Building wealth isn’t just about accumulating money; it’s about creating opportunities for freedom and security that can last a lifetime. Discover the strategies that can transform your financial habits and set you on the path to a prosperous future.

Save Money

Building wealth becomes faster and easier when you master the art of saving money. While earning more is crucial—and we’ll discuss that—knowing how to save is essential. Without this skill, you might find yourself struggling financially regardless of your income.

This is evidenced by tales of lottery winners and professional athletes who, despite acquiring fortunes that seem insurmountable, manage to deplete their wealth astonishingly quickly.

Ultimately, wealth accumulation is significantly influenced by your habits. Adopting sound financial practices is a fundamental step in this journey.

Budget

We know that you might be weary of hearing this repeatedly, but it’s important to acknowledge that you can’t begin to build wealth without a clear understanding of your financial inflows and outflows. Detailed budgeting for every item isn’t necessary, items can all be grouped under summary categories

However, it is essential to budget your money and monitor your spending meticulously. We all have spending leaks—areas where we might not realize just how much we are spending. Reviewing your budget at the end of each month can highlight these areas, enabling you to take corrective actions.

For those new to budgeting or struggling with irregular income streams—such as freelancers or real estate agents—tools like Monarch Money offer user-friendly budgeting solutions, while You Need a Budget is particularly helpful for managing fluctuating earnings.

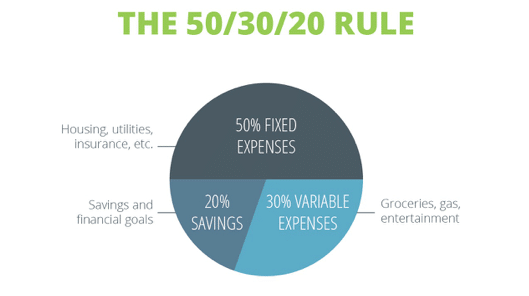

Setting up your budget using a straightforward strategy such as the 50/30/20 rule doesn’t take long, and once everything is in place, it requires minimal effort to maintain.

50%: The Essentials

The 50% represents the essentials in your budget, expenses like housing, HOA fees, utilities, transportation, parking fees, insurance premiums, and groceries among them. This also includes things like child care and child support.

Just because these expenses are essential doesn’t mean we can’t find ways to reduce them. We’ll explore strategies for doing just that.

30%: The Fun Stuff

The 30% is to be budgeted on non-essential (discretionary money), things that you spend money on but could live without.

This percentage includes things like meals out, leisure activities, clothes (clothes are a necessity, yes, but presumably you haven’t been running around nekkid to this point, so you already have some), hobbies, and grooming.

20%: The Important Stuff

The 20% represents the portion of your income that should be allocated towards savings and debt repayment. This includes setting aside money for your emergency fund, investing for the future, and paying off any debts beyond the minimum payments required. This portion of the budget focuses on improving your financial security and building wealth over time.

Major Expenditures

Housing

Housing is the most significant expense for most of us so how much of the 50% should be devoted that and what exactly does “housing” encompass?

Housing should comprise 30 percent of your take-home income. That includes the mortgage or rent, all home repairs and maintenance, property taxes, utilities such as electricity, gas, water, and sewer, and homeowners or renters insurance. In short, it includes every housing-related expense.

Tightening your budget in other areas of the 50% may be necessary, as housing is expensive. For city dwellers, options to mitigate these costs are limited unless you’re willing to take on a roommate, live far from your workplace, or reside with your parents rent-free. There aren’t many alternatives to circumvent the high cost of housing.

For most of us, our rent or mortgage payment is our biggest expense. Within the 50%, we spoke of above. A Harvard report says “22.4 million households in the United States now spend more than 30 percent of their income in rent, with 12.1 million spending more than 50%“.

Remember, the most important thing is to be mindful of your overall financial picture. Track your expenses, including housing costs, and adjust your budget as needed to ensure you can comfortably afford your living situation while meeting your other financial goals.

Cars

There’s a difference between being rich and wealthy. Rich people might have a lot of money, but wealthy people focus on building long-term financial security. This doesn’t necessarily mean wealthy people avoid all nice things, but they tend to prioritize financial planning and making smart investments over flashy displays of wealth.

Buying a brand-new car is often considered a poor financial decision, primarily due to the rapid depreciation it undergoes. It’s hard to predict exactly how much a car will depreciate, but generally, it can lose up to 35% of its value within the first year alone. This is an important factor to consider when buying your first car.

Additionally, if you finance the purchase with a loan, you end up paying interest on an asset that is steadily decreasing in value, further impacting its cost-effectiveness.

This doesn’t mean you should settle for an unreliable, old car. Ideally, you want a vehicle that is dependable, offers good gas mileage, and isn’t costly to insure. It’s best if you can pay cash for a car that still meets these criteria.

However, it’s not always possible to buy a car outright. Nonetheless, there’s a significant difference between taking out a $10,000 loan for a reliable used car and a $30,000 loan for a brand-new one.

Shop Smart

Do Your Research – When you have to buy something, do a little research first to find something that will be of good quality. You may pay a little more upfront, but when you buy something that lasts, you save money overall because you don’t have to replace a broken or worn-out item as often.

30-Day Savings Rule – You might need to delay the purchase to save up for a more expensive item, but practicing delayed gratification is beneficial. One effective way to curb an overspending habit is by using the 30-day savings rule. If you are considering making a large or impulse purchase, write it down and wait 30 days. If you still want the item at the end of those 30 days, you can buy it.

Search for Discounts – If you are planning to make a larger purchase, such as furniture, appliances, or electronics, develop the habit of searching online for discounts, coupons, or discount codes related to the item or store. Additionally, be aware of the best times of the year to buy these items. Consumer Reports provides a helpful list of optimal purchasing times. This practice can save you money and ensure you get the best deal possible.

Don’t turn your nose up at second-hand items. Thrifting can be a lot of fun, and you will be amazed at how many brands of new stuff including clothes and small appliances, people donate to second-hand shops.

Automate

Have you ever been hit with a fee for paying a bill late not because you didn’t have the money but because you just forgot? If you automate your bill paying, you’ll never pay a late fee again. You can set up the automatic bill through most banks online and schedule the payment a few days before the due date.

Cushion helps you organize your bills and provides reminders for what needs to be paid and when. It offers features that allow you to securely link your bank and email accounts to automatically find and organize all your bills, subscriptions, and Buy Now Pay Later (BNPL) payments into a single, user-friendly dashboard. This makes tracking and managing due dates more straightforward.

You should still look at your bills, there could be an error, and you could end up paying more than you owe, but there’s no reason to pay them by hand every month.

80% of people save money by using Rocket Money to find and cancel unwanted subscriptions! With Rocket Money, you can also effortlessly track your spending, easily lower bills and track your net worth.

Your Personal Life

The things you do and the people you allow into your personal life can have a big impact, for good or bad, on your ability to build wealth.

Money Can Buy Happiness

Despite the old cliché, it really can buy happiness if you know what to spend money on. Research shows that we are happier when we buy experiences rather than things. This makes sense when you think about it.

Consider the last concert, play, or art exhibit you attended. Did you enjoy yourself, spend time with friends, and talk about it for days or weeks afterward? Now, think about the last item you purchased. Does it evoke the same level of enjoyment and lasting memories?

The other way spending money can make you happy is through charitable giving. Find a cause you care about and make a donation. It doesn’t have to be a lot. We feel happy when we help others.

Learn How to Have Fun for Free

Learning how to have fun for free is a valuable skill that can enhance your quality of life and reduce stress without straining your finances. Here are a few examples of free activities that can provide enjoyment and fulfillment:

- Exploring Nature: Take a hike, visit a local park, or explore a nature reserve. Nature walks not only provide exercise but also allow you to appreciate the beauty of your surroundings.

- Attending Community Events: Many communities offer free events such as outdoor concerts, movie nights, and festivals. These events can be a great way to enjoy entertainment and socialize with others.

- Volunteering: Giving your time to a cause you care about can be incredibly rewarding. Volunteering allows you to make a positive impact, meet new people, and gain a sense of accomplishment.

- Potluck Picnics or Dinner Gatherings: Organize a potluck picnic or dinner gathering with friends where everyone brings a dish. This is a cost-effective way to enjoy good food, great company, and create lasting memories.

- Engaging in Hobbies: Pick up a hobby that doesn’t require much spending. This could be anything from drawing, writing, or gardening to DIY projects using materials you already have at home.

Having Kids is Costly

To raise a child from birth to age 17, excluding college expenses, a middle-income family in the United States can expect to spend between $280,000 to $312,000. This translates to an annual cost of approximately $12,350 to $14,000.

Daycare can be so expensive that one parent quits their job because the salary is just covering the cost, so it makes more financial sense not to work. That means time out of the workforce which can have a financial impact in the future.

Understanding these expenses helps in making informed decisions about family planning, budgeting, and ensuring that resources are allocated effectively to provide a stable and supportive environment for children

Talk to Your Parents

If talking to a partner about money is uncomfortable, talking to your parents about it can be even worse. We all like to think of our parents as capable people whose job it is to take care of us. But the day may come when you need to take care of them.

That can mean anything from checking in on them from time to time to footing the entire cost of their care to letting them move in with you. If you don’t talk about their plans for the day they can’t fully take care of themselves anymore, you can’t know what will be expected of you.

Here are some important things to discuss with your parents.

Do they have a will including a living will?

You need to know who gets what when they die and what kind of medical care they want if they cannot speak for themselves.

What kind of medical insurance do they have?

Having Medicare alone is not enough. There are a lot of medical expenses it doesn’t cover including many types of long-term care. Dying like everything else in America is not free.

How much are their monthly expenses and what kind of savings do they have?

If they numbers are not working out, you may need to discuss cutting expenses, possibly down sizing their home if they’re empty nesters.

Where are any documents you might need to fulfill their wishes in the event of hospitalization or death?

It’s no good knowing what your parents want if you don’t know how to prove it. They should tell you where to find things like their wills, their attorney’s contact information, and any passwords you might need for various accounts.

This is by no means an exhaustive list, but it will at least give you a starting point.

The People You Know

We are an average of the five people we spend the most time with. To some extent, their habits and behaviors influence our own. That’s why it’s so important to pick your spouse carefully. Make sure you surround yourself with people who share your habits and values.

If your friends are all big spenders (whether they can actually afford to be or if they charge their whole lives to credit cards), you are going to spend too much money when you’re with them. If your spouse keeps a budget and saves money for the future, you will be encouraged to do that.

Fiscal flexibility that’s funny, free and delivered weekly.

Make More Money

A lot of us don’t want to fuss around bringing our lunches to work and researching the best cell phone plan. We would just rather make more money than worry about counting pennies. So how do you make more money?

Find a New Job

For most of us, our regular job will be our biggest source of income. The average raise is 3.8% to 4%. If you want a bigger jump in income, change jobs every few years. Studies show that employees who switch jobs typically receive salary increases between 10% and 20%.

Start networking, polish up your resume, and learn how to negotiate. Strategically changing jobs can be a more effective way to increase your income and build wealth over the long term.

Improve Your Skills

No matter how long you’ve been in a certain industry, there are always ways to improve your performance. Take a public speaking class, get some additional certification or find a training seminar you could attend.

If you’re not sure what you can improve upon that would help you make more money in your current job, take a look at job openings for a similar but higher position in another company. Read the job requirements. Is there anything they’re looking for that you are lacking? That’s a good place to start.

Multiple Sources

Anyone can lose their job, and you may not always find a new one right away. That’s why you need money coming in from more than one source. It doesn’t have to be a ton of money, but something in case your primary source of income is interrupted.

This money can come from any number of places, a part-time job you have on the weekend, a side gig like freelancing, a hobby like making and selling things on Etsy, Amazon Handmade or at craft fairs, tutoring, or income-generating investments like

Even if it’s only a few hundred bucks a month, that can really make a difference financially. Either you don’t have to dip so deeply into your emergency fund, you don’t have to go into credit card debt charging all your expenses, or you can take your time finding the right job instead of taking the first thing offered out of desperation.

Debt

Having debt while you’re building wealth is like driving with the emergency brake engaged. You might get there eventually, but it will take longer and put wear and tear on your car.

Simplify your bills with a debt consolidation loan

- Check your rate in 5 minutes.

- Get funded in as fast as 1 business day.²

- Consolidate your bills into 1 fixed monthly payment.

Get Rid of What You Can

There are ways of reducing your debt without paying it off. If you have credit card debt, first look into doing a balance transfer to a card offering 0% APR. Some cards offer that introductory rate for as long as 21 months. That’s almost two years to work on the balance without having to pay interest.

Just be sure you do pay off the entire balance. Once the 0% APR ends, you’ll have to pay interest on the remaining balance and possibly at a higher rate than the card you transferred the debt from.

You can also look into getting a loan from like Upgrade. They will loan you money to pay off the credit cards. You still owe money, but now you owe it to them at a much lower interest rate than you were paying to the credit card company.

You can also look into getting a personal loan from your bank to pay off credit card debt.

If neither of the above are options, have a plan to pay off debt. Just throwing extra money at credit card debt randomly won’t help you pay it off faster and won’t save you money on interest. There are two methods you can use; snowballing and stacking. We wrote a lengthy article on this but here is the gist:

Snowballing means listing all of your debts in order of smallest to highest dollar amount and then using any extra money to pay off the smallest balance while only paying the minimums on the others.

To use the stacking method, you list your debts in order of highest to lowest interest rate, regardless of the dollar amount of the debt. You throw as much money as you can at the debt with the highest rate of interest. Both have their advantages, but stacking will save you the most money on interest.

If you’re a homeowner, you may be able to eliminate some of your mortgage debt by refinancing. Imagine you refinance and get one percent off your original interest rate. Now, one percent doesn’t sound like much if you’re talking about a raise, but when it comes to interest rates, a one percent difference is enormous!

If you bought a home for $300,000 with 20% down and a fixed rate 30-year mortgage at 4.5% versus 5.5%, you would save $52,794 in interest!

If you have student loan debt, you can refinance that too with a company like Earnest. It may lower your interest rate and your monthly payments. Just be sure you understand that if you refinance federal student loan debt, you are losing certain protections.

Credit Score

One of the most effective ways to avoid debt is to avoid paying interest. While you can’t always avoid it entirely, no bank is going to give you a 0% interest mortgage; you can minimize the interest you pay when you have to borrow money. By having a great credit score.

Your credit score is made up of six components. This number tells lenders how much of a risk they’re taking when they loan you money for things like a home or a car. The higher your credit score, the lower rate of interest you will get on those loans. And we saw in the example of refinancing your mortgage how much difference even 1% can make.

A credit score of 740 or above will get you the best interest rates. If your score could be improved, here are some ways to do it.

Don’t Get a Tax Refund

We all look forward to getting a nice big return come tax time but we shouldn’t. When you get a tax refund, you’ve given the government an interest-free loan. Instead of doing that, you should be putting that money to work for you by paying off debt or investing.

If you’re getting a few hundred bucks back, don’t sweat it. But if it’s a few thousand, you’ll want to give your employer a new W-4. You can use this calculator to determine the changes you need to make.

Investing

The key to building wealth is investing.

Educate Yourself

Investing can be intimidating if you don’t know much about it. But investing doesn’t have to be complicated. We have written a lot on investing for beginners. If it’s all Greek to you, start with Investing 101: An Introduction to Simple Investing.

Once you understand the basics, you can move onto something a little more complicated and dig into Investment Strategy: The Ulitmate Blueprint. Andrew breaks down exactly what to do with your money if your goal is building wealth.

Don’t Procrastinate

The earlier you start investing, the more time your money has to grow. Because compound interest is so powerful, there is no substitute for time. Here is an example:

If you invested $5,000 a year from age 25 at a return of 8% a year, you would have $1,523,000.00 at 65 years old. If you invest $5,000 a year from age 35, you would have just $653,220.00 at retirement.

Free Money

An employer-sponsored 401k is the introduction to investing for many people, and it’s a good place to start. You just fill out a few forms and HR takes care of the rest. Even if a 401k isn’t the best place to invest (the fees can be high, and the choice is limited), there are two features that can make it worthwhile.

For those who have a hard time-saving money to invest, 401k’s are great because the money is taken out of their paycheck before they can spend it. It’s automatically deducted. The other good reason to invest in your employer’s 401k is matching. If your employer offers matching contributions, take it! Even if you have debt to pay off, that matching is free money.

Fees

Even experienced investors often don’t give much thought to fees, but you can lose as much as one-third of your retirement money to these fees over time.

You might know what percentage you are paying but how much is that in real dollars? The average actively managed fund charges 1.25%. That doesn’t sound like much, but over time, it adds up.

It adds up to a lot. If you invest $100,000 in a fund with a 1% annual fee, it will cost you nearly $55,384 over twenty years. If you had invested that $55,384 instead, you could have earned approximately $177,623 with a 6% annual return.

A fee under 1% is a good target, and you can find fees that are low or lower with Index Funds and ETFs. The average traditional index fund has a fee of 0.74%, and the average ETF fee is 0.44%. Vanguard’s lowest-fee fund, the Vanguard 500, has a fee of 0.17%.

If you’re choosing funds through your employer, it’s likely that no one in your HR department is an expert investment advisor so don’t count on them to explain the fees to you or even know what you’re talking about.

Read the prospectus of each choice. That’s where you’ll find information about the fees charged. If you don’t like what you see, do some research on your own to find a fund with better fees and suggest it be included in the choices.

You can use Empower’s Fee Analyzer to find out how much you’re paying in fees. The site will analyze your investments to uncover where you are paying fees and how much you’re paying.

Tax Advantaged Investing

Taxes and interest are two of the biggest drains when you’re building wealth. There are investment vehicles that allow you to minimize taxes on those investments. Your 401k is one type. Your contribution comes out of your paycheck before income tax is deducted which means your taxable income is reduced.

The money grows tax-free in the account, and you are only taxed on it when you withdraw money after you’ve retired. For most of us, our income tax rate is lower during retirement so we pay less tax on that money than if we had paid taxes on it during our working life.

IRA’s are also tax-advantaged investment accounts. There are two types; Roth and Traditional.

A Roth IRA is taxed upfront and not upon withdrawal after age 59 1/2 or after. For 2024, the contribution limits are the same as for a Traditional IRA.

A Traditional IRA is not taxed upfront but at the point of withdrawal. The money grows tax-deferred. Upon withdrawal after age 59 1/2, the money is taxed as income. For 2024, you can contribute up to $6,500, or $7,500 if you are aged 50 or older.

Which is better? When you’re in the prime of your career, you’re being taxed at a higher than you are likely to be in the future. You want the tax advantage of the Traditional IRA during your highest earning years because once you give up those tax advantages, they’re gone forever.

If you really want to minimize taxes check out our episode on Advanced IRA Strategies. It will give you a fuller explanation, but this is the gist:

After you leave your job, you may have less taxable income. During this time, you can slowly roll over the Traditional IRA to a Roth IRA. This rollover counts as ordinary income, so to minimize taxes, convert an amount that keeps your total taxable income within a lower tax bracket and takes full advantage of the standard deduction.

Real Estate

One of the biggest components of building wealth is passive income. Passive income is money coming in that you don’t have to do much or anything to earn. It could be royalties from a book you wrote, dividends from stocks you own, or our favorite, income from rental properties.

What if you don’t want the responsibility of being a landlord, fixing clogged drains and leaking toilets? If you want the income from

A good turnkey management company will find the property, renovate it, and put a tenant in place and deal with any repairs and maintenance that might need to be done.

If even turnkey rentals sound like more involvement than you’re comfortable with, you can still invest in real estate. Fundrise is an online investing platform that allows you to make real estate investments and a virtual space for companies who need financing for their real estate projects to find investors who will buy shares in that project.

Building Wealth Begins Today

Financial independence is the goal most of us have in mind when we think of building wealth. We aren’t interested in the mindless accumulation of money; we want to use our money to buy our freedom. And that’s what building wealth allows you to do.

Stop dreaming and start building.