There are a few simple rules of thumb you can apply to your personal finances. We know math is hard, but the mathematics of money are really straightforward and can help you make better financial decisions.

Back Pocket Rules

There are dozens and dozens of figures and formulas around anything related to investing but some of us (me) are math deficient and even if we are math savants.

Sitting around calculating things before making any investment decisions is the total opposite our LMM’s Set It And Forget It philosophy. So if you have these few back pocket rules in mind, the mathematics of investing will be less mysterious.

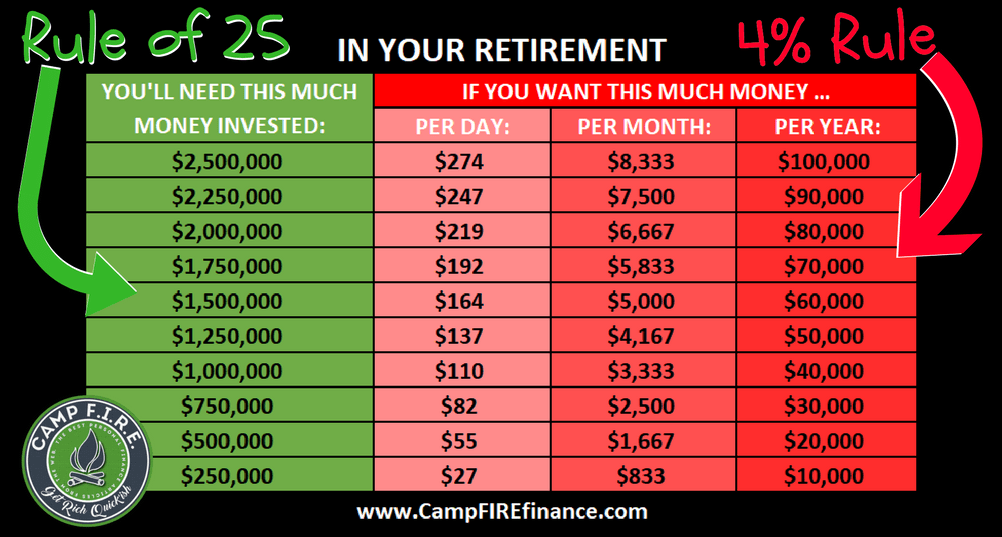

1. The Multiply by 25 Rule

Perhaps the number all of us want to know most is how much money we will need to retire. If you don’t know how to calculate it, you don’t know if you have enough to retire in ten years or fifty years. That’s what the Multiply by 25 Rule can tell us.

First, you’ll need to know how much money you spend a year. You can’t predict the future of course, will you have paid off your home by the time you retire, will you want to move to an area with a higher or lower cost of living than where you currently are? How much more expensive will necessities in the future?

You can’t answer those questions, but it’s good enough to use the number that represents your current yearly expenses. None of these numbers are meant to be an exact science, just a rough, ballpark figure.

Let’s say you need $40,000 to live on per year. Multiply that number by 25. $40,000×25=$1,000,000.

But 25 is based on old data. People are living longer, and health care is more expensive now than it was when this formula was devised.

The new number is 34. $40,000×34=$1,360,000.

There are two other things we need to factor into our number, inflation and how far out retirement is. Your $40,000 today is worth $40,000, but in ten years, it’s worth less because of inflation. You can account for inflation like this:

- 10 years from retirement, multiply by 1.48.

- 15 years from retirement, multiply by 1.8.

- 20 years from retirement, multiply by 2.19.

- 25 years from retirement, multiply by 2.67.

Let’s assume that you want to withdraw $40,000 per year from your retirement portfolio, and you’re 25 years away from retirement.

Multiply $40,000 x 2.67 = $106,800. That number is your inflation adjusted target.

Fiscal flexibility that’s funny, free and delivered weekly.

2. The 4% Rule

The 4% Rule is the inverse of the Multiply by 25 Rule.

Let’s say you are ready to retire, how much you have now is how much you have. So you need a calculation that will tell you how much of that pile of money you can withdraw each year to live on.

Multiply the amount of money you have saved by 4%, that’s how much you can withdraw each year and never run out of money because the gains your remaining investments make will replace that amount each year.

If we use the same numbers from above, we have $1 million, 4% of that is $40,000. That’s how much we can withdraw for our expenses each year.

But like the number 25 in our first calculation, the 4% in this one is out of date. 4% was arrived at using a Monte Carlo simulation in the early 1990’s.

A Monte Carlo simulation models future outcomes by randomly selecting returns, based on the likelihood that they occur – where the “likelihood” is quantified by the average and standard deviation of a normal distribution, which recognizes that extreme returns (to the upside or downside) are less common.

At the time, that 4% could guarantee with 95% certainty that your money would last 25 years. But again, people live longer, and things are more expensive. If you use the 4% rule now, you’ll only have about an 80% guarantee that your money won’t run out.

The new, more conservative number is 3.2% or even better, 3%. So we can either downgrade our lifestyles and live on $30,000 per year, or we need to save a little more than $1.3 million rather than $1 million.

3. The Gordon Equation

You’ve heard various numbers when people talk about how much you can expect to gain on average in the stock market. LMM has always used 7%. But where did we, or anyone else, get that number?

Via the Gordon Equation. And no it has nothing to do with Commissioner Gordon who is awesome or Gary Bettman, the NHL commissioner who sucks and is the reason I am no longer a hockey fan.

The equation looks like this:

S&P 500 dividend yield + about 4.5% = the expected long-term return on stocks.

Current dividend yield = 1.75%

1.75% + 4.5% = 6.25% (current estimated long-term return of stocks)

And by current, we mean the day the podcast was recorded, the number fluctuates. The 4.5% represents the average growth of dividends.

4. Rule of 72, 114, and 144 (Double, Triple, Quadruple)

The Rule of 72 will probably be everyone’s favorite. We tell you to put your money into

But we also tell you not to look at your balance constantly because it will drive you crazy, the ups and downs. Investing is a long con. But you want to know (as much as anyone can know) when you can expect all this investing to pay off!

He who owns the gold makes the rules.

Tweet ThisThat’s what this rule can tell you. The Rule of 72 is a simplified way to determine how long an investment will take to double, given a fixed annual rate of interest.

If the average stock market return is 6.25%, then the rule of 72 tells us that it will take 11.52 years to double our money (72 / 6.25% = 11.52).

So if you put $1,000 in Vanguard and leave it alone for eleven and a half years, you’ll have $2,000.

You can expand this out further too.

Triple: 18.24 years (114 / 6.25)

Quadruple: 23.04 years(144 / 6.2) Twice the amount of time as it took to double our money (11.52 * 2)

This is shorthand, but the actual measurement is insanely close. So when you’re tired of saving money and want to blow it on something fun instead, do these calculations to cheer yourself up and give you the incentive to stay the course.

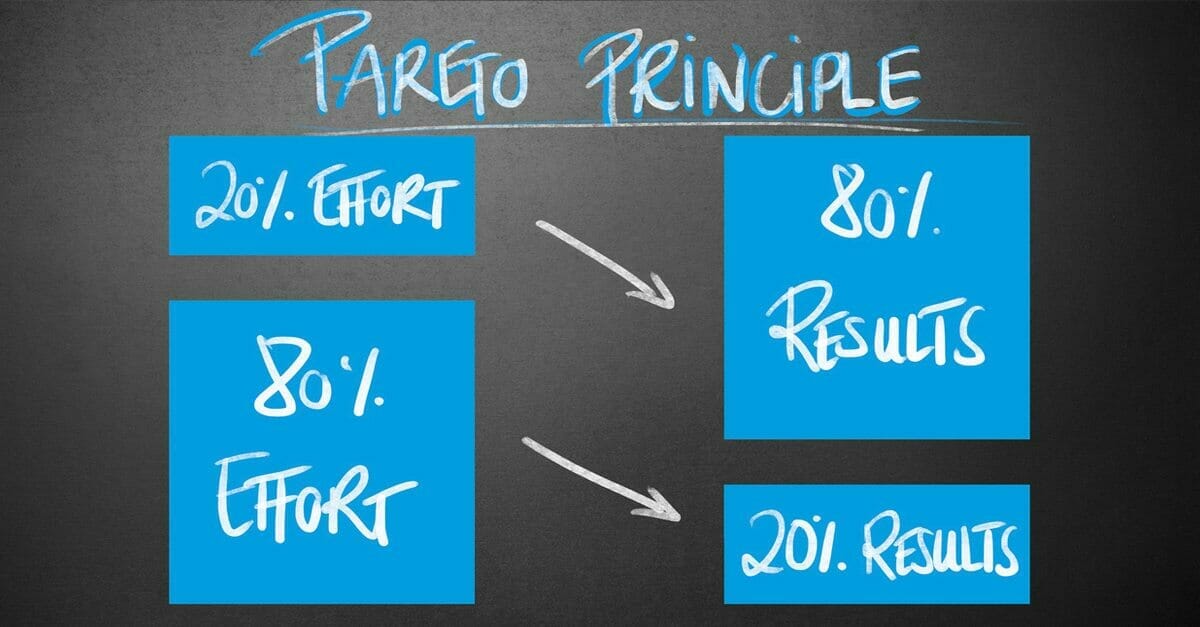

5. 80 / 20 Rule (The Pareto Principle)

Of all these calculations, this is probably the one most of us are familiar with. For many events, roughly 80% of the effects come from 20% of the causes.

You have 100 clients, but 20 of them take up 80% of your time. Roughly 80% of your returns will come from 20% of your investments. 80% of your sales come from 20% of your clients.

What does that mean for investing? For most of us, it means we should avoid picking individual stocks because it’s unlikely that we’re going to pick a whole basket full that is going to give us that 80%.

When we invest with a

Bonus Rule!

We talk a lot about investing in rental property, and we get a lot of emails asking about it, so we’re throwing in a bonus rule that will help you figure out if a potential property is a good investment. The rule is the 1% Rule.

If the monthly rent on a home is 1% (or more) of the purchase price, it’s a money maker. If the house costs $100,000 and you can charge $1,000 a month, shortlist it.

Like Malibu Stacey Said:

“Math is hard.”

Boring too. But the mathematics of investing are not hard and can help you make better financial decisions. When you use these straightforward formulas, you can answer a lot of the questions that make investing seem mysterious. Because there is no mystery about how to get rich, by investing.

Show Notes

River Horse Tripel Horse: A Belgian Style Tripel Ale.

WeldWerks Brambleberry Sour: A wheat ale.

Join the Listen Money Matters Community on Facebook by visiting listenmoneymatters.com/community to send in new catchphrases for the show.

And if you have any questions or topics you’d like us to talk about, email us at [email protected]. All the tools and resources we usually mention on the show are available at listenmoneymatters.com/toolbox.

Thank you to our sponsors: Ahrefs and Swap.com.

Ahrefs is the secret to LMM’s success. They cover every aspect of SEO. If you want to start a blog or improve traffic to an existing one, this is the tool. You can win a free Lite annual subscription by tweeting @ahrefs and @MoneyMattersMan and telling us why you should be our winner.