On your first day of your new job, you get handed a stack of papers about the companies retirement plan and you are undoubtedly confused. Don’t worry, we’ve all been there. What are the differences between a 403b vs 401k? Let us find out.

Most of us were not taught about retirement plans at school. When starting my first job out of college, I had no idea what investments will work best for me and my situation. Out of ignorance, I allocated 15% of my salary towards my 401k contribution. I then entered different percentages towards the various funds available in the plan until the total percentage equaled 100%.

So much for making sense of retirement plans fresh-out-of-college graduate.

![]()

403bs vs 401k: Major Differences

Many retirement plans come in different flavors, and the most common retirement plans offered by employers are the 401k and 403b plans.

Both 403b and 401k plans allow employees to make pre-tax contributions towards a tax-deferred account. This means that your contributions are first deducted before taxes are deducted from your paycheck.

Making pre-tax contributions benefits you financially by lowering your taxable income and by paying less money towards your retirement savings. Your money invested in these retirement plans grow tax-free until you withdraw the money from your plan.

As of 2018, you are allowed to make a maximum contribution of $18,500 per year to your 401k and 403b. Most employers will make a matching contribution towards your retirement plan.

This means for every dollar you contribute towards your retirement plan, your employer also contributes a similar amount.

Your employer’s matching does not count towards the yearly contribution limit of $18,500, giving you a lucrative incentive to save.

You are allowed to begin withdrawing from your retirement savings without penalty starting at age 59½. If you withdraw from your retirement savings before turning 59½ years old, you will be penalized an additional 10%.

You are obligated to withdraw from your retirement at age 70 because of the Required Minimum Distribution (RMD). If you fail to make the RMD, you will be penalized 50% of your RMD for that year.

And that is where the similarities end between 401k vs 403b accounts.

What Makes a 401k Unique?

401k plans are offered at most companies in most field of work. On the other hand, 403b plans, are offered to specific employees who work in the public sector. This can be teachers, government organizations, or non-profit organizations.

With a 401k employees can select from a variety of funds to invest in, including actively managed mutual funds, stock index funds, bond mutual funds, and your employer’s stock.

A mutual fund is a way for investors to pool their money towards a fund, in which the money is invested towards buying stocks or bonds. Actively-managed mutual funds are a kind of mutual fund in which a manager. They manage the fund by picking stocks for the fund based on their analysis.

Stock index funds, more commonly known as index funds, are a kind of mutual fund in which a computer keeps track of a stock market index (such as the Dow, S&P 500, or Nasdaq).

By keeping track of a particular index, the computer allocates money to stocks based on that index. Bond mutual funds invest in various bonds, or debt issued by the government, with the incentive of being paid interest.

You may be offered to invest in your employer’s stock, especially if your employer is publicly traded on the stock market

Fiscal flexibility that’s funny, free and delivered weekly.

How About 403bs Then?

403b plans are also known as Tax-Sheltered Annuities (TSA). Despite its other name, 403b plans allow employees to not only invest in annuities but also invest in mutual funds, depending on the employer.

An annuity is a financial product that is offered to someone who is concerned that he/she will outlive his/her savings. When an employee contributes on a recurring basis, the money is invested in a deferred annuity. This type of annuity pays the employee at a later time.

The money invested in an annuity is then invested in stocks or bonds. Employees are locked into contracts, known as the surrender period, in which money from the annuity cannot be withdrawn within this period of time.

These surrender periods usually last for years, so it is prudent to not put money into an annuity that you may need to withdraw during the surrender period.

When the time comes to receive recurring payments from an annuity, in a process known as annuitization. The employee will start to receive payments from his/her annuity until he/she dies.The amount paid and payment period is determined by the employee’s life expectancy and current age.

Some employees enrolled in 403b plans, such as teachers in public schools, can also enroll in another retirement plan called the 457 plan. A 457 retirement plan is similar to a 401k and 403b plan, with the exception that early withdrawals can be made without the 10% penalty.

Takeaways on 401k vs 403b

There are many takeaways when investing in 401k and 403b retirement plans. First, it is prudent to contribute at least to the full employer match in your company’s retirement plan.

Companies usually match between $0.50 and $1 for every dollar you contribute to your retirement account. This is literally free money you do not want to miss out on.

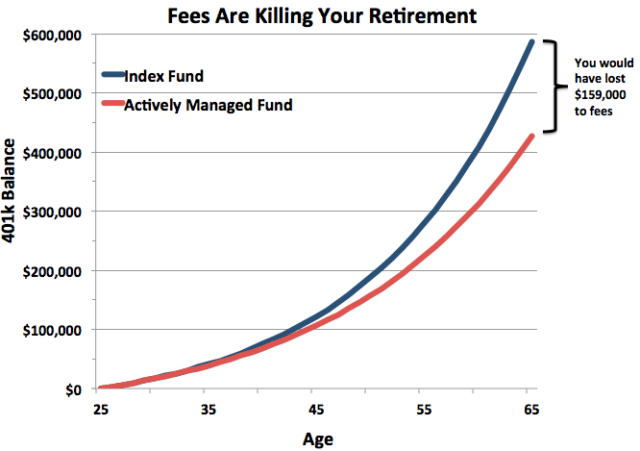

Second, when deciding on what funds to invest in, look for index funds among the investment options. Index funds usually have lower expense ratios compared to other available funds, which are likely actively managed.

In addition to having higher expense ratios, actively managed funds tend to have a front-end cost. A cut of your investment goes to the fund manager before any investment is made- regardless of the funds’ returns.

This means whether or not the actively managed fund performs better than the index fund, the fund manager still gets paid!

How Much Should You Invest?

A good start for a person in his/her 20s is to invest 80% of the retirement contributions in stocks and 20% in bonds. This concept of personal finance is known as asset allocation.

As a person gets older, it is prudent to slowly allocate more of the retirement savings towards bonds. Having more money invested in bonds makes your savings less “volatile” or risky.

Asset allocation is determined by a combination of a person’s age and tolerance for risk. Younger investors can afford to take on more risk, because of time. When viewed from a longer-term window, such as 10 years, the market always goes up.

We cannot predict what will happen to us in the near future, and an annuity is geared towards a longer-termed future that is even more uncertain.

That’s why I made no mention of recommending annuities because most annuities are not good investments. A family friend who is a licensed financial advisor, seldom recommends annuities to her clients.

A life circumstance can happen during the surrender period in which the money from the annuity is needed. The employee will have to pay a penalty in addition to the 10% early withdrawal penalty from the 403(b) retirement plan.

What if I Leave the Company?

Roll over your retirement contributions to an investment advisor when you leave your employer. Rolling over your retirement contributions allows you to consolidate your savings into one place, helping you easily keep track of your funds and investments.

More importantly, you will reduce fund costs and therefore increase your investment returns. The expense ratios of the mutual funds available to invest in my 401k plans ranged between 0.25% and 1.5%.

I rolled over my retirement contributions to a Rollover IRA Brokerage account with Vanguard. By investing my rollover contributions in the Vanguard Total Stock Market Fund Admiral Shares index fund (VTSAX), I significantly reduced annual fund costs and increased investment returns.

This is because VTSAX has no front-load fees and its expense ratio is a stunningly low 0.04%.

Nevertheless, 401k plans and 403b plans are very similar as far as retirement savings plans go. Both have the same basic contribution limits, and both have a required age of 59.5 to start making distributions without penalty. Remeber, if your employer is matching your 401k or 403b, always take the free money.

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.