- Vanguard vs. Fidelity: Who Are They?

- Minimum Investment Requirements

- Financial Advice

- Fees and Costs

- Index Funds, ETFs, and What’s the Difference?

- Building a Core-Four Portfolio: Which Brokerage Service Is Better?

- U.S. Equities: Total Stock Market Funds

- REITs

- Results

- User Experience and Mobile App

- Unique Offerings

- Final Thoughts

Vanguard vs Fidelity conjures up an epic image of two warriors battling it out in the Roman Colosseum. Who will prevail in the coveted wealth management arena? If I were new to investing, I’d want to know who’s best (spoiler alert – they’re both stellar companies offering exceptional products).

But still… what would I want to know?

As an investor, I’m concerned with:

- Fees

- Operating costs

- Minimum investment requirements

- Product offerings and if they’re aligned with my needs

Investing is a core part of LMM’s wealth-building strategy and a few low-cost index funds are its foundation.

I will show you how these two brokerage firms stack up in terms of pricing, fees, and investment products. I will also show you some things that make these companies unique.

We will also compare a lazy-four fund portfolio using only Vanguard funds in one example and only Fidelity funds in another – just for fun. How will they measure up?

Let’s find out.

Vanguard vs. Fidelity: Who Are They?

Fidelity distinguishes itself from Vanguard by offering platforms tailored for active traders, such as the customizable Active Trader Pro, which provides advanced charting tools and real-time analytics. In contrast, Vanguard does not offer a comparable trading platform, focusing instead on long-term investment strategies.

Additionally, Fidelity supports fractional share trading and a broader range of investment options, including cryptocurrencies, whereas Vanguard’s offerings are more limited in these areas.

Vanguard

Vanguard, founded in 1975 by John C. Bogle, pioneered the first index fund available to individual investors. As of September 30, 2024, Vanguard manages approximately $10.1 trillion in assets, serving over 50 million clients worldwide.

It remains the largest provider of mutual funds and the second-largest provider of ETFs globally, following BlackRock’s iShares. John Bogle was renowned for advocating lower costs for individual investors, a principle that continues to guide Vanguard’s operations.

- Traditional and Roth IRAs

- Annuities

- 529 College Savings Plans

- SEP, i401k, and SIMPLE IRAs

- 403(b) Services

- Individual and Joint Accounts

- 401(k) Rollovers

- Mutual Funds & ETFs

- Individual Stocks, Bonds, and CDs

- Sector Investing

- ESG (Environmental, Social, and Governance) Investing

- Advisory Services (Vanguard Personal Advisor Services and Digital Advisor)

- Trust Services

The Vanguard Wellington Fund, established in 1929, celebrated its 95th anniversary in 2024. This fund has successfully navigated significant financial downturns, including the Great Depression and the 2008 Financial Crisis. Vanguard is headquartered in Malvern, Pennsylvania.

Vanguard is owned by their funds so they are uniquely aligned with the interest of their investors. As a result, Vanguard funds usually have the lowest fee rate in their category. Mind you, signing up is more work and requires more decisions than Betterment.

Fidelity

Fidelity Investments, founded in 1946 by Edward C. Johnson II, has a 78-year track record of innovation and growth. It introduced the Puritan Fund, one of the first income-oriented mutual funds investing in common stocks.

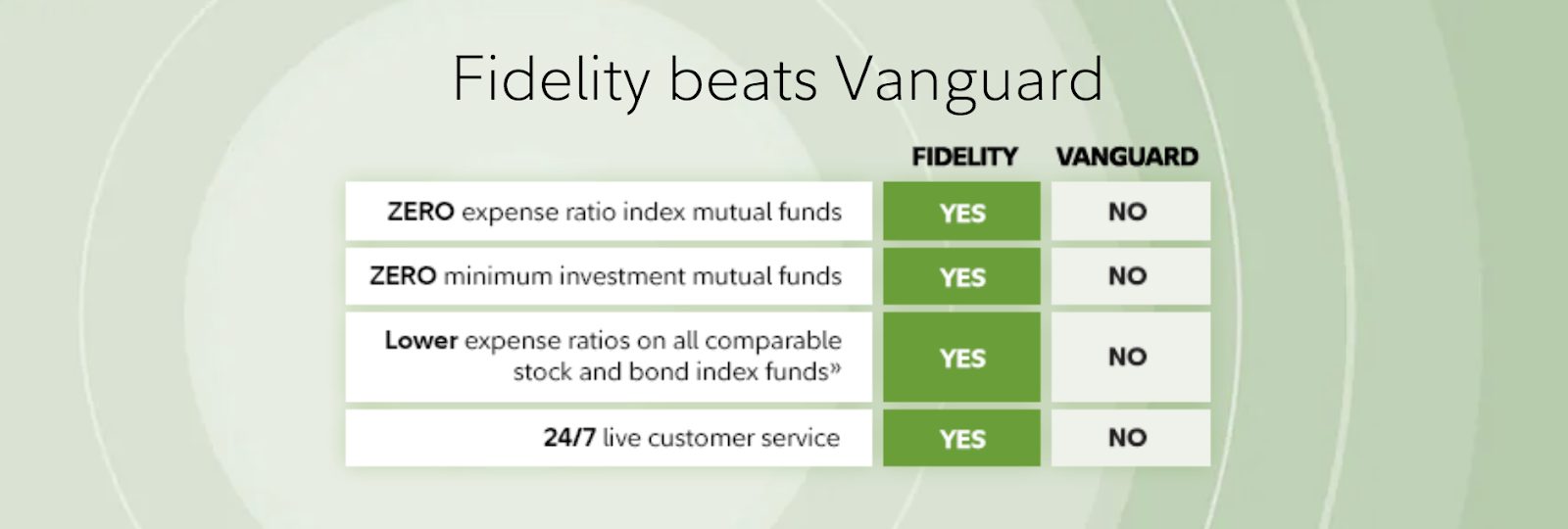

In 2018, Fidelity launched the industry’s first zero-expense-ratio mutual funds, the Fidelity ZERO Index Funds. As of September 2024, it manages $5.81 trillion in discretionary assets.

Fidelity Investments offers a comprehensive suite of financial products and services. Here’s an updated list of their current offerings:

- Mutual Funds

- SEP, SIMPLE, Traditional, and Roth IRAs

- Self-Employed 401(k)s

- Advanced Trading Platforms

- Options

- Stocks, Bonds, Certificates of Deposit (CDs), and Exchange-Traded Funds (ETFs)

- Annuities

- 529 College Savings Plans

- Cash Management and Credit Cards

- Factor-Based Investing

- Socially Responsible Investing (SRI)

- Structured Products

- Money Market Funds

- Fixed Income Annuities

They’re now one of the largest asset managers in the world and offer a broader array of investment products as compared to Vanguard. Fidelity has been rated the number one online broker by StockBrokers.com (2024), Real Simple in partnership with Investopedia (2024), and Investor’s Business Daily. Fidelity is headquartered in Boston, Massachusetts.

Minimum Investment:

$1,000

Management Fees:

0.04% - 0.30% advisory fee

Promotion:

Invest

Tax Loss Harvesting:

Yes

Portfolio Rebalancing:

Yes

Assets Under Management:

$5.3 trillion

Minimum Investment:

$0

Management Fees:

0.35% - 1.05% advisory fees

Promotion:

Open Your Account

Tax Loss Harvesting:

No

Portfolio Rebalancing:

Yes

Assets Under Management:

$2 trillion

Minimum Investment Requirements

Retail Mutual funds

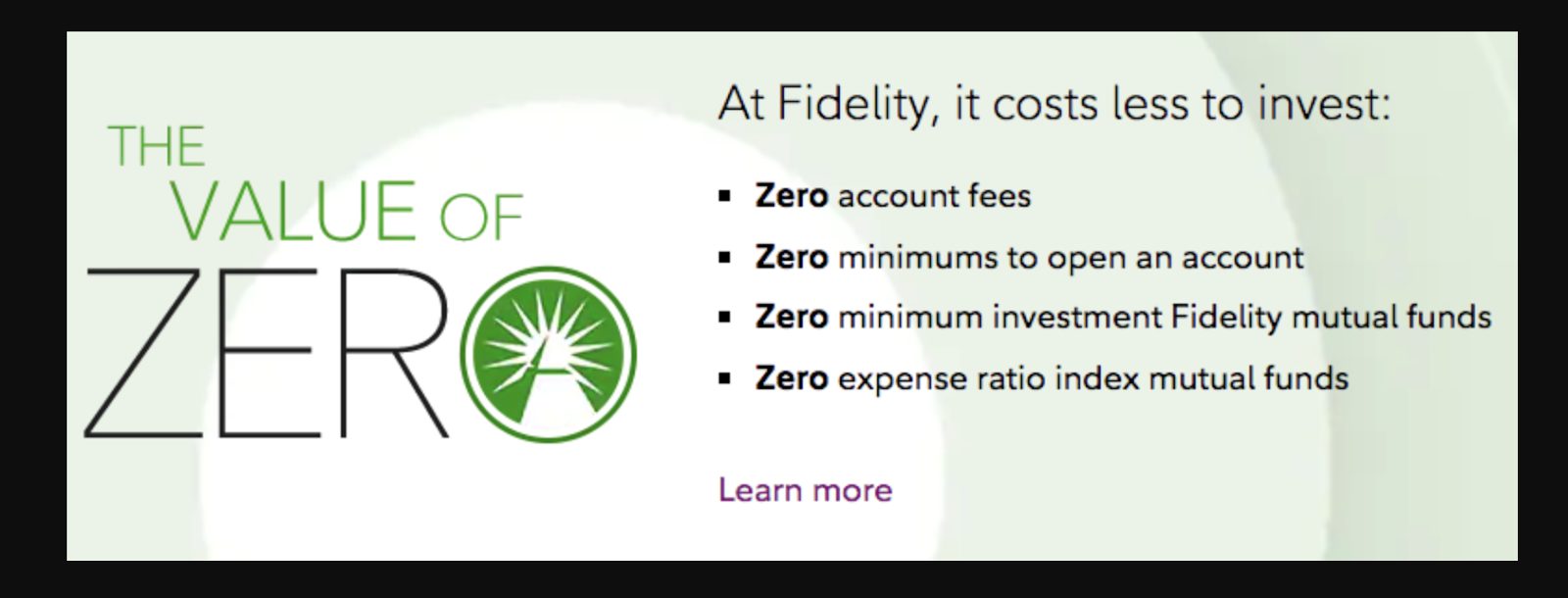

Many times, getting started is the biggest hurdle investors face. And sometimes, it’s because of the minimum investment requirements. Fortunately, Fidelity has no minimums to start investing, making it accessible if you have little money in the bank.

Vanguard funds typically require a $3,000 minimum, though some funds (like their Target Retirement Funds and STAR Fund) start at $1,000. ETFs, stocks, CDs, and bonds all cost the price of one share.

Fiscal flexibility that’s funny, free and delivered weekly.

Financial Advice

If you’re a hands-off investor who prefers professional management, working with a financial advisor can be an excellent option. Advisors provide tailored guidance, manage your portfolio, and help you navigate complex financial decisions.

For those who prioritize convenience and expertise, leveraging an advisor ensures your investments align with your long-term goals while saving you time and effort.

Vanguard

If your net worth is below $50,000, Vanguard offers Digital Advisor, their

For a customized financial plan, Vanguard’s advisory services charge a 0.30% annual fee for accounts under $5 million. The fee drops to 0.20% for investors with $5-$10 million in assets, 0.10% for assets between $10-$25 million, and 0.05% for accounts over $25 million. These fees are in addition to the underlying fund expense ratios.

You’ll have access to a financial dashboard with a bird’s eye view of your economic landscape. Your advisor will explore “what if” scenarios and test whether your asset mix is on track. You’ll also have reports on the projected range of balances for different market scenarios.

Fidelity

Fidelity offers investors various financial planning options, including their robo-advisor service, Fidelity Go. There is no minimum initial investment required to open a Fidelity Go account; however, a balance of at least $10 is necessary for the service to begin investing according to your chosen strategy.

For account balances under $25,000, Fidelity Go charges no advisory fee. Balances of $25,000 and above incur an annual advisory fee of 0.35%.

Additionally, accounts with balances of $25,000 or more gain access to financial coaching with Fidelity’s trained advisors.

If you require a human touch, Fidelity’s robo hybrid, Personalized Planning and Advice Service, offers digital investing and coaching for a $25,000 minimum and a 0.5% advisory fee.

Fidelity’s Wealth Management Service provides access to a dedicated advisor for clients with a minimum of $500,000 in eligible assets. The advisory fee ranges from 0.50% to 1.50%, depending on the level of service and assets under management.

For high-net-worth clients, Fidelity Private Wealth Management offers an advisor-led team and more personalized financial planning. This service requires a minimum of $2 million in managed assets or $10 million in total investable assets. Advisory fees for Private Wealth Management range from 0.20% to 1.04%, offering tiered rates based on asset levels and services.

Vanguard wins this round because their fee is lower. Vanguard’s advisory cost decreases the more you invest while Fidelity’s goes up.

Wealth Management Services

Vanguard’s advisory fees are generally lower than Fidelity’s for comparable services. Vanguard Personal Advisor Services charges a 0.30% annual advisory fee on assets under management, with a minimum investment of $50,000. For higher asset levels, Vanguard offers a tiered fee structure:

- Assets under $5 million: 0.30%

- $5 million to $10 million: 0.20%

- $10 million to $25 million: 0.10%

- Over $25 million: 0.05%

This tiered structure reduces the effective advisory fee as the investment amount increases.

In contrast, Fidelity’s advisory fees vary by program and asset level. For example, Fidelity Wealth Services has a gross advisory fee ranging from 0.50% to 1.50%, depending on the assets under management. Fidelity Private Wealth Management offers a tiered fee schedule, with fees decreasing as asset levels increase, ranging from 0.20% to 1.04%.

While both firms offer tiered fee structures that decrease with higher asset levels, Vanguard’s fees are generally lower across comparable asset tiers.

Fees and Costs

Stock Trading

Vanguard

Only a small number of Vanguard funds charge purchase or redemption fees, designed to offset high transaction costs and discourage short-term trading. These fees typically range from 0.25% to 1.00% and are reinvested into the fund to benefit long-term investors. The majority of Vanguard’s mutual funds and ETFs carry no commissions for buying and selling.

Vanguard previously had a tiered trading cost structure based on account balances, but as of July 2024, they have eliminated online trading commissions for stocks and ETFs. Broker-assisted trades and some specialized services may still incur fees, but most investors enjoy commission-free trading for standard transactions.

Vanguard previously employed a tiered commission structure for online stock trades based on account balances. However, as of July 1, 2024, Vanguard has eliminated online trading commissions for stocks and ETFs, aligning with industry standards. Broker-assisted trades and certain transactions may still incur fees, and specific account service fees may apply based on account type and balance.

Vanguard offers a wide selection of no-transaction-fee mutual funds and commission-free ETFs, providing investors with cost-effective options for building diversified portfolios.

Fidelity

Fidelity has eliminated commissions for online U.S. equity trades, including stocks and ETFs, aligning with industry standards. Broker-assisted trades and options trading may still incur fees; options trades carry a $0.65 per contract fee.

Fidelity’s platform is robust, featuring a suite of research tools and a team of trading specialists. Their award-winning Active Trader Pro platform offers advanced features and is part of Fidelity’s Decision Tech tools.

Fidelity provides tiered trading services with enhanced support:

- Active Trader Pro: Available to all customers who trade 36 times or more in a rolling 12-month period.

- Enhanced support and services: Fidelity offers various levels of service based on factors such as account balance and types of accounts held, rather than just trading frequency.

For the most up-to-date information on Fidelity’s trading services and support, it’s best to check their official website or contact Fidelity directly.

Fidelity offers over 3,500 no-transaction-fee mutual funds and commission-free trading for nearly all ETFs, providing a broad selection for investors seeking cost-effective options.

This extensive range of no-cost investment vehicles allows investors to build diversified portfolios without incurring additional trading fees, making Fidelity an attractive choice for both novice and experienced investors looking to minimize costs.

This one goes to Fidelity. If you like trading, they’re worth a look.

Expense Ratios

The average expense ratio for Vanguard mutual funds is 0.09%, which is 82% lower than the industry average of 0.50%. This low-cost approach ensures that investors pay only what it costs to run the fund. Vanguard’s commitment to low fees has influenced other brokerage firms, such as Fidelity, to offer competitive pricing—a phenomenon known as the “Vanguard Effect.”

“Expense ratios for a market’s mutual funds and ETFs tend to drop when low-cost pioneer vanguard jumps in.” – Marketwatch

“The pressure that the giant’s meager fees put on others to cut costs. Some rivals now sell passive products priced specifically to match or undercut it.” – The Economist

Fidelity has risen to the occasion and undercuts many of Vanguard’s operating costs. For example, Fidelity’s Total Market Index Fund is 0.015% and carries no minimum, while Vanguard’s Total Market Index Fund is 0.04% and has a $3,000 account minimum.

However, it’s worth noting that Vanguard now offers ETF versions of their funds, such as VTI (Total Stock Market ETF), which has an expense ratio of 0.03% and no minimum investment requirement6. This provides a more comparable low-cost option for investors who don’t meet the $3,000 minimum for VTSAX.

Fidelity wins here. Many of their funds now carry a lower cost than their Vanguard equivalent.

To determine how much you’re losing to fees, try Empower’s Fee Analyzer tool. It’s free to use and provides insights on ways to optimize your portfolio.

Empower's free fee analyzer helps you understand how investment fees affect your retirement savings. It analyzes your holdings, estimates future fee impact, and suggests ways to potentially save by lowering fees in your retirement portfolio.

Account Service Fee and Transfer Out Fees

Vanguard charges a $25 annual account service fee for each brokerage account. However, this fee is waived if you sign up for e-delivery of statements or have at least $5 million in qualifying Vanguard assets. Additionally, a $100 account closure or transfer-out fee was introduced in mid-2024 but is waived for clients with $5 million or more in assets.

Fidelity has no account service fees or transfer-out fees. However, fees may apply if transferring assets from another institution to Fidelity.

Index Funds, ETFs, and What’s the Difference?

Similarities between index funds and ETFs:

They both represent baskets of securities that provide built-in diversification. While professionally managed, these funds are passively managed to track a specific index. The manager’s role is to ensure the fund mirrors the index’s performance rather than making active investment decisions like stock-picking or timing the market.

If you’re looking for lower minimums, ETFs are often a better choice. Mutual funds, such as those from Vanguard, typically have minimum investment requirements ranging from $1,000 to $3,000. In contrast, you can invest in an ETF for the price of a single share, which can start as low as $50, depending on the ETF.

Mutual fund minimum initial investments aren’t based on the fund’s share price. Instead, they’re a flat dollar amount. – Vanguard

ETFs are priced in real-time, so the price fluctuates throughout the day like an individual stock. Mutual funds (index funds are just mutual funds tracking an index) don’t care about when you place a trade; you get the same price at the end of the trading day as everyone else.

ETFs traditionally didn’t support recurring deposits, but many brokerages now allow automatic investments, including for ETFs. Platforms like Fidelity even offer fractional share purchases, making it easier to set up recurring deposits. Most robo-advisors also enable automatic investments with fractional shares, simplifying the process further.

Let’s compare a few top funds from Vanguard and a few from Fidelity using index funds as examples.

Building a Core-Four Portfolio: Which Brokerage Service Is Better?

For this game, we’re going to use a lazy portfolio with four funds:

- Total Stock Market Index Fund (U.S. equities)

- Total International Stock Index Fund

- Total Bond Index Fund (U.S. fixed-income)

- Real Estate Investment Trust (REIT)

U.S. Equities: Total Stock Market Funds

Fidelity Total Market Index Fund (FSKAX) vs. Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX)

This wise sentiment sums up the creation of index funds:

Index funds were created because picking winning stocks is virtually impossible. It’s like trying to find a needle in a haystack. Instead, buy the haystack.

Vanguard’s expense ratio is 0.04% (40 cents for every $1,000 invested) while Fidelity’s is 0.015% (15 cents for every $1,000 invested).

Both of these costs are insanely low. Remember the Vanguard Effect? The competition has made it its mission to tackle Vanguard’s low fees.

Each fund has a broad portfolio of stocks, with VTSAX holding approximately 3,599 stocks and FSKAX holding around 3,840 stocks as of October 31, 2024. Both funds have delivered similar returns, though Fidelity’s inception date is more recent. Since inception, VTSAX has had an average annual return of 8.63%, while FSKAX has returned 14.44%.

- 8.63% average return since inception (as of October 31, 2024)

- 0.04% expense ratio

- $3,000 minimum

- 14.44% average return since inception (as of October 31, 2024)

- 0.015% expense ratio

- $0 minimum

Winner: Fidelity.

Award-winning trading platform with robust investing tools, straightforward pricing, and wealth management services.

Fidelity Total International Index Fund (FTIHX) vs. Vanguard Total International Stock Index Admiral Shares (VTIAX)

For international exposure, we’re going to take on a global stock index fund. Again, both funds are insanely low cost.

- 4.89% average return since inception (as of October 31, 2024)

- 0.12% expense ratio

- $3,000 minimum investment

- 6.74% average return since inception (as of October 31, 2024)

- 0.06% expense ratio

- $0 minimum investment

Winner: Fidelity.

Fidelity Total Bond Fund (FTBFX) vs. Vanguard Total Bond Market Index Fund Admiral Shares (VBTLX)

These total bond funds have slightly different holdings, but it’s as close as we’re getting for this round.

FTBFX is a core-plus fund. What’s this?

It takes on adding securities with a greater return/risk component to a core base of holdings with a specified objective – Investopedia

In other words, it invests 80% in investment-grade bonds and 20% in below-investment-grade securities to boost return potential.

VBTLX is classified as a low-cost core fund. What’s this?

It’s a single diversified bond fund product with broad exposure to the investment-grade area of the bond market, primarily in US treasuries. – The Balance.

It’s primarily concentrated in government-backed securities.

- 4.19% average return

- 0.05% expense ratio

- $3,000 minimum

- 4.89% average return

- 0.45% expense ratio

- $0 minimum

Winner: Too close to call. Returnis better for FTBFX, but Fidelity’s expense ratio is higher.

REITs

Fidelity Real Estate Index Fund (FSRNX) vs. Vanguard Real Estate Index Fund Admiral Shares (VGSLX)

Real estate isn’t correlated to either the stock or bond market and adds another layer of diversification to your portfolio.

Fidelity’s Real Estate Index Fund, FSRNX, primarily invests in domestic equities within the real estate sector. Its top holdings include companies focused on industrial, office, and data center properties, such as Prologis, Inc. and American Tower Corporation, along with exposure to other real estate sectors.

Vanguard’s Real Estate Index Admiral Shares VGSLX also invests heavily in domestic real estate equities. Its holdings show notable exposure to industrial, office, and data center properties while maintaining significant investments in retail and residential sectors for broader market coverage.

- 9.31% average annual return since inception (as of October 31, 2024)

- 0.13% expense ratio

- $3,000 minimum investment

- 7.40% average annual return since inception (as of October 31, 2024)

- 0.07% expense ratio

- $0 minimum investment

No Clear Winner: Vanguard has a higher return, but Fidelity has an edge with a lower expense ratio and a $0 minimum investment.

Results

Vanguard total costs:

- $12,000 needed to open an account for these four funds

- 0.08% average expense ratio

- 6.76% cumulative portfolio return

Fidelity total costs:

- $0 needed to open accounts

- 0.149% average expense ratio

- 8.37% cumulative portfolio return

Fidelity wins on both minimums and average return, while Vanguard wins on expense ratios. Does this make Fidelity better than Vanguard? In this round, maybe, but depending on your needs, your expenses will vary.

User Experience and Mobile App

Both Vanguard and Fidelity offer mobile applications compatible with iOS and Android devices, enabling users to manage their investments on the go. The Vanguard app allows users to check balances, track performance, make trades, and deposit checks.

Similarly, the Fidelity Investments app provides access to account balances, trading capabilities, and investment research. Therefore, both platforms are iOS and Android-friendly, offering convenient mobile access to investment accounts.

Unique Offerings

Fidelity

Fidelity unleashed four zero-expense ratio mutual funds between August and September 2018 – the first retail brokerage firm to do this. All to undercut competitors. The four funds are passively managed, tracking a corresponding index. The funds are:

- Zero Total Market Index Fund (domestic equities)

- Zero International Index Fund: tracks ~75% developed and ~25% emerging international markets

- Zero Extended Market Index Fund: small-cap equivalent

- Zero Large Cap Index Fund: S&P 500 equivalent

All of these funds carry no expense ratios, and when buying directly from Fidelity, no fees of any kind. These funds are meant to bring cost-conscious investors to the table.

One way Fidelity keeps costs down is by creating its indexes to track so they avoid licensing fees (from the S&P 500 or MSCI for example).

For the Total Market Index Fund, Fidelity created the Fidelity U.S. Total Investable Market Index. The International Index Fund tracks the Fidelity Global ex-U.S. Index.

The fee-free funds hold fewer stocks than their counterparts with expense ratios. The Total Market Index tracks around 2,500 stocks compared to approximately 3,500 in Vanguard’s Total Stock Market Index Fund. Similarly, the International Index Fund holds about 2,300 stocks versus the 4,735 held by Fidelity’s Total International Index Fund.

Fidelity’s ZERO expense ratio mutual funds have been available for a little over six years, as they were launched in August 2018.

Vanguard

They’ve been the low-cost leader for decades ever since John Bogle created the first index fund revolutionizing the industry and lowering costs for ordinary investors.

They’re also client-owned. You, a shareholder of Vanguard funds, own a piece of the company. You only pay the cost of operating the fund. When outside influences (aka outside stockholders or third parties) own an investment management company, the company has to pay the shareholders (translation: more fees to you).

Because Vanguard is client-owned, there’s no pressure to generate profits for shareholders.

Tweet ThisClients and company owners are never pitted against one another because they’re the same.

Heartbeat Trades

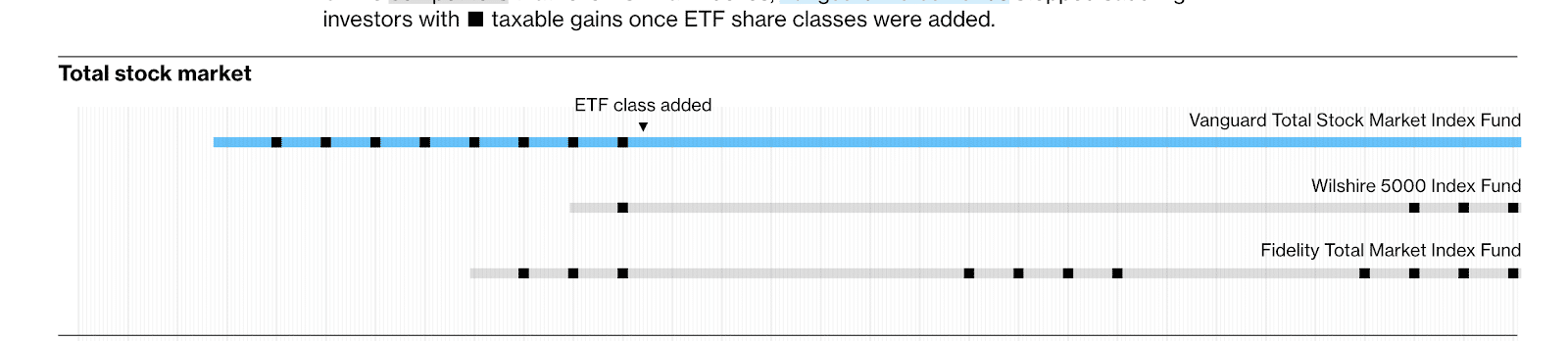

Vanguard has utilized heartbeat trades to pass along tax savings to investors. This process involves large, temporary inflows and outflows of capital—creating a “heartbeat” pattern—to enable in-kind redemption of appreciated securities, deferring capital gains taxes for investors.

They also developed a patented system in 2001 to integrate ETFs as a share class within their mutual funds, reducing taxable events. This innovation, detailed in Bloomberg’s analysis, allowed Vanguard to minimize capital gains distributions across 14 stock funds. Between 2000 and 2018, this system helped the company avoid reporting approximately $191 billion in gains to the IRS, and investors in Vanguard’s total stock market fund paid $0 in capital gains.

These techniques have drawn some controversy, as they defer taxes in ways that some argue could create disparities in tax fairness. The patent expired in May 2023, opening the door for other firms to adopt similar methods. While commonly used for exchange-traded funds (ETFs), Vanguard’s approach extended these benefits to mutual funds, enhancing tax efficiency for its investors.

Here’s how the folks at Bloomberg put it:

Vanguard attaches a more tax-efficient ETF to an existing mutual fund. Then the ETF siphons appreciated stocks out of the mutual fund without incurring taxes, often using heartbeat trades.

It’s referred to as a “tax dialysis machine.” Vanguard patented this structure until 2023, keeping competitors at bay, and unable to duplicate it. Investors in Vanguard mutual funds have the luxury of paying zero capital gains until selling the fund.

Source: Bloomberg

Because Vanguard added an ETF share class to existing mutual funds (and didn’t create a stand-alone ETF), mutual fund and ETF investors would own the same pool of underlying stocks.

What does this mean for Vanguard mutual fund investors? Enhanced tax-efficiency. This article goes into great detail about the ETF tax dodge. It’s all perfectly legal.

Bottom line, once Vanguard added an ETF class back in 2001, investors largely ceased paying capital gains in those corresponding funds. However, as of December 2024, certain Vanguard funds, including the Total Stock Market Index Fund, are expected to distribute taxable capital gains. Investors in Vanguard mutual funds have benefited from this tax loophole – but recent developments suggest this trend may be changing.

Final Thoughts

Vanguard vs Fidelity: Who’s the Best Brokerage Service?

Vanguard and Fidelity are two giants in the investment world, each catering to slightly different audiences. Vanguard excels in low-cost index funds and long-term, buy-and-hold investing, thanks to its unique client-owned structure.

Fidelity, on the other hand, stands out for its tech-savvy platform, zero-expense-ratio funds, and robust research tools, appealing to both active and passive investors. The “best” choice ultimately depends on your investment style and priorities—whether it’s cutting-edge tools or a focus on long-term cost savings.

This comes down to a gut decision. If one feels better, go with them. There’s plenty of value to be had with both companies. They’re established, time-tested, and have displayed why they’re leaders in the retail investing world.