Life comes at you fast in your 20’s. School, work, dating, maybe more school, changing friends, growing families. Everything can change quickly and money is the conduit that flows through it all. Learning the proper money skills is essential to navigating the changes life throws at you.

It’s not always easy though. We get it. You can head to Youtube for a five-minute how-to on chopping an onion or fixing a bike tire.

Personal finance, on the other hand, can quickly overwhelm you in a million directions. Roth IRAs, 401ks, mutual funds, credit scores. (Ahhhh!). I figured the Golden Butterfly was probably a yoga position, not an investment strategy.

So whether you’re looking for a place to start or overcome with decision fatigue, we’ve boiled down the basics of personal finance into four simple money skills to set you on a path to success for your 20’s and beyond.

1. Pay Yourself First

Without much thought, your job can quickly become nothing more than a means to pay bills, put a roof over your head and buy all the wonderful things your heart desires. Our society promotes a rat race mentality, and, before you know it, you’re running on the treadmill and not getting anywhere. Lots of people work hard just to watch their paycheck go into other people’s pockets.

You earned that paycheck, and deserve a cut of the pie. The most important skill you need to master: Pay Yourself First.

Set aside money from your paycheck each month to contribute to your savings. Creating an emergency fund, investing in your retirement, or saving for owning your own home are all realistic goals you can achieve by paying yourself first.

No matter how little you think you may be making, there’s always room to pay yourself first. If you’re early in your career or still working odd jobs, plan to set aside 5-10% of each paycheck. Once you have a comfortable income, 15% of your income should be the minimum threshold your pay yourself each month. Lots of people save above and beyond this baseline based on their goals (and given how long we’re living, you probably should).

It doesn’t have to be complicated. Set up auto deposits that pay into your savings, investments or debt payments each month so you can set it and forget it like any other bill. Paying yourself first each paycheck should be your number one priority.

2. Control Your Spending

You may be thinking 5% is too much to set aside. If you’re just getting by each month, it may be time to take a step back and look at the big picture.

The wisdom of life consists in the elimination of non-essentials - Lin Yutang

Tweet ThisToday’s culture is driven by unprecedented consumerism. Ads were always part of the radio and tv experience, but modern technology has changed the game. Data from smartphones and computers tailor advertisements to speak directly to you, encouraging everyone more than ever to spend, spend and – you guessed it – spend.

Become Conscious of Your Spending

The key to controlling your spending is becoming conscious of your spending habits. Take a few moments to examine how you spend your money each month. Mint is a great resource to understand where your money is going and how you might be able to cut back. There are plenty of ways you can save, even on a small budget.

If you’re feeling like you’re still running short after spending cuts, consider getting a side hustle. The internet has made it easier than ever to earn extra cash if you put the work in. If you do find yourself hustling some extra bucks or negotiating a raise, be sure to avoid lifestyle creep. Set that extra money aside to buoy your savings and investments and watch your nest egg grow.

Start a Budget

Hold up. Relax. There’s no reason to curl up in fear at the B-Word. Budgeting doesn’t have to mean you nickel and dime yourself on every purchase. We want to empower everyone to budget like a badass.

There’s plenty of different budget methods available to suit different tastes and priorities. I was so addicted to my Visa, I decided to go old school and shock my system with financial guru Dave Ramsey’s Envelope Method. You set cash aside each month in envelopes for groceries, gas, video games, El Pollo Loco…you know, the essentials.

Once it’s gone, it’s gone. It gave me a great sense of what I was actually spending. I couldn’t grasp this by swiping my credit card. It’s very reasonable if that sounds too intense for you. It’s just about finding something that will help you understand and guide your spending habits.

Your 20’s is a period when you set goals for your life. Life goals and financial goals work hand in hand. Budgeting is simply a tool to help you achieve them by living within your means. Controlling your spending is a key skill to master so you can always Pay Yourself First.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

3. Manage Your Debt

Debt has found a way to integrate into so many aspects of our lives: homes, cars, and education all run on debt for a lot of people. It’s important to distinguish between good debt (mortgages and student loans) and bad debt (credit cards).

The average credit card debt for Americans 35 and under is about $5,800. That’s the type of debt that can sink your goals and keep you running in place. Lots of people don’t like to deal with their bad debt and stick their heads in the sand. It’s the worst thing you can do.

Credit card debt interest will send you down a rabbit hole of money problems that could take years to recover from. Don’t put it off.

If you have debt, you’re not alone. Lots of people spend their 20’s confused about credit and credit cards. If you’re carrying bad debt the priority for your savings each month should be to pay off your debt. No ifs, ands or buts.

There are different methods you can take to pay off your debt, even if you’re not making a huge income or aren’t a hands-on person (one might even say lazy). Check and make sure your interest rates aren’t too high. If they are, you have options to refinance and consolidate your debt into a more manageable and cost-effective monthly payment.

4. Compound Your Investments

The first three skills are all about mastering money management and getting your financial house in order. Now, it’s time to consider what to do with all the money your saving. Investing in yourself doesn’t mean new clothes and spa days. You need to invest in the market and make sure your money is making money. There’s plenty of investing options, but they all rely on one underlying principle: compounding.

The Magic of Compounding

Compound interest is the interest paid on your initial investment plus the interest accumulated on your investment thus far. In other words, you get paid for your initial investment and the interest on your investment. Contributing regular payments each month begets more interest, which in turn provides a greater profit.

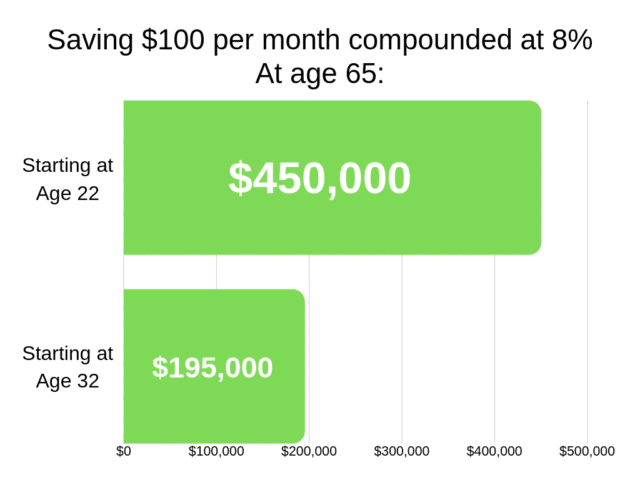

The magic of compounding will make a significant impact on your wealth if you start investing in your 20’s. Take a look at how investing just $100 per month benefits a 22-year-old investor assuming a return of 8% per year:

Don’t worry if you’re reading this at 32 (or later). Making $195,000 is still a great incentive to start paying yourself first. This graph just emphasizes the time value of money. The sooner you start saving and investing, the greater your potential returns will be. Start today!

Dollar-Cost Averaging

How do you get that 8% return? You can’t guarantee it, but you can ride the markets over time and reduce your risk with dollar-cost averaging. This is a long term investment strategy to build savings and wealth using regular contributions.

You can’t time the market with perfect stock picks. Dollar-cost averaging allows you to even out the highs and lows of the market with regular contributions each month regardless of price.

It’s risky to sock away $10,000 and then throw it at the stock market. You have to hope you’re getting a good price and the bottom doesn’t fall out from under you.

With dollar-cost averaging, you spread out $100 over 100 weeks (or months) to build that same $10,000 investment while navigating the ebbs and flows of the market. If your job offers a 401(k) or 403(b) retirement plan, you should definitely be taking advantage of dollar-cost averaging each month with regular contributions.

Don’t leave your savings sitting in your checking account or go for a once-off stock purchase. Making regular contributions to an investment portfolio each month is the secret to growing your wealth.

Taking the Plunge: Basic Investing Options

We appreciate how investing can seem scary, especially given the alarms of a recession and maybe even a stock market crash. But if you always worry about what might happen, you’re just setting yourself back. Building wealth isn’t a short term game, and, over time (that’s decades to be clear), investing in the market is the key to building your wealth.

There are plenty of investment strategies worthy of a deep dive. Just like budgeting, it’s all about finding tools you’re comfortable using and can make part of your normal routine. The easiest way to jump in is with a hands-off Betterment account that will autopilot your investments each month.

There are opportunities to grow your savings outside the stock market as well. Certificates of Deposit, or CDs, can allow you to get a higher interest rate than traditional savings accounts if you agree to not access the money for a specific period.

The longer your CD length, the more interest you can get to grow your money. Betterment recently launched a savings account that pays you interest rates head and shoulders above what the old guard financial institutions offer (that is usually zero) and is still FDIC insured. This is perfect for your Emergency Fund or an Opportunity Fund that can stay liquid.

Own Your 20’s (and Beyond!)

Being a financial badass starts with the decisions you make today. Using these four skills will allow you to escape the hamster wheel and take control of your life. Let your 20’s be the jumping board for a lifetime for success with the right financial decisions. And always Pay Yourself First!