A lot can happen over the decades. There will be recessions, bear markets, bull markets, political upheaval, and possibly even depressions. But we can’t buy and sell based on the prevailing economic conditions.

One of the critical components of our investment philosophy is to set it and forget it. But, unfortunately, you’re practicing the opposite of setting it and forgetting it investing.

We need to create a portfolio that performs well in all conditions. We don’t need to make this portfolio because someone has done it for us.

And that someone is not just anyone. He happens to be Bridgewater Associates hedge fund manager Ray Dalio, one of history’s legendary investors.

Ray Dalio created what is known as the All Weather Portfolio, which contains the exact asset allocation you need to make money in any economy.

But Ray Dalio’s All Weather Portfolio has some competition in the form of the Golden Butterfly Portfolio. Tyler of portfoliocharts.com designed the Golden Butterfly and described it this way:

LMM is a huge Ray Dalio fan. So can the Golden Butterfly best our boy? We love a good smackdown, so we’ll break down the All Weather Portfolio and the Golden Butterfly Portfolio. May the best portfolio win.

Is There a Recession-Proof Portfolio?

Rising stock prices, a steeper yield curve, and the low unemployment rate have lessened the fear of recession that many experts had two years ago, Ray Dalio among them.

What we do know is that we are in the part of the cycle in which the central banks’ getting monetary policy right is complex and that this time around, the balancing act will be tough (given all the stimulation into capacity constraints and given the long duration of assets and several other factors) so that the risks of a recession in the next 18-24 months are rising.

What is the Golden Butterfly?

The Golden Butterfly is a modified Permanent Portfolio with one additional asset class that incorporates some of the characteristics of a few other notable lazy portfolios.

So while the predictions are not as dire as they were, it’s still a scary time for many investors.

No one wants to lose money in the stock market, but we can’t become too risk-averse because doing so won’t allow our money to grow at the rate we need it to for a comfortable retirement.

We need an investment strategy with a permanent portfolio that can weather anything the economy throws.

And add to our wish list an investment strategy that doesn’t depend on trying to time the market.

Fiscal flexibility that’s funny, free and delivered weekly.

Two Main Portfolio Ingredients

This sounds like a tall order, but it’s pretty simple. There are two main ingredients you need to create a portfolio that can roll with the punches and reduce our risk while not diminishing high returns; diversification and risk-weighted return.

Diversification

We’ve talked about diversification ad nauseam, but we’re going to talk about it more because it’s so critical for individual investors.

You are being diversified means spreading your investment dollars out across various asset classes and sectors within those asset classes.

The trick is to take risks and be paid for taking those risks. To take a diversified basket of risks in a portfolio.

Tweet ThisWe might own stock in logistics companies (UPS, FedEx) and banking (Morgan Stanley, Goldman Sachs) if we’re talking about stocks.

If logistics stocks are down, that’s okay because banking stocks might be up. However, you would also have money invested in real estate, REITs, and gold to diversify further.

But don’t put all of your eggs in one basket. Low-cost index funds are an excellent way to ensure a well-diversified portfolio.

Risk-Weighted Return

Risk-weighted return is how much return your investment has made relative to the amount of risk that investment has taken over a given period.

If two investments have the same return over a given period, the investment with the lowest risk will have the better risk-weighted return.

Here’s an example:

Vanguard Total Stock Market Fund

- Average Annual Return +9.4%

- Deepest Drawdown (2008) -49.3%

Golden Butterfly (we’re going to cover this below)

- Average Annual Return +7.94%

- Deepest Drawdown (2008) -10.8%

You can see the peril of chasing returns.

TSMF (Total Stock Market Fund) had a mere 2% earned per year advantage over Golden Butterfly but lost 38.5% more! Conversely, Golden Butterfly investors made slightly less but had a minimal loss compared to TSMF.

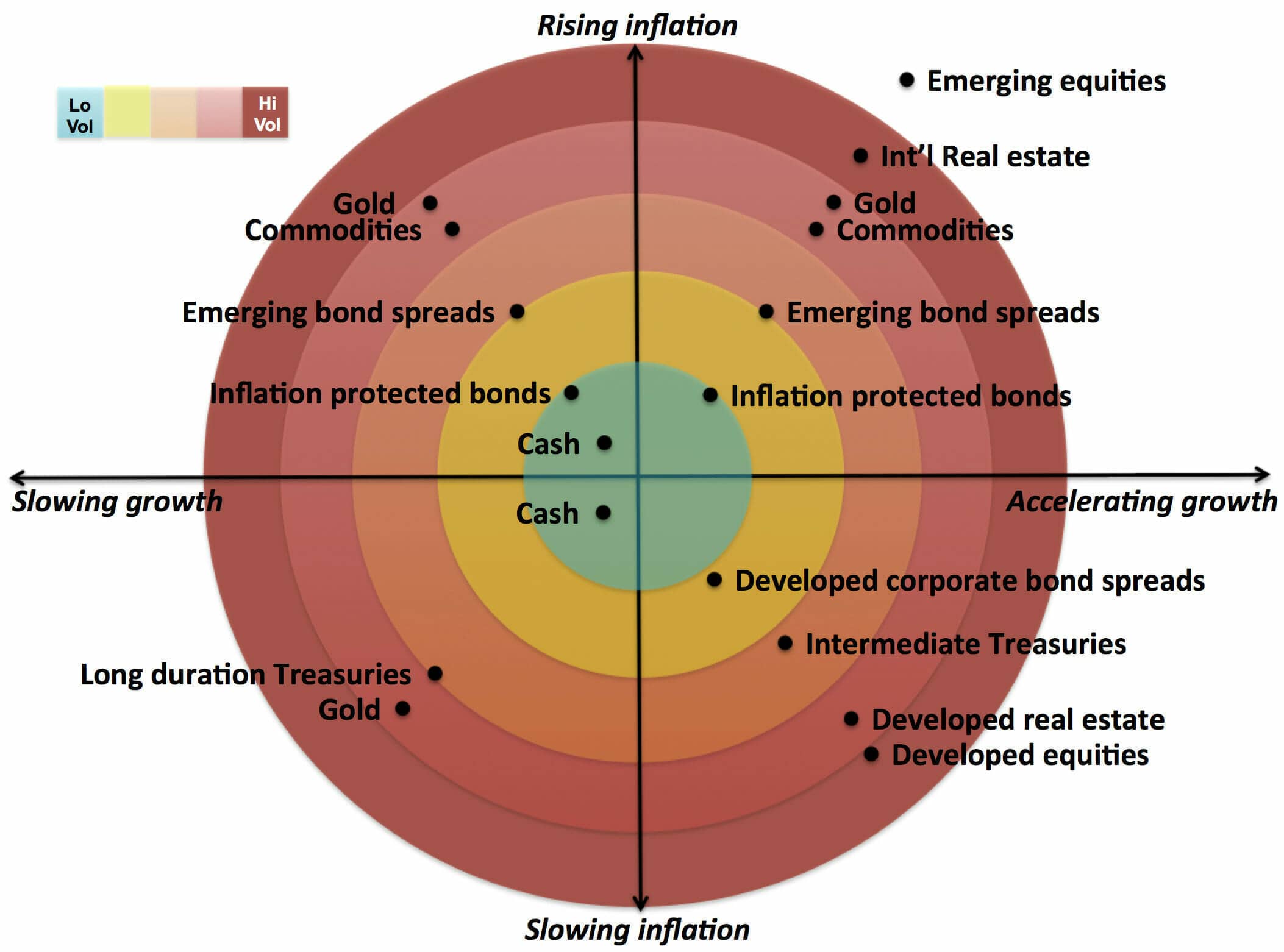

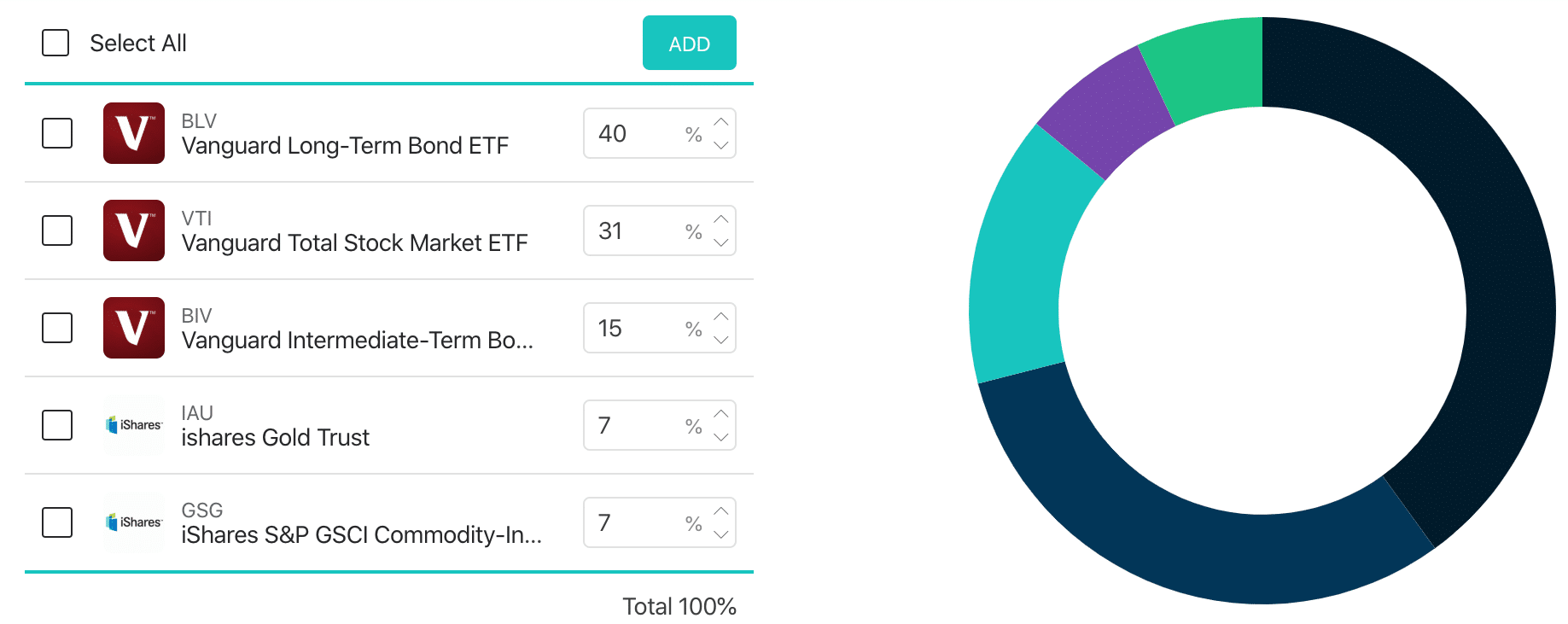

What is in the all-weather portfolio?

We explained who Ray Dalio is, but why did he create a set-it-and-forget-it portfolio? He makes billions of dollars picking stocks, so why need a set portfolio?

After realizing that he had made and would continue to make more money than he could spend in a billion lifetimes, Dalio knew he needed to set up a trust.

Since he wouldn’t be around to oversee the trust, he needed to create a portfolio that would make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is.

According to Dalio, growth, and inflation are all that matter. They are either up or down, and there are various combinations.

Growth is up; inflation is down. Change is down, inflation is up, etc.

Dalio broke this into four quadrants and designed a portfolio that would perform well in each.

He used back-testing to simulate his strategy using historical data to see the results and analyze the risk and profitability.

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

The portfolio also had to hold up against start date sensitivity, meaning to be successful; it’s not necessary to try and time the market.

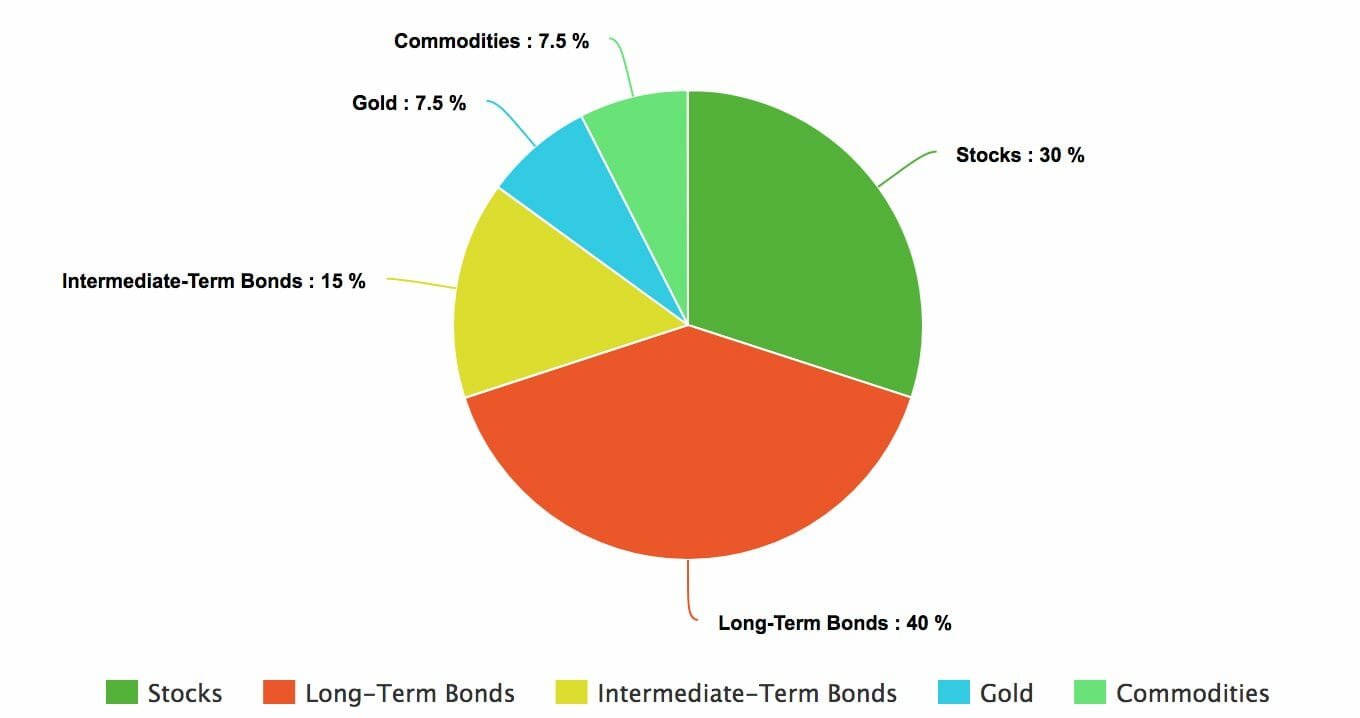

| Weightings | Portfolio Components | Asset Class |

|---|---|---|

| 30% | Total U.S. Stock Market | Stock |

| 40% | Long-Term Treasuries | Bond |

| 15% | Intermediate-Term Treasuries | Bond |

| 7.5% | Gold | Commodity |

| 7.5% | Diversified Commodities | Commodity |

It won’t impact the performance when you start investing with the All-Weather Portfolio.

This is what the All Weather Portfolio looks like on M1 Finance using the best ETFs with the lowest fees:

The Golden Butterfly

The Golden Butterfly was derived from the Permanent Portfolio developed by investment advisor Harry Browne, and it’s a small change to Ray Dalio’s All Weather Portfolio.

While Dalio is agnostic about the stock market, the Golden Butterfly skews toward prosperity. And for a good reason. Over time, there have been more times of economic growth than times of decline and recession.

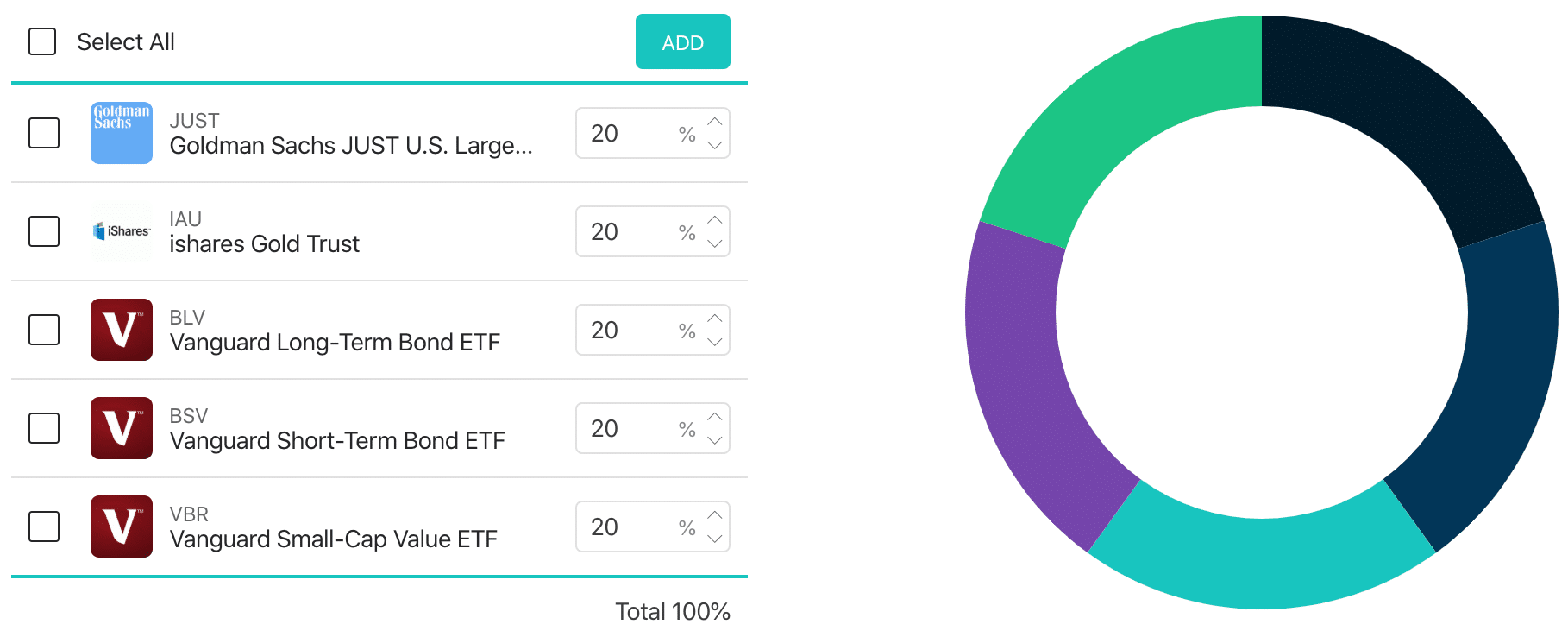

This is what a Golden Butterfly Portfolio looks like:

We want our retirement to earn us money and help ensure we have a world worth retiring in. Not coincidentally, the SRI Large Cap fund outperforms VTI.

This portfolio is a socially responsible version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

You’ll notice we use our Socially Responsible Investing replacement for Vanguard’s Total U.S. Stock Market fund, VTI.

We discussed the JUST decision in our Socially Responsible Investing episode. If you want the original allocation, you can find it here.

Here’s a link to the classic version if you’d prefer that one:

This portfolio is a modified version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

Asset Breakdown

Previously we had recommended SPDR’s GLD here, but IAU is a similar fund. It’s virtually identical to stored gold bullion, but IAU has a lower expense ratio, 0.40%, and 0.25%, respectively.

| Weightings | Portfolio Components | Asset Class |

|---|---|---|

| 20% | U.S. Large-Cap Equity | Stock |

| 20% | U.S. Small-Cap Value | Stock |

| 20% | U.S. Long-Term Treasuries | Bond |

| 20% | U.S. Short-Term Treasuries | Bond |

| 20% | Gold | Commodity |

Do These Assets Make Good Investments?

We know the Golden Butterfly flies in the face of much conventional investing advice.

Most of those in the world of personal finance don’t recommend gold as an investment. It’s the kind of thing you associate with Doomsday preppers.

Long-term treasuries are volatile for treasury bonds and risk losing significant value in the future. Small-cap value is controversial, and there is much debate about its future outlook. With current rates, short-term treasuries seem to waste your investing dollars.

So! Four of the five assets that make up the Golden Butterfly are pretty unpopular, and that’s more than enough for most people to assume that it’s a losing proposition.

You Can’t Argue With Results

During backtesting, Golden Butterfly’s performance against a 100% stock market portfolio over the last 43 years found that GB had almost the same long-term real compound annual growth rate but with 60% less volatility.

Its worst year saw a loss of only 11%, and the most extended drawdown period was just two years. The Golden Butterfly also optimizes the safe withdrawal rate. We’ll cover this more below.

Not only was the Golden Butterfly great for accumulation overall timeframes, but it was also vastly superior in retirement with 40-year Safe and Perpetual withdrawal rates nearly 2%(!) higher than the stock market equivalent.

Golden Butterfly and the 4% Rule

As a retiree, do you plan to use the 4% rule? The 4% rule states that if you only withdraw 4% of your invested money each year to live on, your money will not run out for at least 30 years.

Many experts feel the 4% rule is outdated and should now be 3.5% or less.

With TSMF, you can only afford to withdraw 3.5%, but Golden Butterfly allows you to start at 5.3%. As percentages, those numbers don’t seem that different.

But the difference is significant in terms of the amount of money you have to live on each year of your retirement.

If you have $1 million for retirement, the TSMF will give you $35,000 yearly, but the Golden Butterfly will provide you with $53,000 annually. Quite a difference!

We Haven’t Been Holding Out

Ever since we did the episodes about the coming recession and updates on Andrew and Laura’s rental properties, we have been getting many questions about Andrew’s investment strategy.

We haven’t answered because he wasn’t sure! He has so much money sitting in an opportunity fund, making jack interest because he hadn’t yet decided what to do.

That’s how this episode was born. He was researching his options and started looking into different stock portfolios.

If you’ve listened for any length of time, you know Andrew is a big Ray Dalio fan, and for a good reason. The guy has some of the highest returns in the business.

So it was a surprise to even Andrew when he found himself leaning more toward the Golden Butterfly than the All Weather.

But that’s the plan. While we are expecting a recession, the historical data doesn’t lie. Our economy experiences more periods of economic growth than periods of recession.

All Weather was built for, well, all weather. But we have more good weather than bad, so Golden Butterfly was our winner in the battle of the portfolios.

Show Notes

Philoso Rapper: A Belgium-Style Ale.

Double Dry Hopped Coriolis Effect: A New Zeland Style IPA