We talk a lot about the importance of diversification, asset allocation, and portfolio construction at Listen Money Matters. We know that a buy-and-hold strategy of low-cost index funds(or ETFs) is superior to picking individual stocks (and a smarter way to build wealth). Throughout it all, you may have heard the term minimum variance portfolio tossed around. What the heck is that?

It’s a fancy way of saying a low-risk portfolio (after all, variance is a risk measurement). It carries low volatility as it correlates to your expected return (i.e., you’re not assuming greater risk than is necessary).

Satisfied? Me neither.

In this post, we’re going to talk about what a minimum variance portfolio is, examples of how to build one, and why it’s a useful risk management tool.

The method of beating the market is not to exercise superior clairvoyance but rather to assume greater risk. Risk and risk alone determines the degree to which returns will be above or below average. – Burton Malkiel

What Is A Minimum Variance Portfolio?

A minimum variance portfolio holds individual, volatile securities that aren’t correlated with one another. One security might be surging in value while another is plummeting – it doesn’t matter. Because of their low correlation, the portfolio as a whole is viewed as less risky. But how?

Let’s go deeper.

Any two investments with a low correlation to each other can be a minimum variance portfolio (e.g., stocks and bonds). Variance is a measurement of risk. There’s a lot of math behind it but simply put:

Variance measures the daily fluctuations of an investment. The more significant the change in price, the higher its variance, and more volatile. For example, bonds have a lower volatility than stocks and low variance.

The standard deviation of an investment is the square root of the variance – both measure portfolio risk.

When people talk about what a wild ride the stock market is, that’s what they mean. One day your stock is up 24%, the next it’s down -5%.

If that gives you pause, chew on this:

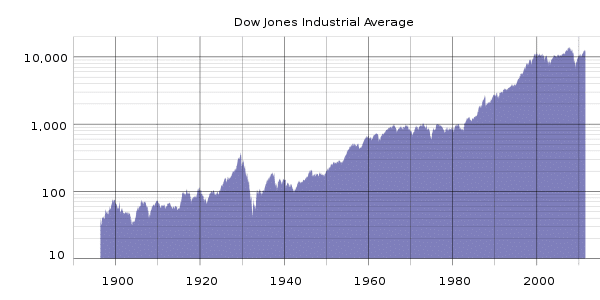

The market always goes up and is a reflection of human progress.

Snapshot of the Dow from 1900 through the present. The market always goes up.

Now back to our regularly scheduled programming.

Correlation measures movements between investments. It’s kind of like watching two people on a date. Sometimes, they’re in sync, move in lockstep, and finish each other’s sentences. Other times, well, let’s say it’s painful to watch.

For example, if two assets are negatively correlated, they’ll move in opposite directions – kind of like that horrible date you had once.

When implementing a minimum variance portfolio, you want investments with low (or negative) correlation. You want diversification across asset classes. Why?

A Word About Diversification

Harry Markowitz, Modern Portfolio Theory, and the Efficient Frontier

Harry Markowitz is a smart guy. His work in the 1950s won him a Nobel Prize and has become a cornerstone for modern portfolio construction. Notable accolades include:

- Nobel Prize recipient in Economics

- His book, Portfolio Selection, was born out of his Ph.D. dissertation while attending the University of Chicago

- Designed a computer language at RAND Corporation

- Hedge Fund Manager

- Acorns Investment Committee Advisor

He discovered that investments (even the volatile ones) if grouped a certain way, could reduce your overall portfolio risk.

Tweet ThisMr. Markowitz explained MPT as a rating of two measurements:

- Volatility

- Expected return

At its core, MPT seeks to lower portfolio volatility through diversification while increasing your return. As investors, that’s the dream.

Investopedia puts it this way:

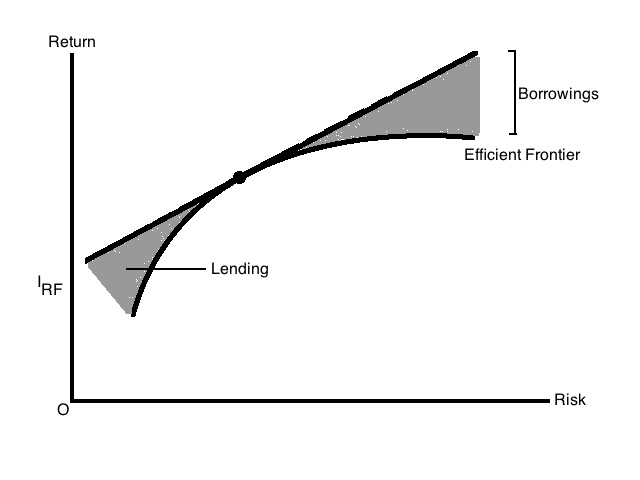

Modern portfolio theory says that portfolio variance can be reduced by choosing asset classes with a low or negative correlation, such as stocks and bonds, where the variance (or standard deviation) of the portfolio is the x-axis of the efficient frontier.

Fiscal flexibility that’s funny, free and delivered weekly.

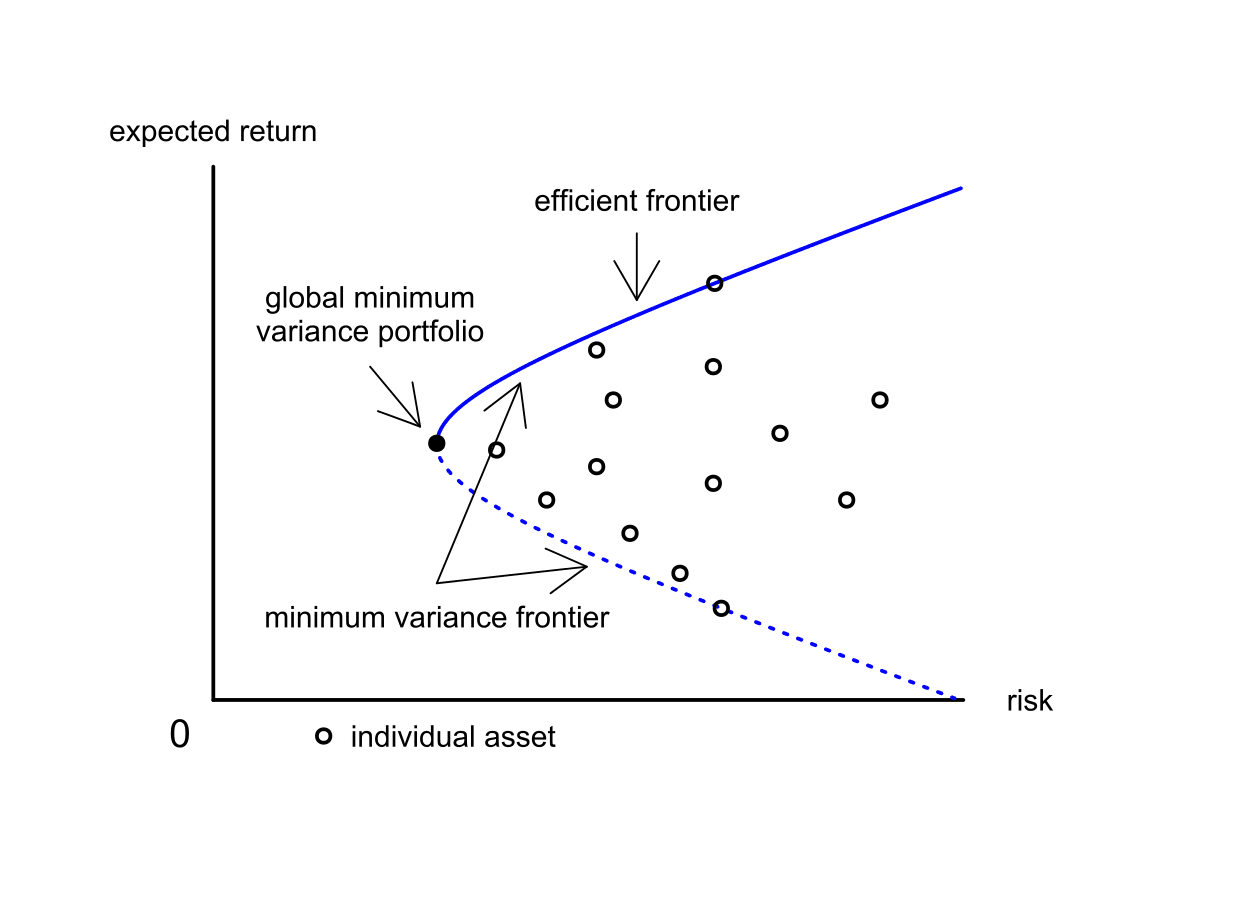

The Efficient Frontier

The Efficient Frontier is a graph that rates your portfolio’s risk (x-axis) versus return (y-axis). It shows you the amount of profit you should expect from an assumed level of risk.

It tells you things like, “Hey! You’re taking too much risk for the reward you’re hoping for. Diversify by adding more investments to your portfolio yo!”

It’s not the riskiness of an individual stock that matters, it’s actually how the stock affects the riskiness of your entire portfolio that determines whether you should invest or not. – Mad FIentist

Not all portfolios operate as efficiently as they could, and not all investments are created equal. Why?

Because there’s only a certain amount of accepted risk you can take before your investment portfolio becomes sub-optimal (i.e., too much risk, not enough return).

Portfolios landing to the right and below the efficient frontier are viewed as inferior because the expected return is too low for the level of risk taken.

The minimum variance portfolio rests where the line starts to curve and risk is at its lowest level as it relates to return. Anything falling on the efficient frontier line above the MVP is considered an optimal choice (i.e., the expected return lines up with the level of risk).

In a nutshell, an efficient portfolio (or a portfolio falling on the efficient frontier) offers the best return you can expect for the degree of volatility you’re taking on. It’s an outgrowth of MPT. Because there’s an infinite number of security combinations producing varying levels of return, the efficient frontier represents the best of those combinations.

One school of thought suggests investors pivot from an efficient portfolio to a minimum variance portfolio as they near retirement.

Highly-diversified portfolios tend to hold a place along the efficient frontier.

Minimum Variance Portfolios In Action

It gets complicated, but for this example, we’ll keep it simple.

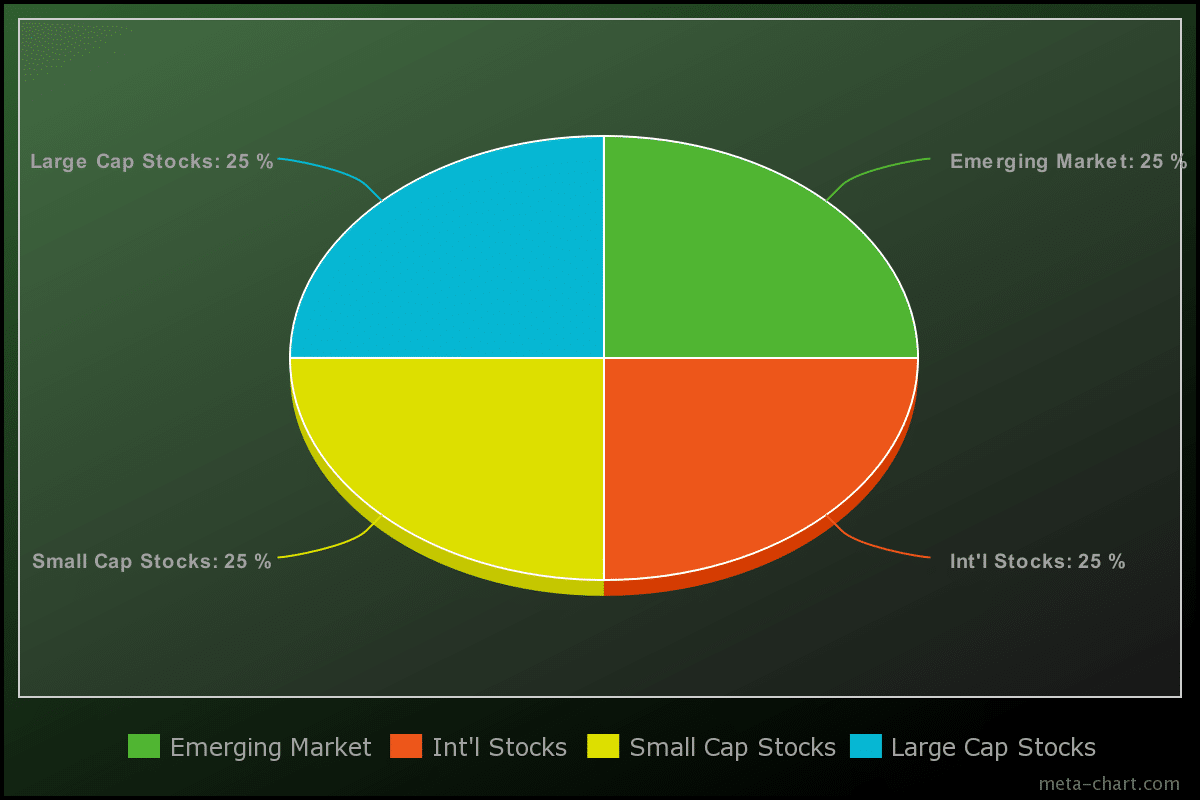

Imagine you’ve got a single asset class. Let’s say it’s stock in an emerging market index fund. That index fund alone is highly volatile. 100% invested in emerging market stocks is a risky play.

But if you throw in small-cap, total international, and large-cap stocks, (split evenly four ways) you’ve reduced your risk through diversification.

For example, a small-cap and an international stock won’t always move in sync with each other. If international goes down, the other three won’t be as affected. You’ve just added four volatile, low-correlated investments to your portfolio while lowering risk.

An alternative would be to hold a percentage of bonds in your portfolio.

Remember, the key ingredient to a MVP is holding investments with a low-correlation to each other.

Larry Swedroe uses this strategy in the Larry Portfolio allocating 70% of it to bonds while only 30% goes to volatile equity funds.

This portfolio's goal is to be both high performance and low volatility. It achieves its performance by tilting your portfolio to higher-risk stocks that are underpriced. Its low volatility is due to only holding 30% in stocks while 70% goes to bonds.

Another example could be Harry Browne’s Permanent Portfolio. His approach holds four asset classes that respond to market fluctuations in specific ways.

The Permanent Portfolio (PP) is a portfolio evenly split between stocks, bonds, gold, and cash. It’s best suited for risk-averse investors wanting to minimize losses while still receiving modest returns.

This strategy gets more complicated when you focus on individual stocks in specific sectors, buying on margin.

If you’d like to learn more about this topic, here’s a curated list of other investment strategies and model portfolios we’ve covered:

- Coffeehouse Portfolio

- Ivy Portfolio

- Swensen Portfolio

- Golden Butterfly

- All Weather Portfolio

- Lazy Portfolio

Minimum Variance and Risk Parity

Another way to maximize returns is through leverage. Rather than overweight your portfolio with risky assets, an alternative is to weight your portfolio with safer securities.

Now, you can borrow against your low volatility portfolio to maximize returns using Risk Parity. Billionaire hedge fund investor and manager Ray Dalio coined the investment strategy at his firm, Bridgewater.

It says that riskier assets are overpriced with sub-par returns. In a nutshell, you’re accepting higher volatility for less reward. It also means that safer assets will get you superior returns considering the lower level of risk assumed.

You’re borrowing against your portfolio and investing heavier in low-risk securities. By increasing leverage in a minimum variance portfolio, you can potentially raise your earnings without using risky assets.

The Sharpe Ratio: A Risk Management Tool

Measuring Return and Risk

It makes sense to start from a risk-based approach. Past performance doesn’t guarantee future results. However, financial analysts still wanted to make sense of it all. If only there were a way to combine an investment’s risk and return into one statistic.

Introducing the Sharpe Ratio.

We already know that the standard deviation is a way to measure portfolio volatility. Then along came William Sharpe. He discovered a calculation that accounts for both risk and return, aptly named The Sharpe Ratio.

He’s also a Nobel Prize recipient for his work in the creation of the capital asset pricing model (CAPM) which says there are two types of risk:

- Systematic (Market) risk can’t be diversified away (e.g., the day-to-day gyrations of stock prices due to interest rates, inflation, etc.)

- Unsystematic (Specific) risk are factors unique to a particular company and can be diversified away (e.g., a company’s CEO is charged with doctoring the books and goes out of business, natural disasters, labor strikes, etc.)

Takeaway: Market risk can’t be removed through diversification and is the type of risk investors are rewarded for.

Math

The Sharpe Ratio in action looks like this:

Risk ⁄ Return

For example, if you have an investment with an expected return of .10 and a standard deviation of .30, you’d have this:

.10/.30 = .33

Now imagine there’s a second investment with the same expected return of 10%, but a standard deviation of .50:

.10/.50 = .20

The investment with the higher Sharpe Ratio wins because you’re getting the same return for less risk.

What makes the Sharpe Ratio special is that it’s not relative to a benchmark (like measuring risk compared to a market index) – it’s absolute. It tells you how much risk you’re shouldering for the return.

Investments with a higher Sharpe Ratio are preferred because you’re assuming less risk for reward. Portfolios that offer the same returns with more risk or less return for the same risk are inefficient and aren’t found on the efficient frontier.

Final Thoughts

Portfolio optimization gets complicated fast. Dizzying minimum variance portfolios aside, your asset allocation matters most. Constructing your portfolio with a few low-cost index funds (or ETFs) and embracing a buy-and-hold strategy will lead you to long-term wealth with fewer headaches.

This lies at the heart of minimum variance: a lower-risk investment portfolio thanks to diversification and low (or non) correlated securities.

Investors chasing higher returns through advanced strategies with little understanding is when they run into trouble.

Keep it simple. Invest across your basic asset classes of stocks, bonds, and cash. You’ll still have your minimum variance portfolio, just a simpler one. And the simpler solution is always best.

But if you’re ready to jump into the deep end of the pool, go for it! If done right, it can potentially enhance your returns.