Investing is not as complicated as Wall Street would have you believe. Anyone reading this can become a successful investor. Part of successful investing is creating a portfolio that’s right for you, your age, time horizon, and financial goals. It’s also where investing gets complicated. Building it from scratch takes a lot of research, time, and effort. But you don’t have to create one out of thin air. You can use the coffeehouse portfolio.

Some investors want a hands-off approach. For example, investing through a low-cost ETF with Betterment. You only answer a few questions, and they invest your money into a pre-existing portfolio without requiring any input from you.

And then there are those investors, a minority, who love everything about the stock market. They want to get their hands dirty, do all the research, read all of the reports, and create their portfolio from scratch.

Then you have those investors somewhere in between. They want a lazy portfolio they don’t have to create themselves but don’t want a generic portfolio designed for a vast swath of people.

This perfectly describes the coffeehouse investor. He or she is not looking for a bespoke portfolio but doesn’t want a one-size-fits-all either.

If this describes you, keep reading!

What Is the Coffeehouse Portfolio?

The Coffeehouse Portfolio takes its name from the idea that it’s such a straightforward investing strategy you could create while sitting in a coffeehouse.

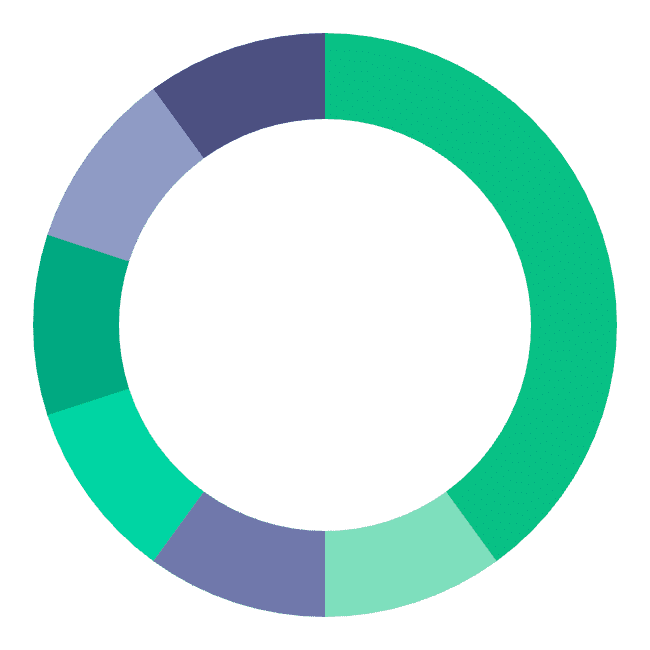

The portfolio contains seven assets, 40% is U.S. stocks, 20% is REITs and international stocks, and 40% is bonds.

Bill Schultheis

The creator of the coffeehouse portfolio is financial adviser Bill Schultheis. He introduced it in his book, The Coffeehouse Investor: How to Build Wealth, Ignore Wall Street, and Get On with Your Life.

Schultheis was an insider having been a broker with Smith Barney, but his book advised people to disregard Wall Street’s advice.

Don’t look for sexy, new investments, and try to beat the market. It’s something professional investors rarely accomplish.

So what hope do the rest of us have? Hardly any chance at all, as Schultheis explains in his book.

Only 14% of all managed mutual funds beat the stock market average in each of the last three, ten, and fifteen-year periods.

The Coffeehouse Portfolio is hands-off investing; you make no changes to it apart from rebalancing once a year so the original asset allocation remains intact.

According to Bill Schultheis, there are three fundamental principles to successful investing:

- Asset Allocation: Having the right mix of securities in your portfolio.

- Approximating the Stock Market Average: Not attempting to beat the market.

- Saving: Choosing and maintaining a savings rate that matches your financial goals.

Components and Asset Allocation

Seven funds with a 60/40 stock-to-bond allocation make up the Coffeehouse Portfolio.

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 10% | U.S. Large Cap Equities | Stock |

| 10% | U.S. Large Cap Value | Stock |

| 10% | U.S. Small-Cap | Stock |

| 10% | U.S. Small-Cap Value | Stock |

| 10% | International Equities | Stock |

| 10% | REITs | Real Estate |

| 40% | U.S. Total Bond Fund | Bond |

The 60% stock portion splits evenly among six funds, and the bonds (or fixed income) are in a total bond fund.

This portfolio takes its name from the idea that it’s such a straightforward investing strategy you could create it while sitting in a coffeehouse. It focuses on diversification and keeping things simple - it's also exceptionally conservative.

Investment Strategy

Well, it’s not the sexiest portfolio you could imagine, is it? But there is a method to the complete lack of madness.

What is drilled into our heads over and over as investors? Diversify, diversify, diversify. The Coffeehouse Portfolio certainly does that.

Each of the six funds that make up 60% of the portfolio covers a different part of the overall market, and the 40% invested in a total bond fund tracks the entire bond market.

What’s something else we’re told as average investors? KISS: keep it simple stupid. You don’t need to overcomplicate investing; you don’t need a dozen different funds, just a handful that are low-cost and perform well in bull markets and bear markets.

And what is something that LMM has always told you about investing and wealth-building?

Set it and forget it.

A lazy portfolio like the Coffeehouse Portfolio follows this advice. All you have to do is build the portfolio using inexpensive index funds and call it a day.

You’re not continually trading, trying to time the market, researching individual stocks, you’re not doing any of the things that make investing overly complicated.

Investing should be dull.

Tweet ThisSet it and forget it. Go do something more interesting with your time!

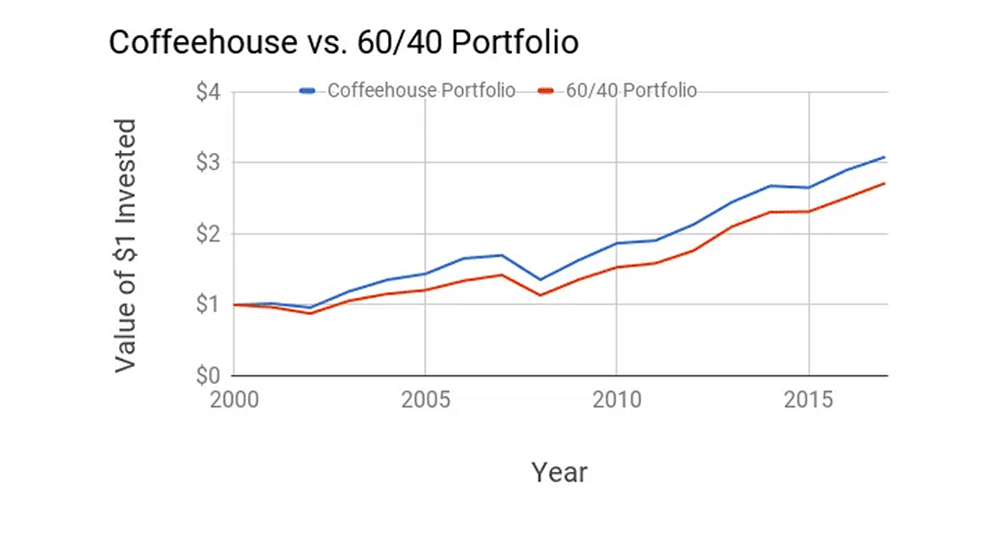

Portfolio Returns

So, is the proof in the pudding (or in the coffee in this case)? How does the Coffeehouse Portfolio perform? Pretty well!

From 2001-2016, the Coffeehouse Portfolio has returned 6.9%, while a 60/40 total stock/total bond portfolio has returned 5.9%

Again, not the sexiest numbers out there, but we’re not trying to be sexy; we’re trying to make and not lose money.

Coffeehouse Portfolio Risk Factors

The Coffeehouse Portfolio isn’t without risk, which is true of any investment.

Too Little International Exposure

With only 10% in international stocks, some investors may feel that’s not enough.

Much of the world’s economies are tied together now more than before, but how the United States economy performs doesn’t mean the rest of the world will follow.

And it’s not only your investment portfolio that’s largely domestic; your job and likely company are in the U.S.

If the U.S. economy falters, it could impact your job and impact your portfolio’s domestic stocks Having so little money overseas could unduly affect you.

Rebalancing

As we explained above, the only thing you need to do with the Coffeehouse Portfolio once you’ve set it up is to rebalance once a year.

Some platforms like

If automatic balancing isn’t offered, you’ll have to do it yourself. Either way, there is a cost involved. Having to rebalance too many funds gets expensive.

Too Conservative

When it comes to asset allocation, a general rule of thumb is to subtract the decade of your age (20s, 30s, 40s, etc.) from 100. Using that rule, your allocation between stocks and bonds would look like this:

- 100-20 = 80 stocks/20 bonds

- 100-30 = 70 stocks/30 bonds

- 100-40 = 60/stocks/40 bonds

Some financial experts feel that’s too conservative, and if you’re under 30 and sometimes even under 40, your allocation should be 90 to 100% in stocks because you have such a long time horizon to ride out the ups and downs of the stock market.

That looks like this:

| Age | Under 30 | 30s | 40s | 50s | 60s |

| Stocks | 100% | 90% | 80% | 70% | 60% |

| Bonds | 0% | 10% | 20% | 30% | 40% |

You can see according to the age-based asset allocation, the Coffeehouse Portfolio is exceptionally conservative. Young investors would have the same recommended allocation as a 60-year-old.

Fiscal flexibility that’s funny, free and delivered weekly.

Replicating the Coffeehouse Portfolio

If you’re looking to create a lazy portfolio, you can quickly and easily replicate the Coffeehouse Portfolio.

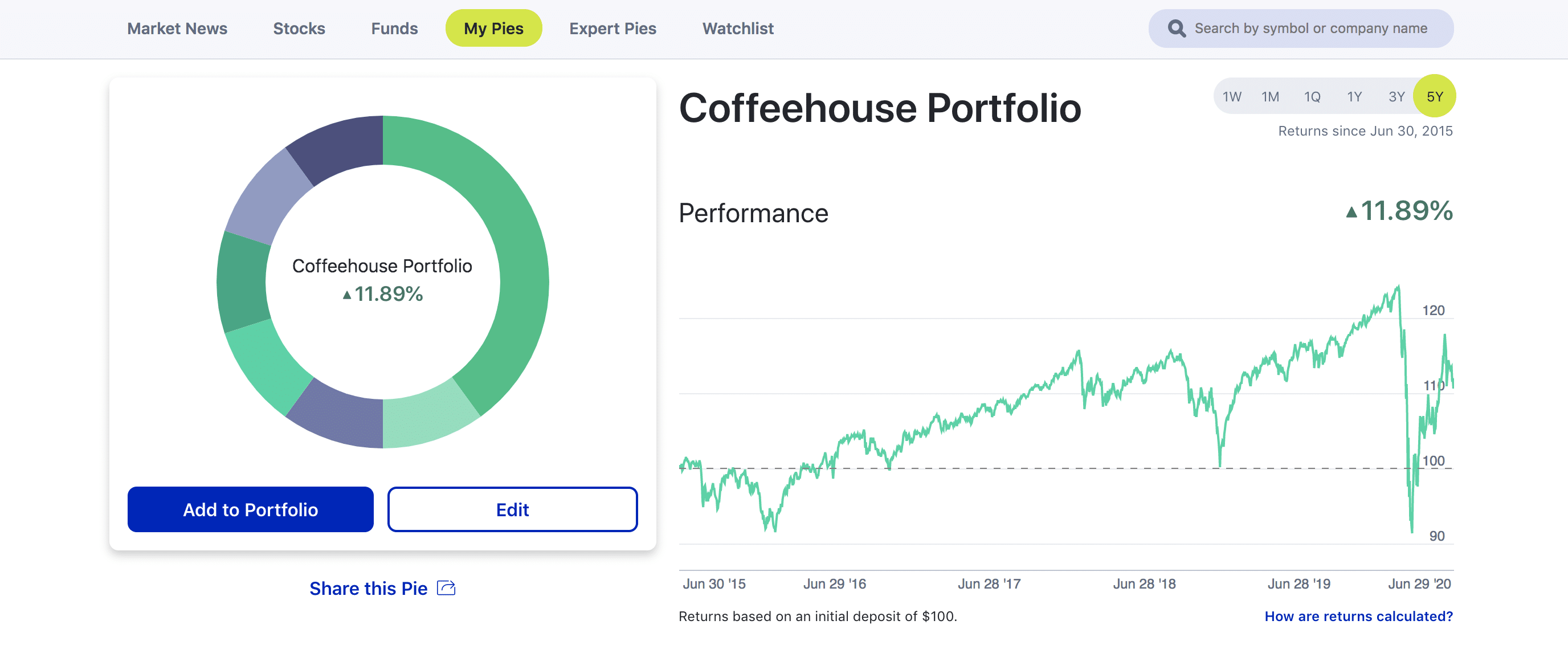

Automate it with M1 Finance

M1 Finance is the best of both investing worlds; it lets you automate investing while also allowing you to customize your portfolio.

That’s why it’s a great place to build yours. Below is an example of how you’d create the Coffeehouse Portfolio using M1 Finance.

Opening an account is easy. Enter your email and create a password. M1 Finance doesn’t charge for portfolio management, placing trades, or for deposits and withdrawals connected to your bank account.

If you’re building a portfolio from ETFs, you can incur management fees from the underlying funds, but the fees are low, ranging from 0.06% to 0.20%.

Once you’ve created your account, you’ll be taken to the “pie-building” page, where you can create your portfolio using ETFs, index funds, or individual stocks.

This model combines asset classes with Vanguard large-cap stocks, value stocks (small-cap value & large-cap value), real estate, and the total bond market.

This portfolio takes its name from the idea that it’s such a straightforward investing strategy you could create it while sitting in a coffeehouse. It focuses on diversification and keeping things simple - it's also exceptionally conservative.

Here’s an example of how you could build the Coffeehouse Portfolio using M1 Finance.

| Weighting | Fund | Asset Class |

|---|---|---|

| 10% | Vanguard Large-Cap Index Fund (VV) | Stock |

| 10% | Vanguard Value Index Fund (VTV) | Stock |

| 10% | Vanguard Small-Cap ETF (VB) | Stock |

| 10% | Vanguard Small-Cap Value Index Fund (VBR) | Stock |

| 10% | Vanguard Total International Stock Index Fund (VXUS) | Stock |

| 10% | Vanguard REIT Index Fund (VNQ) | Real Estate |

| 40% | Vanguard Total Bond Market (BND) | Bond |

Perk Up Your Portfolio Allocation

The Coffeehouse Portfolio has a lot of appeal because it makes sense. It’s easy to set up, and maintaining the asset allocation is simple.

You don’t have to think about it; you can set up automatic deposits and let your money do its thing, making you more money!

Apart from rebalancing once a year, maybe even once every two years, you don’t have to think about your lazy portfolio.

But in our opinion, the most significant benefit stems from passively managed money as it relates to behavioral finance.

Hands-off management regularly outperforms active management and is cheaper because you’re not paying someone to manage your portfolio. Management fees take a big chunk out of your money.

A lazy portfolio leaves investor behavior out of the equation. When it comes to our money, we don’t always act rationally.

Behavioral finance focuses on the fact investors are not always rational, have limits to their self-control, and are influenced by their biases.

That last sentence is why lazy portfolios are so attractive. It prevents us from making dumb decisions based on emotion because there are no decisions to make!

If you want to be a lazy, successful investor, Mr. Schultheis designed the Coffeehouse Portfolio with you in mind.