Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Many people are afraid to get started investing. Some are scared to lose money, feel they don’t have enough money or it can be due to lack of personal finance knowledge.

Investing is not hard and anyone can do it. You can start investing with any amount of money and the earlier you start, the better. We’ll explain the fundamental concepts, lingo, types of investments and the basics of how to start investing. You got this!

No Time Like The Present

Well, there is a better time than right now to start investing and that time was when you were 18, the age you have to be to open an investment account. But most of us didn’t have money on our minds when we were 18 so the second best time to start investing is now. Right now. Without investing as early as possible, it will be hard to reach your financial goals.

The Two Magic Ingredients

You don’t need a lot of money to invest or some insider information or innate intuition regarding what to invest in to make money in the stock market. What you do need are the two magic ingredients of compounding interest and time (and a little personal finance knowledge).

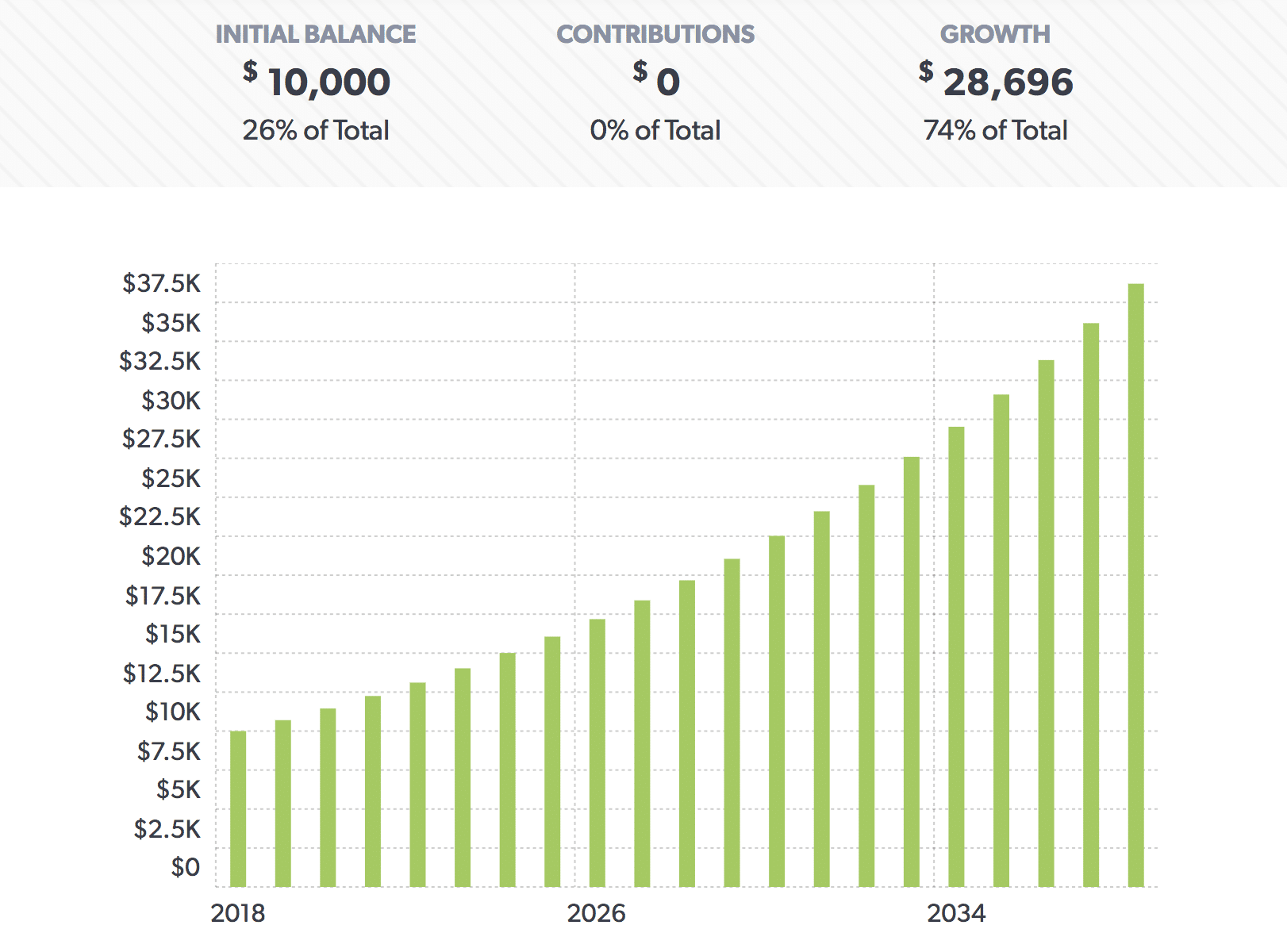

Compound interest is the interest you earn on your interest. That’s hard to understand, here is an example.

If you invest $10,000 at 7% interest for 20 years without adding anything to the initial investment, that $10,000 will turn into $38,696.84.

You didn’t do anything to earn that extra money, you didn’t even add anything to your initial investment, and like magic, you end up with an additional $28,696.84! That’s the power of compounding interest.

The other ingredient is time for the compounding interest to do its thing. There is no substitute for time when it comes to growing your money. Don’t believe us? Take a look at the numbers.

Example 1:

Ryan invested $1,000 a month from ages 25-35. He didn’t invest any additional money, but he didn’t touch the $120,000 invested until he retired at 65.

Example 2:

Elizabeth got a later start. She invested the same $1,000 a month for ten years at 7% but did not start investing until she was 35. No further contributions but the money was left to grow until Elizabeth retired at 65.

Example 3:

Amanda got a really late start. She invested $1,000 a month for ten years at 7% but not until she was 45. No additional investments and the money grew by 7% until Amanda retired at 65.

So how did each of our investors do?

Each invested the same amount of money, $120,000 for the same amount of time, ten years, at the same average return of 7%.

Ryan: $1,444,969

Elizabeth: $734,539

Amanda: $373,407

The numbers speak for themselves. The only thing different between these three investors is the amount of time their money had to grow. There is no substitute for time when it comes to investing.

Fiscal flexibility that’s funny, free and delivered weekly.

Investing 101

Investing can be complicated, timing the stock market, short selling, day trading, opportunity funds, but it doesn’t have to be, and you don’t have to know anything to get started. But you want to understand some basics of investing.

Common Types of Investments

When many people hear the word “investing” they think of stocks, and while individual stocks are one type of investment, they are not the only kind. These are the most common types of investments.

Stocks: When you buy a share of stock, you are buying a tiny bit of a company. Stock prices follow a company’s ups and downs and those of the broader economy.

Bonds: Buying a bond is lending money to the entity that issued it. That entity could be a corporation or a government. In exchange for the loan, the bondholder receives interest payments over a predetermined period, and the principal is repaid when the bond matures.

Investment Funds: These are things like mutual funds and ETF’s, exchange-traded funds. Lots of investors pool their money and invest it based on a particular strategy (lifecycle funds, tax-efficient funds, etc.). Your 401k and Roth accounts are examples of mutual funds.

Real Estate: Real estate investments can include the home you live in,

CD’s: A certificate of deposit is similar to a savings account but pays higher interest, and your money cannot be withdrawn for an agreed upon amount of time without penalty.

Money Market Account: A MMA is a type of savings account that you can write checks from and have a debit card for that pays slightly higher interest than a standard savings account and typically has a higher minimum balance.

This list covers the most common types of investments. There are others, but these are what most beginners will be dealing with.

Retirement Accounts

We gave these accounts a separate section because they will make up a significant portion of most people’s portfolios and because there are limits to how much you can contribute to them yearly and penalties for withdrawing funds from them before a certain age (although there are some exceptions).

401K: This is the first foray into investing for many people because they are offered by employers. A 401k is an easy way to save because the money is taken from your paycheck before you get a chance to spend it.

Some employers offer to match. If you invest 6% of your income, for example, the company will match 3%.You should at least invest enough to get the match because that is free money. It’s a great way to start your nest egg.

IRA’s: There are two basic types, Traditional and Roth. A Traditional IRA lets you invest pre-tax income into a brokerage account that will grow tax-deferred. The money is not taxed until you withdraw it. You can withdraw funds after age 59.5.

A Roth IRA is similar to a Traditional, but the money is taxed up front and not upon withdrawal after age 59.5. We did a deep dive with the Mad Fientiest about IRA strategies.

Learning the Lingo

There are so many investing terms that it can almost seem like a foreign language. But you don’t have to be fluent; you just need to know some basics.

Investment Portfolio

An investment portfolio is a collection of assets. Your portfolio can include all of the investment types we discussed above.

here should be further diversification.

Diversification is an established tenet of conservative investment.

Tweet ThisDiversification

Being diversified means spreading your investments out to reduce your risk. The old cliche about not keeping all your eggs in one basket.

You want several different kinds of investments; stocks, bonds, real estate, cash. And within those categories, there should be further diversification.

You should own stocks in companies across several different industries, tech, healthcare, energy, etc. and a mix of domestic and international firms within those.

The bond funds in your portfolio should include US Treasuries, municipals, foreign bonds, and emerging market bonds.

Asset Allocation

Stocks are riskier but have a higher return. When you’re young, you can afford to take more risk because you have years to ride out the ups and downs of the stock market.

“When it comes to investing, the biggest and most important decision revolving your portfolio is asset allocation. Jack Bogle, the founder and former CEO of The Vanguard Group, once said, “The most fundamental decision of investing is the allocation of your assets: How much should you own in stocks? How much should you own in bonds? How much should you own in cash reserve?”

As you get older and have fewer years to ride things out, you want to invest more heavily in bonds. There will be lower returns but so is the risk.

Rebalancing

Your portfolio has a certain asset allocation. An example would be 50% stocks and 50% bonds. That allocation can change. If bonds are doing well and stocks are doing poorly, your allocation is no longer 50/50.

To rebalance, you need to sell off some of your assets and buy some others to bring your portfolio back into balance.

If you have $500 in stocks and $500 in bonds and you lose $100 in stock value, you take $100 from your bonds and buy stock. That sounds crazy.

Why would you take money from something doing well and put it into something doing poorly?!

Rule #1 of investing is to buy low and sell high.

Stocks are low so now is the time to buy. Bonds are high so now is the time to sell.

You may pay capital gains taxes when you sell investments, but that can be mitigated through tax loss harvesting which companies like

Dividends

When you own stock in a company, you may receive dividends. A dividend is a distribution of a portion of a company’s profits. They are decided by the board of directors and can be issued as cash payments, as shares of stock or other property.

It’s an opportunity for a company to reward shareholder loyalty. Investors, notably retired investors, like the steady income that dividend stocks provide and also like the option of reinvesting dividends to buy more shares of stock.

Dividends are a form of passive income.

Fees

People have no idea how much of their retirement money they are losing to fees; it can be as much as one-third of your money!

You might know what percentage you are paying but how much is that in real dollars? The average actively managed fund charges 1.25%. That doesn’t sound like much, but over time, it adds up.

It adds up to a lot. If you invest $100,000 in a fund with a 1% annual fee, which is less than average, it will cost you nearly $28,000 over twenty years, according to Securities and Exchange Commission calculations. If you had that $28,000 to invest, you would have earned another $12,000.

Under 1% is a good percentage to look for and you’ll find fees that low and lower with Index Funds and ETF’s. The average traditional index fund has a fee of 0.74%, and the average ETF fee is 0.44%.

Inflation

There are lots of reasons to invest and protect your money from inflation is one of them. Investing lets you save your money in an account where it grows more quickly than if you had just left it in a checking or savings account or stuffed under the proverbial mattress.

Many people are afraid of investing, so they leave their money in those places thinking the money is safer there.

But, if your money is in a bank account or kept as cash, it’s losing value because of inflation. Inflation is the rising cost of goods and services over time.

Inflation decreases the purchasing power of your money. The cost of things goes up, and the value of your money goes down.

The average rate of inflation in the US is 3.22%. If a pencil costs $1 now, a year from now it will cost $1.03 in a year. The average rate of interest on a checking account is 0.05%, and a savings account is 0.06%.

You can see that those rates aren’t even close to the rate of inflation. Inflation is eating into your money’s value when you leave it sitting in those low yield accounts.

Roll Overs

When you leave a job, you should bring your 401k with you. You will have more options for better investments with lower management fees. It’s also a mistake to have money scattered all over, it makes it hard to manage and keep tabs on.

Open a Roth IRA if you don’t already have one and tell your 401k plan that you want a direct rollover. They will send the money directly to your IRA and not to you which is essential for tax reasons.

Investment Time Horizon

Investment time horizon means how long you plan to keep an investment. Your time horizon will help determine what kind of investments you select for your portfolio. The longer you plan to hold an investment, the riskier your portfolio can be.

Short term is money you will need in five years or less. This money should either be invested very conservatively in something like a CD or a savings account. A short-term goal would be something like a vacation.

Medium term is money you will need in five to ten years. You can afford to take a little more risk with this money, something like a 30%/70% split between stocks and bonds. A medium-term goal would be like saving for a home.

Long-term money is money you will need in ten years or more. This money should be your “all in” money and invested at the highest risk level you can tolerate, perhaps even as high as 90%/10% split between stocks and bonds. Long-term money is invested for your retirement.

Before You Start Investing

Investing is ultra-mega essential, but there are a few things we need to take care of first.

Pay off Your Bad Debt

If you have debt, should you invest or wait until the debt is paid off? The answer largely depends on what type of debt you have and how much the interest rate is.

If you can make more through investing, you can expect an average return at about 7% return a year; then you are paying in interest on debt, then the answer is yes. If you have low-interest debt like federal student loan debt or mortgage debt, then yes. You should be investing.

If you have high interest like credit card debt, it’s better to focus on paying that off first.

In an interview with Justin Krane, he made an interesting point. As a financial advisor, He says that we do both, invest and pay off debt at the same time. When you are slogging away paying the debt, it can be easy to get discouraged. You don’t have anything to “show” for the money that went to pay the debt off.

When you do both, you can at least see some progress in your financial life because you know your money is growing in an investment account.

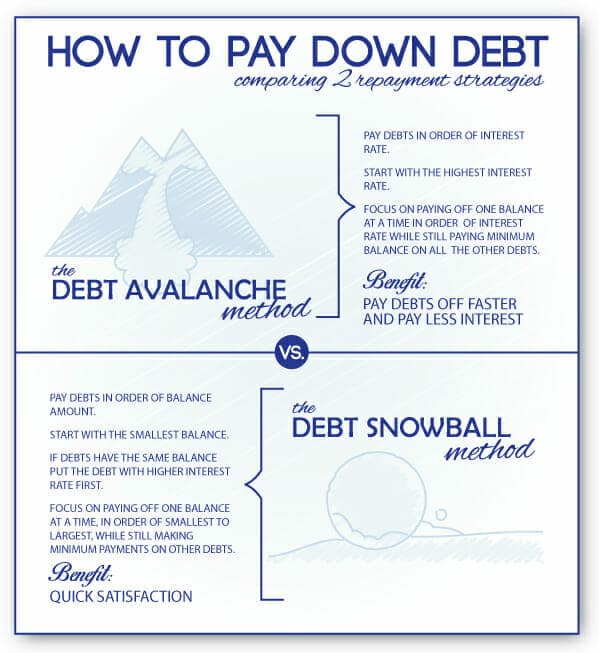

Does this always make financial sense? Not if the interest on your debt is higher than what you can earn through investing, but humans are not always rational creatures, often we are emotional creatures. That’s why for some of us it’s better to use the snowball method of debt repayment than the stacking method.

The stacking method saves you money but the snowball method gives you emotional wins. Those emotional successes can help us keep up our motivation.

Another scenario where it makes sense to invest while you have debt is if your employer-sponsored 401k offers to match.

That is free money, and you should never walk away from free money.

Start an Emergency Fund

Just as important as investing is having an emergency fund. An emergency fund is 3-6 months worth of bare-bones expenses that you keep on hand in the event of something like a job loss, a medical, home or car expense.

Not having one when disaster hits can set you back months and even years on the road to financial independence. There is a lot of debate about exactly how much it should be and where it should be kept, but at the very least you want to have $1,000 saved for something unforeseen.

How to Start Investing Step by Step

If you’re nervous about investing, we’re going to walk you through it. We’ll go one step at a time and at the end, you’ll be an investor.

How Much Can You Invest?

You don’t want to invest whatever is left over at the end of the month because often there isn’t anything left. We have to pay ourselves first. That means the money we’re going to invest is allocated ahead of time just like the money for the rent or mortgage.

Take that money and divide it into short, medium and long-term investments. How much you dedicate to each depends on what the investment goals are for each horizon.

Don’t worry if you don’t have a lot of money to invest. Remember, time is more important.

What’s Life Without Risk?

When deciding how to invest your money, you need to determine your risk tolerance and the time horizon of the money. Remember, the sooner you need the money, the less risk you can take with it.

Part of your risk tolerance will be based on your age. You can tweak numbers based on other personal circumstances, but a good rule of thumb is to base your asset allocation based on your age. You subtract your age from 120 to get the right ratio:

| Age | % of Stock | % of Bonds |

|---|---|---|

| 18-25 | 100% | 0% |

| 30 | 90% | 10% |

| 35 | 85% | 15% |

| 40 | 80% | 20% |

| 45 | 75% | 25% |

| 50 | 70% | 30% |

| 55 | 65% | 35% |

| 60 | 60% | 40% |

| 65 | 55% | 45% |

| 70 | 50% | 50% |

| 75+ | 45% | 55% |

You get the point. The old formula subtracted your age from 100, but people are living longer now, so the formula was amended to reflect that.

Build Your Portfolio

The first place to start is to decide what broad categories will make up your investment portfolio. Stocks versus bonds like as shown above. Within that, you can diversify among things like large and small-cap funds, domestic and international companies.

You can add additional asset classes to your portfolio besides stocks and bonds. There are also cash and cash equivalents and real estate which can include

If you need help getting started, below are several investment strategies we’ve covered designed by industry finance leaders you can steal:

- The Ivy Portfolio

- Coffeehouse Portfolio

- Golden Butterfly

- Swensen Portfolio

- Larry Portfolio

- Permanent Portfolio

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

For example, billionaire hedge fund investor Ray Dalio designed the above mentioned All Weather portfolio to perform well regardless of the current economy.

Great! Where’s the Investment Store?

You can’t walk into the investment store and fill up a basket with investments. You have to open investment accounts with investment companies.

401k: Some employers offer a 401k, so all you have to do is choose between the funds your employer offers and fill out some forms.

IRA: We often recommend

ETF:

Lifecycle Fund: A lifecycle fund is the ultimate in set it and forgets it investing. In just a single fund, you get a fully diversified portfolio with the allocation based on the year you plan to retire.

It starts heavily weighted towards stocks and shifts to be weighted towards bonds the nearer you get to retirement. We love Vanguard’s Target Retirement 2050 Fund.

REIT’s: Fundrise is a crowdfunded platform that allows average investors access to real estate returns they could not access on their own or through a traditional REIT.

Their bread and butter are real estate deals that are typically overlooked by large institutional investors and out of reach for most individuals.

Rental Property: Not everyone wants to be a hands-on landlord, but

This approach lets you earn passive income without the hassle of being a traditional landlord.

If you’d like to learn more about Andrew’s criteria for finding a great property, the things he thinks about when scouting a neighborhood (and why those decisions matter), visit his course Rental Properties for Passive Investors.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

Leave it Alone (Mostly)

Investing might sound like a lot of work, but most of the work is front-loaded. Learning about and choosing different types of investments, deciding on asset allocation, and keeping track of it all.

For the most part, once you have everything set up, you can just let your money do its thing. The more you pull it in and out, try this, try that, the more work and probably less money you are going to make for yourself.

Investing is not your full-time job, and it shouldn’t become your hobby either. There are more fun and exciting things in life than watching CNBC.

An easy way to check in on your investments, which you need to do at most, once a month, is Personal Capital. It gives you a 1000 foot overview of all of your money.

You’re Afraid of the Wrong Thing

Too many people let the fear of investing hold them back, but your more significant worry should be what would happen if you never start investing.

Not everyone is going to make a fortune from their job, and even fewer people are going to win the lottery.

Time is ticking, and every day that you put it off, you are leaving money on the table. The best time to start investing was when you were 18; the second best time is right now. Get over your fear and start investing today with a few simple steps.

Show Notes

An Mas Chili Jesus: 12% ABV, what else do you need to know?

Krane Financial Solutions: Justin’s fee only investing firm.

JKrane.com: Justin teaches business owners how to be smart with their money so they can fund personal goals.

Investable: Research and evaluate rental properties.