Annuities are not exactly transparent, and neither are the people selling them. They are almost always a terrible investment, and when we explain what the f**k are Annuities, you will understand why and stay far away from them.

There is so much misleading information out there for Annuities in no small part because the financial incentives for selling Annuities is very high. We will take an unbiased look at them. We’ve never accepted a dollar from an annuity company, and there probably won’t be any beating down our door after this!

What the F**k are Annuities

Annuities are a financial product, typically backed by insurance companies and sold by investment banks that guarantee a fixed stream of payments primarily used as an income stream in retirement.

This income is taxable just like ordinary income you earn from your job and subject to the same tax rules. You fund the Annuity with your own money either through a lump sum or monthly contributions.

Your eventual payout depends on your contributions, the type of annuity you choose and its term.

They are often compared to pensions or even directly labeled as “personal pension plans.” You pay a certain amount of money during the accumulation phase that is later paid out to you as fixed payments during the annuitization phase.

Tax Deferred

A fixed Annuity has a set, guaranteed interest rate, and a guaranteed payout. A variable Annuity depends mostly on the performance of its underlying investments so the payouts can vary from month to month.

Often the most popular annuity is described as a “fixed income” style product with quoted returns as high as 6%. This is disingenuous at best and generally a flat-out lie. Technically you would have to live infinitely for the return to hit the sticker rate.

“Buying an annuity begins with the immediate loss of 100% of your original investment. So for the first 15 years, the annuity company is simply giving you back your original purchase price. The way most salespeople describe thinking about the annuity discourages investors from realizing that their original money is gone forever. They do this by referring to it as an investment. I would not call it an investment because after you purchase an annuity, your principal no longer has any value.”

If we don’t recommend Annuities, why are we even talking about them? Because eventually, someone is going to pitch them to you. Andrew and Laura got the hard sell by an Uber driver on the way home from the airport!

And it’s not surprising Annuities are pitched so hard. The commission on them can be as high as 10%! There are even Annuity startups popping up, and they can be very seductive, so it’s important to know just what you are being sold.

Fear is what you are being sold. It’s often a big part of an Annuities sales pitch although it can be so subtle, you don’t realize it. People can be fearful of the stock market, especially during a shaky economy. Those selling Annuities play on this fear and pitch them as a safe alternative.

Annuities are mostly marketed to those nearing retirement age because people in that demographic are understandably nervous that they might not have enough saved for retirement and will outlive their money.

The Annuities Business Model

As we all know, there is no such thing as a free lunch, and that is especially true when it comes to Annuities.

Annuities are a gold mine for the people who sell them. The commission can be as much as 10%. If a salesperson convinced you to contribute $100,000 to an Annuity, he or she could earn as much as $10,000!

How can a salesperson earn such a huge commission? Where is that money coming from? A big part of it is from the “surrender charge.” Annuities have a high surrender charge which is a fancy way of saying that you will be charged a punitive fee of up to 7% if you withdraw your money early.

You can’t access the money until age 59 1/2. If you withdraw money before that, you will pay a 10% tax penalty similar to a 401k on top of the 7% fee charged by the company holding the Annuity.

Unsurprisingly, over 75% of the more than $200 billion Annuities sold every year are the complex high commission types. But the good news is, sales are going down.

Fees

In our research, we found the following statement on a site that sells Annuities.

“Unlike variable or indexed annuities, fixed and income annuities don’t have any fees. All expenses incurred by the insurance company, including paying us as distributors, are reflected in the price they’re able to offer. The income or return quoted is exactly what you’ll get – no more, no less.”

This is simply not true. You will absolutely be charged fees, but they are being obscured by including them in the price and not providing an itemized breakdown. It’s like buying an item online with free shipping. No such thing as a free lunch remember so the cost of shipping has just been factored into the price.

The funds your Annuity invests in have fees, the insurance company underwriting your annuity takes a fee for the risk, rider fees, and flat contract fees. And of course the previously mentioned surrender charge.

It typically takes 7-8 years before the surrender charge period phases out entirely. The penalty usually reduces by 1% a year. This is the Annuity company locking down your money and charging you a sliding scale fee depending on how early you withdraw.

And remember, like a 401k, you will be hit with a 10% early withdraw fee from Uncle Sam if you access the money before the age of 59 1/2. All these fees conspire to lose money.

The old joke about annuities is that you make a fortune on the headline and then the fine print takes it all back.

Tweet ThisEven without the surrender charge, you could be paying 2-3% in fees a year all totaled. Remember, you want to pay a total fee of less than 1%, so 2-3% is just completely unacceptable.

Inflation

Inflation can pose a real risk to your retirement, and you need investments that will insulate you from its effects. Annuities will not do that. They do not account for inflation. According to the Government Consumer Price Index (CPI), $5,081 in 1970 had the same buying power as $30,000 today.

Imagine thinking you were all set for retirement in 1970 because you bought an immediate Annuity paying $5,081. You purchased the Annuity as longevity insurance, but you are now trying to live off a sixth of the money you needed in the first year of retirement.

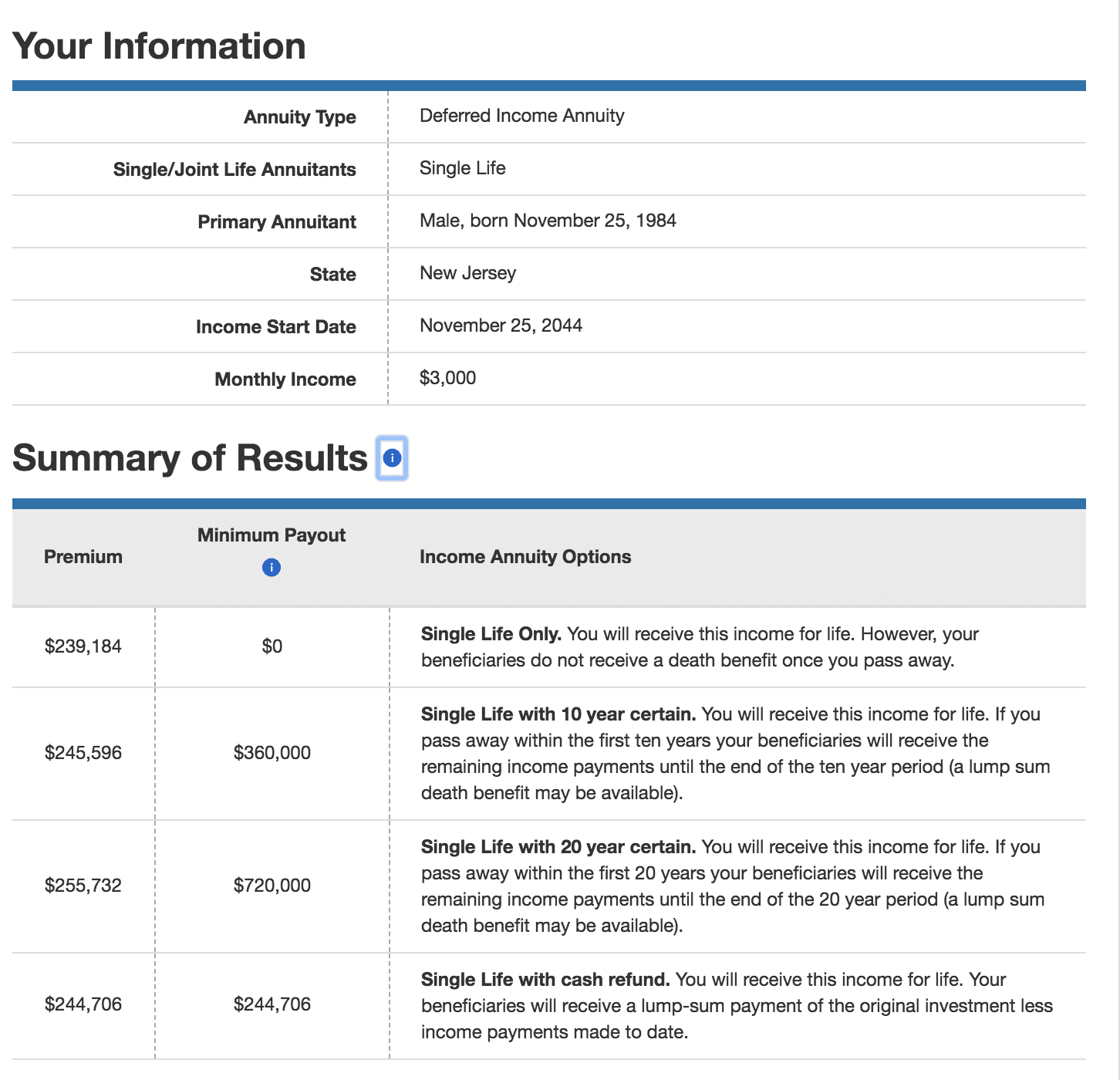

How Do They Calculate What You Get?

It’s an insurance premium so “black magic.” Andrew ran his own numbers:

With the above Annuity from Schwab, it would take 6.6 years for him to reach a 0% return on his. Investment. Six and a half years! And don’t forget all the years leading up to withdrawal when he was getting a $0 return.

The Rule of 72 is a rule of thumb that shows how long it takes for an investment to double your money. With a 6% return, it would take 12 years.

Should Anyone Buy Annuities?

Okay, hopefully, we have convinced you to stay away from Annuities. But is there anyone who should buy them? If you make a ton of money and have already maxed out your other retirement accounts and want to lower your taxable income, an Annuity is an option. And they have no contribution limits, unlike 401ks and IRAs.

If you have a pending judgment against you or expect one and want to attempt to shield your money, an Annuity would be a way to do so. Are you insanely and unrealistically petrified of the stock market and you have no use for math or common sense? You might like Annuities, but we suggest reading our article on how to get over your fear of investing instead.

Fiscal flexibility that’s funny, free and delivered weekly.

Annuities, Just Say No!

Books, courses, and financial advisors that tell you Annuities might make sense in some situations are being intellectually lazy. Based on the fees, limited access to the funds, ability to lose everything if the insurance company goes bankrupt and inability to pass it along to your heirs, we are going to take a firm stance here and say there is no place in your portfolio, ever, for an Annuity!

If the idea of having a fixed source of retirement income is something that appeals to you,

Troegenator: A Double Bock with notes of caramel, chocolate, and dried fruit.

Toolbox: All the best stuff to manage your money.