No one can predict the future but based on past events; a market correction is coming. You need to start preparing for a market correction with an opportunity fund.

No one can predict the market but we can try to understand the present and try to make the best decisions for the future.

What is a Market Correction?

A correction is a decline in the stock market of at least 10% from its 52 week high that stops an upward trend. Is a correction a crash? No, a crash is a loss of 10% in a single day. A correction happens over a longer span of time.

While no one can predict a correction, we can look to past events to anticipate when the next one might be coming.

According to market analytics firm Yardeni Research, there have been 36 corrections in the S&P 500 since 1950 of at least 10%, or about one every two years.

What Causes a Correction?

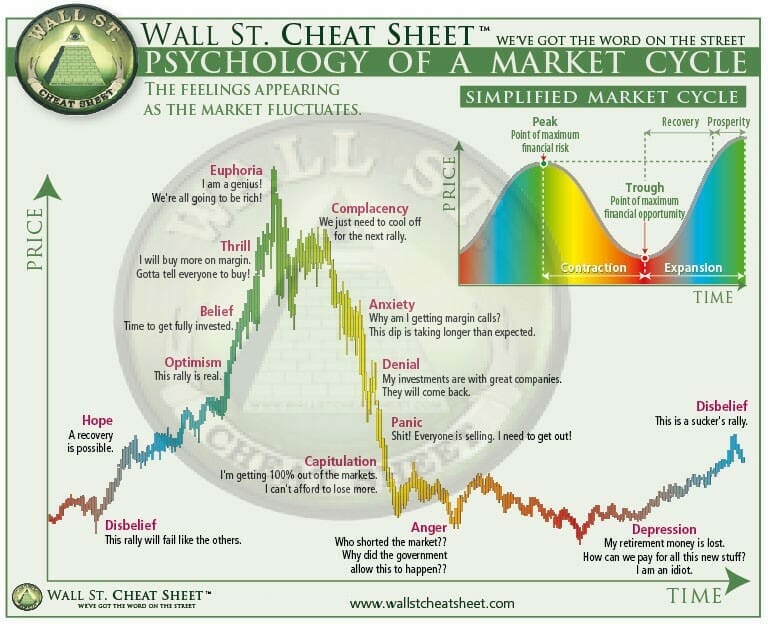

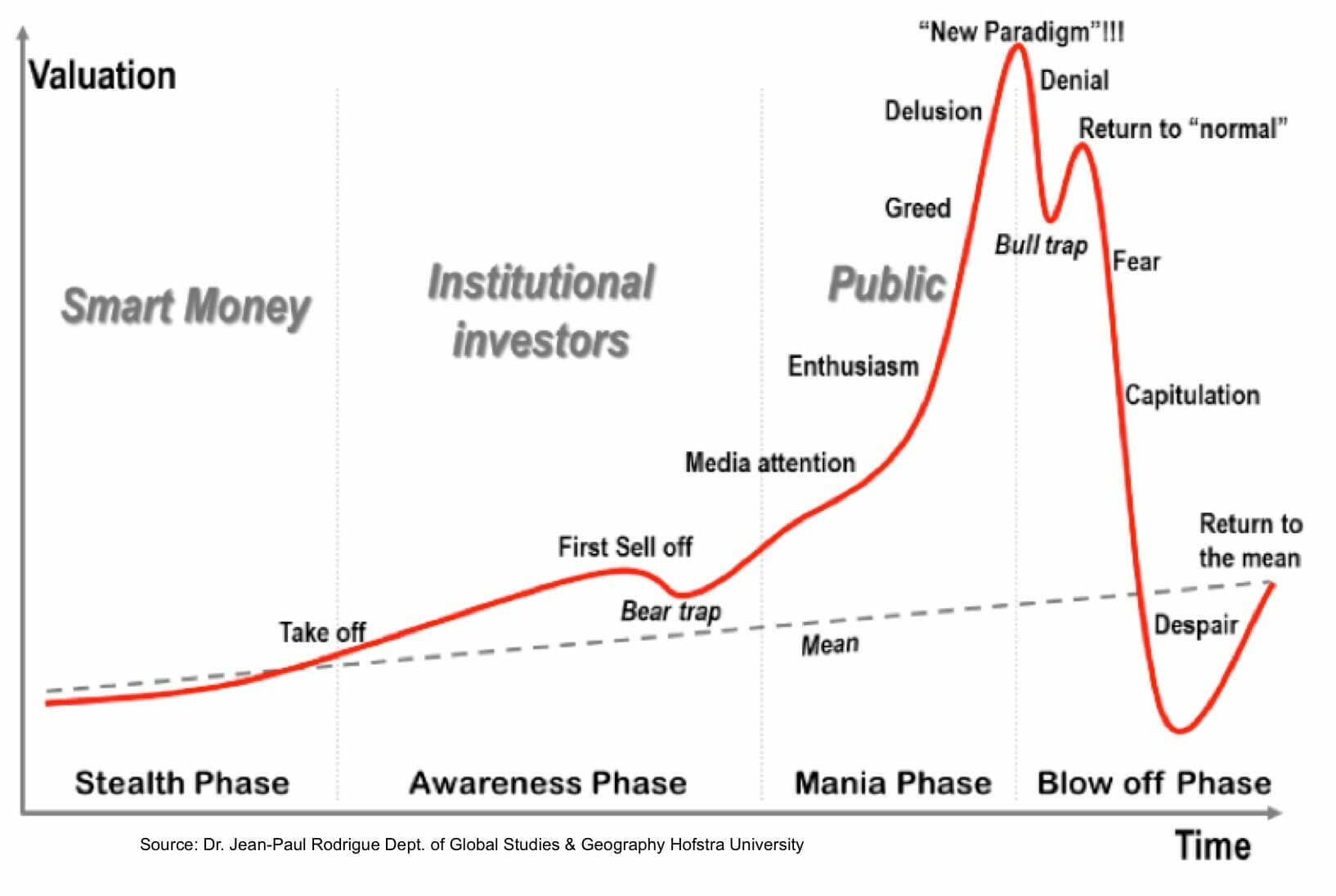

You’ve heard the term “irrational exuberance” when it comes to the stock market.

It means that investor’s enthusiasm is driving up stock prices to levels that aren’t supported by fundamentals. The market goes up, and everyone jumps on the bandwagon hoping to get in on the profits.

When the prices return to where they should be, a correction has occurred.

It’s Coming

We are in the second longest boom cycle in the history of the US. In exactly 12 months we will be tied for the longest with that boom cycle ending in the dot-com bubble in 2000. The low, slow burn of this recovery prevented things from overheating, and we avoided the fast boom-bust cycles that the economy has experienced in the past.

But many economists are predicting a correction and it could much more than 10%, some think it might be as high as 30%. What do they see in the tea leaves that indicate this? A few factors including increasing credit loans, an increase in the U.S. fiscal deficit, doubts about touted infrastructure spending plans and what is shaping up to be a nasty trade war.

When Will It Happen?

There are some other signs pointing to an upcoming correction.

Shiller PE Ratio

Yale Professor Robert Shiller invented this ratio to measure the market’s valuation. Some believe it to be a more reliable indicator than the standard P/E ratio because it eliminates fluctuation of the ratio that is caused by the variation of profit margins during short-term debt cycles.

The Shiller P/E ratio is calculated using the annual earnings of the S&P companies for the past ten years. Past earnings are adjusted for inflation using CPI. Past earnings are adjusted to the current dollar. Average the adjusted values for E10. The Shiller P/E equals the ratio of the price of the S&P 500 index over E10.

The standard P/E uses the ratio of the S&P 500 index over the trailing 12-month earnings of the S&P 500 companies. In an up economy, the companies have high-profit margins and earnings. That makes the P/E ratio artificially low because of higher earnings. In a recession, profit margins and earnings are low. That makes the P/E ration higher.

How can we use this to make better investing decisions? The information can help us devise investment strategies at different market valuations. In an overvalued market (rational exuberance) as we have now, it’s best to sit back and wait. When the correction comes, you can buy while the prices are low.

What Ray Dalio Thinks

Ray Dalio is the founder of Bridgewater Associates, the biggest hedge fund in the world. No one can predict the future, but if there is such a thing as an economic Nostradamus, Ray Dalio is it.

One of the factors Dalio uses when attempting to make predictions is debt cycle. Understanding the cycles can help us better understand the present and to see what is likely coming down the road.

Conventional economics focuses on cash, but credit is what makes up the vast majority of transactions across the world. Cash and credit work differently. If you pay cash for a good or service, the transaction is complete. If you use credit to make a purchase, the transaction is not complete until the borrower pays the debt.

This form of money created out of thin air via buying on credit compounds over time and creates cycles and these credit cycles impact and drive the economy.

Short-Term Debt Cycle

A short-term debt cycle, also called the business cycle generally happens every 5-7 years. The Federal Reserve Banks causes these cycles when they increase and lower interest rates. When rates go down, people and businesses borrow more money.

Debt a person or business already has gets cheaper. The rate at which assets are valued is lowered, and investors start jumping on the bandwagon with irrational exuberance as we described earlier.

Long-Term Debt Cycle

Long-term debt cycle happens much less frequently, hence the name, every 50-75 years. There are limits to how much spending (economic growth) can be financed because eventually, the money comes due. This is the long-term debt cycle. When we reach this limit, growth declines.

Dalio believes we are nearing the end of both the short term and long term cycles in the next 18-24 months. Knowing or at least suspecting that these things are coming allows us to position ourselves not only to cushion ourselves from the impact but to take advantage of the situation as well.

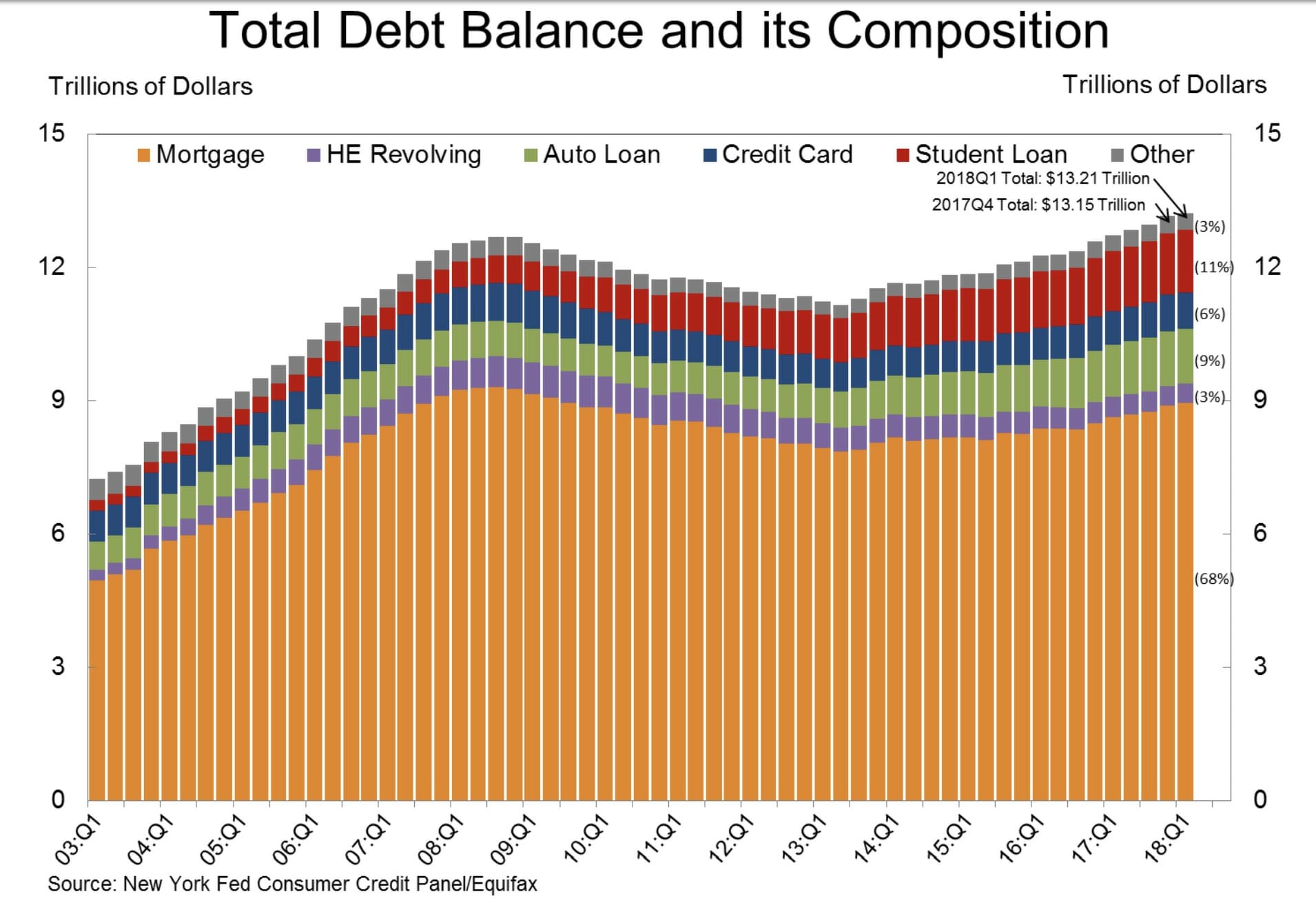

A Whole Lot of Debt

How much debt is floating around out there? Consumer debt is at a record high. The last time our debt level was nearly this high was in 2008 in the midst of the recession.

When the economy is nearing a correction as some economists think it is now, everyone starts looking for the next bubble about to pop, and this amount of debt could be it.

Or China

China’s bubble could be the next one to pop. The Chinese economy continues to grow but if that growth can’t happen fast enough to pay off its huge investments that have been fueled by enormous amounts of government credit, POP!

The country is building a huge amount of infrastructure, cities, malls, and roads. The Washington Post reported in 2015 that China used more cement between 2011-2013 than the U.S. used in the whole of the 20th century.

But as the population continues to age, there are no people in many of those cities and malls or on those roads. As this continues, the growth is slowing dramatically, but many businesses already carrying a tremendous amount of debt continue to borrow from lenders with no incentive to stop loaning.

The looming financial crisis in China will affect the U.S. and world economies.

Fiscal flexibility that’s funny, free and delivered weekly.

What’s Our Mantra?

If you’ve followed LMM even for a short time, you have heard us talk about using a buy and hold strategy when it comes to investing, and you know we don’t try to predict the future. But you can’t ignore the signs that are popping up and the wisdom of people like Ray Dalio.

You know the theory that it’s better to have “the talk” with your kids, so they don’t learn about sex from “the streets”?

That’s why we wanted to do this episode.

Not to scare you but to make sure you have the correct information. Because when all of this starts to heat up to a point where people way dumber than Ray Dalio are starting to take notice you are going to hear and read a lot of scary rhetoric.

While we don’t predict the market, we have our opinions on what may happen, but we’re careful not to drastically change our approach to investing based on suspicions or opinions.

The second word of our mantra is “hold,” and that’s what we want you to do no matter how many people tell you the sky is falling. Don’t panic and pull your money out of the market.

And Buy

The first part of our mantra is “buy,” and when the correction comes, you can do that because as people start to panic, they will be selling off their stocks at fire-sale prices. And what has our other idol, Warren Buffet told us?

Be fearful when others are greedy and greedy when others are fearful.

Tweet ThisIn fact, you should set aside money just for the purpose of buying up stocks at these coming bargain basement prices.

Opportunity Fund

An opportunity fund is money set aside so that when an opportunity arises, you have the money to take advantage of it. As an investor, your most important job is to get a good deal. Most of the growth you get in the market is during a recovery phase.

In the case of a market correction, you can use your opportunity fund to buy stocks or rental properties at great prices, investor’s job done!

Continue doing what you’re doing but consider diverting some money from your current investing strategy to an opportunity fund. If you’re investing $1,000 per month, invest $700 and put $300 in your opportunity fund.

Like all money that you plan to use in the short term, it should be kept in a safe, easily accessible place. RIght now online bank CIT is offering a 1.55% interest rate on their Premium High Yield Savings Account. That rate isn’t outstanding, but it is a lot better than you will get with most banks.

Play Your Game

What should you do with this information? Nothing really. Continue to do what you’re already doing. Keep investing, keep your emergency and sinking funds topped up. Consider starting an opportunity fund so when a correction comes you can hit the gas and scoop up bargains.

Remember, no one can predict the market, and we aren’t encouraging you to try. We just want to make sure that you are prepared for events like a market correction when they do inevitably come. Nothing lasts forever.

Show Notes

Transmitter Saison Ale: An earthy, dry beer with hints of pepper and fruit.

Tool Box: All the best stuff to manage your money.

Thank you to our sponsors: HiCharlie, Legal Shield, Gabi, and Leesa