Wrapping your head around saving for retirement can be quite scary. Many of you reading may have just started saving for retirement and others haven’t saved a penny. We’re not here to shame you about not having a retirement plan. We’re here to tell you that, just like Luke Skywalker, it’s never too late to begin.

Get To Know Your Options

Since Social Security isn’t going to be enough for anyone looking to retire. You’ll need a more intuitive you-powered plan. Creating a retirement plan is not as scary as you might think.

Before we dive into the best ways to save for retirement here’s some basic information you need to know surrounding retirement regardless of age.

There are a few different kinds of retirement accounts:

- 401(k): This retirement savings plan is sponsored by an employer. It allows employees to save and invest a piece of their paycheck before taxes are taken out. Taxes are only paid on the money once it is withdrawn from the account.

- IRA: An Individual retirement account (IRA) is a savings account that offers tax breaks to people for investing money for retirement. Contributions made to IRA’s are tax-deductible (up to IRS limits). You can contribute up to $5,500 yearly, separate from a 401(k).

- Roth IRA: Different from an IRA, a Roth IRA is a retirement account you fund with post-tax income. This means you cannot deduct contributions made to this account like you can in a traditional IRA or 401(k). Since your contributions are taxed you can withdraw any time, tax-free and penalty-free.

- SEP IRA (Simplified employment pension): This type of IRA is specifically for business owners and those who are self-employed. It’s still a basic retirement account just like an IRA and contributions are tax-deductible. The big thing to note with the SEP IRA is if you have employees the IRS considers eligible to participate in your plan you’ll have to contribute to their IRA as well.

- Solo 401(k): If you make the jump into self-employment you’ll notice very quickly the lack of 401(k)ness going on. That’s where the solo 401(k) comes in. It’s exactly what it sounds like and is designed for a business with no employees. IRS rules state you can’t contribute to a solo 401(k) if you have employees, but you can use the plan to cover both you and your spouse.

If you’re starting with $0 in retirement savings and you’re over 40 years old, you’re legally allowed to save $18,500 per year in a 401k fund. If you’re over 50 you can increase that $18,500 – $24,500.

Now, if you stay on track with $18,500 at a minimum of a 7% return rate you’ll hit well over $1 million dollars by your 64th birthday – just in time for retiring.

Ah, the beauty of compound interest.

Aside from funneling cash into your 401k, you can also contribute to your IRA. As it stands, you’re allowed to contribute $5,500 to an IRA each year ($6,500 if you’re over 50). That’s an additional $132,000 you can add to your retirement pool.

For the hustlers out there we highly suggest starting a SEP IRA. SEP’s are a traditional IRA for the self-employed/business owner type. With these accounts, you’re allowed to add 25% of your income or up to $53,000, whichever comes first.

Be Realistic About How Much You Need

I’m just going to say it. Even to live a simple life in retirement, you’re going to need that $1 million. Possibly more to compensate for inflation. If you’re thinking you won’t need this kind of cash because you’re going to live a simple life out in the woods at zero cost, think again.

A simple life these days requires exact planning and the understanding that you’ll be living off of $30,000 – $40,000 a year.

By the way, that’s $1 million in retirement if you’re living off the 3-4% rule.

We suggest setting yourself up for success by determining how much your simple retirement life will cost each year, and then set up savings goals according to meeting your lifestyle needs.

Personal Captial has an awesome retirement planner that is 100% free. It’s the most realistic retirement planning calculator available.

It will help you understand exactly where you stand relative to your retirement goals so you can build, manage and forecast your retirement plan in one convenient location.

We are all in different situations so there are ways to design a retirement savings plan around your specific life, needs, and future goals. The bottom line is the earlier you start the better so get started now, however you can.

Fiscal flexibility that’s funny, free and delivered weekly.

Take Advantage of Employer Contributions

The moment you get your first big job or your current employer offers a 401k program – jump on that train. Most employers these days offer a 401k match program that requires you to hit a certain contribution amount. Make sure you take note of what that is and adjust your contributions accordingly.

On average employers will match up to half of 6% of your pre-tax income, meaning on average you should aim for a minimum contribution of 6%. Not to beat a dead horse or anything here but, we say a min of 10% is really the right path to take here.

If your employer isn’t currently offering a match program then think about skipping the 401k and utilizing a Roth IRA. Our suggestion is to max out your IRA and if you still have money leftover, switch back to the 401k and make it an addition to your retirement savings strategies.

Diversify Your Money

Being in your 20’s and 30’s means retirement is probably a ways away. This is a good thing because you’re able to tolerate a little extra risk. Don’t go full-on risky as many did back in 2008, instead keep that tragic year in mind when you begin working towards creating a well-balanced portfolio.

When you first invest in stocks and the market takes a dip, HOLD ON. The market will recover and being that you’re young, you can ride it out.

While you’re holding onto the bull keep in mind how intense you can get with the risks you take regarding the diversification of your retirement savings.

What to do in Your 20’s and 30’s

So how risky can you get in your 20’s and 30’s? Well, being that you’re young, you can load up on risk because you have plenty of time to ride out any rough patches you may encounter. More often than not, wealth advisors recommend an all-stock portfolio for this age group.

The issue here is not everyone enjoys taking that much risk, especially with what the market has been dishing out lately (and is predicted to dish out later).

According to Bankrate.com, only 26% of millennials own stock. That’s it.

So what’s a money-smart millennial to do when they can’t handle the bull? Our suggestion is to allocate 60% of your investments into stock with the remainder in bonds. This will allow you to get more comfortable with stocks without risking it all.

What to do in Your 40’s, 50’s and 60’s

This age group is in their peak earning years. This is when equities and a more bond-focused strategy come into play. That is if you didn’t wait until your 40’s to begin saving for retirement.

If that’s the case, you’ll need to be a little Tom Crusie with your money.

Still, though, we recommend a strategy of 60% stocks and 40% in bonds. When it comes to the bond element it’s going to be a smarter move for you to look for bonds with shorter maturity rates and place some money into high-yielding bonds.

Many will suggest a brokerage firm be in charge of creating a strong stock portfolio but we suggest taking

You can link your company 401k to your Retirement Goal and receive advice on how much you really need for retirement each year if you’re not already doing the math.

Create An Automatic Savings Habit

Once you’re set up for success with your investment accounts, Roth IRA, and 401k, it’s time to let the automation processes do the work for you.

Get into a habit of putting something, anything away on a regularly. This can be easily automated and then let compound interest do the work.

Utilizing accounts like

We love this tool because it takes the aches and pains out of monthly wealth management and turns it into a few easy minutes each month.

You won’t have to research aggressive strategies to death anymore because

If

So, if you spend $2.50 on a cup coffee, Acorns rounds that up to $3 and invests the $0.50 for you. The founders of the app know a lot of users are new to investing so the app provides a lot of guidance.

There are also other tools within the app that allow you to set and reach goals.

Similar to credit card rewards programs, Acorns has partnered with “found money partners” that rewards app users for shopping through select retailers. Basically, you shop within their partner network, you get cashback that is automatically invested, no effort on your part.

Utilizing both of these apps will ultimately help you achieve a well-balanced retirement portfolio.

Don’t set it and forget it though, check in on your retirement accounts a few times each year, and peak into your

What To Do When You Change Jobs

We love it when your guys share in our Facebook Community that you’ve gotten a job promotion or that you’ve accepted a kick-ass new job. This does leave many of you with some questions regarding what to do with your retirement accounts when you change jobs.

When you leave an employer you can choose whether you want to leave the money with your old employer or roll it over to your new one.

Leaving your money behind has some disadvantages so it’s best to keep your retirement money all in one place. Whatever you do don’t cash out as this will be an option tossed in front of you as well.

If you’re not sure what you should do, always keep in mind whether you want to be able to easily access your investments and savings upon retirement.

Moving everything along with you to your new place of work will always make it easy to keep your personal information as updated as possible.

The Worst Thing You Could Do

When it comes to your retirement savings, the worst thing you can do is to not save now.

Seriously.

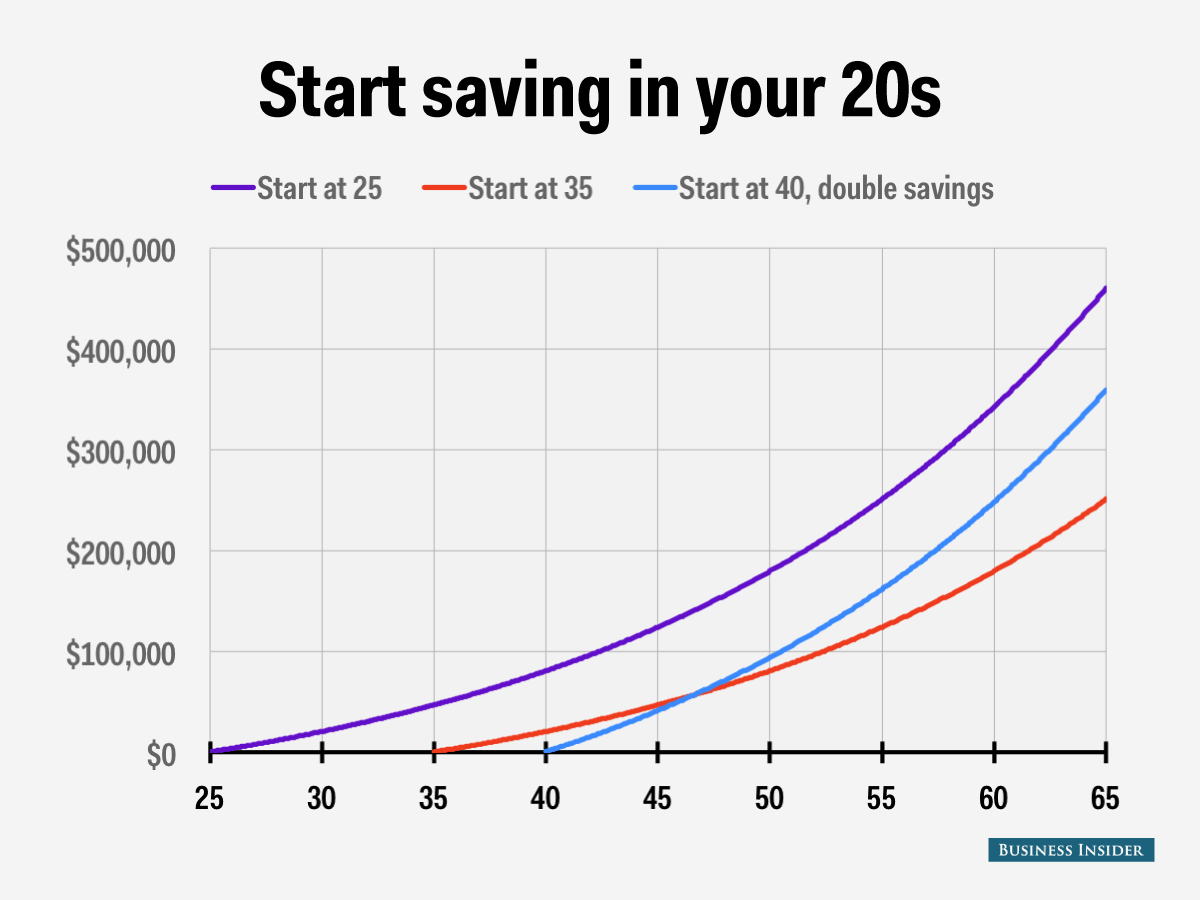

If you started at age 22 and put 10% of your income away each month, by the time you hit 65 you’ll be sitting pretty with a cool $1.7 million in your retirement savings (not counting any social security or pension).

Flash forward ten years later, at 32, the most you’ll be able to save is $780,000, which is a lot, but isn’t exactly where you’ll need to be in order to feel secure.

Dudes, I’m going to be super rich one day based on my investments, I’ll be fine.

Dude, you might if you’re lucky, but it’s pretty damn hard to get there unless that’s the only way you spend your time. Playing the market is rough.

A better bet to make with yourself is to diversify your investments and savings accounts. If 2008 taught us anything it’s that it is best not to put all your eggs in one basket.

Another thing a lot of people did wrong back in the day was cash out their retirement accounts before they were ready to retire.

Believe us, it can be tempting to pull out some money from your savings when you’re in a money pinch but if you do before you’re 50 ½, you’re going to face some gnarly penalties.

When it comes right down to it, start saving for retirement now and get your financial goals in order so you can live your best life when you retire.

Even if you’re aging out of your thirties. Some retirement is better than none.