Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Investing isn’t as complex as it might seem. In fact, with the right guidance, it’s quite simple. We’ll teach you how to invest like a pro, even if you’re just starting out. Learn expert strategies and take control of your financial future, no expertise is needed!

Personal Finance 101

If you had to choose the three pillars of personal finance, they would probably be budgeting, saving, and investing. Budgeting and saving might not come naturally to everyone, but with a little practice, you can pick them up quickly. It’s investing that tends to throw most people off.

Investing is important, especially for retirement, but it can be confusing with all the terms—mutual funds, Roth IRA, ETFs, robo-advisors, index funds, and more. Understanding these basics will help you make smarter decisions for your future.

Investing can feel overwhelming with all the jargon, and it’s easy to see why some people give up before they even start. But you don’t need to be a financial expert to invest wisely. We’re not aiming to make investing a full-time hobby—we just want you to feel comfortable making smart decisions with your money.

This guide is for the casual investor. We’ll show you how to manage your money and make informed investment choices without needing to become an expert.

Get clarity, confidence, and peace of mind for your finances. Track all of your account balances, transactions, and investments in one place.

You’re Ready to Get Started

You have paid off your high-interest credit card debt by taking out a consolidation loan with Upgrade. You’ve paid off your student loans (or at least refinanced them to a lower interest rate) with Credible. Your emergency fund is fully stocked with six months to cover necessary expenses.

You’re ready to start investing and might be considering hiring a financial advisor to help you get started. Before making that decision, it’s worth knowing that with a basic understanding of investing, you can begin managing your money on your own. Learning the essentials will give you confidence in setting up your personal investment plan.

While financial advisors can provide valuable guidance, especially as your portfolio grows, many of the early steps in investing are things you can handle yourself. This guide will show you how to take a DIY approach to get started, with the option to seek professional advice later if needed.

Easy Mode

Investing 101 starts with choosing beginner-friendly platforms like Empower (formally Personal Capital), Fidelity, or M1 Finance, which offer tools and resources to help you build a diversified portfolio with minimal effort, whether you’re into automated investing or prefer more control over your choices.

These platforms make it easy to begin investing without needing advanced knowledge, allowing you to grow your money while learning along the way.

Empower

Empower, known for its exemplary suite of free financial tools, also offers a financial advisory service tailored for high-net-worth investors. It combines the automation of a

Empower offers three tiers of wealth management depending on your account balance. Empower requires a $100,000 minimum investment and starts with a 0.89% management fee.

You’ll gain access to a custom portfolio based on your financial goals, curated from six asset classes. Empower provides dynamic rebalancing and smart indexing as part of its tax-optimized strategy.

The U.S. equity portion of its portfolios is a diversified selection ranging between 80-120 individual stocks.

Sign up to use their free tools.

Best for: High net worth investors

Management fees: 0.49% – 0.89%

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

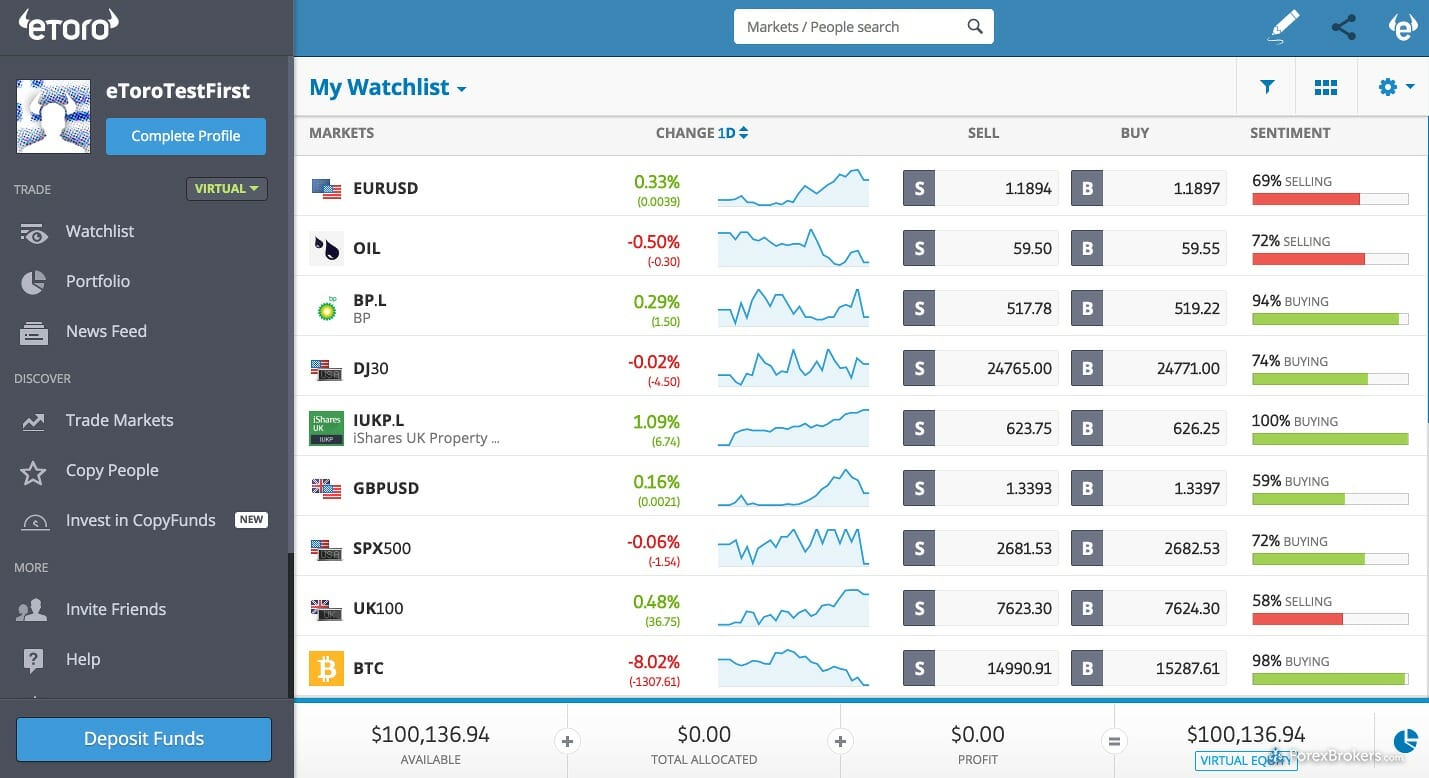

eToro – Track and Mirror The Investments Of Professionals

eToro is a hybrid investment platform that combines traditional investing with social trading. It offers a range of assets, including stocks, cryptocurrencies, ETFs, and commodities, allowing users to build diverse portfolios. To withdraw funds, you must sell specific equities, which provides control but requires careful planning. Note that eToro charges a $5 withdrawal fee, with a minimum withdrawal amount of $30. Withdrawal processing times may vary depending on the payment method used.

The platform’s main appeal is its social trading feature, particularly the CopyTrader tool. This enables users to learn from and replicate the strategies of experienced investors. By following seasoned traders, you can align your trades with theirs and potentially achieve similar results. However, gains and losses are shared, so evaluating a trader’s performance and risk profile is crucial before copying their strategies.

eToro’s transparency stands out. You can review top traders’ profiles, analyze their past decisions, and mirror their investments. This transparency allows you to make informed decisions about whose strategies to follow. When skilled investors succeed in buying low and selling high, you can share in the gains—but also the losses.

Overall, eToro offers a blend of control, transparency, and community. With its social trading tools and educational opportunities, it’s a valuable option for those ready to learn, grow, and navigate the risks of investing.

That said, diversity is critical.

eToro lets you mirror the strategies of experienced traders, helping you diversify your portfolio. For example, you could allocate portions of your investment to different traders, ensuring no single individual influences all your savings.

This mirroring feature offers the potential for learning while participating in the market. In the US, the platform currently supports copying crypto traders, with plans to expand to stocks and ETFs.

eToro requires a $100 minimum deposit, with a $200 minimum to start copying a specific trader. Fees vary by investment type, so review eToro’s current fee schedule for details.

With tools for collaboration and portfolio management, eToro connects users to a community of experienced traders, providing an interactive approach to investing.

Fiscal flexibility that’s funny, free and delivered weekly.

Intermediate Mode

Once you have your

While retirement investing isn’t exactly difficult, you will need to know a little more than you did to invest with

Retirement accounts require a little more research and understanding because they have rules and advantages very different from other types of investments. Retirement accounts have tax advantages and regulations about when you can withdraw money from them.

Regular saving and investing aren’t enough. Investing in retirement accounts is a critical part of your personal finance plan.

Unforeseen illnesses, the financial needs of your dependents, and the uncertainty of Social Security and pension systems are but a few of the factors at play. A secure nest egg will do wonders to help you cope with the challenges of your life’s later years. The challenges of your younger years is finding a way to set that up.

A 401k

A 401k is an employer-sponsored retirement savings vehicle that allows you to invest part of your paycheck, pre-tax, where it grows tax-free until you are ready to start withdrawing from it after age 59 1/2.

Most plans are made up of mutual funds that include stocks, bonds, and money market investments.

The money is taken directly from your check, so it’s a built-in way to save consistently which is a significant component of successful investing. A 401k also lowers your taxable income. If you earn $5,000 a month and invest $1,000 into your account, you are only taxed on the remaining $4,000.

What’s even better than an employer who offers a 401k is one who gives 401k matching. If you invest 6% of your income, for example, the company will match 3%. Always invest at least enough to get the match.

For 2024, there is a limit to how much you can invest in your 401(k):

- Maximum employee contribution: $23,000

- Catch-up contribution for those 50 and older: Additional $7,500

- Total maximum contribution (employee and employer combined): $69,000

The combined employer and employee contribution limit allows for significant retirement savings. If you’re 50 or older, your total potential contribution can reach $76,500.

When choosing between 410k investment options, be sure to know what fees and how much you’ll be charged. Investing fees can eat up a significant portion of your long-term investments over time.

Read the fee disclosure statements for each plan your employer offers and choose the fund providing the lowest fees. If all of the choices have high fees, you may want only to contribute enough to get the match from your employer and put the extra money in an IRA.

The average employer match is around 4.7% of salary, but this can vary widely between companies.

Personal Capital’s Fee Analyzer can show you how much you’re paying in fees.

If you withdraw from your retirement savings before turning 59½ years old, you will generally be taxed on the money and may face a 10% penalty. However, as of 2024, there are some new exceptions and rules to be aware of:

- Emergency withdrawals: You can now withdraw up to $1,000 per year from your eligible retirement accounts (like 401(k)s, IRAs, or 403(b)s) for unforeseeable or immediate financial needs without incurring the 10% penalty. You’ll still owe income tax on the withdrawal.

- Domestic abuse victims: If you’re under 59½ and have been a victim of domestic abuse, you can withdraw up to $10,000 (or 50% of your vested account balance, whichever is less) without the 10% penalty.

- Exceptions still apply: The pre-existing exceptions to the 10% penalty, such as certain medical expenses, disability, or first-time home purchases, remain in effect.

- Roth IRA contributions: You can still withdraw your Roth IRA contributions (but not earnings) at any time without penalty.

- Rule of 55: If you leave your job in or after the year you turn 55, you can withdraw from that employer’s 401(k) without the 10% penalty.

Remember, while these options provide more flexibility, it’s generally advisable to avoid early withdrawals from retirement accounts if possible, as they can significantly impact your long-term savings.

IRAs

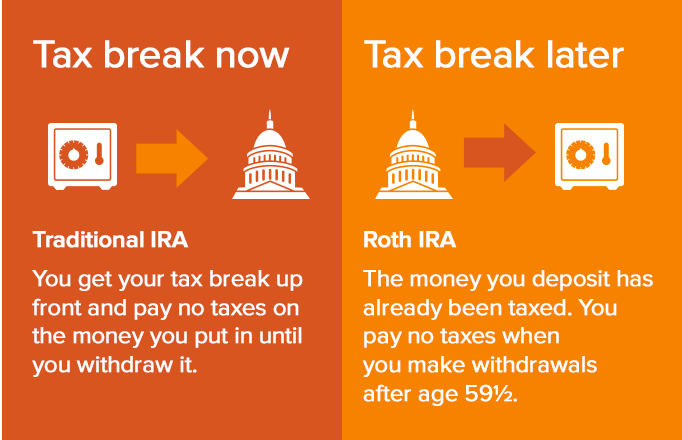

There are two main types of Individual Retirement Accounts (IRAs): Traditional and Roth. Both are tax-advantaged retirement accounts, but they differ in how and when taxes are applied.

Traditional IRA:

- Contributions may be tax-deductible, depending on your income and whether you’re covered by an employer-sponsored retirement plan.

- The money grows tax-deferred.

- Upon withdrawal after age 59½, the money is taxed as ordinary income.

- Required Minimum Distributions (RMDs) must begin at age 73 (as of 2024, increasing to age 75 in 2033).

Roth IRA:

- Contributions are made with after-tax dollars (no upfront tax deduction).

- The money grows tax-free.

- Qualified withdrawals after age 59½ (and if the account has been open for at least five years) are tax-free.

- There are no Required Minimum Distributions during the owner’s lifetime.

For both types:

- As of 2024, the annual contribution limit is $7,000 for individuals under 50, and $8,000 for those 50 and older (including a $1,000 catch-up contribution).

- Early withdrawals (before 59½) may be subject to a 10% penalty, with some exceptions.

- Contribution eligibility and deductibility are subject to income limits, which are adjusted annually.

It’s important to note that the choice between Traditional and Roth IRAs depends on individual circumstances, including current and expected future tax rates, retirement plans, and overall financial strategy.

For 2024, you can contribute up to $7,000 to an IRA, and if you’re 50 or older, you can add an extra $1,000, bringing your total to $8,000. If you put money into a Traditional IRA, it might help lower your taxable income for that year, depending on your situation.

When you take money out of a Traditional IRA, it’s taxed as regular income. If you’re under 59½ when you withdraw, you could face a 10% early withdrawal penalty unless you qualify for certain exceptions.

On the other hand, a Roth IRA is funded with after-tax dollars. This means you pay taxes on the money before you put it in. The good news? When you take money out after age 59½ (and the account has been open for at least five years), those withdrawals are tax-free!

You can also take out your Roth contributions anytime without penalties or taxes. Plus, after five years, you can withdraw up to $10,000 of your earnings tax-free for things like buying your first home.

So, which one is better?

It depends on your situation. If you think you’ll be in a lower tax bracket when you retire, a Traditional IRA might be the way to go since it gives you a tax break now. But if you expect your tax rate to go up in the future or want to leave some tax-free money to your heirs, a Roth IRA could be a smarter choice.

Also, if you’re thinking about rolling over a Traditional IRA into a Roth later on—like during retirement when your income is lower—that can be a good strategy too. Just keep in mind that any amount you convert will count as taxable income for that year.

It’s always a good idea to chat with a financial advisor or tax pro to figure out what works best for you!

We have a whole article that will explain this strategy in greater detail.

When it comes to Individual Retirement Accounts (IRAs), there are fees you need to keep an eye on. Understanding these fees can help you make smarter choices about your retirement savings.

Understanding IRA Fees

When it comes to Individual Retirement Accounts (IRAs), there are fees you need to keep an eye on. Understanding these fees can help you make smarter choices about your retirement savings.

Common IRA Fees

- Account Maintenance Fees: Some providers charge an annual fee to keep your account open. This can range from $0 to over $100.

- Transaction Fees: If you buy or sell investments in your IRA, you might pay a fee for each trade. This can be anywhere from $0 to $50 or more, depending on your broker.

- Management Fees: If your IRA includes mutual funds or ETFs, you’ll pay management fees, often called expense ratios. These fees can be low for index funds but higher for actively managed funds.

- Advisor Fees: If you have a financial advisor managing your IRA, they may charge a fee based on a flat rate, hourly rate, or a percentage of your assets.

Tips to Keep Fees Low

- Shop Around: Compare different IRA providers to find the best fee structures.

- Choose Low-Cost Investments: Look for index funds or ETFs with low expense ratios.

- Limit Trading: Frequent buying and selling can rack up transaction fees.

- Check for Fee-Free Options: Some providers offer IRAs with no fees for certain balances.

By staying aware of these fees and managing them wisely, you can keep more of your money working for you in retirement. Always review your statements and ask your provider about any fees you’re unsure about. Being proactive can make a big difference in your retirement savings!

Advanced Mode

At LMM, we are passionate about passive income. It’s the ultimate way to let your money work for you while you relax! One of the best strategies for generating passive income is investing in real estate. And don’t worry—you don’t need to be a seasoned expert to get started in real estate investing. We’ll show you how to make it simple and accessible for anyone.

Real estate investing, even on a small scale, remains a tried and true means of building an individual's cash flow and wealth.

Tweet ThisWe’ve got two great ways for you to jump into real estate investing, even if you don’t have any special knowledge. These options might need a bit more homework compared to some other investments we’ve talked about, but with just a little extra effort, you can start building your real estate portfolio and bring in steady passive income.

Real estate investing is an awesome way to reach financial freedom, and we’re here to guide you every step of the way.

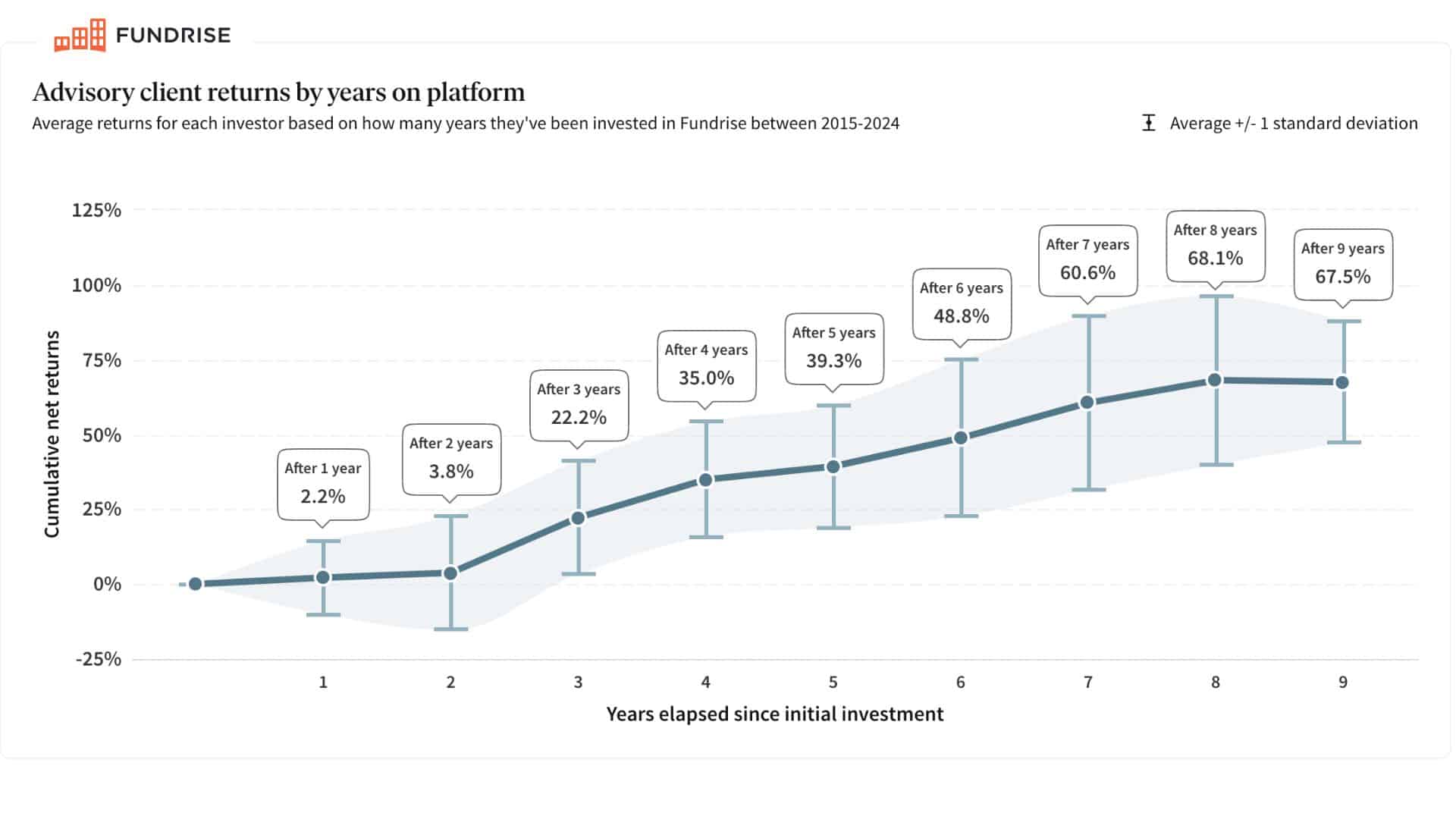

Fundrise

You don’t need a large amount of money to invest in real estate. Platforms like Fundrise allow individual investors to participate in commercial real estate online through eREITs (Real Estate Investment Trusts) or eFunds.

Fundrise’s crowdfunding model distinguishes it from traditional REITs, enabling average investors to engage in real estate deals. By selling eREITs directly to investors and eliminating intermediaries, Fundrise can offer fees lower than 90% of the competition.

A REIT is a company that owns or finances income-producing real estate.

Fundrise: What You Need to Know

Fundrise invests directly in real estate properties, which means you can’t just pull out your money whenever you want like with some other investments.

Liquidity Options

They offer quarterly redemption windows, but keep in mind:

- You can request to cash out four times a year, but it’s not guaranteed.

- Requests are handled on a first-come, first-served basis.

- They can pause or refuse redemptions if needed.

Redemption Fees

Here’s how the fees work:

- No penalty for cashing out from the Flagship Fund.

- If you have eREITs or eFunds, you might face a penalty of up to 3% if you sell before 5 years. After that, it’s penalty-free.

Fees

Fundrise charges:

- 0.85% annual asset management fee

- 0.15% annual investment advisory fee (this can be waived sometimes)

Investment Plans

They offer different plans based on your goals:

- Growth

- Income

- Balanced

Bottom line: Fundrise is a great way to invest in real estate, but remember that it’s more of a long-term commitment!

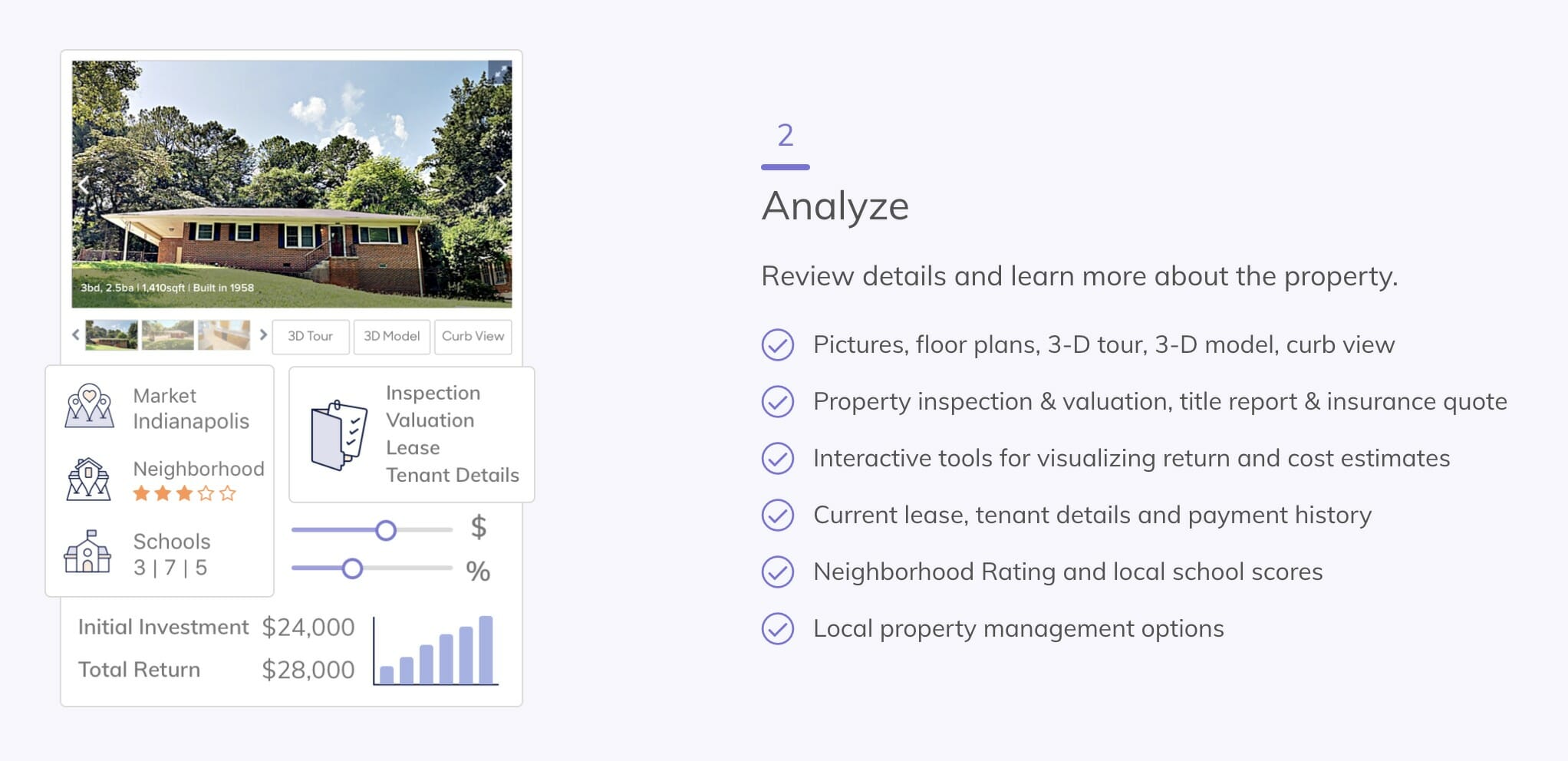

Roofstock

Want to be a landlord without the hassle? Roofstock might be your answer. It offers the benefits of owning a

What is Roofstock?

- An online marketplace for single-family rental properties

- Focuses on making real estate investing more accessible and efficient

- Offers pre-vetted properties, often with tenants already in place

Key Features

- Properties are independently screened and certified

- Many listings come with tenants, providing immediate cash flow

- Comprehensive property data and analytics available

- Options for remote investing across various U.S. markets

- Connections to property management services for hands-off investing

Bottom line: Roofstock aims to simplify real estate investing, making it more accessible for both new and experienced investors. It’s designed to provide the benefits of being a landlord while minimizing the traditional hassles.

Roofstock makes it easy to invest in real estate online. With properties available in over 70 U.S. markets, you can buy rental homes without ever visiting them. Most buyers live far away from their investments, and everything—from buying to managing the property—can be done online.

You can start investing with properties that typically cost around $25,000. If you’re an accredited investor, Roofstock One lets you invest with as little as $5,000 by buying shares in properties instead of whole homes.

Many of these properties already have tenants, so you can start earning rental income right away. It’s a great option for anyone looking to get into real estate without the usual headaches of being a landlord.

Invest like an Expert Without Being One

You don’t need years of experience tracking the stock market to grow your wealth. With the right approach, you can earn significantly more than the negligible returns offered by traditional savings accounts. Your hard-earned money deserves to work as hard as you do.

Every day you delay investing is another missed opportunity for potential growth. The sooner you put your money to work, the more time it has to compound and build your future financial security. By taking action now, you can set yourself up for long-term success and reach your financial goals faster.

Don’t let your money sit idle—invest like your future depends on it. Because it does.

Featured Image Photo Credit: “Money” by Pictures of Money on Flickr