The two biggest expenses in life are interest and taxes. We know how to avoid paying a lot of money in interest, achieve and maintain an excellent credit score, refinance debt to a lower interest rate, and avoid credit card debt. How to reduce taxable income is slightly more complicated.

But legally paying less in income tax is well within the capabilities of everyone reading this. The biggest savings on your tax bill will come from your tax-advantaged retirement accounts. If you’re strategic and max out various IRA accounts and other retirement savings accounts, you can see tremendous tax savings.

Some of the IRA stuff is super high level, and we brought in Brandon from the Mad Fientist to break things down for us. Some of Brandon’s strategies may be too much work for some of us.

But there are plenty of simpler methods those of us lower down on the personal finance nerd scale can use to reduce taxable income.

Tax planning isn’t something you should only think about at the end of the tax year or a few days before the filing deadline every April when you’re scrounging for receipts and trying to find the closest H&R Block office.

If you’re serious about saving money, don’t worry about cutting out your daily Starbucks order. Learning how to reduce taxable income is where the real money is.

IRAs

An IRA is an Individual Retirement Account. It’s a tax-advantaged way to save and invest for retirement. There are several types of IRAs, but the following are the most common.

Traditional IRA

A Traditional IRA is not taxed upfront but at the point of withdrawal. The money invested through the Traditional IRA grows tax-deferred. Upon withdrawal after age 59 1/2, the money is taxed as income. IRA contributions are updated sometimes.

For 2019, you can contribute up to $6,000. If you are aged 50 or older, you can make a catch-up contribution of an extra $500, for a total of $6,500. Withdrawal is considered income and taxed as such.

One of the significant advantages of investing through a Traditional IRA is its ability to reduce taxable income:

Contributions to a traditional IRA can reduce your adjusted gross income for that year by a dollar-for-dollar amount.

Roth IRA

A Roth IRA is taxed upfront. The money inside the Roth grows tax-free. For 2019, the contribution limits are the same as for a Traditional IRA. Because you paid taxes on contributions going in, there is no tax on the money when you start withdrawals at age 59 1/2.

SEP IRA

A SEP IRA is a simplified employee pension. It’s a retirement account for those who are self-employed. The employer is given a tax deduction for SEP contributions and can make contributions on behalf of eligible employees. You can have a SEP in addition to a Roth and Traditional IRA, and the SEP has a much higher allowance for the contribution.

SEPs can get set up to contribute up to 25% of salary up to an annual maximum, which is $56,000 for 2019.

A SEP IRA is considered a Traditional IRA by the IRS, so the same tax rules apply to a SEP as to a Traditional IRA.

Traditional or Roth?

When you’re in the prime of your career, you’re making more money and in a higher tax bracket than you are likely to be in the future. You want the tax advantage of the Traditional IRA during your highest-earning years because once you give up those tax advantages, you lose them forever.

Will tax rates be raised in the coming years? Yes, probably. But new loopholes will be added too, and as long as there are people like Brandon around, we will know ways to take advantage of them. Is it a risk? It is, but it’s a calculated one.

Advanced IRA Strategies

Having any kind of IRA is a good start, plenty of people have no retirement savings:

A recent report from the U.S. Federal Reserve found that nearly a quarter of all American adults have no retirement savings or pension at all.

But if you want to ramp up your retirement plan, these advanced IRA strategies can help you do it.

Roth IRA Conversion Ladder

Both types of IRAs are used at different stages of life to take advantage of current tax law and reap the most tax benefits possible. Brandon has a method for this, the Roth IRA Conversion Ladder. You contribute to a Traditional IRA during your working life because it’s likely that your tax rate is higher now than it will be after retirement.

After you leave your job, you will have less taxable income. During this time, you slowly roll the Traditional IRA to a Roth. This rollover counts as ordinary income, so to do this tax-free, convert a dollar amount equal to your tax deductions and exemptions.

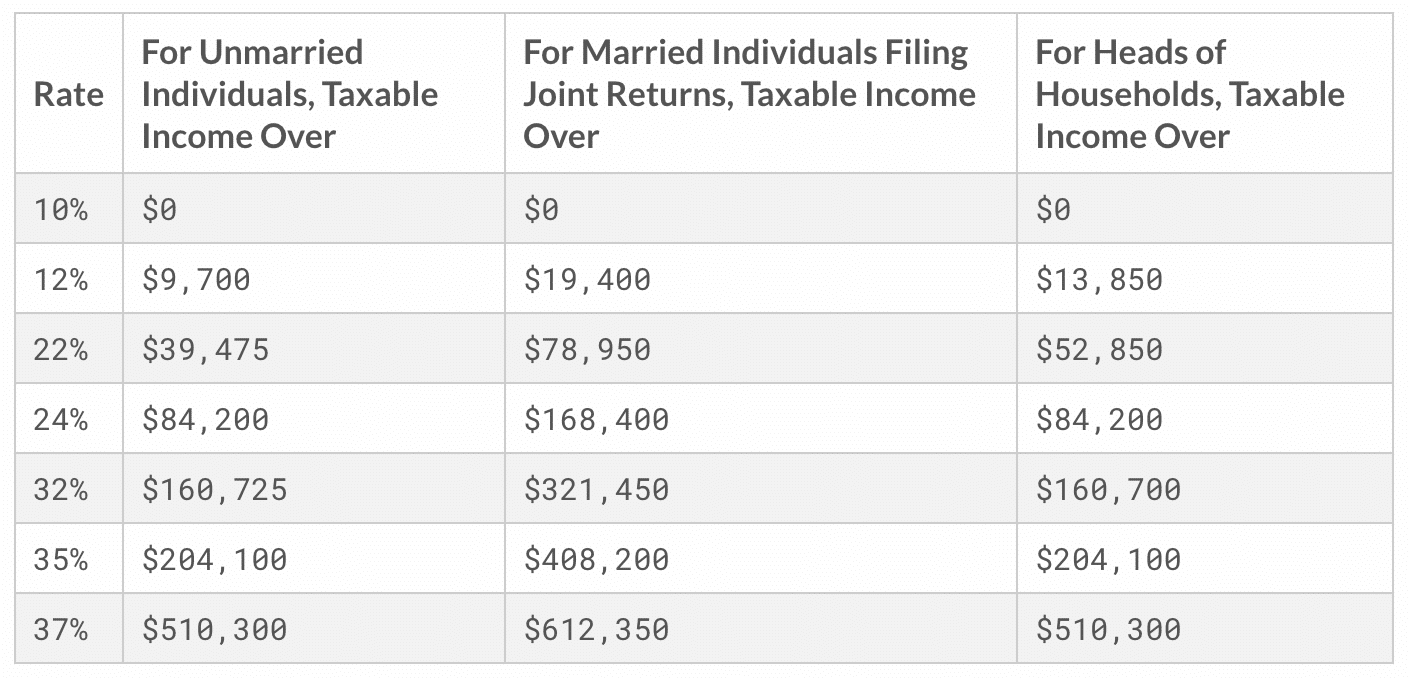

During this time, you live off your long-term capital gains and dividends because they are taxed at 0% so long as you’re in the 10% or just under the limit for the 12% tax bracket. For 2019, anyone making less than $9,700 is in the 10% bracket, and anyone making between $9,701-$39,475 is in the 12% bracket.

Long-term capital gains are taxed at 0% for those making between $0 and $39,375.

The Roth IRA Horse Race

For our listeners with advanced personal finance knowledge, Brandon has a strategy he calls the Roth IRA horse race. It’s a way to supercharge your Roth conversion ladder by minimizing taxes.

When you roll a Traditional IRA to a Roth IRA, you can undo the conversion before filing your tax return. This is known as a Roth recharacterization.

You could execute the conversion in January and then undo the conversion by April 15th of the following year (or October 15th, if you file an amended return) to the IRS; it’s like the rollover never happened.

This is high-level stuff, and it’s a lot of work. It can pay off, though.

Fiscal flexibility that’s funny, free and delivered weekly.

401ks

Many people may be more familiar with 401ks than IRAs because some employers offer 401k accounts as an employee benefit. A 401k is similar to a Traditional IRA. The money goes in tax-free.

When you leave your job, whether it’s to take a new one or to retire, roll that account into a Traditional IRA. This simplifies things. You aren’t trying to keep track of several accounts, and it gives you more control over fees.

You may not even know how much you’re paying in fees for your 401k, and if you take the time to find out by reading the prospectus, there isn’t much you can do about it anyway.

Your employer selects your options. And investment account fees can cost you a lot of money. Americans pay over $6 billion in investment fees per year.

Vanguard makes rolling over your 401k easy, and they have very low fees.

HSAs

An HSA is a Health Savings Account. While not created as a retirement account, you can use it that way if you know what to do.

If you’re in a high-deductible health insurance plan, you can use an HSA. It’s tax-free money set aside for medical expenses.

An HSA is a bit like a Traditional IRA or 401K in that the money is not taxed going in. It grows tax-free while in the account, and when used for medical expenses, it isn’t taxed going out either. Completely tax-free money!

The contribution limits for 2019 are $3,500 for an individual and $7,000 for a family.

Should you leave your job, get fired, or laid off, you can take your HSA money with you and use it to pay Cobra health insurance premiums. Once you reach 65, you can use it to pay Medicare premiums.

Even if you’re self-employed, you can set up an HSA for yourself. Just buy a plan that is HSA qualified, and you can reap the rewards available to the rest of us wage slaves. About 20% of the offerings on the health care exchange are HSA qualified, so you’ll have several to choose from.

Now here’s the hack. Brandon had surgery that cost $2,500 out of pocket to meet the deductible. He paid that with his money, not the money in the HSA account. He kept the receipt.

When he wants to spend $2,500 on a vacation or a new television or whatever, he takes the money out of the HSA, spends that and then provides the receipt he was given for the surgery. Genius!

Other Ways to Reduce Taxable Income

At some point, your retirement accounts are maxed out, and if you want to lower your tax rate, you’ve got to look for other ways to do it.

Monetize Your Hobby

As we learned in our Natali Morris episode, it’s the people who earn salaries from an employer who take the hardest tax hit. The tax law is set up to encourage people to create small businesses.

Do you have a hobby, cooking, photography, knitting? monetize that hobby. Or maybe you have a side hustle, pet sitting, babysitting, or mowing lawns.

Set up an LLC and take advantage of all of the tax-deductible business expenses like the home office deduction, health insurance (if you don’t have employer-sponsored health insurance, and bought your own coverage), self-employment tax, internet, and phone bills.

Save For College

With college costs at sky-high levels, using a tax-advantaged account to save for educational expenses with a 529 plan is a necessity. The account can be for your children or any children in your life or yourself if you plan to start or go back to college one day.

529 contributions are not tax-deductible on your federal income tax. Still, the money invested through the account grows tax-free. And depending on where you live, you may be able to deduct the contributions from your local taxes. These states allow tax deductions or tax credit for 529 contributions.

Make a Donation

It’s a scientific fact that being generous makes us happy.

Researchers have found a connection between happiness and the performance of selfless acts. Giving to others, they say, activates an area of the brain linked with contentment and the reward cycle.

Charitable contributions are tax-deductible so long as you itemize. Both cash gifts and donating items of value are deductible. Just be sure you have documentation of your donations.

Buy a Home

Remember what we said was the other most expensive thing in life apart from taxes? That’s right, interest. For most of us, buying a home requires a mortgage, and we pay interest on that mortgage.

But you can deduct your mortgage interest and property taxes. For 2019, you can deduct all of your mortgage interest up to $750,000. The interest on home equity loans or lines of credit may be deductible, too, if you use the money for home improvements.

To qualify for the mortgage interest deduction, you must itemize.

Make Your Home Energy Efficient

Want to double dip the tax savings you get from that home equity loan or line of credit? Use the money to make your home more energy-efficient. There are several residential renewable energy tax credits homeowners can take advantage of in 2019, including installing solar panels and solar-powered water heaters.

Bonus Content

While we had the chance, we wanted to pick Brandon’s brain on a few other subjects apart from how to reduce taxable income.

What To do With $3,000

We asked Brandon what he recommends if you have $3,000 to invest. He suggests putting all of it into a 401k if you have matching. Always take matching because it’s free money.

If you don’t have matching, put it into a Traditional IRA. If you can’t contribute to a Traditional because you’re over the allowed contribution limit for the year, then it goes into a Roth.

What If You Need Your Money Sooner?

This is all great if you plan to retire late in life, but what if you want to retire early? You need money to live on, and you don’t want to pay early penalty withdrawals.

If you’re concerned about having a lot of money tied up and not easily accessible, a Roth IRA is a better choice. The principle can be withdrawn anytime without being taxed or penalized, making it an excellent place to park a portion of your emergency fund, too, because it’s growing tax-free.

Index Funds

We are fans of set it and forget it, and Brandon is too. He uses Vanguard’s Total Stock Market Index for his Roth contributions because it covers a large swath of the market. We did a review of the best Vanguard funds – you should check it out!

If you pay a fund manager to invest your money because you think the best brains Wall Street has to offer can do a better job than an index fund, you’re wasting your money.

Here is a curated list of several investment strategies we’ve already covered and you can build them all with index funds or ETFs:

- Coffeehouse Portfolio

- Swensen Portfolio

- Ivy Portfolio

- Larry Portfolio

- Permanent Portfolio

- Lazy Portfolio

- Minimum Variance Portfolio

- Dividend Aristocrat Portfolio

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

Index funds outperform managed funds 90% of the time.

If you think you can spend enough time researching stocks to be in the 10% that’s beating the index, give us a call, and we’ll get you on as a guest ASAP.

Really, though, you would be better off spending your time the way Brandon has and researching how to reduce taxable income. Remember, tax fraud is illegal; tax avoidance is encouraged.

Fees are the biggest drag on investing.

Tweet ThisThe Mad Fientist Lab

Perhaps unsurprisingly, Brandon is a developer like Andrew. They must be wired differently than the rest of us. He wrote software that is available in the Mad Fientist Lab that allows you to input some numbers and chart your timeline for reaching financial independence.

Show Notes

The Mad Fientist: Brandon’s website and podcast.

Betterment: Our favorite investing tool. Use this link and get six months with no fees!