Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Many people want to know how to become a millionaire, but getting rich isn’t about learning a few financial secrets. There’s no such thing as getting rich quickly. Unless you win the lottery, which you won’t. And there is a very significant difference between wealthy people and rich people. We’ll show you how to get rich and stay wealthy.

Achieving financial freedom is about a long-term commitment to saving and making wise investments to build your wealth.

I know; it’s not sexy at all, but it’s entirely true. It’s like Warren Buffett says:

Building wealth is a marathon, not a sprint. Discipline is the key ingredient.

Even though becoming a millionaire might seem out of reach, long-term wealth building is an attainable goal for most people regardless of their income, skillset, or stage of life.

You don’t have to be making six figures as a doctor, lawyer, or engineer to have a lot of money.

And one of the secrets of getting rich isn’t hard work, good news for all of us slackers out there.

It’s various income streams, most of which could be considered passive income that accounts for about 20% of the millionaires in the United States.

It’s not hard to become a millionaire.

You don’t need any particular skill or education—just diligence. Every person who reads this can become a millionaire. Sound good? Great! Let us show you how to get rich.

Changing Your Mindset About Money

When you seek advice about asset building and money management, you may hear more about how to grow your capital than you do about how to change your thinking.

But, adopting the proper mindset is critical if you are serious about investing.

Without this shift in mindset, all the rest falls flat.

So, what is it that sets investors apart from non-investors when it comes to thought process? Part of it is how they respond to stress and unexpected changes.

People who are successful with investments are far from obsessive. Instead, they react to changes and opportunities as they arise and allow their money to work for them.

Rather than checking numbers several times a day and making drastic changes based on minor market shifts, a successful investor thinks about his or her investments over many years.

Another characteristic of people who successfully build their wealth is a realistic viewpoint.

You cannot become a millionaire overnight unless you’re this guy who invented the shake weight…

The shake weight: America’s biggest inside joke since 2007.

Thank you, sir, thank you!

But the truth is, if you’re looking to get rich from a single, short-term investment, the odds are against you.

Building your capital while insulating yourself from risk takes time, a lot of time, and you must be prepared to take on investments for the long haul.

But where do we start?

Kill Debt

Not all debt is created equal, and tackling bad debt must be the first step before you start worrying about how to get rich.

High-Interest Debt

Bad debt is high-interest debt, which for most of us, means credit card debt. The average interest rate on an existing credit card is a little over 15%.

You aren’t going to get a 15% return in the stock market most years, but if you have credit card debt, you’re on the losing end of compound interest.

If you have credit card debt, it’s a personal finance emergency! Paying it off should be your priority, before investing or buying a house or any other financial goals you may have.

If you have a good credit score, consider getting a debt consolidation loan.

You’ll have debt, but the interest rate may be drastically lower than the rate on your cards, and that lower rate will allow you to save a lot of money and kill the debt faster.

You can get a variety of offers through Credible, and browsing them won’t impact your credit score.

If you can’t get a loan, use the snowball or stacking method to help you pay off the cards more efficiently.

Low-Interest Debt

Is debt from things like student loans, mortgages, and auto loans an emergency? Probably not.

Those things tend to have relatively low interest rates, and it can be argued that because time is such an important factor in investing, it’s better to invest than to rush to pay off low-interest debts.

What can we consider low-interest?

If we take the conservative average return you can get in the stock market, which is 7%, anything a few points lower than that will qualify.

That stated, lowering your interest rates on these and any debts will save you money. You can refinance your student loans, mortgage, and auto loans.

There are many variables, and doing so isn’t always the best choice, but it is something you should consider and research to find out if it makes sense.

Pay Yourself First

Aside from paying off high-interest debt, paying yourself first is the most crucial step you can take when you’re learning how to get rich.

Because if you don’t PYF, you may end up with no money to invest. It’s vital to underscore what this means when it comes to saving and investing.

Paying yourself first means prioritizing savings over discretionary spending.

Let’s say you have a weekly income of $800 and average weekly expenses (things like gas and groceries) that total $300.

In this example, paying yourself first means you contribute to your savings before you spend the extra $500 on discretionary expenses.

Developing the discipline it takes to pay yourself first is a process, so it’s helpful to use automation tools to hold yourself accountable.

You can set up automatic paycheck deductions for your 401(k) or IRA. You can also use a savings platform or application to set up automatic savings contributions.

If you struggle to save, but you know that your spending is higher than it should be, it’s essential to put things in perspective.

Instead of thinking about the items you want now but have to refrain from buying, think about the quality of life you will be able to enjoy later on in life thanks to your hard work and commitment to savings now.

Delayed gratification is a substantial part of building wealth.

You can pay yourself first by contributing to a retirement investment account, an investment portfolio, or your emergency fund.

The important thing is not how you’re saving, but that you are saving.

Fiscal flexibility that’s funny, free and delivered weekly.

Start Investing Early

The earlier you invest, the more time you’ll have to build your wealth, and the more likely it is, you will find success.

The truth is that it’s never too early to start investing for your future—but it can be too late.

Giving yourself decades to invest allows you to weather the downward turns that the market may take and hold out for positive market changes.

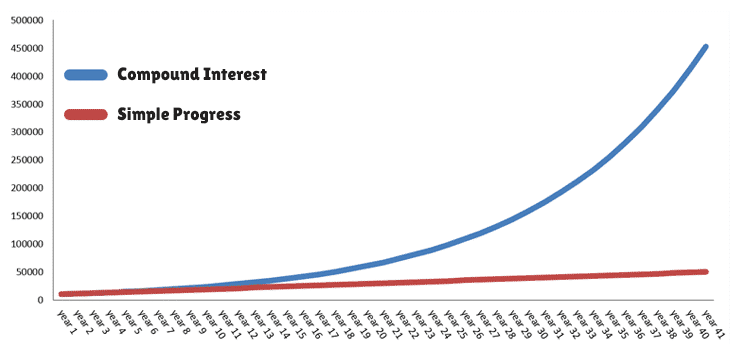

It also allows for the magic of compound interest to kick in.

If you don’t give yourself enough time to invest strategically, you are more likely to suffer in a market dip without reaping the benefits of the eventual market climb.

If you needed your retirement funds at the height of the 2008 financial crisis, you were hurting. However, if you simply weathered the storm and sat tight, you’d be well above your pre-2008 highs.

There are many reasons why it’s beneficial to start your investment journey early on if you want to learn how to become rich. These include the following:

Benefit From Compound Interest

Compound interest is money earned on interest. In other words, it gives you a financial boost for reinvesting your money.

The earlier you start your investments, the more interest you will accrue, and the more compound interest you will earn.

Opportunity to Take Risks

Some of the most lucrative investments also have the highest risk associated with them.

Although it’s essential to understand the extent of any risk you assume, taking calculated risks can be highly beneficial.

If you’re investing short term, you probably don’t have enough time to recover from risky investments that go south, which could leave you with even less capital than you started with.

More Time to Develop Good Financial Habits

It takes time to learn positive spending and budgeting habits, but you have to start somewhere.

Many people find that their spending and other financial behaviors improve as they begin to think about investments and long-term financial planning.

Good habits help build more good habits.

An excellent way to start is by tracking your spending habits with a tool like Mint. Or you can use the good old refrigerator method.

Better Long-Term Success

Investing is all about planning for your future—and your future will be far more secure if you start investing earlier.

Giving yourself more time allows you to build your investments effectively to enjoy the quality of life you want throughout your working life and retirement.

Know Your Numbers

What gets measured, gets managed.

Your Monthly Expenses

How much money do you spend every month, and what are you spending it on? You probably aren’t 100% sure, and that means you probably have spending leaks.

Use Mint to create a budget.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

A budget isn’t something only poor people use. Everyone needs to know where their money is going.

Go through your transactions monthly and cut unnecessary spending. Not all of it. Life isn’t worth living if we can’t spend the money we work hard for on some pleasures.

But eliminate or trim stuff (like restaurant spending and the various subscription services) you pay for but don’t need or use often.

Your Credit Score

A credit score tells potential lenders how likely or unlikely you are to pay back borrowed money. Day to day, your credit score doesn’t matter much, but it matters a lot when it matters.

The better your credit score, the cheaper it is to borrow money. In other words, the lower the interest rates you’ll be offered. And one of the most expensive things in life is interest.

What credit score do you need to get the best rates? Anything above 760 will do. If you’re not quite there, start working on improving your credit score.

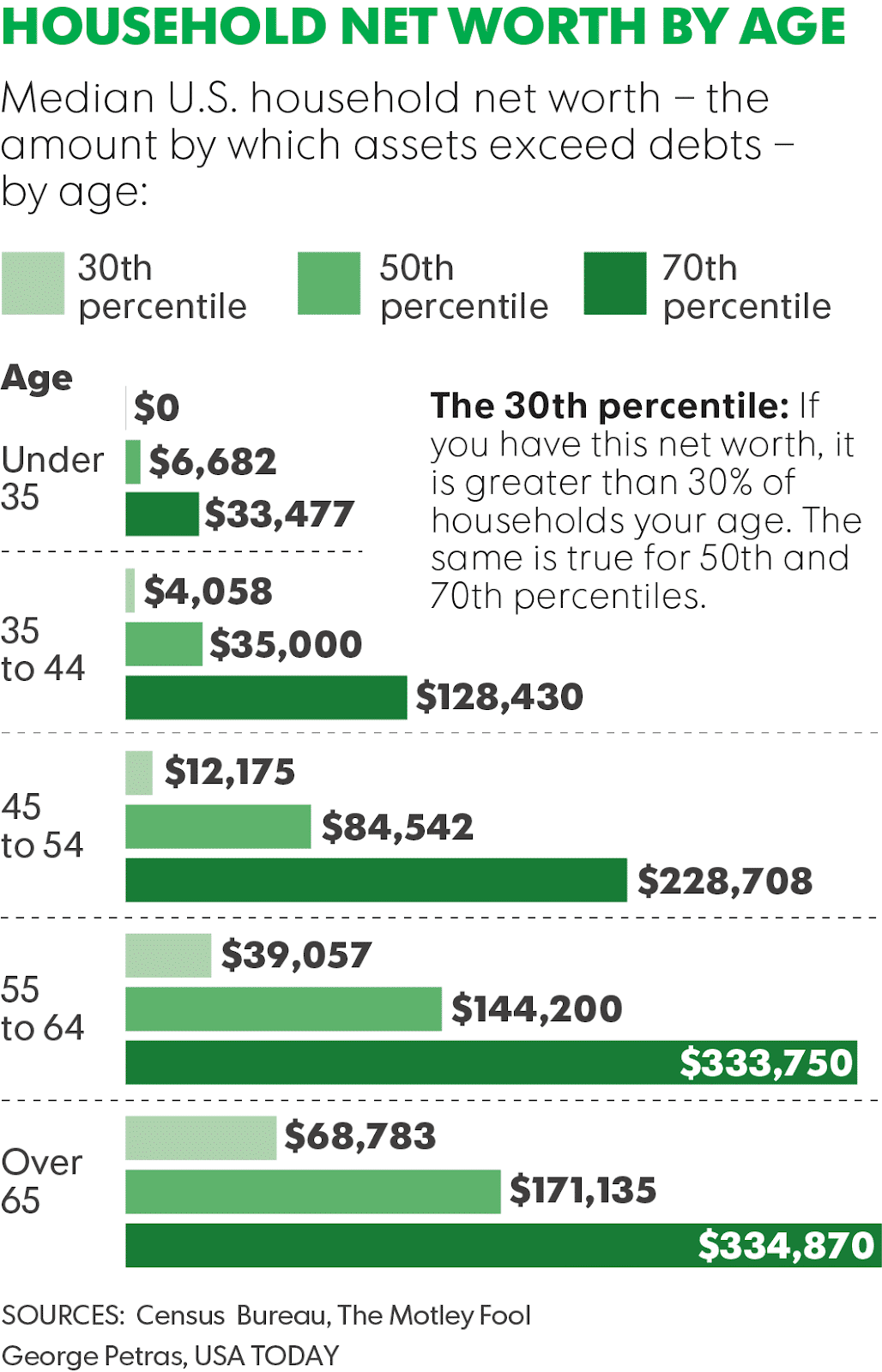

Your Net Worth

While every person is unique, having some kind of metric to weigh your financial health against your peers can be helpful.

If you are ahead of the game, this information will affirm you’re on the right track.

If you’re lagging, it might just be the motivation you need to make some necessary changes.

One of the ways you can look at your financial health from those around you is via net worth. It’s a calculation that includes all of your liabilities subtracted from all of your assets.

Take account of your assets, including your savings, your home equity, and your valuable possessions, and then subtract liabilities such as loans, lines of credits, and other debts.

The average net worth for an American under age 35 is $6,676.

By age 40, that figure climbs to $35,000 and up to $84,542 by age 50. At age 60, right about when most people are starting their retirement, the average net worth is $143,564.

If you are looking at these figures and feeling wholly inadequate when it comes to your net worth, you’re not alone.

Thinking about saving so much in just a few decades can be daunting.

The good news is that it’s possible as long as you put healthy financial habits into practice and invest your money wisely.

It can even provide you with a path when determining how to become a millionaire in the long term.

Early on in your career, your choices form the basis for your future financial successes and failures.

To get started on the right track, it’s good to have about half of your annual salary saved by the time you’re 30.

If you make $50,000 a year, your goal by 30 should be to have $25,000 saved.

Start now!

Use a tool like M1 Finance to open up a savings account and start socking money away.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

If you’ve already passed the age of 30 and don’t have this level of savings, there’s no need to worry—a late start is better than no start.

Establish a budget that allows you to maximize the amount you can save.

Avoid discretionary spending and try to make cuts where you can. Again, this is a crucial tip when figuring out how to become rich.

Read More and Educate Yourself

If you want to learn how to ski, your first step wouldn’t be to hit the slopes at the Winter Olympics.

Investing is not about chance—it’s about strategy. To invest and save effectively, you must take advantage of the information available to you.

You don’t need a Ph. D. in Finance to become a successful investor, but you can’t be completely ignorant about it.

If you’re genuinely wondering how to get rich, look to sources of information that detail strategies and sound investment advice.

A prospective skier might look to the advice of Bode Miller to improve his or her form, while those who aim to improve their financial health may take advice from a podcast like Listen Money Matters, or other kickass free online resources.

You won’t be able to effectively navigate the financial world unless you’re familiar with the various factors at play.

If your eyes glaze over when you hear words like securities, mutual funds, and asset allocation, it will help you to brush up on your investment literacy.

Read some books about investing or check out some trusted resources online.

Emulating success stories is important, but you should also try to learn from the failures of others. Make sure you are aware of the common missteps that befall investors so you can avoid them.

Think About Passive Income

Passive income allows you to collect money overtime on an investment or type of work that you’ve already completed.

For example, purchasing a home and renting it out is a way to collect passive income. In this example, you benefit indefinitely from a one-time investment of initial time and money.

If you don’t have the kind of capital it takes to purchase property, you can still create passive income with a smaller investment of time and money. Below are some ideas:

Rent a Room

If you have an extra room in your house, you could be pulling hundreds of extra dollars per month in rent. It’s a great option to develop a stream of passive income.

You may be able to benefit significantly from this option, especially if you live in a high-demand rental market, and your home is in a good location.

Crowdfunded Real Estate

You don’t have to purchase a whole property to get involved in real estate investing.

Crowdfunded real estate allows you to benefit from real estate returns without buying a home or commercial property outright.

There are a variety of resources available for people who want to invest in crowdfunding, including Fundrise.

Diversify into income-producing real estate without the dramatics of actual tenants. Fundrise eREITs are a diverse family of funds, each of which pursues a focused real estate investment strategy.

Disclosure: When you sign up with this link, we earn a commission. All opinions are our own. I am an investor with Fundrise.

Peer-To-Peer Lending

Individuals who cannot get approved for loans through traditional financial institutions and lenders often turn to alternative financing sources, such as peer-to-peer lending.

Because these tend to be higher-risk loans, interest rates typically range from 6 to 10 percent.

You can use programs like Lending Club to get involved with peer-to-peer lending quickly and easily.

Start a Business

For many people, working for someone else for the duration of their lives is entirely discouraging. Working for someone else inhibits your freedom, and it can also prevent you from reaching all your financial goals.

When you think about how to become a millionaire and get rich, it’s crucial to think about adjusting your career trajectory to accommodate your goal.

Sometimes, the best thing you can do for your financial future is to establish a business that you can run part-time and on the side, in the beginning.

The best way to start a business is to pursue a field that you are passionate about and develop a product or service that fills a need.

If you’ve always been a music lover, but your career is in technology solutions, consider starting a company that deals with the development of music software.

If you’re a good writer, consider starting a freelance business by taking odd jobs on freelance websites like Upwork, Fiverr, or Freelancer.

Sell your skills and get paid using Fiverr's platform. It's free to join, has no subscription cost, and has over 200 marketable service categories. Create a gig, do the work, and earn money.

Even though you might not be able to quit your day job and run your business full time right away, you will be able to build your profits as time goes on as long as you have a marketable product, and you make the necessary investment of time and energy.

Speak to friends or advisors you trust to determine whether the business concept you have has potential. Unfortunately, even great ideas may not be profitable.

It’s essential that you consider your business’s long-term financial viability before you choose to quit your current job and commit to being a business owner.

The key is it should cost you minimal upfront, and if it crashes and burns, you aren’t living on the street.

At least you learned something, a calm sea never made a skilled sailor!

Staying Wealthy

If you follow the advice here, you will get rich. But how do you stay wealthy? Rich people are flashy with their money. We see this a lot with lottery winners.

They buy everything they ever wanted and don’t stop until the money runs out. And it often does.

Lottery winners are more likely to declare bankruptcy within three to five years than the average American.

You stay wealthy the same way you got rich; by spending considerably less than you have and continuing to invest wisely. That’s it.

Much like getting rich, there is no sexy secret to staying wealthy.

It Is Possible

Becoming wealthy isn’t simple, but it’s possible (if you have the courage and commitment to work at it).

Start by educating yourself and implementing healthy financial habits to get yourself off to a good start.

With the right strategy and the right resources, you can figure out how to become a millionaire. But not overnight.

Fiscal flexibility that’s funny, free and delivered weekly.

Current Project: Making bloggers money with Lasso.