For most people, understanding how stocks, bonds, and funds work sounds about as exciting as a trip to the dentist’s office. But not you. You’re a Listen Money Matters reader and a personal finance nerd (closeted or otherwise).

You may not know what the different types of stocks are or possess an encyclopedic knowledge of the financial markets, and that’s ok.

We’re going to talk about the key differences, the role each one plays within your investment portfolio, and the types of investments used to build wealth.

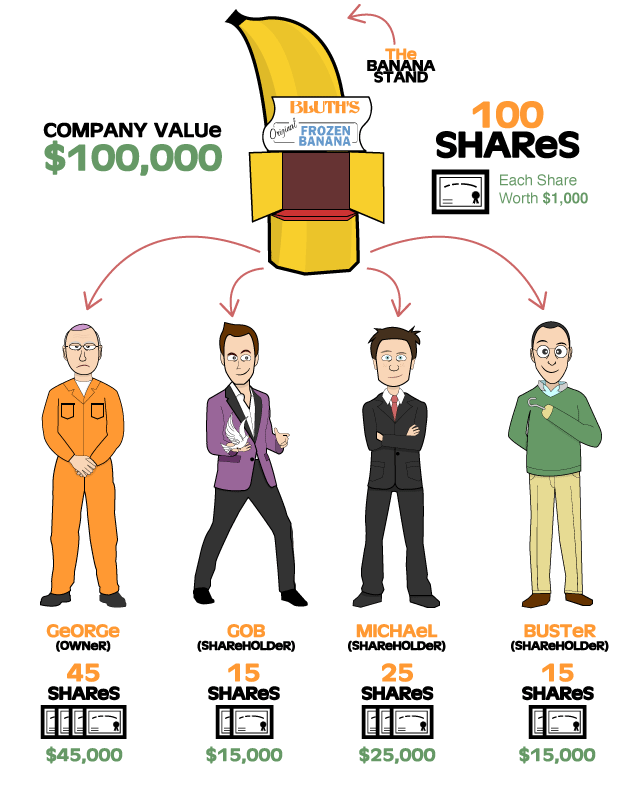

This article was initially created as an attempt to explain to Matt how stocks, bonds, and funds work. Because Matt’s favorite show is Arrested Development, Andrew explained it to him in simple terms using the Banana Stand as an example (hence the Arrested Development infographic).

If you’re unfamiliar with the show, watch it. It’s brilliant.

You can listen to that podcast episode right here!

This article by Andrew goes into greater detail (fully-equipped with high-quality Arrested Development imagery for easy reading).

Get ready to dazzle your friends and colleagues at your next cocktail party with this information.

Speaking of cocktails, what are you drinking this evening?

The Primary Difference Between Stocks and Bonds?

In a nutshell…

Stocks make you an owner while bonds make you a lender. Satisfied? Didn’t think so. Onward.

Asset Class #1: Stocks

Stocks give you an ownership stake in a company. When buying a company’s stock, you’re betting on their success (because if the business fails, you lose money). Stocks are bought and sold on exchanges, e.g., the New York Stock Exchange.

A company issues stock in the form of shares to sell to investors. If you’re a business owner and want to raise more money than your business can generate on its own, you sell shares of stock.

It’s kind of like crowdfunding if crowdfunding was regulated by the SEC.

Each share represents fractional ownership in the business. The more shares you own, the greater the percentage of ownership you have in the company.

Are Stocks Risky?

Stocks are higher-risk but can carry a higher return. There are ways to mitigate that risk (for example, investing in funds) which we’ll get to in a minute. Investing in stocks requires a higher risk tolerance due to the volatile nature of the stock market.

Investing in stocks is ideal for people who can handle market swings, want to create a passive income source, and build wealth over the long-term.

Types of Stock

There are many different types, but the two primaries are:

- Common stock

- Preferred stock

Common stock represents ownership in a company and carries voting rights. The bulk of ordinary investors hold common stock. However, its shareholders (you) are at the bottom of the food chain. I.e., if the business goes bankrupt, common shareholders must get in line behind bondholders and preferred shareholders before getting paid.

Preferred stock carries a couple of perks. Owners have first dibs on assets if the company goes belly-up. I.e., you get paid before anyone else. You also receive dividends regularly (monthly or quarterly). Some dividends follow a benchmark interest rate while others are fixed. Preferred stockholders have no voting rights.

Fiscal flexibility that’s funny, free and delivered weekly.

Asset Class #2: Bonds

Bonds are debt instruments issued by government and corporate entities. Bonds don’t appreciate in value the same as stocks do and carry a lower return. And bonds seek to mitigate the risks carried with stocks and offset the dips in the stock market (bonds and stocks aren’t highly correlated to each other).

If you’re looking for a steady income stream while preserving your principal, bonds are ideal for you.

Bonds have two potential benefits when holding them as part of your portfolio: they give you a stream of income and offset some of the volatility you might see from owning stocks. – Vanguard

You aren’t buying shares in a company with bonds, instead, you’re loaning money.

Tweet ThisIt’s like when you buy something on a credit card. Visa is lending you the money to pay for your new iPhone assuming you’ll pay it back. If you don’t pay it back promptly, you’re charged interest on the amount you borrowed.

You also have no ownership stake in a company with bonds. Once the issuer has fulfilled their end of the contract, that’s the end of it.

Are Bonds Risky?

All investments carry risk. As with any loan, you run the risk of the loanee defaulting. This sucks but it does happen. No investment is 100% risk-free. However, bonds are perhaps the least risky of them all.

Bonds are typically from corporations or the federal government (and if the federal government defaults on its loans, we’ve got bigger problems.

Buying bonds from corporations carry higher credit risk, but you’ll also get a higher yield.

If you own foreign bonds, you run the risk of currency devaluation from the issuing country. If it falls below what the U.S. dollar is worth, you could potentially lose money.

There’s also an inverse relationship between bond prices and interest rates (aka the coupon). When interest rates rise, bond prices fall and vice versa.

Why Do Interest Rates Matter for Bonds?

Imagine you’re loaning $2,000 to your friend, and he offers to pay you 6% interest on top of the $2,000 he already owes and pay you back in one year. That’s $120 collected in interest.

Now let’s imagine your neighbor starts loaning money to people at 4%. Who’s loan is sexier? If you wanted to buy the loan off someone, would you want to be the debt owner of a $2,000 loan at 6% or the owner of the same loan at 4%?

It’s a no-brainer. You could sell your loan (even charge a premium, earning even more because your loan offers a higher interest rate).

Interest rates affect you only if you’re selling your bonds on a secondary market. Typically, if you hold a bond to its maturity date, you’ll get your principal returned with interest.

Types of Bonds

Like stocks, there are many types of bonds you can invest in, all with varying degrees of risk and return. Let’s look at a few common examples.

United States Treasuries. If you’re looking for the safest kind of bond investment, these are it. Interest from these bonds are tax-exempt at the state level, but you will pay federal income tax. Treasuries come in many forms, including Treasury bills, Treasury notes, and Treasury Inflation-Protected Securities (TIPS).

Government Bonds. Government agencies also issue bonds to help cover spending and finance projects. These are high-quality, liquid bonds and nearly as safe as Treasuries.

Municipal Bonds (aka Munis) are issued at the state and local levels (also to cover spending and to finance projects). Municipal bonds are exempt both from federal income tax and state income tax (from the issuing state). They’re not quite as safe as government bonds, but are appealing because of their favorable tax treatment for investors.

Corporate Bonds. Companies issue these bonds and carry the highest risk. Credit risk varies from high-quality bonds to high-yield junk bonds. Junk bonds have a higher yield because their credit rating is low (the lower the credit rating, the higher the risk). They’re also taxable at both the state and federal level.

Ways to Mitigate Risk: Mutual Funds

Investing in individual stocks is a high-risk investment. For example, if your life savings is stashed away in your employer’s company stock and your employer goes out of business, damn – nice knowin’ ya life savings.

But if you spread your money across hundreds or even thousands of stocks and one goes bankrupt, you won’t even notice. It’s called diversification, and it’s the number-one way to mitigate the risks associated with the stock market.

How Do Mutual Funds Work

Mutual funds are baskets of securities (usually stocks or bonds) with a pool of money from many investors. Mutual funds are run by a fund manager who picks the stocks based on that fund’s investment objective.

A mutual fund’s share price is called its net asset value (NAV).

The price you pay for a mutual fund depends on a few key factors:

- Expense ratios. This is the cost of operating the fund. Kind of like how you have to pay your utility bill to keep the lights on. Expense ratios are like that – they keep the lights on.

- Management fees. Some funds are actively managed, and that service comes with a price, usually between 1%-3% of assets under management.

- Front-end load. You pay this when buying the fund.

- Back-end load. You pay this when you sell it.

- Redemption fees. Selling a fund you’ve owned for a short time (usually between 60-90 days)

The type of fund you buy determines the amount you pay in fees. You want to minimize costs by purchasing funds that carry no sales loads (front-end and back-end loads) or transaction fees. No-load funds are what you want, and we think they’re the bee’s knees.

Another way to keep costs down is to sidestep professional management. Unless you have a complex portfolio with many moving parts, you probably don’t need a portfolio manager.

Invest in 2-3 low-cost index funds or exchange-traded funds (more on that in a minute) and get on with your life.

Most brokers get paid on commissions, so avoid the sales charge and buy the funds yourself. Do you see the conflict of interest? How do you keep costs down while the broker is trying to upsell you products that benefit the mutual fund company?

Investing in mutual funds has become the preferred method. It saves you the time of researching individual companies and instead, lets you invest in a portfolio of stocks (or bonds) based on your financial goals.

How Do Mutual Funds Pay

The two primary ways you get paid from mutual funds are:

- Dividends

- Capital Gains

Dividends come from owning stock in a fund’s portfolio. The fund pays investors virtually all of its annual net earnings throughout the year. If you have a bond fund, income is earned from the interest. Investors have a choice to reinvest the earnings or take a cash payment.

Capital gains occur when you sell your shares for a profit (i.e., you’re selling them for more than you originally paid). It’s wise to hold your shares for at least a year to avoid the short-term capital gains tax (it taxes you at your ordinary-income rate versus a lower rate if held for over one year).

Different Types of Mutual Funds

There are many types of mutual funds representing portions of the market. There are large-cap, mid-cap, and small-cap funds based on a company’s size while other funds track a market index like the S&P 500.

Growth funds are companies expected to have high earnings while value funds (Warren Buffet’s method of choice) are seen as undervalued companies who have fallen out of fashion with investors (though still potentially have solid earnings and excellent management).

Let’s take a look at a few types of mutual funds.

Fixed-Income Funds (aka bonds). Just as the name implies, these funds provide you with a steady income stream. These are bond funds invested in government and corporate debt. They become interest-generating cash-flow instruments when held to maturity.

Money Market Funds. Short-term debt in the form of government treasury bills. This is a virtually risk-free investment. Because of the low-risk, the return is equally low.

Equity Funds (aka stock funds). These funds invest in baskets of stocks and come in all shapes and sizes. Offerings have grown into the thousands. There’s an equity fund for virtually every investor – U.S., international, sector funds (e.g., technology or energy), and on and on.

Target-Date Funds. These funds are a mix of stocks and bonds with a built-in retirement date. The fund rebalances your portfolio automatically and adjusts your stock-to-bond asset allocation (i.e., your portfolio will carry less and less stock the closer you are to retirement).

Depending on your preferred level of risk, there’s a mutual fund to match. If you’re looking for stability with low-risk, perhaps government bonds are the way to go. Or, if you’re looking for a bigger payoff while assuming a larger risk premium, a U.S. total stock fund might make more sense.

The number of shares found in mutual funds differs widely. Hundreds or even thousands of holdings can be found. Vanguard’s Total Stock Market Index Fund holds 3,637 stocks!

Index Funds

Index funds are the low-cost leader of the mutual fund universe. These guys don’t try to beat the market but instead mirror an index.

These funds are passively managed (usually by a computer with a human at the helm to ensure the fund doesn’t stray off course from the index being monitored).

Index funds seek to duplicate the returns of the market. They require little research by “analysts”(another reason for their low cost).

When considering your investment strategy, ask yourself what kind of portfolio you want to build. If you need some inspiration, below are several model portfolios you can use to get started:

- Swensen Portfolio

- Coffeehouse Portfolio

- Ivy Portfolio

- Minimum Variance Portfolio

- Larry Portfolio

- All Weather Portfolio

The Permanent Portfolio (PP) is a portfolio evenly split between stocks, bonds, gold, and cash. It’s best suited for risk-averse investors wanting to minimize losses while still receiving modest returns.

Harry Browne designed the above Permanent Portfolio using four uncorrelated asset classes that respond differently to specific market conditions.

Final Thoughts

Wealth building takes time and should be viewed as a long-term investment. When you’re younger, opt for a portfolio with a heavier percentage of stocks to bonds (for example, 80/20 or 90/10).

Stocks carry more risk, are more volatile, but you can expect higher returns. Bonds are less risky, provide a fixed-income stream, while preserving capital.

You can reduce your risk by purchasing mutual funds, which are baskets of securities that provide instant diversification. Index funds or exchange-traded funds (ETFs) have the lowest costs and are the most tax-efficient.

And now you understand how stocks, bonds, and funds work. Happy investing!