What’s a mere 1%? It’s significant when it comes to fees. Discover the long-term impact of fees on your investments. They can erode your savings more than you think, potentially devastating your retirement funds.

Actively Managed Accounts Underperform

It’s important to be aware that historically, actively managed accounts and funds may underperform the broad market index, like the S&P 500, over the long term. This is because actively managed accounts typically charge higher fees, and attempting to beat the market consistently can be challenging.

According to the analysis, 99 percent of actively managed US equity funds sold in Europe have failed to beat the S&P 500 over the past 10 years, while only two in every 100 global equity funds have outperformed the S&P Global 1200 since 2006. Almost 97 percent of emerging market funds have underperformed.

But what about all the markets ups and downs? You need someone with expertise to make sure you don’t lose all of your money when the market is volatile. You don’t. Andrew did the math.

If you had invested $10,000 in 1990 in the S&P 500 and just let it ride until 2017, you would end up with $137,000, an average return of 11.3% per year. Those 28 years included two of the worst recessions in our lifetimes, 2001 and 2008.

The total return in that time was 1,058%! You made $127,000. The only way you would have lost money would have been if you had sold.

Your investments should be generally boring.

Tweet ThisThat’s how you get rich. It’s not sexy and exciting, but it works.

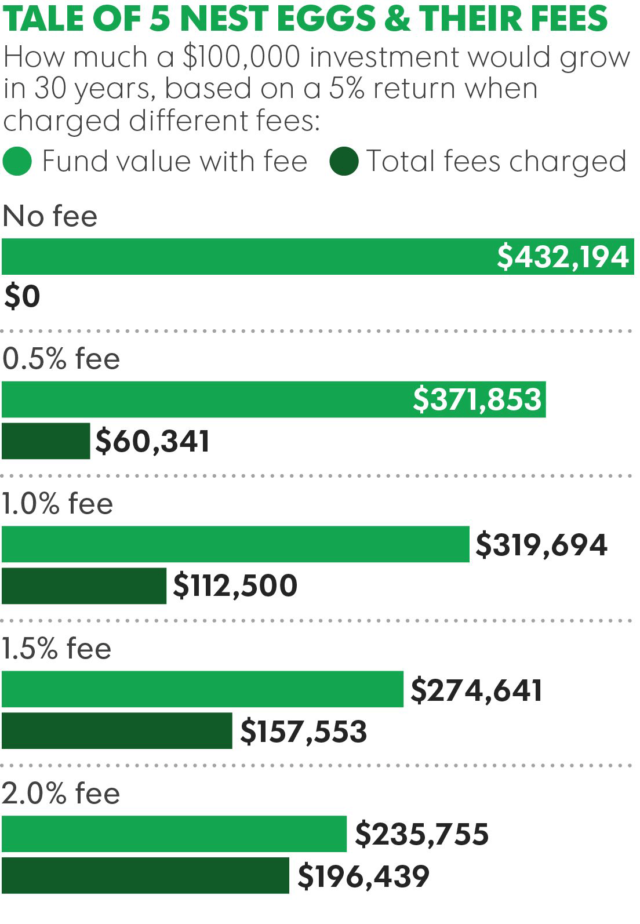

What’s So Scary About 1%?

Okay, well what if in that scenario you were paying a 1% management fee?

One percent is tiny; it’s nothing! It’s a single penny on each dollar. But just as exponential growth is the reason we invest, exponential growth is the reason we avoid high fees.

In our above scenario, at 1% we would have paid $11,000 in fees. You’re not earning exponentially on the money you earn when fees are eating into it. With a 1% fee over that 28 years, we weren’t earning an 11.3% return. We only made $95,800. We lost 24%, nearly a damn quarter of our gains!

If your advisor told you up front that his or her fee would be 24%, would you say yes? Of course not. But that is what you are saying yes to when you say yes to high fees.

Fiscal flexibility that’s funny, free and delivered weekly.

Preying on the Ignorant

Advisors that charge high management fees are preying on the ignorance of many investors. Money and investing all seem so complicated, and they can be. So, of course, you need someone who knows what they are doing to help you. This is your money! You can’t gamble with it.

And investing can be complicated, we make lots of things harder than they need to be. But investing doesn’t have to be cumbersome and you don’t need some specialized knowledge to make money in the stock market.

It’s like cleaning my house. I don’t like doing it, so I pay someone else to do it for me. But cleaning my house isn’t hard or complicated. I could do it if I wanted to or had to. And if my cleaner were charging me 24% of my income to do it, of course, I would do it myself. Handling your own money is the same. You might not like doing it but you can do it, and it will cost you less than paying someone else, way less.

But You Have This Whiz Kid

Your advisor is different, wears expensive clothes, has a fancy office, drives a swanky car. They must be doing something right; surely they are worth whatever management fee they are charging. Well, there is one way to find out.

Ask to see their portfolio and the returns. If they are outperforming the index and have been for some time, you have found the golden ticket. But trust us, they aren’t, and you haven’t.

But I Like My Guy or Gal

You have been with your advisor for years and so have several members of your family. If you dump them, they will be hurt. It’s like breaking up with a lover.

But it’s not. No matter how unique you think your relationship is, you are just another client to them. They may not make you feel like that; they make you feel like you are their only client, their most special client.

That’s because they are a salesperson and making you feel that way is part of their job. It’s true of your favorite stripper too. Sorry to be the one to tell you.

Fee Finder

So how can you find out how much you are paying in fees? You can read through the dull prospectus, but there is an easier way.

Personal Capital has a Fee Analyzer that will hunt them down for you. You can visit their site, register your account and add in financial institutions much like Mint.

From there you’ll go to the Investments header in the top right, and click 401k Fee Analyzer. On the page, you’ll be greeted with an excellent graph of your potential 401k earnings.

If your only 401k is the one you have with your current employer, there may not be much you can do about this. The best you can do is read through all of your fund choices and choose the one with the lowest fee.

If you have 401k’s scattered around at previous employers, there is a lot you can do. When you leave a job and leave a 401k behind, the 401k company may charge you an administration fee to continue managing the money of a former employee. This is on top of any other fees you are being charged.

If your new employer has a 401k, you can to a direct transfer from your old plan to the new one without having to pay taxes or an early withdrawal penalty.

If your new employer doesn’t offer a 401k or you don’t like any of the choices, you can do an indirect rollover. You get a check for the amount of your account, and you have 60 days to complete the rollover by putting the money into an IRA. If you miss the 60-day window, you will be taxed on the amount, and if you are younger than 591/2, you will be hit with a 10% penalty.

So What is a Fair Fee?

No one works for free, and there are costs involved in investing. So what kind of fee should you be looking for?

Well, no fee is pretty impressive and you can get that when you buy stocks through Robinhood. But you have to choose your own stocks which means you are actively managing your money. And we told you that actively managed money does not beat an index.

A good rule of thumb is to look for a management fee under 0.4%. Vanguard’s Total Stock Market Index Fund charges a fee of 0.15%.

This is Your Money

We are talking about your money, and no one is ever going to care about it as much as you do. It’s your responsibility to understand what is happening in your investments. As we said, investing can be complicated, but it doesn’t have to be.

We have written about all things investing, from getting started, to overcoming your fear, to investing on a small income. You don’t have to be the type who devours and understands the Wall Street Journal every morning, but you do have to know the basics. And you do you have to know what fees you are paying. Because when it comes to management fees, that is the scariest 1%.

Show Notes

Serpent’s Stout: An American Double, Imperial stout.

How Not To Be Wrong: The math behind everyday things.