Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

We talk a lot about making sure your portfolio is diverse enough to insulate your investments from risk. But if you want to ramp up returns, consider diversifying your retirement with alternative assets. How can you do that? A Self Directed IRA is one of the most powerful tools in your retirement arsenal. Alternative investments can improve your chances of retiring with enough money.

And having enough money for retirement is something millions of Americans are going to be grappling with soon.

If we do nothing in the next 12 years, 40% of middle-class, older workers will be poor and near-poor elders.

But investing in alternative assets through a Self Directed IRA isn’t as easy as investing through

Rounding them all up takes more time than a lot of us are willing to spend. Those of us who were “raised on

Eric Satz wants to make investing in alternative assets just as easy as opening a

The Wonders of a Self Directed IRA

Before we jump into how to use a Self Directed IRA to invest in alternative assets, let’s do a quick refresher on IRAs. An IRA allows you to invest money on a tax-deferred or tax-free basis.

The money that goes into a Roth IRA has already been taxed. When you withdraw it during retirement, you don’t pay taxes on it. The advantage is that it helps reduce your taxable income. A Traditional IRA is taxed when you withdraw it during retirement. The advantage is that most people are in a lower tax bracket during retirement. Pretty simple!

For 2019, the contribution limits for IRA accounts are $6,000 for those under age 50 and $7,000 for those aged 50 and over.

What are Self-Directed IRAs

Self Directed IRAs work the same as described above. Your Self Directed IRA can be a Traditional or a Roth. Here’s the difference.

If you open an IRA through a company like Fidelity or Schwab or similar platforms, you get to choose from a list of securities that have been deemed appropriate for retirement by those company’s investment committees.

You won’t find so-called alternative investments on those platforms. What does that mean for the diversity of your investment portfolio?

In the past, there were 9,000 public companies. Now there are less than 4,000. And of those 4,000, about 200 of them account for all investor returns.

So all fund managers have some combination of those 200 companies in their basket of goods to generate returns. Not exactly diverse, is it?

If you want to be an Alpha Investor, you need some portion of your portfolio to be in alternative assets.

Fiscal flexibility that’s funny, free and delivered weekly.

So what exactly are alternative assets?

Alternative assets classes can include things like private equity funds, venture capital investments, precious metals, cryptocurrency, small business loans, tangible assets like collectibles, and real estate.

There are a growing number of platforms that make this type of investment accessible for regular people the way

Viva liberté, égalité, fraternité! More investment opportunities for everyone!

Those platforms include Republic, Ground Floor, and PeerStreet. They are driving capital markets away from Wall Street towards Main Street.

Real Estate

We wanted to give real estate its own little section because it’s something we talk a lot about and something a lot of you are interested in.

It’s great to have some real estate in your investment portfolio, but what’s even better? Investing in real estate in a tax-advantaged account.

How do you do that? With a Self Directed IRA!

You can invest in REITs (Real Estate Investment Trusts) like Fundrise through your Self Directed IRA. You can also buy rental property through your Self Directed IRA.

Check out Andrew’s course, Rental Properties for Passive Investors, if you’d like to learn more about investing in turnkey rental properties.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

What’s Wrong With Betterment ?

You all know that we love

According to Eric, ETFs, and index funds like Betterment, Vanguard, and Wealthsimple are a victim of their success. Due to their popularity, these platforms have created a pile on. Massive amounts of money is invested, which makes these platforms more expensive to use than they previously were. The higher the fees, the lower our returns.

Are these platforms still a great way to invest. Yes, there are. But they aren’t as good an opportunity as they used to be, and now other opportunities may give investors higher returns.

Know the Rules

For 2019, the contribution limits for Self Directed IRA accounts are $6,000 for those under age 50 and $7,000 for those aged 50 and over.

There are rules governing the use of Self Directed IRAs. If the rules are broken, you can lose the tax-deferred status of your account. This can lead to the disqualification of the IRA, which will have severe tax consequences.

- Prohibited Transactions and Investments: Discover what investments your IRA cannot make under IRS guidelines.

- Disqualified Individuals: Your IRA may not buy an investment from or sell an investment to a “disqualified person.” Learn more about “disqualified persons.”

- Indirect Benefits: The purpose of the IRA is to provide for your retirement in the future. It is considered to be an “indirect benefit” if your IRA is engaged in transactions that, in some way, can benefit you personally today. Learn more about “indirect benefits.”

- UBIT: Learn how and when your IRA incurs tax because of leveraged investments or business income, and how to deal with the situation.

The Benefits of a Self-Directed IRA

- More Choice: This is the most significant advantage of a Self Directed IRA. When you can include alternative assets among your choices, you have a lot of assets to choose from, which means a much more diverse investment portfolio.

- Tax-Advantages: The two most expensive things in life are interest and taxes. A Self Directed IRA helps you legally minimize taxes on your investments.

- Bankruptcy: The assets in a Self Directed IRA are protected under federal bankruptcy laws.

- Inheritance: Certain Self Directed IRAs allow the assets inside the account to go to beneficiaries with few or no tax implications.

Potential Risks

It’s up to you to do your due diligence on any potential investments you want to make with a Self Directed IRA. You will have far more opportunities than you would with standard IRAs, but not all opportunities will be a good fit for you. Know your risk tolerance and your financial goals.

Financial goals are indicators to the path you should take to reach the ultimate life goal.

Tweet ThisIt can be harder to find information on alternative investments so you may have to do a lot of digging. Eric recommends Kingscrowd. It’s kind of like the Motley Fool but for the Private Equity sector. Alto is planning to launch a community where members can discuss the investments they made and why and exchange ideas.

Are alternative investments so much more high-risk than traditional investments that companies like Fidelity choose to stay away from them? That isn’t the reason. Large companies like Fidelity have millions of customers. They can’t vet all of the investment opportunities that clients would bring if they dealt with alternative investments.

Those sorts of companies have a fiduciary relationship with clients. A company like Alto does not. They act purely as an administrator. They are neither judge nor jury. Do you want to make an investment? They will help you do that.

Because a Self Directed IRA is a tax-advantaged retirement account, it’s illiquid compared to a taxable account like

Self Directed IRA or any other kind of retirement account.

Who Are Self-Directed IRAs Best For?

If you prefer to be a hands-off investor or don’t have a high-risk tolerance, a Self Directed IRA may not be the best fit for your investment portfolio. You have to do quite a lot of research and man alternative investments come with a higher risk than do more traditional investments.

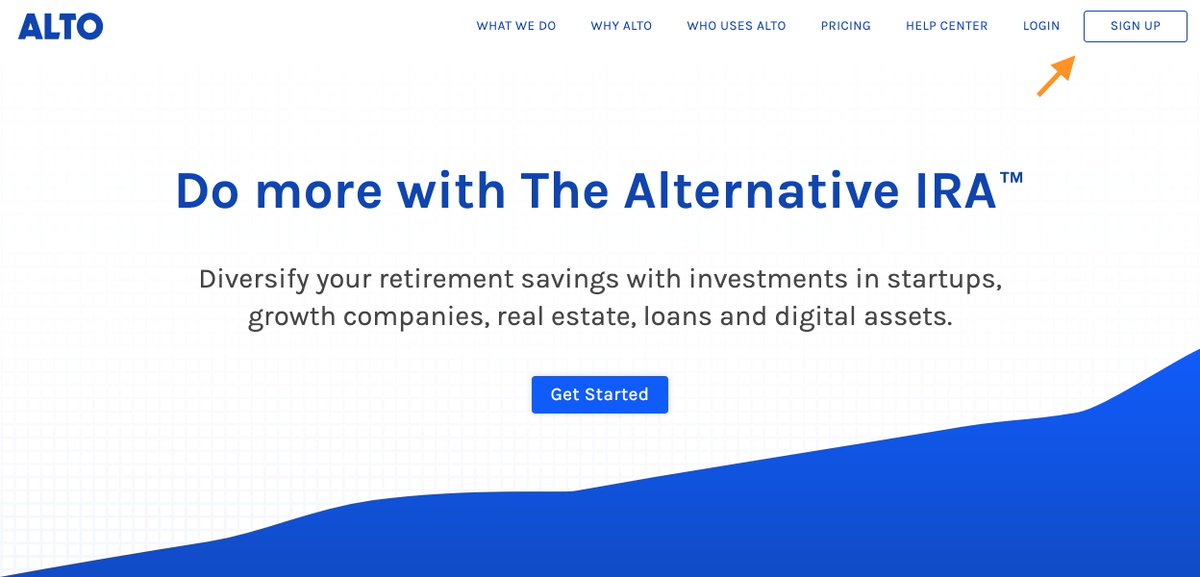

Introducing Alto

Alto wants to make managing your retirement assets online as simple as managing your bank accounts and taxes online.

The Alto platform provides users with a simple interface to set up, invest with, and manage a diversified portfolio of alternative assets. Eric was a venture capitalist who wanted to use the money in his Self Directed IRA to invest in a startup company. He wanted the investment to be long-term and tax-advantaged. How could he do it?

The process took a lot of time, 6 to 8 weeks to execute the transaction and was expensive. He wanted a solution to this but was it a big enough problem that maybe other people would like a solution too? Eric wasn’t sure but took the “If you build it, they will come approach” because a tiny fraction of invested money is in alternative assets. He built Alto to bring alternative investments to the masses the way Turbo Tax brought self-filing to the masses.

Alto is a tech-driven platform. It has partnered with investment platforms like AngelList, Carofin, Silicon Prairie, and YieildStreet.

If you want to make an alternative investment through one of those or another company, when you get to the question, “How Do You Want To Fund This?” you choose your IRA with Alto. What would have taken weeks and weeks of work can be done with Alto in just a few clicks.

If you want to invest with a company that isn’t an Alto partner, you can. Someone from the Investor Relations department of a non-partnered company will work with someone from Alto to make the investment happen. It’s more work for the non-partnered company and Alto but not for you.

Alto’s Fees

In the past, if you wanted to invest in private equity companies, you had to be an accredited investor. The SEC changed this rule. When these kinds of investments were only open to high-net-worth individuals, it was only wealthy people who could invest in alternative investments and have access to the high returns they can provide.

You no longer have to be an accredited investor to invest in alternative assets. Alto doesn’t charge a percentage but a flat fee. The fee is $99 per asset per year. Each platform is considered a single asset though so if you buy three rental properties through Roofstock with your Self Directed IRA held by Alto, it only counts as one asset.

But if you’re a Millenial, Alto has excellent news for you. Alto wants to encourage you to include alternative investments in your investment strategies so for people in that age group or anyone else whose account is under $10,000, will pay $49 per asset per year. Pretty good deal!

The Bottom Line

We are not saying, nor is Eric, that you should take all of your money out of private markets and go totally private. But having some exposure to alternative asset classes can help to diversify your investment portfolio and may help to ensure that you outlive your retirement money.

Show Notes

Apricot Compote Sour: A refreshing summer beer from Evil Twin.

Alto: The Alto platform provides users with a simple interface to set up, invest with, and manage a diversified portfolio of alternative assets.