Crafting a monthly budget is a crucial aspect of managing personal finances. A monthly budget can show where you’re overspending, where you need to make adjustments, and how far along you are toward reaching your financial goals. We’ll show you how to budget painlessly!

Everyone needs a budget, no matter how much or how little money you make. A budget does a lot more than track spending. A good budget can help you absorb unexpected expenses like car repairs and medical bills.

A monthly budget can help you find extra money for your savings goals. Essentially, a budget shows how much money is coming in, how much is going out, and where it’s going.

What gets measured gets managed.

Tweet ThisAttempting to achieve your financial goals without a budget is akin to navigating to a destination without a map—or Google Maps, in today’s world. While you might eventually arrive, the journey will likely take longer and cost you more money.

Don’t think of a budget as a punishment, this thing that is stopping you from spending your money the way you want. Nothing can do that, not even the world’s greatest budget.

Instead, think of a budget as a tool that will help you reach your financial goals.

How Do I Make A Monthly Budget?

The great news is, that with the abundance of excellent budgeting tools now available, you’re no longer limited to an Excel spreadsheet for managing your finances. Budgeting apps have modernized the process, bringing it squarely into the current millennium.

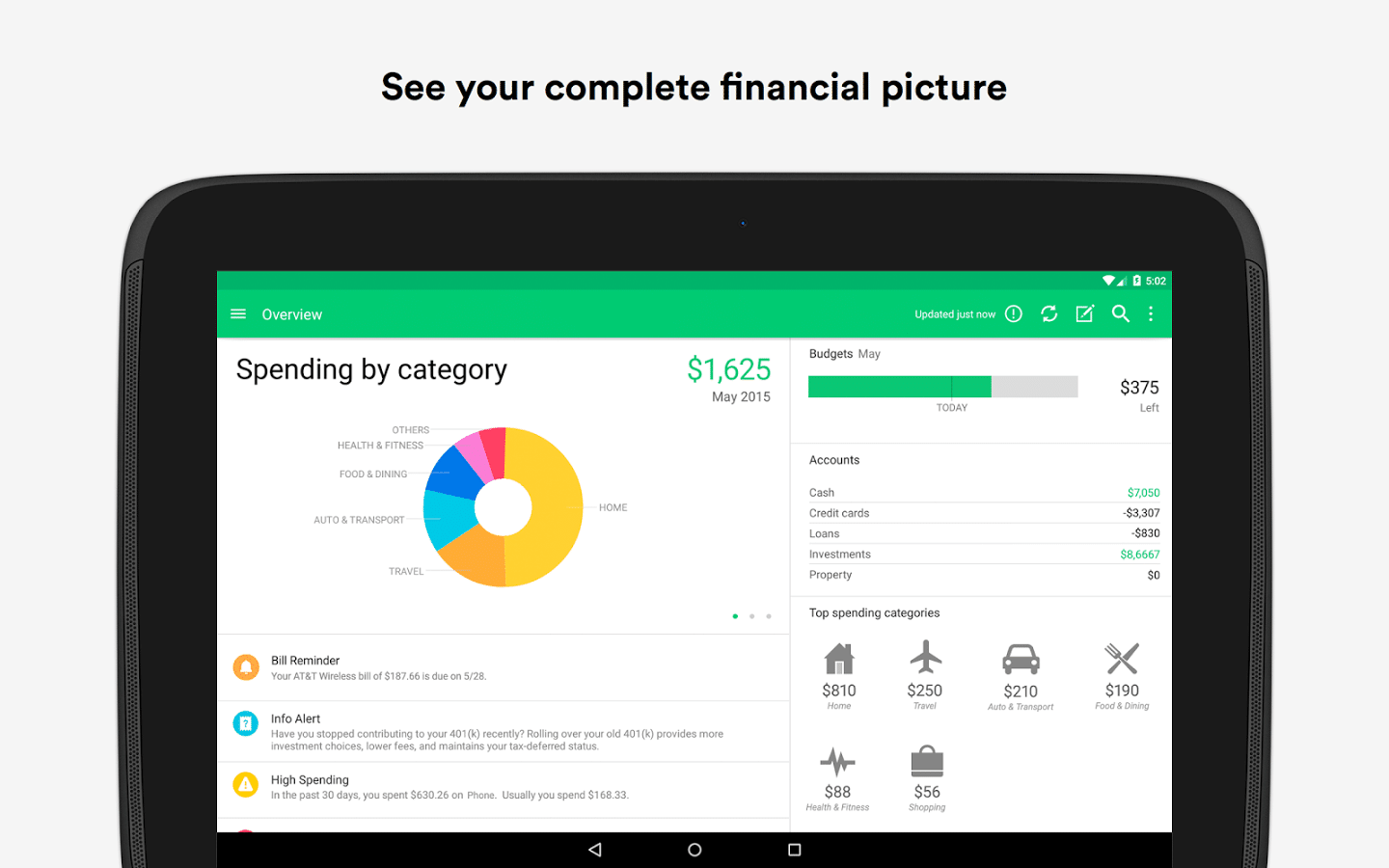

Mint

Mint offers a fantastic solution to make budgeting effortless, eliminating the need to manually review bank statements each month to track spending.

By creating an account and linking your bank and credit card accounts, Mint automatically imports your transactions and categorizes them on your behalf.

While it may require occasional adjustments, Mint generally categorizes transactions accurately, streamlining the budgeting process significantly.

We wrote a book on how to make a budget with Mint!

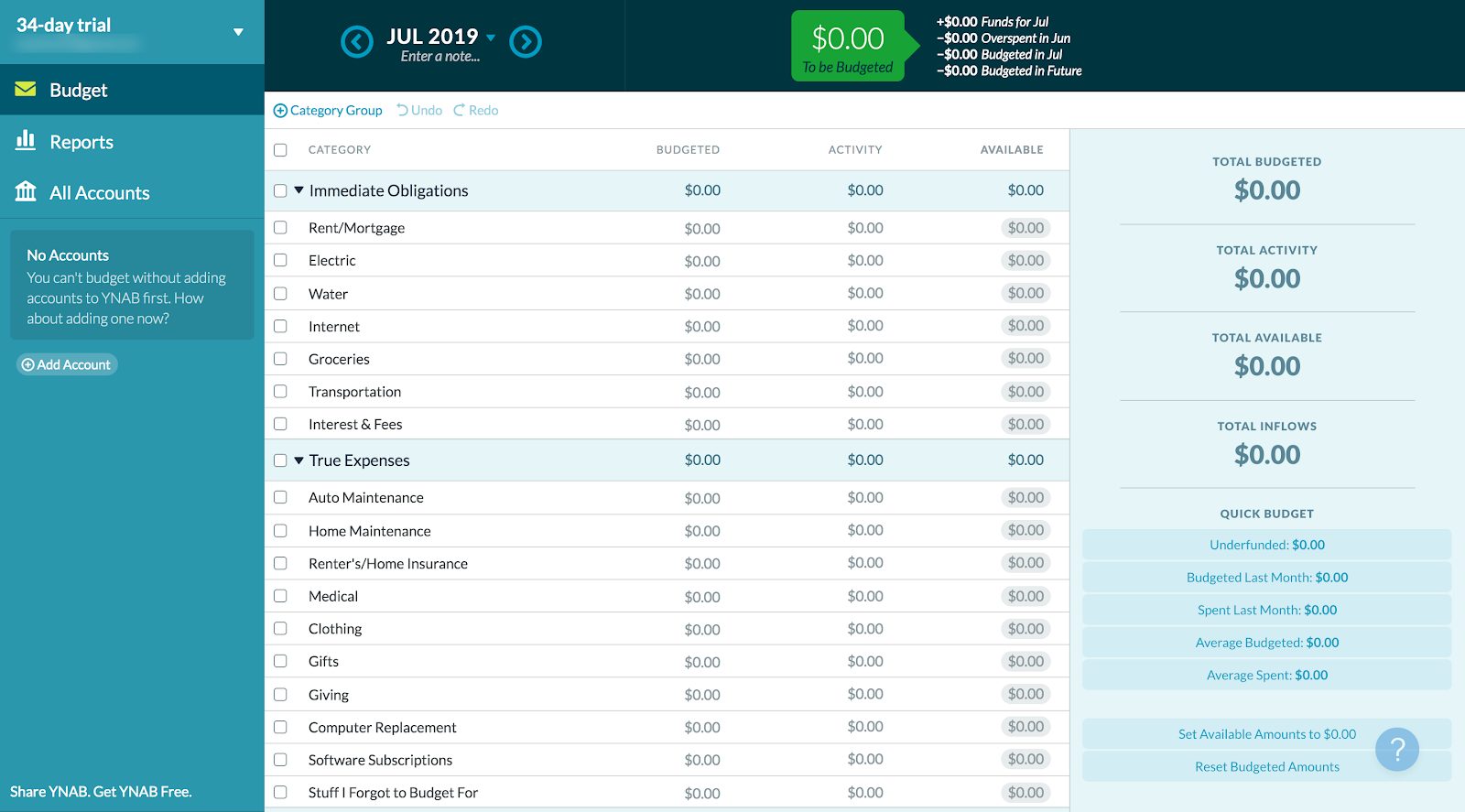

You Need A Budget

We love Mint for its budgeting capabilities, yet there’s a superior tool available for those with irregular income. If your monthly earnings fluctuate due to a side hustle or a commission-based job, such as in real estate, you might find this alternative more suited to your needs.

If that’s your situation, Mint and similar budgeting apps might be more challenging to manage. However, You Need A Budget (YNAB) could be exactly what you’re searching for.

YNAB uses a method known as Zero-Based Budgeting.

Zero-based budgeting is a method that encourages you to allocate every penny of your monthly income toward expenses, savings, and debt payments. That means giving every dollar a job. In other words, only budget what you have right now.

If your income is irregular, you will budget the money you made last month with YNAB for the upcoming month since that’s the known quantity.

YNAB has a steeper learning curve compared to Mint, and it may require a month or two to effectively implement its zero-based budgeting system. However, it’s the optimal monthly budget system for those with fluctuating take-home pay.

The Envelope System

If you find your spending habits are a bit out of control and previous budgeting methods haven’t worked for you, the envelope system could be the answer.

This method isn’t necessary for essential expenses such as housing and utilities, as these typically aren’t the areas where overspending occurs.

Instead, use the system for variable expenses prone to overspending, such as food, entertainment, and drinks. Label each envelope with the category of spending and allocate the budgeted amount of money to each.

A weekly setup is more effective than monthly, as carrying large sums of cash isn’t advisable. Whenever you purchase in any category, use the cash from the corresponding envelope.

Once an envelope is empty, you’re done spending in that category. Simple!

You can do this the old-fashioned way with actual envelopes, but there is a budgeting app that simulates the envelope system – Goodbudget.

What Is a Good Budget?

A good budget is one you can adhere to! While that may sound a bit simplistic, there’s much more to crafting an effective monthly budget. Let’s delve into some fundamental budgeting principles and share a few practical budgeting tips.

Be Realistic

If you’re carrying debt from credit cards or student loans, creating a budget to swiftly eliminate that debt is a wise decision. Paying off debt is crucial, as the funds used for debt payments could otherwise be saved. Moreover, high-interest debt constitutes a financial emergency.

Going for a super tight budget can backfire because it doesn’t leave wiggle room for surprises or fun stuff. If every penny is accounted for, unexpected bills or the occasional treat can throw the whole thing off track.

Sticking to a super strict budget can get old fast, making it tempting to just ditch it. A little breathing space in your budget can keep you sane and on track. A budget, like a diet, that doesn’t allow for any wiggle room, or any pleasure is not sustainable.

If you try to implement a budget that is too strict, you’ll fail.

Make Adjustments

Your first budget should not be your last budget. A budget is a fluid thing, and you should make changes to it as your financial situation changes.

If you get a substantial raise, you don’t want to just put any money left over after your monthly expenses into your savings account. You want that money to work for you.

It’s a Team Sport

If you live with a partner or spouse, budgeting becomes a team sport. The two of you have to agree on how you’re going to budget your money.

It’s not necessary to agree down to the last penny, but achieving agreement is essential. Without it, you’re likely to face many fights over money.

Budget for the Unexpected

How do you budget for the unexpected when you can’t predict the cost of unforeseen events? The solution lies in allocating a portion of your monthly budget to an emergency fund. This fund is your safety net for handling unexpected expenses. But how much should you save?

Ideally, your emergency fund will contain 3 to 6 month’s worth of necessary expenses.

That’s a lot of money, and while you don’t need to come up with it within two months, prioritizing it as a top savings goal is crucial. An emergency fund can be a lifeline, preventing a severe financial crisis.

Budget for the Expected

By expected, we mean expenses that may not be monthly but they are regular. These can be things like your property tax bill, a yearly family vacation, or Christmas.

Many are caught off guard by expenses that recur regularly, though not monthly. Yet, these costs are predictable. By budgeting a small amount each month for these expenses, you can manage them more easily, avoiding financial surprises.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

How To Get Started Budgeting

Don’t be intimidated if this is your very first budget! Budgeting isn’t complicated or time-consuming. Follow these steps, and you’ll be a budgeting pro in no time.

Choose Your Tool

We explained a few different budgeting tools above. Mint is free to use, and

Try a few options out until you find the one that works best for you.

Gather Necessary Information

If you’re going to use budgeting apps, you’ll need to provide them with some information like account information for bank accounts, credit card accounts, student loan accounts, investment accounts, etc.

Have account numbers, user names, and passwords before you get started so you can get all of the necessary information entered quickly.

If you’re understandably nervous about handing over such sensitive information, do some research on the security measures these apps have in place to keep your data safe.

Make an Appointment

This only applies to those who share finances with a partner. Let them know that you want to work on a budget with them, tell them the information they need to provide (what we discussed in the above point), and schedule a time and day to sit down and create your monthly budget together.

Making a budget is not the kind of thing you should spring on your partner.

Make a List

Make a list of all of your income sources and all of your expenses. These things are going to be the entries you make in your budget, so again, you want to have them on hand when you sit down to create yours.

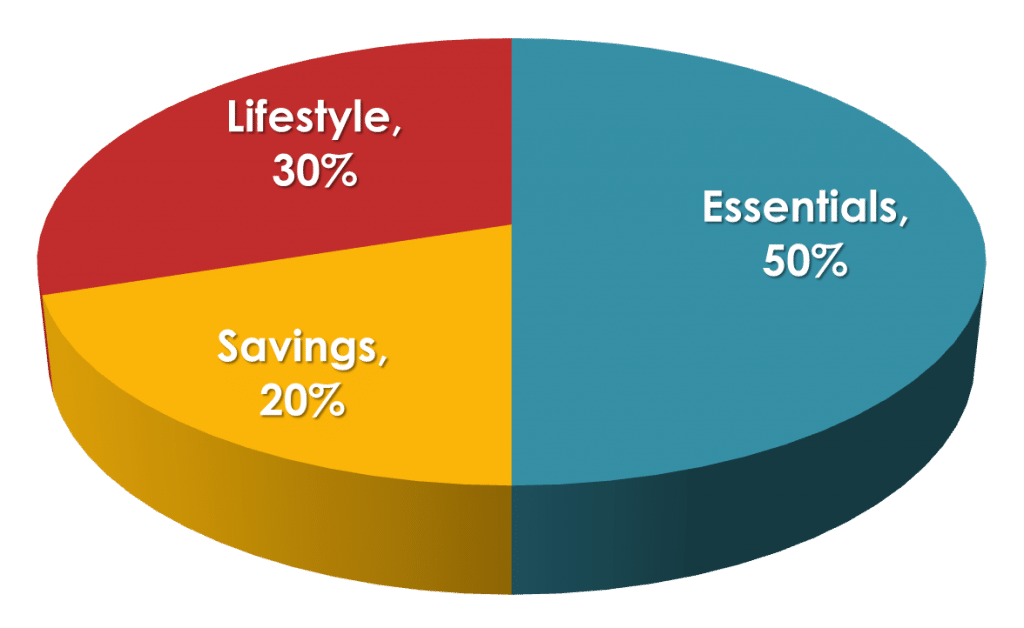

What Is the 50/30/20 Budget Rule?

What’s missing from the previous section? Indeed, guidance on how to budget your money! We’ve decided to dedicate a separate section to this crucial topic. Our approach is to keep things uncomplicated, and the 50/30/20 budgeting rule offers a clear, straightforward strategy.

Editor's Note

The 50/30/20 Rule doesn’t require creating detailed budget categories. It’s broken down into three broad segments, essential expenses, discretionary expenses, and financial goals.

This is a summary of the rule; we did a deep dive that will explain it more fully.

50%: Essential Expenses

Half of your net income is budgeted for things you must pay for, which can include:

- Housing

- Auto expenses

- Groceries

- Insurance

- Utilities

30%: Discretionary Expenses

Thirty percent of your net income goes to non-essential spending. This is the fun stuff like:

- Dining out

- Entertainment

- Drinks

- Gym membership

20%: Financial Goals

The final 20% is the most essential part of your budget and one that often gets overlooked. If you don’t budget money for financial goals, you may spend all of your monthly income. Financial goals include:

20/30

Instead of allocating 30% of your budget to discretionary spending, shift that percentage towards aggressively paying down your debt. This might mean temporarily reducing discretionary spending to 20% of your income.

It won’t be easy, but becoming debt-free is a worthy goal that will free up your finances in the long run.

That’s All There Is To It!

Creating a monthly budget is one of the fastest, easiest things you can do to take control of your finances and put yourself on the path to financial success. If you’ve been putting it off, use this guide to help.

The budgeting tool for the person that budgeting doesn't work for. YNAB has a unique approach that's based on forming positive habits. Their Four Rules will stop you from living paycheck-to-paycheck. It also supports multiple currencies!