- The difference between an Index Fund (ETF) and a Mutual Fund

- 1. Vanguard Total Stock Market (ETF) – VTI

- 2. Vanguard Total Bond Market Index (ETF) – BND

- 3. Vanguard Total International Stock Index Fund – VXUS

- 4. Vanguard Small-Cap Index ETF – VB

- 5. Vanguard REIT Index Fund – VNQ

- 6. Vanguard Social Index Fund Admiral Shares – VFTAX

- 7. Vanguard Target Retirement 2050 Fund Investor Shares – VFIFX

- 8. Vanguard Growth Index Fund Admiral Shares – VIGAX

- 9. Vanguard 500 Index Fund Admiral Shares -VFIAX

- Vanguard Select Funds

Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

We absolutely champion Vanguard, though we recognize that diving into its funds might seem more intricate than your typical Robo Advisor experience. Don’t fret! We’re here to guide you through our top Vanguard fund picks, striking a balance between stellar performance and cost-effectiveness.

Before jumping in, it’s important to mention why we focus so heavily on fees here. Due to their exponential nature, fees of just 1% can cause you to lose up to 25% of your earnings. That’s pretty horrendous and often what turns investors on to Vanguard in the first place.

I also highly suggest you check the fees on your accounts via the free Empower’s fee analyzer. It runs simulations and pinpoints all of the overly fee-hungry funds across your accounts – retirement or otherwise.

We’ll delve into the world of Vanguard funds, identifying the top eight choices that will provide you with the diversification necessary to withstand market fluctuations and maximize your returns. Whether you’re a seasoned investor or a beginner seeking to build a solid foundation, these Vanguard funds will offer you the perfect blend of assets to ensure a well-rounded and prosperous financial future.

Let’s embark on this journey together and unlock the full potential of your portfolio!

If you’re looking for a deeper dive into our logic as well as some colorful commentary, then check out the podcast episode we did on this:

The difference between an Index Fund (ETF) and a Mutual Fund

First, let’s quickly discuss an Index Fund (ETF or exchange-traded fund) and a mutual fund. Who better to ask than Vanguard themselves?

An ETF is a collection (or “basket”) of tens, hundreds, or sometimes thousands of stocks or bonds in a single fund. If you’ve ever owned a mutual fund—particularly an index fund—then owning an ETF will feel familiar because it has the same built-in diversification and low costs.

Source: Vanguard

A Mutual Fund is very similar to an ETF with one crucial difference:

You can set up automatic investments and withdrawals into and out of mutual funds based on your preferences.

Source: Vanguard on ETF vs. Mutual Fund

In other words, if you are a beginner or want to automate your investing, then you use a Mutual Fund. If you want cheaper fees over time and don’t mind making contributions every month, then you should choose an ETF. I use ETFs because I don’t mind making investments manually, and fees are the worst.

We often get asked how much we need to invest in Vanguard. If you’re investing in a Vanguard ETF, it will cost you the price of one share (Vanguard ETFs typically cost between $50 to several hundred dollars. If you’re investing in a Vanguard Mutual Fund, then the minimum initial investment is between $1,000 and $3,000 (depending on the fund).

1. Vanguard Total Stock Market (ETF) – VTI

VTI | Vanguard | MorningStar | Fee: 0.03% |

Vanguard’s premier ETF, VTI, stands out as a crown jewel, representing a share class of the Vanguard Total Stock Market Index Fund. This ETF encompasses Large, Mid, and Small cap U.S. companies, mirroring the performance of the CRSP US Total Market Index.

It boasts one of the lowest expense ratios at 0.03%, achieved through its passive management approach and efficient automation, minimizing active management costs.

Often, when people mention that they invested in Vanguard, they refer to the Vanguard Total Stock Market ETF (VTI). Since over 90% of fund managers can’t beat this fund after fees, skepticism is warranted if someone claims they can perform better. Even Warren Buffett agrees with this approach. However, while VTI is impressive, it’s not all-encompassing, and it would be prudent to diversify your investments beyond just this fund.

The minimum investment in the Vanguard Total Stock Market ETF (VTI) is the price of one share.

VTI is a popular and versatile ETF, its inclusion in the All-Weather Portfolio (by Ray Dalio) is a modern adaptation .

This portfolio's single goal is to make money in all market conditions regardless of interest rates, deflation, what new pandemic is threatening our shores, or who the POTUS is. It does this by focusing on growth and inflation cycles.

Fiscal flexibility that’s funny, free and delivered weekly.

2. Vanguard Total Bond Market Index (ETF) – BND

BND | Vanguard | MorningStar | Fee: 0.035% |

Any well-balanced portfolio has bonds in it. They’re much less sexy than stocks but are also much less risky. When you’re young, 10% of your portfolio should be in something similar to BND, and as you get older, you’ll increase that percentage significantly.

The Vanguard Total Bond Market ETF (BND) tracks the Bloomberg Barclays U.S. Aggregate Float Adjusted Bond Index, providing broad exposure to the U.S. investment-grade bond market.

The bonds within this fund are of investment-grade quality, making it suitable for a medium to long-term holding strategy given its composition.

This quality and diversification across different types of bonds make BND an appropriate option for investors seeking stability and steady income over the medium to long term.

Since bonds often perform better when the U.S. stock market is doing poorly, including them in your investment portfolio can provide stability.

The Coffeehouse Portfolio is a simple and effective investment strategy that balances 60% stocks and 40% bonds to provide steady returns with minimal effort.

This portfolio takes its name from the idea that it’s such a straightforward investing strategy you could create it while sitting in a coffeehouse. It focuses on diversification and keeping things simple - it's also exceptionally conservative.

3. Vanguard Total International Stock Index Fund – VXUS

VXUS | Vanguard | MorningStar | Fee: 0.08% |

Similar to our #1 choice, VTI, this fund provides exposure to a broad range of stocks in developed and emerging markets outside the US. Its large size and low expense ratio make it a popular choice for investors seeking international diversification.

The Vanguard Total International Stock ETF (VXUS) is considered a moderately volatile fund, so we keep it as a small portion of our portfolio to help offset our heavy US exposure.

VXUS has a market capitalization of $72 billion (as of June 2024). The strategy of this ETF can found in the The Coffeehouse Portfolio fas well as the Ivy Portfolio.

This portfolio attempts to diversify your money by dividing it into stocks, bonds, commodities, and real estate in a way that mirrors the Ivy League endowment funds. It doesn't attempt to mirror every move the endowment fund makes.

4. Vanguard Small-Cap Index ETF – VB

VB | Vanguard | MorningStar | Fee: 0.05% |

A small-cap is generally a company with a market capitalization of between $300 million and $2 billion. This ETF invests in a diversified basket of US small-capitalization stocks. Small-cap stocks can offer potentially higher growth but also carry greater risk compared to larger, more established companies..

Also, again, this one’s the riskiest of the bunch. We wouldn’t recommend making this one more than 10% of the total amount you invest in your Vanguard investments.

VB is most known for its inclusion in the Larry Portfolio. The Larry Portfolio typically allocates a substantial portion to small-cap value stocks, recognizing their potential for higher long-term returns despite their increased short-term volatility

This portfolio's goal is to be both high performance and low volatility. It achieves its performance by tilting your portfolio to higher-risk stocks that are underpriced. Its low volatility is due to only holding 30% in stocks while 70% goes to bonds.

5. Vanguard REIT Index Fund – VNQ

VNQ | Vanguard | MorningStar | Fee: 0.12% |

Buying and owning rental properties can be great when it diversifies your personal finances but can be a lot of work; this REIT seeks to solve that. Instead, invest in a REIT and take rental profit and liquidity. This index fund is not just a REIT but a fund of many REITs, so you’re heavily diversified in the rental game.

The Coffeehouse Portfolio includes a 10% REIT component and the Ivy Portfolio a Real Estate component as well.

Note: You won’t find much yield here, which is a bit of a drag considering real estate is a stable income play. As a replacement for the income portion of your portfolio, we recommend Fundrise.

Diversify into income-producing real estate without the dramatics of actual tenants. Fundrise eREITs are a diverse family of funds, each of which pursues a focused real estate investment strategy.

Disclosure: When you sign up with this link, we earn a commission. All opinions are our own. I am an investor with Fundrise.

Compared to VGSLX, Fundrise sticks to mid-size deals overlooked by large funds and, as a result, may provide a higher return. You can also opt to concentrate on income or appreciation-focused funds.

6. Vanguard Social Index Fund Admiral Shares – VFTAX

VFTSX | Vanguard | MorningStar | Fee: 0.14% |

VFTAX (Vanguard FTSE Social Index Fund Admiral Shares) applies a Socially Responsible Investing (SRI) lens, focusing on companies with strong environmental, social, and governance practices. It includes firms like Apple, Microsoft, and Google (Alphabet), which are known for initiatives such as renewable energy and gender pay equality.

Tesla may be included for its eco-friendly focus, but its inclusion depends on meeting all SRI criteria. Unlike VTI (Vanguard Total Stock Market ETF), VFTAX excludes companies that fail to meet its SRI standards

While VFTAX invests in companies that focus on reducing energy costs and attracting top talent, this does not mean it consistently outperforms VTI. The performance of these funds varies based on market conditions and the specific companies included. VFTAX may do better in some periods, but not always.

The SRI Golden Butterfly Portfolio offers a more diversified approach aimed at balancing risk and return across multiple asset classes.

This portfolio is a socially responsible version of the Permanent Portfolio with one additional asset class. This is done to incorporate some of the characteristics of a few other notable lazy portfolios.

Note: However, you will notice that we use JUST by Goldman Sachs in the portfolio. That’s because it’s an ETF, so that we can buy it on the open market, VFTAX, you need to buy directly from Vanguard.

7. Vanguard Target Retirement 2050 Fund Investor Shares – VFIFX

VFIFX | Vanguard | MorningStar | Current Fee: 0.08% (January 2024) |

This fund is a lifecycle fund, so it starts with most of the money invested in stocks and slowly tilts its asset allocation into bonds over time. The point is you take on risk now while you’re young and gradually reduce risk as you reach retirement age, so big market swings don’t wipe out your retirement money.

While this fund isn’t Vanguard’s best regarding the fee, it covers a much-needed gap in most people’s portfolios. As you know, we’re big fans of buy and hold, and this fund fits in there perfectly.

The number in the fund name, for example, “2050”, corresponds to your “typical” retirement date – usually, that’s when you’re 65. We often find ourselves picking funds with dates well past the typical retirement age, so we get something a bit more growth-focused early on, which is why this is the best pick for most people.

8. Vanguard Growth Index Fund Admiral Shares – VIGAX

VIGAX | Vanguard | MorningStar | Fee: 0.05% (May 2024 |

VIGAX focuses on high-growth companies, which can provide substantial returns but come with higher risk. The fund tracks an index, which results in a buy-and-hold style investment by default. While it doesn’t actively select and hold individual stocks for long periods based on stability, the underlying index methodology ensures relatively low turnover and a focus on long-term growth.

9. Vanguard 500 Index Fund Admiral Shares -VFIAX

VFIAX | Vanguard | Morningstar | Fee: 0.04% (April 2024) |

Pioneering the market as the first index fund tailored for individual investors, the 500 Index Fund offers an affordable gateway to the vast U.S. equity landscape. By investing here, you tap into the potential of 500 of the U.S.’s leading enterprises across a spectrum of industries, ensuring diverse exposure. Given its breadth within the large-cap segment, this fund deserves a pivotal spot in your investment portfolio.

Vanguard Fund Tracking and Monitoring

Manage your cash and optimize your investments in one place. With Empower, you can analyze your 401k to diversify your holdings better and reduce fees. I had no idea I was paying over 1% of my assets in fees every year, but with their help, I was able to get it down below 0.3%.

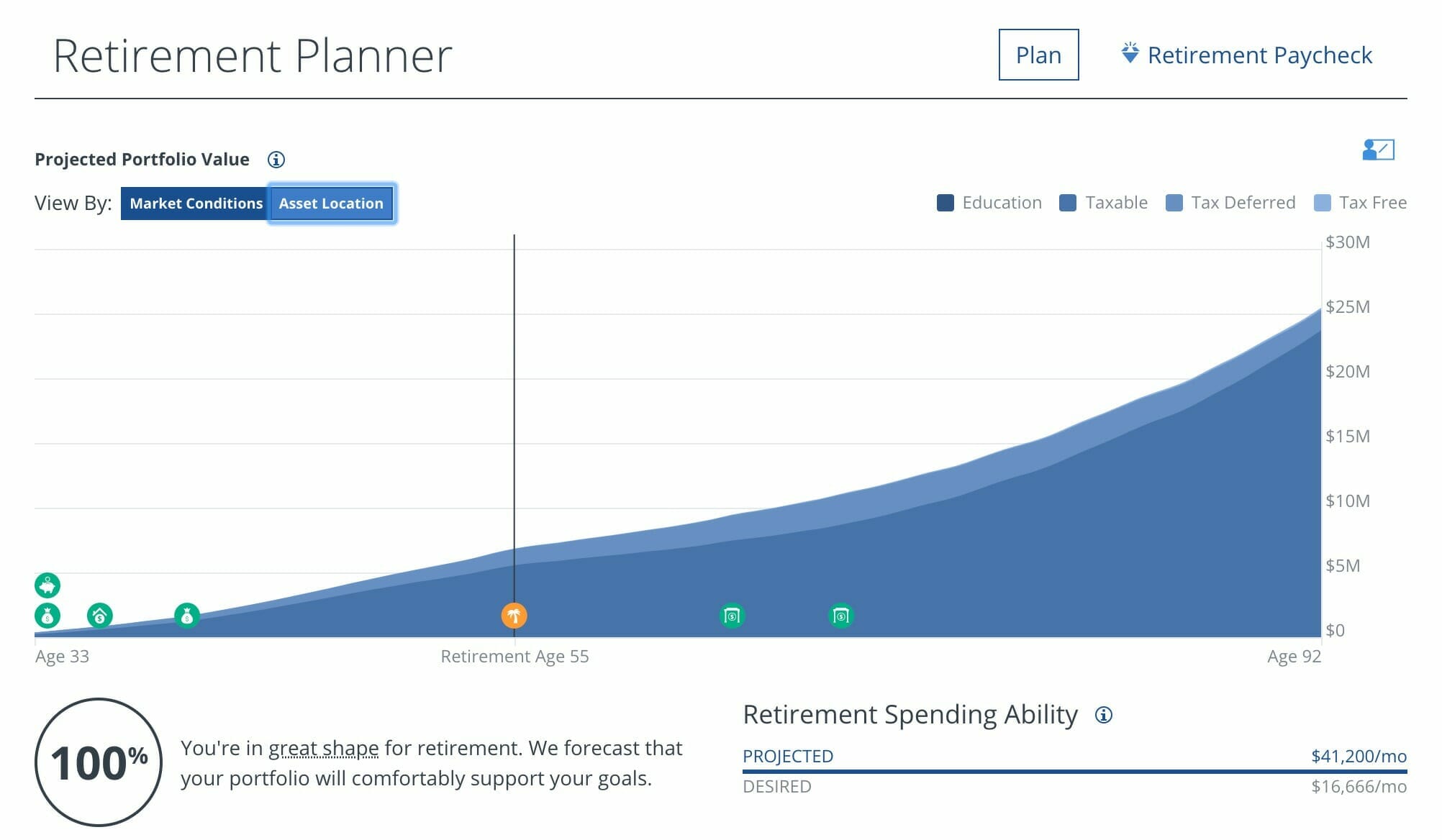

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

Once you have all of your brokerage accounts linked, you can also leverage their Retirement Planner to plot out exactly what your retirement would look like. Using a Monte Carlo simulation, they determine how likely it is that you’ll reach the level of income in retirement that you’re hoping for.

Vanguard Select Funds

Vanguard created a shortlist of their funds called the Vanguard Select Funds. One exciting thing about the list is how they determine what funds get on it:

The Vanguard Portfolio Review Department evaluates our low-cost fund lineup on an ongoing basis to determine the funds selected. This in-house team of investment professionals evaluates the funds using a proprietary screening process and criteria. – Vanguard Select Funds

I will say that a lot of their most expensive funds (where they can make the most money) are on that list, like the Windsor II, whose fee is 0.34% or the Vanguard Alternative Strategies Fund (with an expense ratio of 0.51%).

It’s worth mentioning that most of the funds on our list are on their list, with the exception that we excluded the high-cost funds. There are a billion studies that show there is no correlation between a high cost and a high return. That’s why we focus on “shooting for the average” on the show, easily the best bang for your buck given the risk.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.