I’m a 30-year-old bachelor who works from home, and I no longer worry about money.

For many years I worried about money, but now I spend time enjoying it.

Very few people wake up one day and just become wealthy suddenly, becoming a million dollars richer. It is a choice you make and a way you live your life every day.

It took me a long time and a ton of hard work, but I eventually learned how to get rich quick for real. I’m certainly not super-rich, but my money mindset has changed dramatically.

Most of us don’t get rich quickly; it’s a journey. So if you are looking for a get-rich-quick scheme or some hack, you’ve come to the wrong place. Want to know how I did it? How can I possibly teach you how to get rich quickly?

Here’s how I became rich quick (for real):

Just in case you’re a busy professional who only has time to read lists, all you need to know to get rich is the following:

- Realize you suck with money and believe wealth is possible for you.

- Start investing now, and your future self will thank you.

- Educate yourself on money and learn to build wealth the right way.

- Make more money and live a life that makes success happen for you.

- Listen to our podcast and free your inner financial badass.

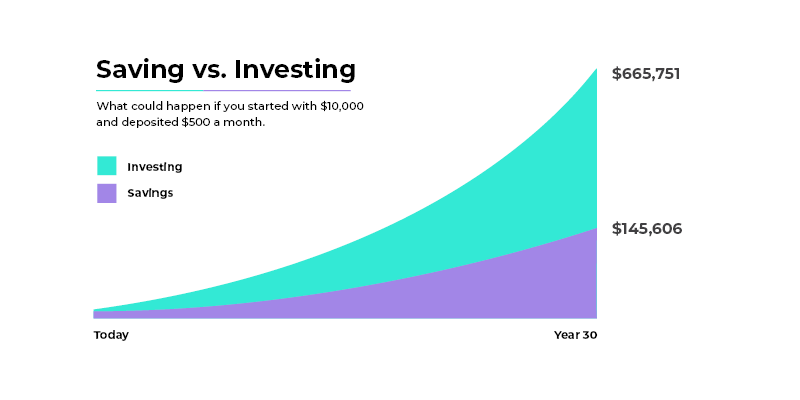

Investing

Being frugal is important, but it’s only one side of the coin. Cutting your fancy cappuccino habit to save a few bucks isn’t going to push the needle for you. While there is a limit to what you can save, there is no limit to how much you can earn. You have to make your money work for you.

Investing in the Market

The easiest and the most efficient way to grow the money you’ve already saved is through investing in the stock market. The best part is it doesn’t take much work on your part; it can be put on autopilot while the compound interest does the rest.

No, investing in the stock market will not make you rich overnight. It’s a slow, steady, and consistent building of wealth. With a 7% average yearly gain, your initial investment will double in a few years.

You can’t do that by keeping it in a savings account. In fact, in 10 years, your savings will be worth less because of inflation.

You don’t need much money to start investing, and every little bit counts. If you’re an investing newb and need help getting started, we’re here to hold your hand.

We love M1 Finance for beginner investors because there is no minimum, the fees are low, and you don’t need to know anything about investing to get started. We wrote an in-depth review that will walk you through getting invested with M1.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

Invest in Real Estate

Real estate can make you rich, but you need a little more money to start.

If you’re reading this article, you’re probably not ready for real estate investing yet, but you might want to put it on your list of financial goals.

Investing in turnkey rental properties can have fantastic returns; it’s how Andrew got started.

He and his wife saw deals to completion, documented the process, and created a course focused on using their turnkey real estate investing strategy to build meaningful wealth.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

If you’re interested, we have a bunch of resources and podcast episodes you can check out. We cover everything from cash flow to tax benefits.

If you are looking to invest in real estate and want something a little more hands-off, check out Fundrise, where you can invest in crowdfunded real estate projects.

Take Away: You have unlimited earning potential, and the only thing stopping you from earning more is you.

Less Stuff = More Money

Just a year ago, I worried about money all the time. I never had enough money to live the life I wanted, but I could pay my bills. I had a house that ran me close to $2,000 a month, a BMW that cost over $400 a month, and a bunch of stuff inside of both. I needed at least $3,000 a month just to keep up with my stuff.

Then, I lost my job. I needed to downgrade my life, or I wasn’t going to make it. I sold the BMW and bought a Honda Civic for half the price. I rented out my condo and moved in with my younger brother – reducing my monthly living expenses dramatically.

I made a list of what was important to me and what was not. I sold every non-essential I could to make some cash.

Why do you need all that stuff?

If I were to take an inventory of my life and the things I use every day, it would be a bed, a chair, a car, a computer, a frying pan, and a French press. Those are things I couldn’t live without. The rest of the stuff I rarely use.

We live in a consumer world. That’s why we even think about how to get rich quickly. However, we don’t have to conform to it. You probably have a house full of useless stuff; get rid of it.

When I had this epiphany with stuff, everything changed. The way I thought about money shifted dramatically.

Do I Need This?

If you’re buying stuff daily, you need to take a step back and think about it. I like to create a 30-day list of things I’d like to buy on my phone.

If I see something in a store, I don’t buy it immediately; instead, I just put it on my list. That curbs the urge. 95% of the time, I end up not wanting it in 30 days. I also always ask: Will this thing improve my life?

Most of the time, it won’t. Most of the time, I can’t even remember why I wanted that thing; I put it on the list anyway. If you need to buy stuff, ensure you get the best quality for the price.

Take Away: Stuff costs money. Keeping stuff in your house costs money. Using stuff costs money. Less stuff, more money.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Educate Yourself

Financial education is your best investment. I made it my New Year’s resolution to educate myself about money — since I spent almost 20 years being terrible with it.

There are two books: The Simple Dollar and” I Will Teach You To Be Rich. Start there. We also created an awesome podcast where we drink beer and talk money to help make it all a bit easier.

Invest in yourself, in your education. There's nothing better. -Sylvia Porter

Tweet ThisThe one thing I learned was debt is the devil. Both books drilled into my head that I should be debt-free.

Debt is The Devil

Now that I was a streamlined bachelor with very low living expenses and nothing to buy, I had some available cash. I decided to pay off my credit card debt. Having no debt is freedom, and that’s an idea I could get behind.

Having debt while trying to achieve financial independence is like driving with your foot on the brake. While debt can be valuable and even profitable if used correctly, too many people spend money they don’t have.

Bad debt, like credit card debt, compounds many times faster than the best investments ever could and can quickly outpace your ability to earn and pay it off. Not to mention what it does to your credit score.

The good news is you don’t have to drown yourself in debt. However, the minimum payment is not going to cut it. Attempting to escape debt with minimum payments is like trying to toast bread with a flashlight.

I did some more research to determine the right method for paying off my debt and found the stack method. I won’t go into detail, but you can read about it here.

You refinance all the debt you can and then prioritize the most expensive debt first.

It can also help to have someone negotiate your debt away for you.

Student Loans Suck

I don’t personally have student loans, but I know many people like my brother who make that dreaded monthly payment. From now until what seems like an eternity, a few hundred bucks out the window every month.

The interest on those loans will ruin you. The quickest way to reduce your student loan balance and pay less interest is to refinance.

Companies like Credible can dramatically reduce that interest rate and save money on your loan.

Take Away: No stress, no debt, uh, freedom! A feeling better and longer-lasting than sex. If you need a little help, we have a free book here to help you with your debt reduction plan.

Track Your Net-worth

Taking a hard look at your finances can be scary, especially if you’re in the negative. But if you want to be rich or a millionaire, you can’t avoid it forever, and it is best to face your fear now. You will feel relieved knowing where you stand financially instead of just guessing. Then you can set goals and track them.

An excellent free budgeting tool. I use it, and if you're getting started, you should too. If you don't track your spending, you'll never know where you're wasting money.

What gets measured gets managed. - Peter Drucker

Tweet ThisNetworth is probably the most important financial number you can track. It’s a simple way to see your financial life with a few basic calculations. Every month income comes in, and expenses go out to pay bills and rent. If you still have some money left over after all your expenses are paid, that’s great. Now you have some money to invest and grow.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

Personal Capital is a great tool for budgeting and tracking your net worth, and it’s free to sign up.

Living below your means is the simplest way to save money. If you are in the negative month after month, it’s time to look at your budget and see where you can cut and how you can make more money to make ends meet.

Tracking your net worth will show you your finances on a small scale, month by month, and on a larger scale, year by year.

Make More Money

Invest in Yourself

Not every investment has to start with money. Making simple changes in your lifestyle can drastically improve your life and work, which can make you more money.

Are your friends ballers? Do they go out all the time and spend tons of money buying expensive dinners, gadgets, and other crap they don’t need? If your friends are not financially responsible, it will be harder for you to be responsible.

You want to surround yourself with people with the same goals as you and people you can learn from. You need financial friends, and it’s probably about time you got financially naked.

Maybe you have a great job, but your 3% raise every year isn’t going to make you rich. You need to push the needle a little bit; work with me here.

Moving jobs every few years is the best way to keep bumping your income. People who change jobs often make 50% more over their lifetime than those who stay longer.

If you don’t feel you have the skill set to find a better position, then upgrade your skills. Take a class or read some books that can help you get to make more money at your current company or help you find a better spot for a new one.

Invest in Building your Own Business

Who doesn’t want a little (or a lot) more money? There are many great ways to grow your income streams outside your day job. From selling crap, you don’t need to building a side business; it’s always an excellent idea to make some extra money. It can help you pay off debt quicker, grow your investments, faster become into a full-time gig.

Earning some extra cash on the side can be fun; it will increase your level of income security and confidence. There are also a ton of tax incentives for small business owners.

Never depend on a single income. - Warren Buffett

Tweet ThisWant to earn some passive income and start your side hustle? Most rich people have become wealthy by starting their own businesses. Learn how other successful entrepreneurs and millionaires made their money. Get inspired and start to work on a great business idea.

I’m a skilled web designer and knew I could make money by designing a few websites. I started reaching out for work by cold emailing and walking into local businesses. I paid off my debt in a few months with the extra income. I didn’t have a ton of debt to begin with, but I’ve been working on it for over 15 years.

I now realized I had extra money because it wasn’t going towards paying my credit card bills — this was on top of the fact that my living expenses were much lower than they were. I found myself with a lot of extra income.

How Will You Get Rich Quick?

A total life transformation won’t happen overnight, but it will start to slowly take shape with each choice. Action will be the key to success. You also need to learn about personal finance. That knowledge is critical if you want to achieve financial freedom.

Building wealth is not something you will just stumble upon one day. It’s something you work at every day, forever.

Fiscal flexibility that’s funny, free and delivered weekly.

I live South Jersey (actually, I just refer to it as Philadelphia). Follow me on Twitter and we can chat about pools, beer or internet marketing.