The stock market did exceptionally well in 2023-2024, but some people are hesitant to invest because they worry prices might be too high or the economy might slow down. While timing the market is virtually impossible, focusing on long-term goals and maintaining a diversified portfolio can help manage risk and maximize opportunities.

“It’s overwhelming”, you think to yourself. “I have no idea how to build an investment portfolio!”

What if I told you there’s no need to be scared? Investing doesn’t have to be complicated. Building a well-balanced portfolio can be simpler than you think.

Don’t be intimidated by the noise.

Understanding the basics is crucial. Think of it like driving a car: press the gas pedal to accelerate, use the brake to stop, and turn the wheel to steer. Mastering these fundamentals gives you control and confidence.

Here’s what you’ll learn:

- Key insights to understand before building an investment portfolio from scratch

- An overview of the three fundamental asset classes

- Strategies for achieving a balanced portfolio through effective diversification

- Practical portfolio models you can start applying today

Let’s dive in!

Building an Investment Portfolio or Fine-Tuning Your Existing One

Before diving into the deep end, it’s important to have a clear understanding of a few key factors:

- Your financial goals: What do you want to achieve with your investments?

- Your timeline: When will you need to access the money?

- Your risk tolerance: How much risk are you comfortable taking on?

The above three factors are what you should already know before getting started. They’re your road map. You can’t take a trip without a plan. If you don’t know where you’re going, you won’t get there.

Before creating your well-balanced portfolio, it’s crucial to know your financial goals. For example, is this money intended for a retirement account, a house, or an emergency fund? The purpose of the funds will guide your investment decisions and strategy.

When will you need the money?

- If it’s for retirement, you likely won’t need it for many years.

- However, if it’s for a short-term goal, such as a down payment on a home, you’ll need it much sooner.

- Understanding your timeline helps you set a clear target and choose the right investment approach.

What’s your risk tolerance?

- It’s one thing to consider your comfort with risk in theory, but experiencing a market drop firsthand is entirely different.

- Knowing your limits will help you create a portfolio you can stick with during market fluctuations.

- Can you handle market ups and downs without hitting the panic button? Some people pull their money out at the first sign of trouble and miss out when things bounce back.

Understand what type of investor you are. What’s your financial approach? Jumping in and out of the stock market is a risky game that rarely pays off. Staying consistent with your strategy is key.

Age Matters

Your age plays a big role in how you should invest. Here’s how to think about it:

- If you’re in your 20s or 30s: You have plenty of time to ride out market ups and downs, so you can take more risks by investing mostly in stocks. Stocks typically grow more over time.

- If you’re closer to retirement: You’ll want to play it safer by focusing more on bonds, which are less risky. This helps protect the money you’ve already saved.

- Try the 120-minus-age rule: Subtract your age from 120 to get a rough idea of how much of your portfolio should go into stocks. For example, if you’re 33, 87% (120 – 33) could be in stocks. It’s a simple guide, but you can adjust it to fit your comfort level.

- Think about how long you plan to work, too. If you’ll work for many more years, you can afford to take more risks. If retirement is just around the corner, focus on preserving what you’ve saved.

Just because you’re turning 65 doesn’t mean you have to retire.

Tweet ThisAdditional Factors to Consider for Investing and Saving

- Keep earning if you can: If you’re still earning a great living, there’s no need to withdraw from your investment portfolio. Let it grow while you focus on building your income.

- Kill your high-interest debt: High-interest debt is like an anchor holding you back. Pay it off as quickly as possible. Until it’s gone, it will keep dragging you under, making it hard to move forward financially.

- Take advantage of your employer’s 401(k) match: If your employer offers a retirement match, don’t leave free money on the table. It’s essentially a 100% return on your investment and an easy way to build wealth over time, even if you’re managing debt.

- Personalize your portfolio: There’s no single formula for a balanced portfolio. Everyone’s situation is unique, so your investment strategy should reflect your goals, timeline, and financial needs.

The Three Basic Investment Asset Classes

Fundamentals. They’re crucial for success in everything you do. Whether you’re building a home, learning jiu-jitsu, or whipping up a marinade for your steak, specific criteria must be met.

A well-balanced portfolio is no different. Whether it’s something you constructed yourself or your financial advisor built for you, you’ll most likely see these three asset classes:

- Equities (Stocks): Represent ownership in companies and offer potential for capital appreciation, making them a key component of growth-focused portfolios.

- Fixed-Income Securities (Bonds): Debt instruments that provide regular interest payments. They’re usually less risky and more stable than stocks, but things like rising interest rates or inflation can still affect their value.

- Cash and Cash Equivalents: Highly liquid assets that can be quickly converted into cash, providing stability and acting as a safety net for short-term needs.

There is usually very little correlation, and in some cases a negative correlation, between different asset classes. This characteristic is integral to the field of investing. – Investopedia

The success (or failure) of one investment type won’t necessarily affect another. For example, if all your money is in the stock market and it tanks, you could lose a lot.

Even worse, it could take years for your portfolio to recover. What if you’re near retirement and can’t afford to wait that long?

That’s why diversifying your portfolio with a mix of stocks, bonds, and cash is a fantastic idea—it’s a core part of most portfolios. Diversification helps balance risk and can protect your investments when one asset class underperforms.

You could even go further by adding real estate investments, futures, commodities, and other financial derivatives. However, these types of investments come with their own risks and complexities and might be more suited for experienced investors. But that’s a topic for another article.

Fiscal flexibility that’s funny, free and delivered weekly.

Ways to Have A Balanced Portfolio

There are numerous ways you can divide your asset classes.

Total Stock Market

For example, when dealing with stocks, you can keep it simple and buy a total stock market index fund.

Vanguard’s Total Stock Market Index Fund (VTSAX) currently consists of approximately 3,624 stocks (as of January 2025), offering broad diversification across various sectors, including technology, financials, consumer services, and healthcare.

The fund provides exposure to leading blue-chip companies such as Apple, Microsoft, Amazon, Berkshire Hathaway, NVIDIA, Alphabet, and Meta Platforms. These top holdings collectively make up about 31.4% of the fund’s total net assets, ensuring substantial representation of large-cap companies (as of January 2025).

Investment Styles

You can diversify your investments even more by spreading your money across different types of U.S. stocks. For example, you can invest in value stocks, which are typically more stable, and growth stocks, which have higher potential for big gains.

You can also mix large companies (large-cap stocks) with smaller, often less predictable companies (small-cap stocks). This strategy helps balance risks and rewards, as these types of stocks tend to perform differently depending on the market conditions.

Global Diversification

Global diversification is a smart way to strengthen your investment portfolio. By splitting your investments between U.S. and international markets, you can benefit from opportunities in foreign economies while reducing risk.

One popular example is the MSCI EAFE Index, which tracks stocks from developed countries like those in Europe, Australia, and Asia. Adding these to your portfolio spreads your risk across different markets.

You can also invest in emerging markets, like those in developing countries. These markets often offer higher growth potential, but they come with more risk, so it’s important to balance them carefully.

By diversifying across regions and types of investments, you create a more balanced portfolio that can handle ups and downs while still aiming for long-term growth.

Bonds

Bonds are another great way to stabilize your portfolio. Unlike stocks, bonds are less risky and can help cushion your investments during market downturns. They provide a steady income and help reduce overall volatility.

Bonds can be divided into three primary groups:

- Government Bonds: These are issued by the U.S. government, like Treasury bills and notes (Treasuries are also exempt from state and local taxes). They are very safe but usually offer lower returns.

- Corporate Bonds: Companies issue these to raise money. They usually pay more interest than government bonds but come with a bit more risk.

- Municipal Bonds (Munis): These are issued by state and local governments to fund public projects. The interest earned is often tax-free, which is great for people in higher tax brackets.

Each type of bond has different pros and cons. Government bonds are the safest but pay less. Corporate bonds pay more but are a little riskier. Munis can save you money on taxes, but their safety depends on the financial health of the issuer.

Think about your goals and how much risk you’re comfortable with when choosing which bonds to invest in.

Each carries different risks, rewards, and benefits.

The maturity date of a bond affects its risk and return. Short-term bonds offer lower returns but are less risky, while long-term bonds provide higher returns but are more sensitive to interest rate changes. Choosing a mix of both can help balance risk and reward.

Cash is king…

But not if you’re concerned with building wealth. Why?

Inflation!!!

Emergency Fund

It’s a good idea to have some on hand in case of emergencies. An emergency fund is a savings account set aside to cover unexpected expenses or financial emergencies, like medical bills or job loss, ensuring financial stability during tough times.

It’s a good idea to keep your emergency fund in places where it’s safe and easy to access:

- High-Yield Savings Accounts: These accounts offer higher interest rates (around 5.00% APY) compared to traditional savings accounts and are FDIC-insured.

- Money Market Accounts: Similar to savings accounts but may include check-writing options. They are low-risk and FDIC-insured.

- Certificates of Deposit (CDs): Short-term CDs offer fixed returns and are a safe option if you don’t need immediate access to your money.

- Treasury Bills (T-Bills): Short-term government securities that are safe and liquid, ideal for short-term savings.

Choose an option based on your need for quick access, safety, and interest earnings.

These are fantastic places to house your Emergency, Opportunity, and Sinking funds.

Individual Stocks

If you enjoy picking individual stocks, limit it to no more than 10% of your total portfolio. This reduces the risk of losing too much on a single “hunch,” like betting on marijuana stocks.

A great place to experiment with stock-picking is in tax-advantaged accounts like a Roth IRA. These accounts let you buy and sell stocks without worrying about immediate tax consequences.

Be mindful of trading fees or transaction costs your broker might charge, as these can add up. Remember, keep your stock picks fun and limited to 10% of your portfolio!

Replicate These Portfolio Models Yourself

Let’s take a look at a few portfolio models you can use today. I’ll start with the more straightforward examples before getting into the hairy weeds.

The below models can all be easily automated using M1 Finance.

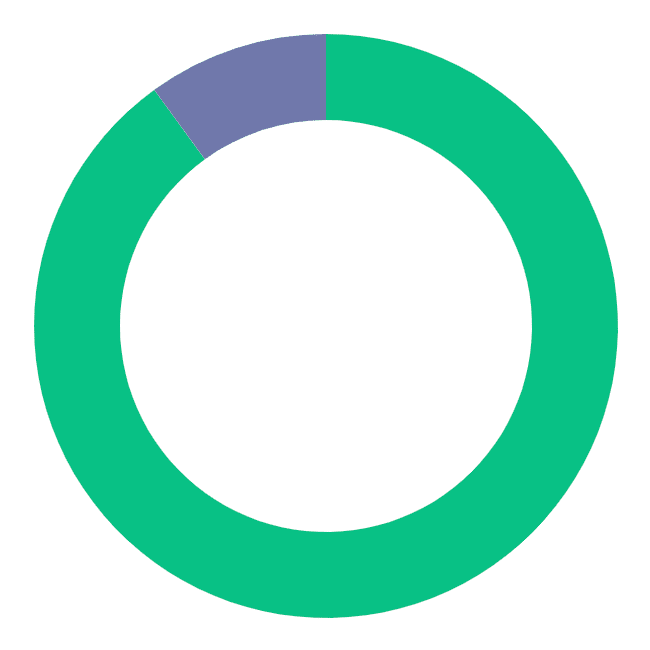

The Warren Buffett Model

This is the allocation he said he’d want for his wife after he passes. It’s a two-fund portfolio with a 90/10 stock-to-bond allocation.

Warren announced that after he passes, the trustee of his wife's inheritance has been told to put 90% of her money into a stock index fund and 10% into short-term government bonds.

The Warren Buffett allocation for his wife entails 90% in a low-cost, exchange-traded fund (ETF) of the S&P 500. A low-cost option could be the Vanguard S&P 500 ETF (ticker VOO).

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 90% | U.S. Large-Cap Equity | Stock |

| 10% | Short-Term Treasuries | Bond |

The remaining 10% goes into short-term government bonds. An inexpensive option could be iShares Short-Term Treasury Bonds (ticker SHV).

Read his biography, The Snowball: Warren Buffett and the Business of Life, to learn the guiding principles that turned him into one of the world’s greatest investors.

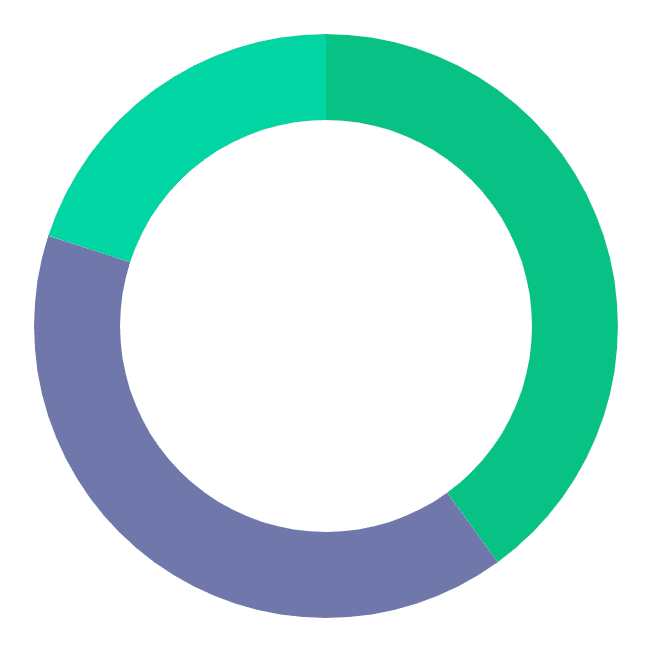

Rick Ferri Three-Fund Portfolio

Famed personal finance author and columnist, Rick Ferri, suggests this as his three-fund model:

| Weighting | Portfolio Components | Asset Class |

|---|---|---|

| 40% | Total U.S. Stock Market | Stock |

| 20% | Total International Stock Market | Stock |

| 40% | Total U.S. Bond Market | Bond |

For a detailed exploration of Mr. Ferri’s investing approach, read his books All About Asset Allocation and All About Index Funds.

Typically, three-fund portfolios hold a combination of U.S. stocks, international stocks, and U.S. bonds. Rick Ferri allocates 40% to U.S. stocks, 20% to international stocks, and 40% to U.S. bonds.

The above shows how your three-fund portfolio could look when using Vanguard funds.

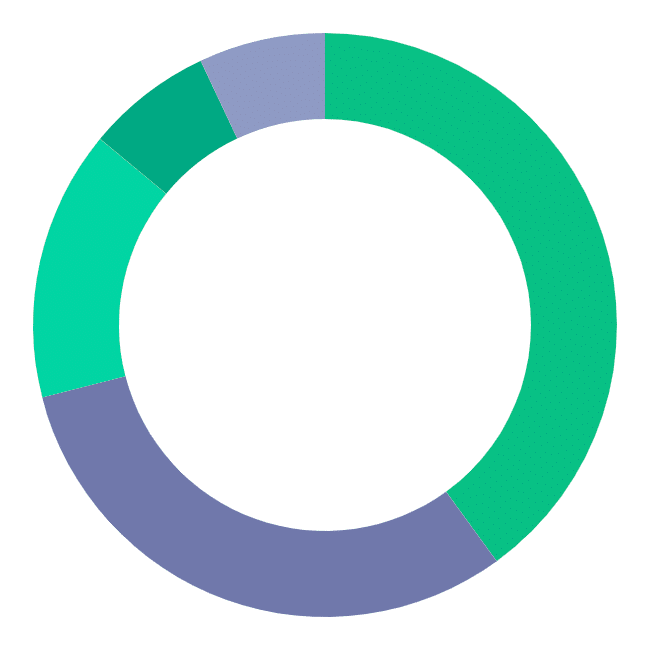

The All-Weather Portfolio

Ray Dalio is the Obi-Wan of the investing world. He’s up there with Warren Buffett. His book, Principles: Life and Work is a must-read and an LMM favorite.

He created this portfolio as one to withstand the ups and downs of the market – hence the name All-Weather.

This one adds a couple of asset classes into the mix that we didn’t talk about – gold and commodities.

| Weightings | Portfolio Components | Asset Class |

|---|---|---|

| 30% | Total U.S. Stock Market | Stock |

| 40% | Long-Term Treasuries | Bond |

| 15% | Intermediate-Term Treasuries | Bond |

| 7.5% | Gold | Commodity |

| 7.5% | Diversified Commodities | Commodity |

Here’s what the All Weather portfolio looks like.

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

A popular variation of the All-Weather portfolio is the Golden Butterfly.

Both portfolios hold five securities, but, the Golden Butterfly replaces the diversified commodities and intermediate treasuries with small-cap value stocks and short-term treasuries.

This portfolio is a socially responsible version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

The above is another variation that uses a Socially Responsible Investing tilt. Instead of using a total stock market fund, you’d replace with the Goldman Sachs JUST U.S. large-cap equity fund (or an SRI-equivalent).

If you’d like to see the original Golden Butterfly allocation, head here.

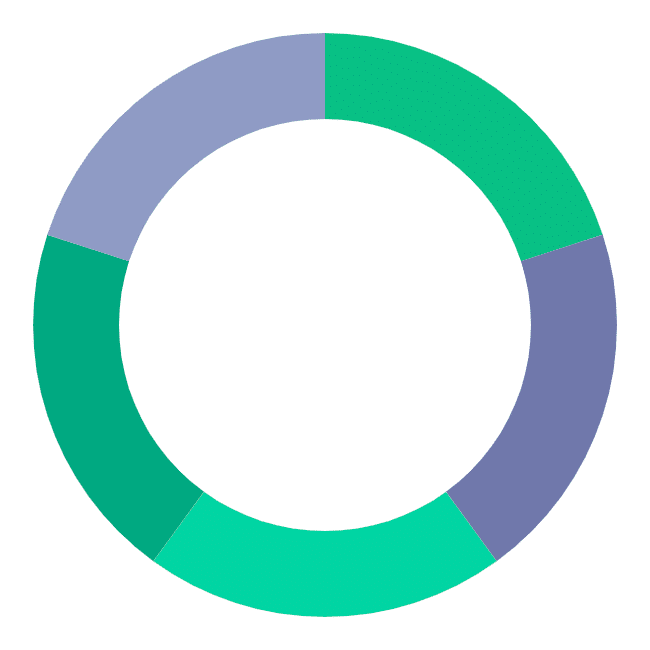

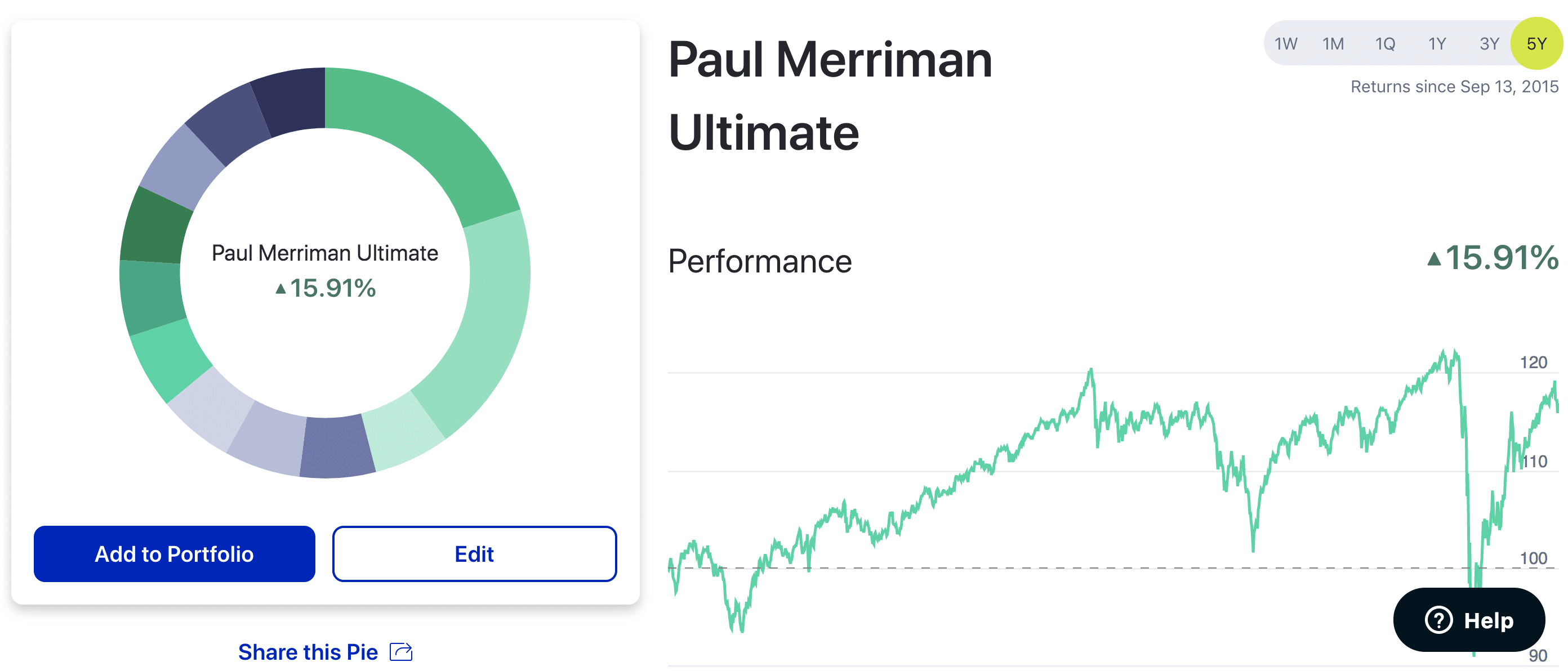

The Paul Merriman Ultimate Buy and Hold Strategy

This one shows how far you can diversify a traditional 60/40 portfolio of stocks and bonds if you’re willing to do the extra work.

The Merriman Ultimate is an enhanced version of a traditional 60/40 stock/bond portfolio. It's based on academic research and a proven track record of outperforming the S&P 500 Index, generating higher returns with less risk.

Mr. Merriman based this portfolio on the conclusion that long-term investment success depends on your choice of asset classes.

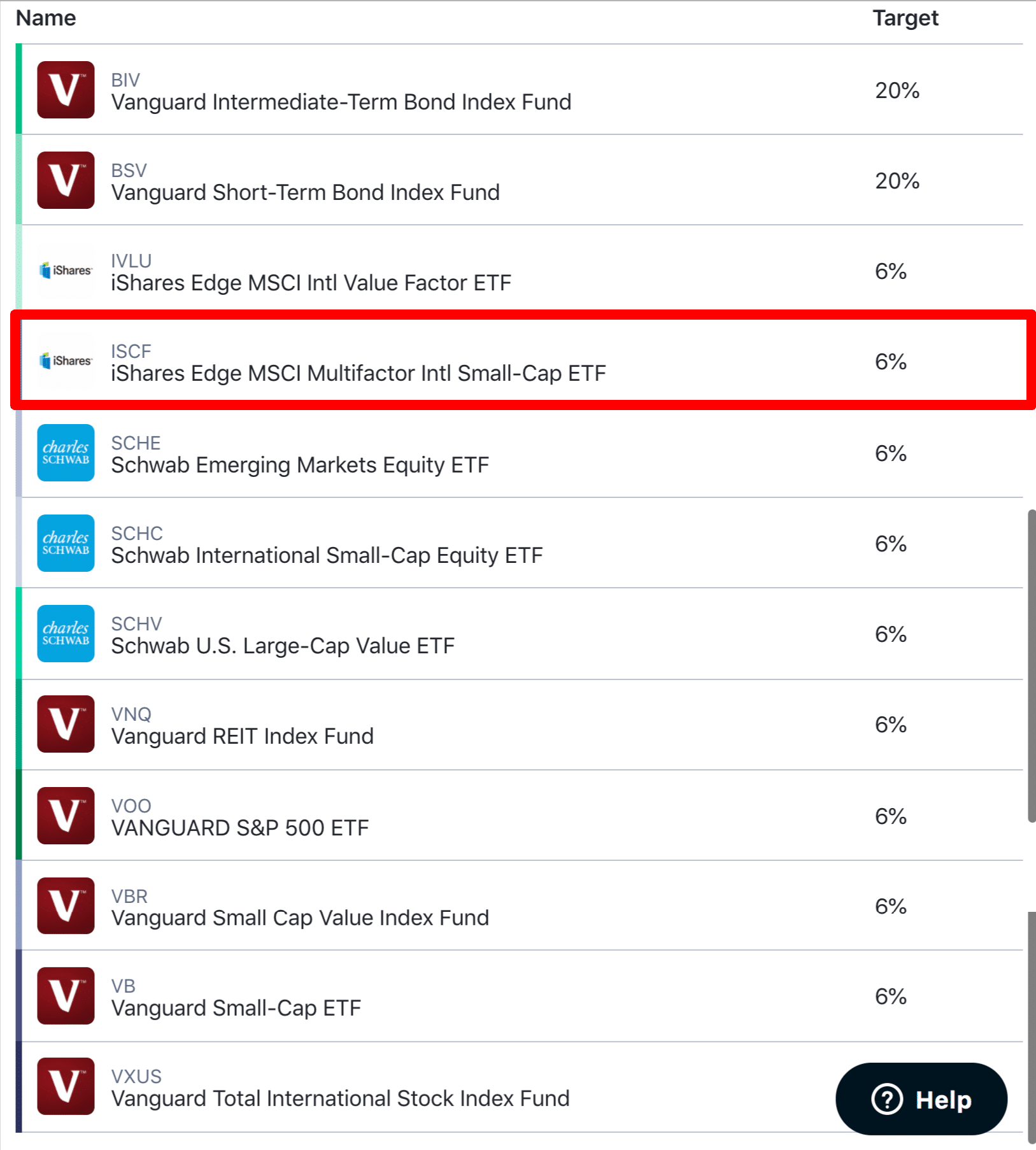

| Weightings | Portfolio Components | Asset Class |

|---|---|---|

| 6% | U.S. Large-Cap Blend | Stock |

| 6% | U.S. Large-Cap Value | Stock |

| 6% | U.S. Small-Cap Blend | Stock |

| 6% | U.S. Small-Cap Value | Stock |

| 6% | International Large-Cap Blend | Stock |

| 6% | International Large-Cap Value | Stock |

| 6% | International Small-Cap Blend | Stock |

| 6% | International Small-Cap Value | Stock |

| 6% | Emerging Markets | Stock |

| 6% | REITs | Real Estate |

| 20% | Short-Term Treasuries | Bond |

| 20% | Intermediate Treasuries | Bond |

The above allocation works best in tax-sheltered accounts (e.g., IRAs). If using a taxable account, it’s recommended removing the REITs and dividing that portion equally among the four U.S. stock asset classes.

But if you wanted to build this portfolio using M1 Finance, here’s one way to go about it.

I highlighted the iShares Multifactor International Small-Cap ETF in the above screenshot because this is a substitution.

I highlighted the iShares Multifactor International Small-Cap ETF in the above screenshot because this is a substitution.

Currently, international small-cap value funds aren’t available on M1’s site (at least none that I saw).

The two common funds I encountered for this asset class are DFA Intl Small Cap Value (DISVX) and Avantis Intl Small Cap Value (AVDV), however, neither exist on M1.

For some, this approach might be excessive; sometimes simpler is better.

If the above portfolio looks like too much work, try a target-date fund or a robo-advisor. They do all of the heavy lifting for you. Investing should be simple – let’s not complicate it.

Final Thoughts

There are many ways you can construct a well-balanced portfolio – international stocks, real estate, mutual funds, government bonds.

Simplicity is key. What’s important is having one with a few non-correlated asset classes and going from there.

Different investments carry different risk. Do your homework. High expense ratios (the cost to operate the fund) eat away your returns so look for low-cost ones. Your retirement date will determine how your investment portfolio is allocated. There is no one-size-fits-all approach.

The above examples serve as a blueprint for executing your investment strategy. Customize them to fit your personal finance goals.

Show Notes

Personal Capital: The investing version of Mint.

LMM Ultimate Investment Strategy: Andrew lays out a blueprint for you.