- Do I Need to Roth?

- Roth Account Income Limits

- Do You Qualify for a Roth IRA?

- Contribution Limits

- Rules for Withdrawing from a Roth IRA

- The 5-Year Rule

- You’ve Held Your Account for Five Years or Longer

- You’ve Held Your Account Five Years or Less

- Backdoor Roth

- Roth IRA Contribution Calculator

- Roth IRA Changes in 2019

- Final Thoughts

I’m sure you’ll agree with me when I say learning the rules about a Roth IRA retirement account is something you’d never wish upon your most hated enemy. It’s boring. And it’s even less fun when the rewards you’ll reap are 20, 30, or 40 years away.

In fact, if you told me 10 years ago (hell, even five years ago) that I’d be writing about the badassity of retirement accounts like the Roth IRA, I’d of smiled, knocked back the remaining contents of my La Fin Du Monde ale and politely told you to f!@# off.

However, after the curtain was pulled back, it was revealed to me that it was not as hard as I thought. While terms like contribution limits, required minimum distributions, and tax-deductible aren’t as rock ‘n roll sexy as when Led Zeppelin performs “A Whole Lotta Love,” they’re not the snooze fest I once thought they were either.

They’re quite enticing in an “I’m seizing control of my financial independence journey to have the freedom to do what I want, when I want it,” kind of way.

“Think winter in the summer.” – Jim Rohn

I’m going to show you what the Roth IRA rules are and how you can optimize them towards your retirement savings. Are you ready to tap into your inner financial badass? Read on!

Do I Need to Roth?

A Roth IRA account is a powerful wealth-building tool to grow your retirement savings. It has many benefits like tax-free withdrawals, no RMDs, and can be gifted to a family member after you pass away.

What’s even sweeter about the Roth is that you’ve already paid income taxes on this money, so it’s yours to withdraw tax-free in retirement.

However, many Americans don’t even save enough to reap the benefits of all the Roth has to offer.

To play the game, you gotta know the rules.

Roth Account Income Limits

Contributing to your Roth, there are specific income requirements you must meet. If you’re a single filer and your modified adjusted gross income (MAGI) is $120,000 or less, you can contribute the full amount.

If you’re earning greater than $120,000 but less than $135,000, you’re only allowed to make a partial contribution. This incremental phase-out ends once you go above $135,000. If you’re earning more than that, you’re shit outta luck unless you use a Roth conversion. We’ll get to that in a bit.

If you’re married and filing jointly (or a widow(er), earning $189,000 or less you can contribute the full amount. If your earnings are greater than $189,000 but less than $199,000, you may add a partial amount. Once you cross the $199,000 threshold, you’re SOL once again.

If you find yourself earning more over time and your income exceeds the contribution limit, you can still keep your Roth. However, you can’t fund it anymore.

Fiscal flexibility that’s funny, free and delivered weekly.

Do You Qualify for a Roth IRA?

If you’re wondering who can contribute to a Roth the answer is: Anyone. Anyone can contribute to a Roth IRA as long as you’ve earned income. There is no age requirement.

Children and adults alike can set up a Roth and start funding their retirement plan immediately. As long as your MAGI falls within limits set by Uncle Sam you’re golden.

Also, a Roth IRA is an excellent idea if you think you’ll be in a higher tax bracket when you’re older.

Contribution Limits

The IRS determines annual contribution limits. In 2018, that amount of money is $5,500. However, if you’re 50 years or older, the IRS lets you play catch-up. You’re allowed to put an extra $1,000 into your account bringing your total to $6,500 per year.

Your contribution amounts aren’t tax deductible. Unlike a Traditional IRA, where you can deduct your contributions, a Roth IRA account doesn’t let you.

For example, if you earn $50,000 and you contribute the full amount of $5,500 to your Traditional IRA, the IRS will only tax your earnings up to $44,500.

It’s a different story with a Roth.

Using the above example, you contribute $5,500 to your Roth, and Uncle Sam will tax you on all the money you made that year – $50,000 in this example. However, when you withdraw your money in retirement, it’s yours tax-free.

Also, you can’t contribute more than you earn. For example, if you’re young, working part-time, and living with your parents, your earnings for that year might only be $4,500. In that situation, you’d just be allowed to contribute up to $4,500 – not the $5,500 limit.

Rules for Withdrawing from a Roth IRA

First, the easy bit.

If you’re 59 ½ or older and your account’s been open for at least five years, you can withdraw as much as you want.

You can withdraw your Roth contributions anytime without facing taxes or penalties. You’ve already paid taxes on that money. They’re yours if you decide you need them in the future.

Withdrawing earnings gets a bit tricky.

The 5-Year Rule

The 5-year rule means that to avoid getting an early withdrawal penalty on your earnings, you must be 59 ½ or older AND have opened your account for at least five years.

This rule applies to your earnings only. Remember, Roth IRA contributions can be withdrawn anytime without penalty. You’ve already paid taxes on that money.

The five-year rule on your earnings starts on January 1st of the calendar year you made your contributions. Fun fact about adding money: you can make them up to April 15th the following year.

For example, if you make your first contribution in March 2019 but designate it for the 2018 tax season, the five-year rule starts January 1st, 2018. Meaning you’d only have to wait until 2024 to receive tax-free withdrawals. Hell yeah!

You’ve Held Your Account for Five Years or Longer

You can avoid paying any taxes or penalties upon withdrawal by meeting any of the below criteria:

- Purchasing your first home (up to $10,000-lifetime maximum)

- Your age is at least 59 ½

- You’re disabled, or you die, and the money is used on behalf of your estate or beneficiary

You’ve Held Your Account Five Years or Less

If you’ve held your account for less than five years, you’re still subject to paying taxes, but you can avoid the 10% early withdrawal fee on earnings if:

- You’re paying for your first home (up to $10,000 maximum)

- You’re 59 ½ or older

- You become disabled or die (money’s drawn down from your beneficiary in this case)

- Your money is paying for qualified educational or medical expenses

- You’re experiencing financial hardship and start taking substantially equal periodic payments.

The reason you’re subject to paying taxes on your earnings is that you haven’t met the minimum holding requirement set by the IRS. Holding your account for at least five years is how you avoid this.

Unlike a Traditional IRA (where you’ve got to take an RMD when you’re 70), your Roth lets you let it ride. There are no required minimum distributions. Your money can sit there for as long as you like.

You can even gift it to a family member when you pass away. Also, you’re allowed to continue contributing as long as you want.

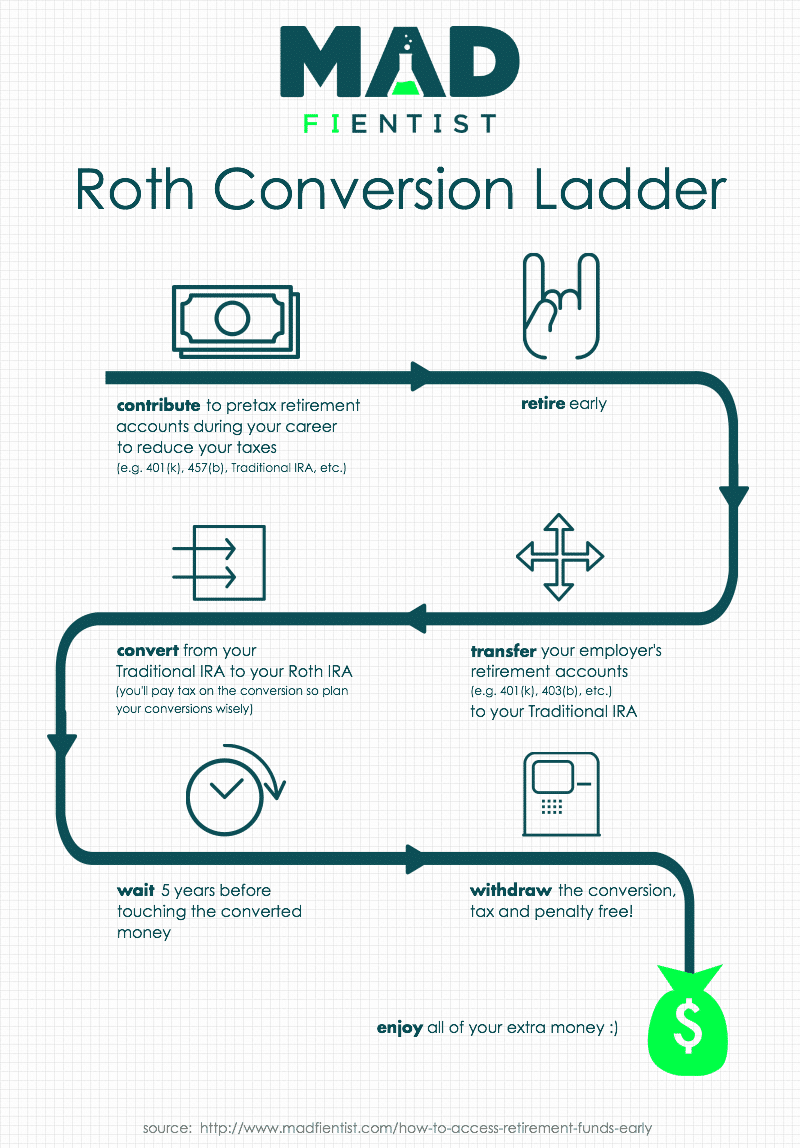

Backdoor Roth

Earn too much money to contribute to a Roth? If your income is higher than the limits allowed and you’re not able to make contributions to a Roth, you can do a Roth conversion, also called a backdoor Roth.

A Roth IRA conversion is a winning idea if you’re income exceeds the limits set by Uncle Sam.

You can set up a Roth conversion by contributing money to a Traditional IRA because there’s no limit on what you can earn. Once there, you’d sell shares from your Traditional IRA account and roll that money into your Roth.

The backdoor Roth is a significant tax optimization strategy for high earners who want to get their hands on some tax-free money down the road.

You’ll still pay taxes on the conversion but what’s left over is yours. It’s perfectly legal too. Check with your tax advisor to walk you through it.

Roth IRA Contribution Calculator

If you’re like me and math scares the bejesus out of you, there are plenty of handy tools online to help you determine how much you can contribute.

Here’s one I found that’s simple to use. All you do is plug in your age, contribution tax year, tax filing status, and modified adjusted gross income. The calculator does the heavy lifting for you.

Don’t let math get the best of you. Math never lies. Always run the numbers.

Tweet ThisRoth IRA Changes in 2019

As 2018 comes to an end, there have been a few changes for 2019 – The amount you’re allowed to contribute increased to $6,000 ($5,500 in 2018). If you’re 50 or over, it’s $7,000.

Your contribution amount depends on your tax filing status. You still won’t receive a tax deduction on your Roth IRA contributions but is still a fantastic investment vehicle. The single-filer income limit rose to $122,000 ($120,000 in 2018).

You can make the maximum contribution if it’s this number or below. The incremental phase-out runs between $122,000 and caps at $137,000. Above $137,000 and you’re ineligible to make contributions.

For married couples filing jointly with a MAGI of $193,000 or less, you’re allowed the maximum contribution. Between $193,000 and $203,000, you can contribute a partial amount. Anything above $203,000 and you’re ineligible.

Final Thoughts

A Roth IRA is a fabulous wealth-generating tool that’s easy to set up. Your earnings grow tax-free, and you can fund it with anything from stocks to bonds to real estate. You can open an account lickety-split online.

The government wants you to invest your money which is why they created tax-advantaged accounts like IRAs.

Uncle Sam even lets you dip into your Roth for special occasions like a first-time home purchase, qualified education expenses, or drawing down your contributions in case of an emergency.

However, having an emergency fund in place would be a better idea (that way you don’t lose the power of compounding that’s working for your Roth).

Knowing the rules puts you in a strong financial position, and better prepares you for the obstacles that life will inevitably throw at you along the way. The sooner you start, the more you’ll have. Imagine that.