401k fees can cost tens of thousands of dollars in retirement savings over your lifetime. Hidden fees. Service fees. Registration fees. It doesn’t seem like much, but enough of them over time will consume your bottom line. Learn what the different fees are in your 401k and how to avoid them.

We accept fees as a fact of life. However, there’s one place where you can reign them in – retirement savings plans like a 401k or an IRA. This is also where controlling your fees can have the most impact on your future wealth. Why?

Retirement plan fees often rise with your savings due to percentage-based charges. Some plans may also have flat fees.

This means that the more you make, the more they make from your fees. This is good for them but not so much for you.

Types of 401k Fees

401k fees can be summed up into two broad categories: Investment and administrative. The best way to differentiate these fees is to realize that your 401k account and the investments within your 401k are two different things. The two roles are usually not held by the same organization.

Investment Fees

This covers the cost of maintaining the investments that are bought and sold in your 401k account. This includes sales commissions, marketing, and distribution costs that are incurred by the mutual fund companies (also known as 12b-1 fees).

Actively-managed mutual funds having substantial buying, selling, and decision-making to create and maintain the fund, typically charge more. These are covered under a fund’s management fees.

If you were to trade individual stocks, you would need to invest your time in researching stocks and balancing your portfolio for the right asset mix.

This is why index funds in your 401k carry lower fees. If all you’re doing is buying every stock in the S&P 500, then you get to punch the clock early and go home.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

Administration Fees

Think of this as the cost of maintaining the 401k account itself. This could be for operating expenses such as record keeping or writing fee disclosure documents. That person you call when you are confused about something on your statement has to be paid.

Unlike investment fees, administrative fees may not be as visible as you’d like. Usually the company that’s providing you with the 401k account (i.e. your employer) pays these fees.

Administrative fees in your 401k plan help cover the costs of recordkeeping, plan administration, and other services. These fees are usually deducted as a percentage of your total account value, not by directly removing shares from your holdings.

Spotting High Fees in Your 401k

Thankfully you don’t have to track down all of these fees individually. While the administration fees may not be as transparent to the average account holder, they tend to be less significant than the investment fees.

There’s not much you can do about the administration fees short of complaining to your HR department. And that’s usually more trouble than it’s worth.

Investment fees can significantly impact your retirement savings. While you might not see a specific line item for them on your regular statements, you can find them in the annual plan fee disclosure documents or within the prospectuses of the individual investment options offered in your 401k. Look for the expense ratio, which expresses the investment fees as a percentage of assets under management.

Terms to look for include expense ratio, loads, and management costs. They’re likely to be expressed as a percentage of the investment assets.

And though the percentages seem small (usually between 0.5% to 2%), due to the miracle of negative compounding interest, this can be quite significant over time depending on your investment growth.

There are also websites out there that spell out the fees associated with any given publicly traded fund or ETF. Empower has a feature where you can give them access to your account and they will track down the fees you’re paying and summarize it all in one graphic. More on that later.

Fiscal flexibility that’s funny, free and delivered weekly.

How Fees Affect Your Returns

One percent of a thousand dollars is only 10 bucks. So when you’re starting out, it doesn’t seem like much. But one percent of $200,000 is $2,000 and that’s in annual fees.

Not only that, but if you take the effects of negative compounding interest, by the time you’re ready for retirement it will be a healthy chunk of your 401k balance. If you have enough of them and with enough time, those fees do add up.

How You Can Reduce 401k Fees

Thankfully, you have some choices to minimize the impact on your retirement funds. Investment fees vary significantly between funds. And though your 401k may not have a plethora of investment options, I’d bet that there are some relatively low-cost funds there.

If you want to do the research yourself, you can. The fees for your 401k funds are likely readily available either on your plan’s website or in other documentation. The problem is that you don’t get a sense of how reducing these fees will impact your bottom line. I’ve found a tool from Empower that helped me do just that.

There may be other similar tools out there to the one I’m about to describe, but this is the one I have experience with.

Empower’s Retirement Fee Analyzer

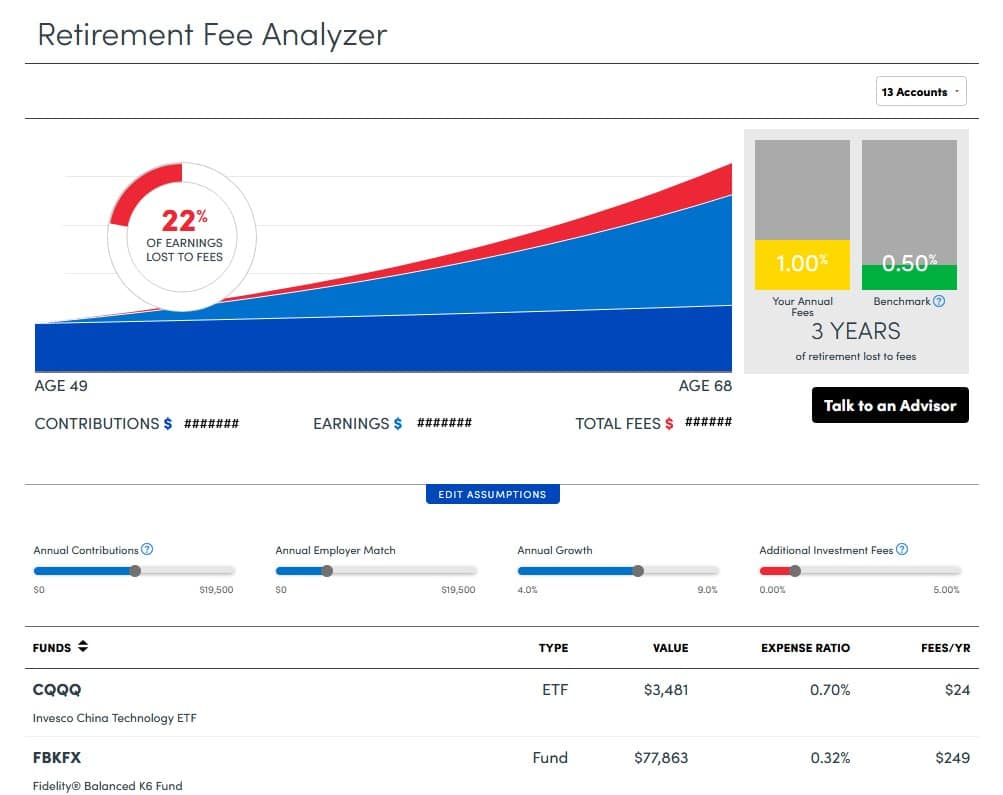

The first step after logging in is to input your account information from the investment company where your 401k is invested. Then it takes the current value of your account, your estimated contribution, and matching rate going forward, and assumptions about future market conditions.

Next, it applies the known fees in the funds within your accounts and produces a graph of the results.

In deep blue are your employer and your contributions, including the current value of the account (because they are not calculating all the previous years of growth).

In lighter blue is the projected earnings of your account without fees. And in red is the effect of your funds’ fees on your earnings.

In a cruel twist of the dagger, they highlight on the graph how much as a percentage of your earnings will be lost to plan fees by the end. In the example above it’s a whopping 22%.

You can edit most of the initial assumptions based on your future outlook with the slider bars beneath the graph. Your results update immediately.

In the above example, I set the annual growth at 7% and adjusted the fees to be a 1% average over all of my accounts. The tool uses the data from your funds to give you “Your Annual Fees” (yellow, depending on severity) along with a “benchmark” (green) of what they think you should be targeting.

It also lists your account’s funds, their expense ratios, and how much annually per fund you are paying in fees.

My Experience Using Their Retirement Planner Tool

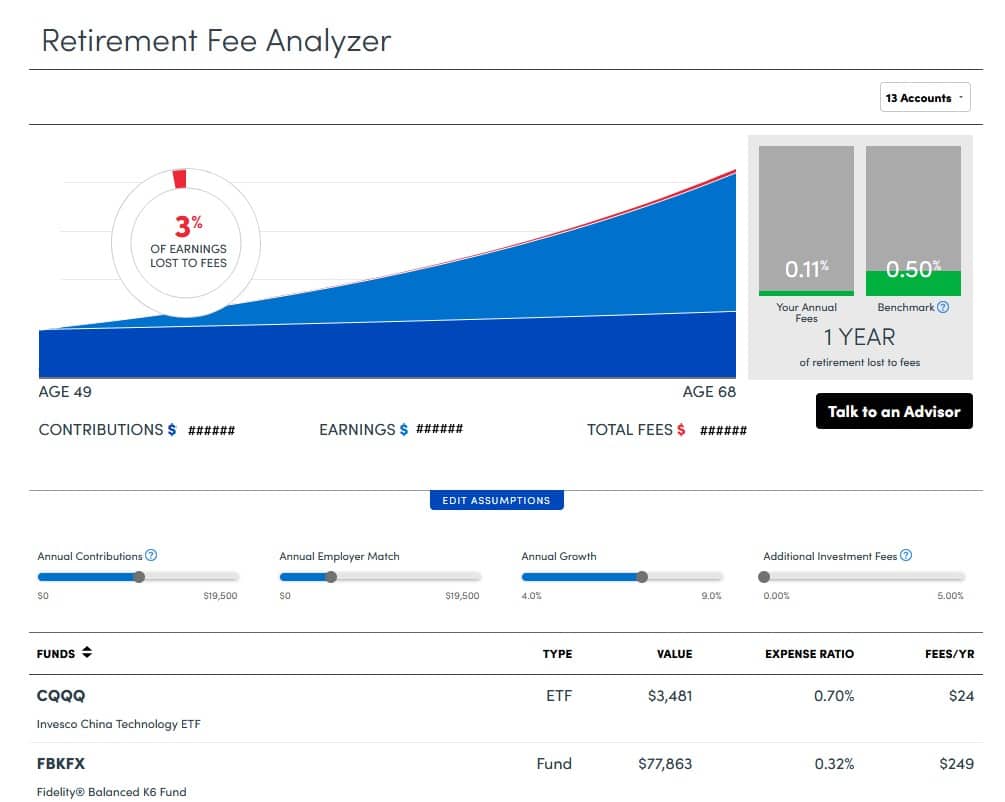

When I used this tool a few years ago, I noticed that I was paying more in fees than I cared for, so I changed my fund mix in my retirement accounts to lower my fees. The chart below reflects the results of those changes.

As you can see, I dropped my effective annual fee rate to a measly 0.11%. It then showed the percentage of earnings lost to fees was now only 3%. Not too shabby.

Reasons to Have a 401k

So what does all this mean? Should you bail on your 401k to avoid them? Absolutely not. 401k plans have so many advantages over other ways of saving for retirement that they vastly outweigh any negative effects of the fees.

Employer Match

If you get a match from your employer for your contributions, fees should be an afterthought. If you’re lucky enough to get a dollar for dollar match to your contributions, even if the fees are double that of other investments, you’re starting out with double contributions and double gains on those contributions. The effective fees you are paying are half that of an equivalent non-matching plan.

Even if your matching is at a lower rate, it cushions the blow of the effect of the fees accordingly. The potential gains on that matching contributions will likely dwarf anything lost in fees. This is why you should always participate in your employer’s 401k up to the match whenever possible – don’t leave free money on the table.

Tax Advantages

401k plans offer significant tax advantages. Contributions are often pre-tax, lowering your taxable income now. In retirement, you may withdraw funds tax-free (Roth 401k) or at a potentially lower tax rate (traditional 401k). However, fees associated with your 401k plan can also impact your long-term savings.

All Investments Have Fees

It’s really hard to avoid fees in doing your own trading as well. Some brokerages offer free trades. Mutual funds and ETFs usually have fees, but there are low-cost options out there too! Index funds can be a budget-friendly way to invest.

401(k)s vs. Savings Accounts

With savings accounts paying a percent or two in interest at most and stock-based investments returning conservatively 6-7% annually, a 1-2% loss from fees is relatively a small price to pay for the increase in potential returns.

401k plans have so many advantages over other ways of saving for retirement that it vastly outweighs any negative effects of the fees.

Tweet ThisThe Takeaway

401k fees can silently chip away at your retirement savings. These fees not only reduce your current balance but also prevent that money from growing through compounding interest over time. The impact can be significant! However, you have some power. By reviewing the investment options within your 401k and choosing lower-cost funds, you can keep more money working for your future.

It’s precisely the reason to use a fee analyzer tool, uncover what you’re paying, and do your best to remove those high-priced funds from your 401k.

Plan for retirement with our free tools today.

- Get your Retirement Readiness Score™ in minutes.

- Run the Recession Simulator to get perspective on today’s market.

- Use Fee Analyzer™ to find hidden fees in your retirement accounts.