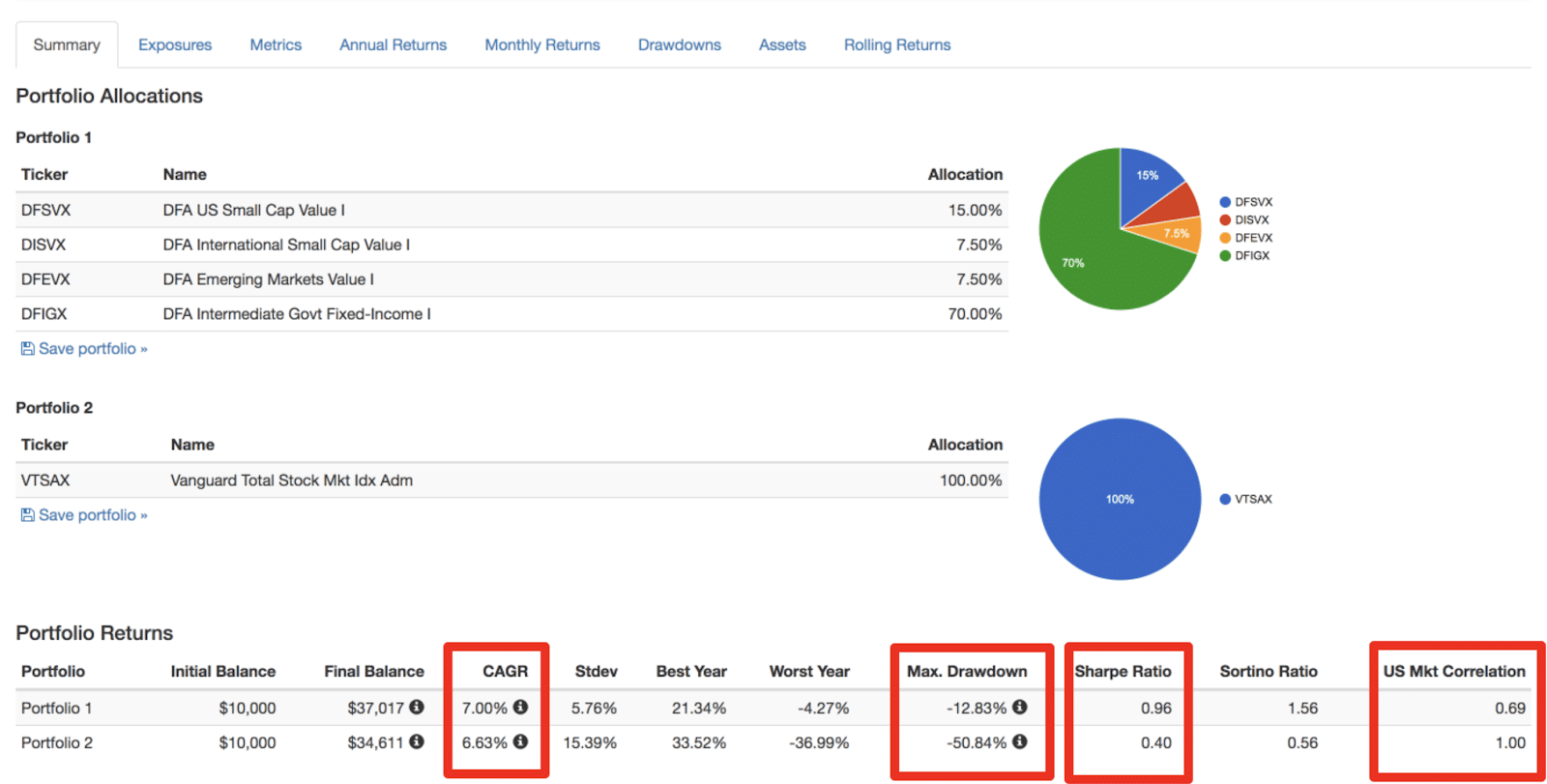

I used Portfolio Visualizer to run a backtest comparing the LP (using Dimensional funds) to Vanguard’s Total Stock Market fund.

I built mine using DFSVX, DISVX, DFEVX, and DFIGX for U.S., international, emerging markets, and bond holdings respectively.

This is only one example. Mr. Swedroe has mentioned other funds as well and this should only be considered one option of many.

The time period was limited to the available data for Vanguard’s Total Stock Market fund which only dates back to December 2000.

You can see the LP outperforms the total stock market fund VTSAX slightly. It’s also worth noting the max drawdown, Sharpe Ratio, and U.S. market correlation metrics.

The max drawdown for the LP is only -12% compared to -50% for VTSAX. That’s a considerable difference. And the worst year of the LP was only -4.27%.

The Sharpe Ratio is 0.96 compared to 0.40 with VTSAX. It means the LP is assuming less risk for more return (Sharpe Ratio measures level of risk you’re taking for an expected return. The higher this number the better).

The LP isn’t as correlated to the U.S. market as VTSAX is either. Beta measures market risk and has a value of 1. The LP has a value of 0.69 which means it’s less volatile than the overall market.

Replicating the Larry Portfolio

There are a couple of ways to model the Larry Portfolio without it becoming too complex. You could use the funds Larry recommends for a globally-diversified factor-based portfolio.

For example, he also suggests using the Bridgeway Omni Small-Cap Value Fund (BOSVX) for U.S. exposure and the DFA World ex-U.S. Targeted Value Fund (DWUSX) for international.

Not everyone may have access to these funds depending on which brokerage you use (or wish to incur added costs by going through a Dimensional fund advisor).

However, you can still tilt your portfolio in Larry’s direction with a few substitutes.

Fund Selection

Larry has mentioned (along with Bridgeway and Dimensional funds) using the iShares S&P 600 Small Cap Value, SPDR S&P 600 Small Cap Value ETF, or Vanguard Small-Cap Value stocks.

Whichever components you use, take note of how much the funds cost and pay attention to the expense ratios, management fees, or any other associated costs.

Automate the Larry Portfolio Using M1 Finance

If you’re building a portfolio using M1 Finance, you won’t see the Bridgeway or Dimensional funds Larry recommends. But, there are alternatives.

This portfolio's goal is to be both high performance and low volatility. It achieves its performance by tilting your portfolio to higher-risk stocks that are underpriced. Its low volatility is due to only holding 30% in stocks while 70% goes to bonds.

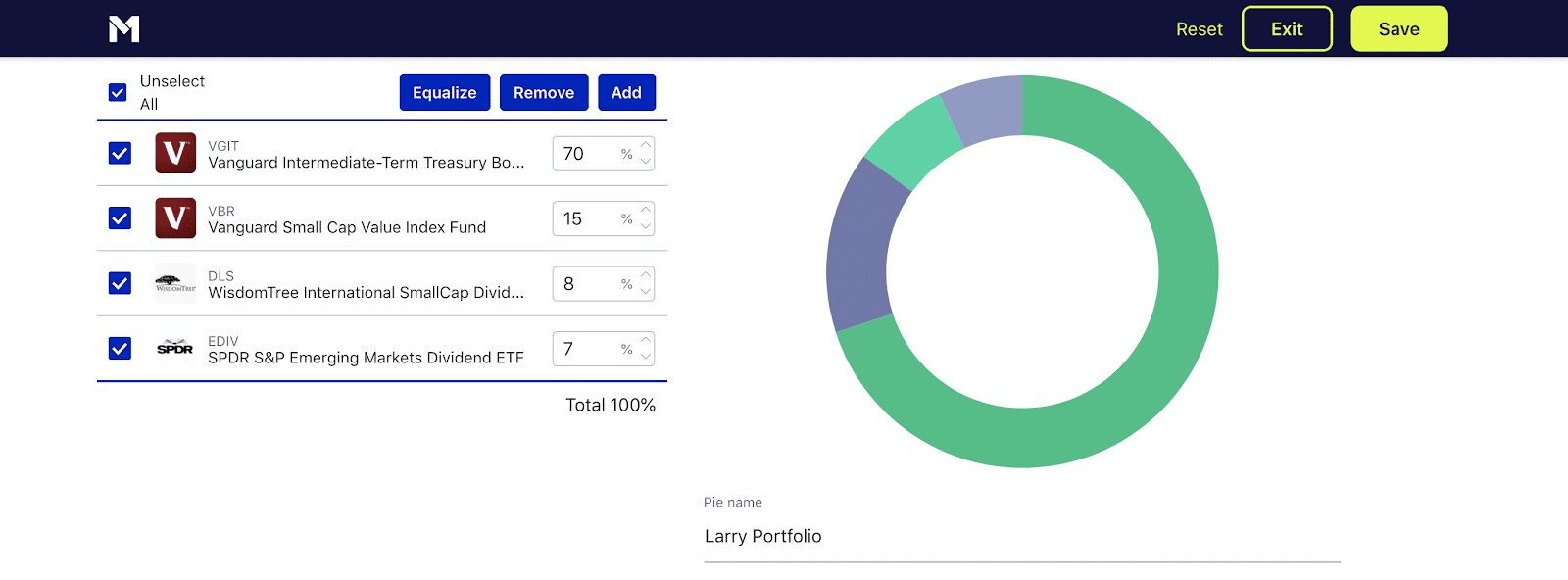

For example, I created the Larry Portfolio on M1 Finance using Vanguard Small-Cap Value, WisdomTree International Small Cap Dividend fund, SPDR S&P Emerging Markets Dividend ETF, and Vanguard Intermediate-Term Treasury for the bond portion.

I didn’t see much in the way of international small-cap value or emerging market value stocks when researching and M1 has neither. Minor adjustments were made.

M1 Finance doesn’t allow fractions in portfolio weightings (e.g., you can’t split the allocation 7.5% for international and 7.5% for emerging markets), only round numbers.

When picking funds on M1 Finance, you’ll see the expense ratios, dividend yield, fund profiles, holdings, and fund inception date with every selection.

The costs associated with this portfolio are only 0.13% (the expense ratio) as M1 doesn’t charge a management fee, trading fee, and dynamically rebalances your portfolio as needed. Creating an account is free.

For a closer look at M1’s platform, read our M1 Finance review here. Or, check out their site.

Why the LP Doesn’t Use Gold

Gold is a hot-button topic. There are many investors (including Ray Dalio) who believe gold belongs in your portfolio. The LP doesn’t include it. Why? (Afterall, the LP is low beta by design).

There are several resilient portfolios including the Golden Butterfly, All-Seasons, and the Permanent Portfolio which all hold gold. These portfolios are built to weather extreme economic downturns with less volatility.

Larry cites commonly-held beliefs about gold and disagrees. He doesn’t believe gold is an inflation hedge, a currency hedge, nor is it a safe haven during bear markets.

Warren Buffett makes an interesting point on this issue when asked about gold; it doesn’t produce anything. Companies generate revenue through production. Gold doesn’t.

Final Thoughts

There are infinite possibilities for building a portfolio. What’s critical is choosing the one most aligned with your financial goals. There is no single portfolio that rules all.

From experience, the simplest option is the best. If the Larry Portfolio seems simple enough to you, it might be worth trying.

For a deeper dive, check out any of Larry’s books. The two most relevant to this article would probably be Reducing the Risk of Black Swans and Your Complete Guide to Factor-Based Investing.