There isn’t a “one-size-fits-all” approach to finding the right budgeting system. It should target your financial goals. I’m going to show you different ways to create a budget that sticks to your lifestyle. Simply put, if you want to finally take control of your money, you’ll love this post. Let’s get started!

Your budget should be goal-based. Whether it’s for reducing spending, boosting savings, or crushing debt, knowing your why and your what will keep you on point. What do you want to achieve?

Knowing what those goals are before you attempt to budget is essential.

The hard and fast budgeting rule: Use the one that works and spend less than you earn.

Types of Budgeting Systems

What’s the 50-30-20 Budget Rule (aka Balanced Money Formula)?

Elizabeth Warren and Amelia Tyagi coined this term in their book: All Your Worth: The Ultimate Lifetime Money Plan. It breaks down like this:

A percentage of your post-tax income is split three ways (or placed into three different buckets):

- 50% Needs (must-haves / non-negotiables)

- 30% Wants (e.g., dinner out with friends)

- 20% Savings (e.g., credit card payments, retirement, or an emergency fund)

It’s easy to use and works regardless of how much money you earn.

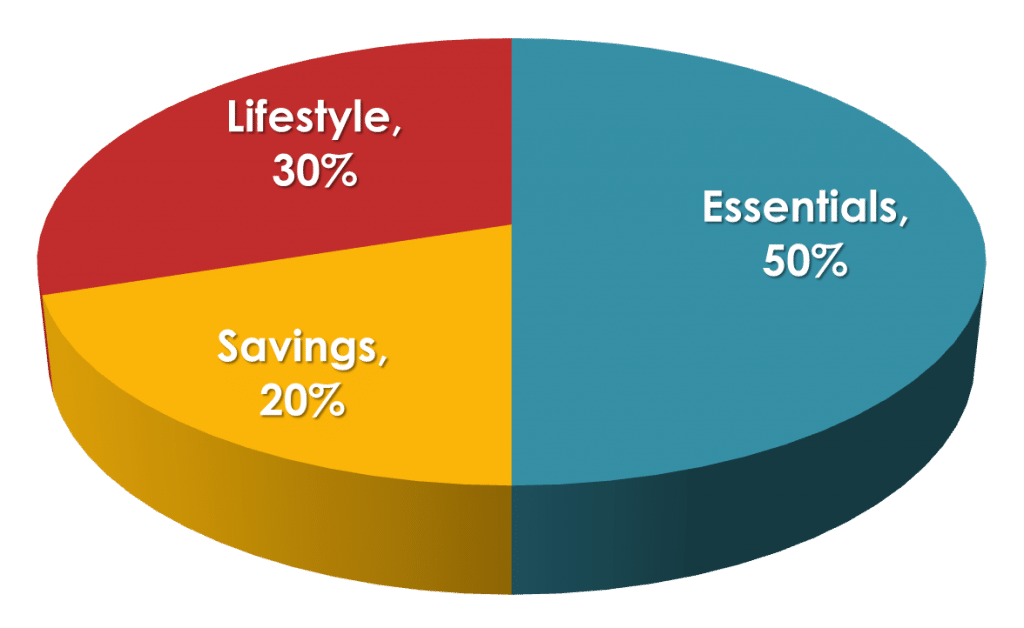

The 50/30/20 Rule

The 50-30-20 Budget Rule says 50% of your income goes to essentials, 30% to wants, and 20% to savings.

For example, if your after-tax monthly income is $5,000, you’d put:

- $2,500 into your Needs bucket (50%)

- $1,500 into your Wants bucket (30%)

- $1,000 goes to Savings (20%)

Next, you’d categorize your spending into these three buckets. Your needs would be rent, utilities, and groceries; all of the essentials you cannot live without.

Wants would be gym memberships, music streaming services, or happy hour drinks. Your wants are the non-essentials (or “nice-to-haves”).

Savings could be either short-term or long-term goals. Perhaps you’re trying to build savings for a home downpayment or retirement. Maybe you’re trying to pay down debt. 20% of your income goes here.

The beauty of this system is in its simplicity. Some people prefer to only track three categories because it’s easier.

Also, feel free to adjust the percentages to accommodate your lifestyle. Or swap categories.

For example, I set aside 30% of my income to savings and only 20% to wants. Maybe 50% doesn’t seem like enough to you – increase it to 57% and adjust the remaining buckets accordingly.

The 50-30-20 budget rule affords you flexibility, which is at the heart of every good budget.

The Envelope System (aka Envelope Budgeting)

It’s the non-digital approach to budgeting: an old school system using cash. It doesn’t even require an Excel spreadsheet. Ideal for those unwilling to share their financial data or are wary of technology.

Break up your monthly cash flow into categories. What are your living expenses? Your envelope categories might look like this:

- Cell phone

- Health insurance/health care

- Car payment / car insurance

- Eating out

- Rent

- Utilities

- Debt payments / loan payments

- Gas / transportation

The Envelope System

The Envelope System assigns each spending category an envelope based on your monthly expenses. Allocate a cash dollar amount to each category. Once you spend the cash in that envelope, you can’t spend any more.

Grab an envelope and assign it to a spending category.

For example, one envelope will be labeled ‘rent’ while another will be marked ‘debt payment.’ Assign enough money to each category based on your monthly expenses.

Fill each envelope with that month’s cash. Once you spend the money in each envelope, you’re not allowed to spend any more.

If you’re desperate for cash, borrow the money from one of your other categories to cover it (or wait until next paycheck). The idea is not to go tapping your emergency fund or retirement savings to cover a night of bar hopping.

That’s how the cash envelope system helps you save money.

Reverse Budgeting System

Paying yourself first is the number one habit to build. Think of it as your present self taking care of your future self. Take a percentage of your monthly income and set it aside.

This money goes towards your emergency fund, retirement, and long-term savings goals.

Second, pay your fixed expenses like rent, food, and utilities. Lastly, use what’s leftover for discretionary spending. Things that aren’t necessities like bars and restaurants.

For example, if you’re using the 50-30-20 Budget Rule, you’d take 20% of your income and put it towards your savings.

Keep it simple. The fewer moving parts, the better. Think of your monthly income as buckets and think in terms of percentages – not dollar amounts. Why?

Because percentages ensure you’re contributing the right amount to each category. They’re more accurate than dollar amounts and help to increase your savings rate (or curb your spending).

What if one week you earn $200 and the next week you make $550? Your 20% will look different week to week (especially true for those with variable income).

Using a percentage ensures its relative to your income size.

60% Solution

This one comes from Richard Jenkins, the former MSN Money editor-in-chief. After two decades of budgeting, he arrived at a simple conclusion which breaks down like this:

- Keep it simple

- Prevent overspending

- Avoid carrying excess debt

The 60% Solution stems from the periods in his life when he and his wife felt relatively in control of their finances – even when they were making less money.

It’s a 60/40 split with two buckets. 60% of your income goes to committed expenses while the other 40% (split four ways) goes towards savings.

Let’s break it down.

60% Committed Expenses. Food, clothing, household expenses, insurance, all bills, and taxes.

Mr. Jenkins views “committed expenses” like this:

I call these ‘committed’ expenses rather than ‘fixed’ nor ‘non-discretionary’ expenses because things like music lessons are neither fixed in amount nor absolute necessities, but rather commitments my wife and I have made to provide for our children.

Back to that 40%

10% Retirement Savings. Your 401(k), Traditional, Roth, and SEP IRAs, and any other retirement accounts.

10% Long-Term Savings. Your emergency fund, down payments for a home or car, and debt payments.

10% Short-Term Savings (aka Irregular Expenses). You know Xmas happens every year, but how many people save for it? Home repairs, birthdays, and upcoming vacations are “predictable irregular” expenses.

10% Fun Money. Spend it on anything you like during the month. Hobbies, dining out, and monthly memberships live here.

The simpler you make it, the easier it will be to follow. If you automatically deposit money into the appropriate buckets, you never have to think about it again.

Budgeting Tools to Keep You On Track

Setting up a monthly budget allows you greater insight into your spending habits. Start with your take-home pay.

Look at your bank statements for help. A reasonable budget considers two factors: what’s coming in and what’s going out. Creating a spending plan helps when you have the right tools.

Here are a few worth a look.

Personal Capital

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

Personal Capital is a budgeting and wealth management tool catered to investors. It tracks your spending along with your investments. The tool analyzes your portfolio for weaknesses and helps you avoid overpaying in fees. It also offers suggestions on ways you can improve.

You Need a Budget

You Need A Budget (YNAB) is zero-based budgeting where you assign every dollar a job. Your financials are all in one place, divided into categories, and lets you anticipate upcoming expenses. It’s a digitized, more robust version of the Envelope System and costs $84 a year. We interviewed YNAB’s creator. Have a listen here.

What's Zero-Based Budgeting?

Zero-based budgeting is when you assign every dollar of income to an expense category until you hit zero (i.e., there’s no more money left to budget). It’s when your total monthly income minus your total monthly expenses equal zero.

For example, if you had a $500 paycheck (and needed to allocate that $500 amount towards expenses) a mock allocation might be $275 to rent, $100 to groceries, $75 for utilities, and $50 for savings.

You’ve just given every dollar a job and have zero dollars left to budget.

EveryDollar

EveryDollar is a zero-based budgeting tool created by Dave Ramsey. It lets you add your monthly income, plan expenses, and track your spending. The app has both a free and paid version ($129 annually).

The paid version lets you link your bank account (and view your account balance), automatically stream transactions, and gains you complete access to Ramsey’s Financial Peace University (call-back support and coaching calls).

Mint

Mint is free software that lets you create a budget, keeps you up to date with your spending, looks for patterns, and ways you can cut costs. It even looks for deals that align with your spending habits.

For example, if you spend a lot of money at grocery stores, Mint will suggest a rewards credit card that compliments that spending habit. It also offers budgeting tips, sends alerts for unusual account charges, and reminds you of upcoming bills.

We even created a course on how to use it because we thought it was that important. It’s called Mastering Mint.

Mvelopes

Mvelopes is a digital version of the Envelope System. They offer three plans for their customers from a basic version letting you create an online budget and linking your bank accounts; to having your own financial coach who calls you monthly and helps you create and follow a personalized financial roadmap.

Quicken

Quicken is a money management tool offering several different plans depending on your needs. Their software lets you view and pay bills, create a budget, plan for retirement; as well as run your business and handle property management.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Automate Your Budgeting Tools

Many digital tools let you link your bank account and set up alerts to manage your spending. They also monitor your spending habits, filter your income and expenses into appropriate categories, and run monthly comparison reports.

Integrate these tools into your personal finances.

The more you can put your financial infrastructure on autopilot, the less you have to think about it. Set up recurring deposits into your savings accounts. Set up auto bill pay for monthly expenses. Make it even easier and set them to all pay on a specific date.

Then monitor it all through your budgeting system to see what’s coming in versus what’s going out.

Having a separate checking account to handle fixed (and variable expenses) while another handles long-term savings goals like retirement and emergency funds are ok. It’s part of having a savings plan.

You're more likely to follow through with a budget when you've got individual savings accounts for each goal.

Tweet ThisPrioritize: Know What’s Important and Why You’re Saving

In his book, Mastering Mint, Andrew talks about creating budgets that fit your life based on your core needs and desires. What do you love? Travel? Artisanal imported coffee? Live sporting events? Location independence?

Keep your list short with three to four core needs. For me, it’s location independence, travel, and providing experiences for my family.

Andrew refers to your budget as a tool that lets you “maximize your happiness while building financial security.”

When you focus your budget towards your goals, using one of the styles mentioned above, it should become clear what’s worth spending money on and what’s not. Suddenly, tracking monthly expenses doesn’t seem as dull.

Ramit Sethi calls this conscious spending:

Spend extravagantly on things you love, and cut costs mercilessly on things you don’t.

Be Comfortable with Your Budgeting System

Remember the hard and fast budgeting rule: use the one that works and spend less than you earn. It should be easy for you.

It might have all of the bells and whistles but that’s irrelevant if you never use it because of its complexity.

For example, if you hate digital devices don’t get a budgeting app. If you’re turned off by tech you’ll be turned off by budgeting.

Using an Excel spreadsheet is just as good as using Mint. It might require a little more work to use a spreadsheet but it’s just as effective.

Technological advances (e.g., budgeting apps) created to enhance your life only work if using them makes your life easier.

Decide what the preferable option is for you: digital or manual?

Final Thoughts On Budgeting Systems

Your first budget takes the most time to set up. Going through your bank statements isn’t my idea of a good time. But it’s revealing. You’ll notice spending patterns and discover things about yourself you weren’t paying attention to.

Having money left over at the end of the month feels fantastic. Allow yourself some wiggle room. If you’re too strict with yourself, you’ll be less inclined to follow it. Know that you’ll have unexpected expenses and roll with it.

You don’t have to do it alone; there’s plenty of budgeting apps to help you hit your savings goals. Are you setting money aside for your soon-to-be little girl arriving into the world? Putting money aside to hit financial independence sooner?

A budget with a goal behind it is likely to be more successful than one without. You just need the right system.