Do you know your net worth, does it matter? What is tracking your net worth, worth?

There are many financial metrics to consider when it comes to managing your finances, and net worth is one of the key figures. But what exactly is net worth, and is it worth tracking?

What is Net Worth?

Net worth is simply your financial health snapshot. It’s calculated by subtracting what you owe (liabilities like loans) from what you own (assets like savings or a house). A positive net worth means you have more assets than you owe. Tracking your net worth helps you understand your financial progress over time.

To calculate your net worth accurately, you should show the value of your home and auto gross (full market value) as an asset and include any outstanding mortgage or loan balance as liabilities.

Assets for Net Worth Calculation

Assets represent all the valuable things you own that contribute to your financial well-being. To get an accurate picture of your net worth, it’s important to consider these assets. Here’s a breakdown of some common categories:

- Liquid Assets: Cash, checking, and savings accounts.

- Investment Accounts: Stocks, bonds, mutual funds, retirement accounts (like IRAs or 401(k)s).

- Real Estate: Your primary residence, vacation properties, or any other land you own.

- Tangible Assets: Cars, motorcycles, boats (anything with resale value).

- Valuable Possessions: Art, jewelry, antiques (things with significant resale value).

- Life Insurance Cash Surrender Value: This is the amount of money you’d get if you cashed out your life insurance policy before it matures.

While calculating your net worth, it’s important to consider what shouldn’t be included. Here are some items that typically don’t hold significant resale value and are excluded:

- Everyday Household Items: These include things like towels, furniture, and appliances. While they may have value to you, their resale value is generally low.

- Debts Receivable: Money owed to you by others is technically an asset. However, it’s uncertain when or even if you’ll be able to collect it, so it’s not typically factored into net worth calculations.

Liabilities for Net Worth Calculation

Liabilities represent all your financial obligations that you owe money on. To calculate your net worth accurately, you need to factor in these debts. Here’s a breakdown of some common liabilities:

- Credit Cards: The outstanding balance on your credit card statements.

- Student Loans: The total amount of money you borrowed for education, including any accrued interest.

- Car Loans: The remaining balance on your car loan.

- Personal Loans: Any loans you took out for personal reasons, such as home renovations or debt consolidation.

- Mortgage: The outstanding balance on your home loan.

In addition to these, other potential liabilities include:

- Medical bills

- Money owed to businesses

- Unpaid taxes

How to Track Your Net Worth

There are several ways to keep tabs on your net worth. Let’s explore some popular options:

- Manual Spreadsheet: This is a simple do-it-yourself method, but it can be time-consuming to update regularly. You’ll need to manually track your assets and liabilities and calculate your net worth yourself.

- Free Online Tools: Many websites offer free net worth calculators and trackers. These tools can simplify the process and provide basic insights into your financial health.

- Financial Management Apps: Tools like Monarch Money automate the process by aggregating your financial data from various accounts (assets and liabilities) and calculating your net worth. While some budgeting features within these apps might be free, in-depth functionalities may require a paid subscription.

Get clarity, confidence, and peace of mind for your finances. Track all of your account balances, transactions, and investments in one place.

Assessing Your Net Worth: How Am I Doing?

Understanding your net worth is crucial because it reflects your overall financial health—what gets measured gets managed. Without this number, you lack a comprehensive view of your financial situation.

Compare your net worth to benchmarks tailored to your age, income bracket, and financial goals, which can vary widely but are available from financial advisors and online resources.

Regularly updating these calculations and comparisons will help you gauge progress, identify potential issues early, and inform decisions to improve your financial standing. Adjusting for life changes such as marriage, home purchases, or retirement is also essential to maintain an accurate measure of your financial health.

Resources for Benchmarking Your Net Worth

Here are some resources to compare your net worth to benchmarks tailored to your age and income bracket (consider these as general guidelines, not rigid goals):

- LMM – How to Compare and Improve Your Finances by Age

- listenmoneymatters.com/average-net-worth-age

- Empower – The average net worth by age in America

- T.RowePrice – How Much Should You Have Saved

- SmartAsset – Average Net Worth by Age

Consider using salary as an indicator of financial health and progress. If you have steadily increased your income each year since you began working, it might seem like you are on the right track—the numbers continue to rise, after all.

However, salary is not the whole story. While you may receive regular raises, these increases can lead to spending sprees that subsequently inflate your credit card debt. Thus, a rising salary does not necessarily indicate financial health, as it reveals nothing about your debts or investments. This oversight can lead to a misleading sense of security and financial stability.

Self-worth and net worth are not the same.

Tweet This

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

Improving Net Worth

If your number is negative, don’t think beyond getting it to zero. As with any goal, you have to break a big task into a series of smaller ones. You might think to have a $0 net worth sucks, but that zero represents no debt!

If you have credit card debt, use the snowball or stacking method to attack it. Check your credit score. If it’s good enough, get a balance transfer card or take out a consolidation loan with Upgrade If it’s student loan debt, refinance for a lower interest rate with Credible.

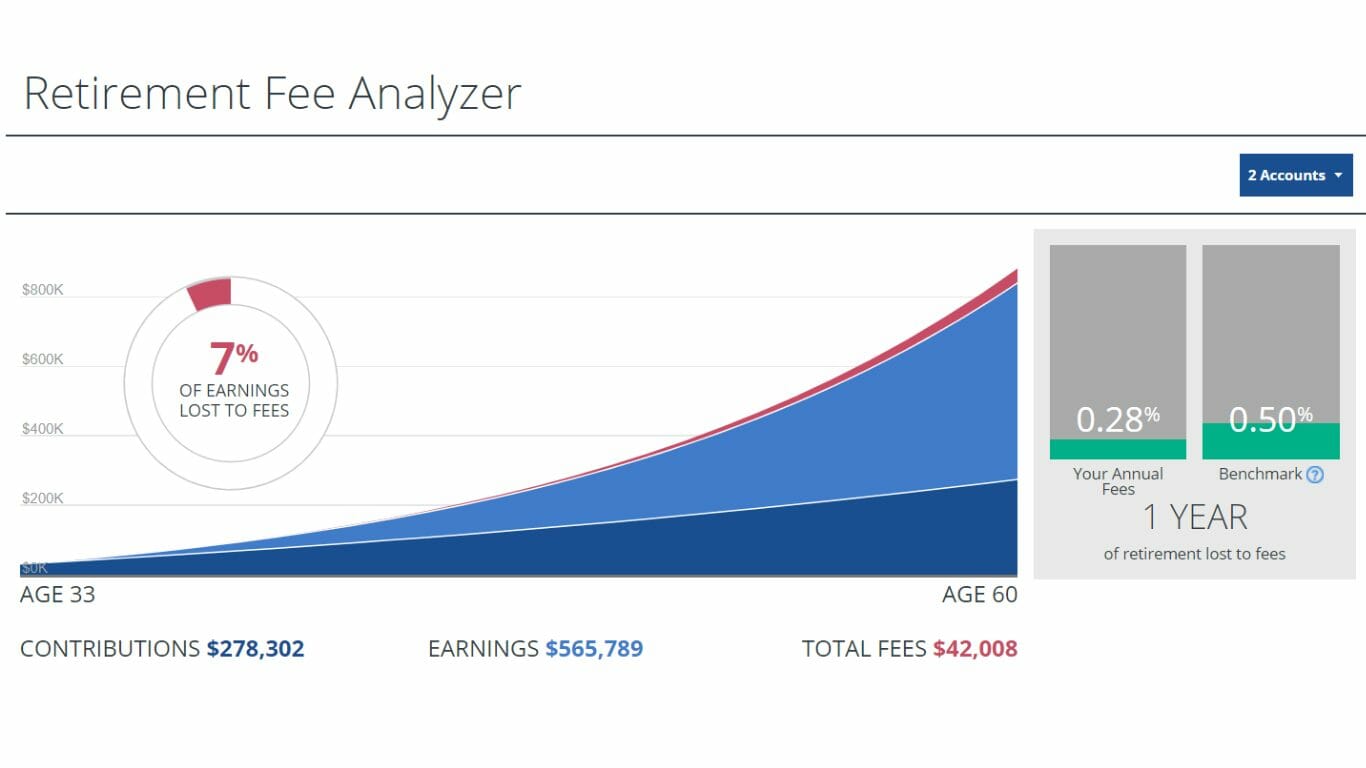

Over the decades, investing fees can eat up a considerable chunk of your net worth. Use Personal Capital’s Fee Analyzer to see how much you’re paying and the long-term effects.

Cut your expenses painlessly. Let Rocket Money cancel subscription services you don’t use and negotiate lower rates on some of your utilities.

If you’re not investing, what are you waiting for? You don’t have to be an expert to start investing with Betterment. If your employer offers a 401k, start contributing. These investments grow over time and are what is going to increase your net worth.

What are you doing in your free time to bring in extra money? Driving for Uber, working on your blog, babysitting? Most of us have more free time than we realize and you shouldn’t be wasting it watching TV or playing video games when you could be bringing in a little extra cash.

Checking In

Once you have the number, how often do you need to check it, every day, once a week, once a month? I know some of you love playing around with your numbers, you check your Mint, Betterment, and Credit Karma accounts every day.

Well, if that’s your idea of a hot Friday night, go ahead and add Personal Capital to your list!

If you’re struggling to stay motivated while paying off debt, it’s a good idea to check in whenever you need a boost, see the last paragraph.

For the rest of us, once a month at most and once per quarter at least. It’s a good idea to check it before making any biggish financial decisions. What should you do with your bonus or tax return? Pay off some debt or take a vacation?

My brother asked to borrow $5,000, should I loan it to him? I really want to buy a home, but I only have a 10% down payment which means borrowing a lot of money and paying PMI. Should I do it or save up longer until I have 20%?

Take the dollar amount of these decisions and apply it to the asset or liability side of your number and recalculate. How do you feel about what your decision does to that number? These kinds of decisions have a real impact on our finances, and sometimes we don’t fully see it. Seeing how it affects your net worth can really show you what the right decision is and what making the wrong one will mean.

A Little Lagniappe

Lagniappe is a New Orleans word that means “a little something extra.” I thought I’d share the little something extra reason I started tracking my net worth.

When I was in debt, I decided to tackle it once and for all. I used the snowball method and killed off a few of my smaller debts. Woo! I felt great.

But then I had to start tackling the more significant debts, which of course took much longer to pay off than those little ones. And I had already been paying off debt for several months. I was starting to lose motivation, always a dubious thing to count on when trying to achieve a goal anyway.

The number just didn’t seem to be going down at all. So I decided to start looking at a different number, my net worth. That number was going up a lot faster than the debt number was going down!

It gave me something else to focus on and seeing progress somewhere, anywhere! helped me stick to my snowball plan of action.

If you’re in debt and afraid to calculate your net worth, remember this little lagniappe. Watching that number get closer to zero lets you feel like you’re progressing. And once you’re part of the Zero Club, you can start growing that number up!

Show Notes

Schlafly Ibex Celler: A Barrel-aged Imperial Stout.

Armadillo Ale Works Brunch Money: An Imperial Golden Stout

Thank you to our sponsors: Ahrefs and Swap.com

Ahrefs is the secret to LMM’s success. They cover every aspect of SEO. If you want to start a blog or improve traffic to an existing one, this is the tool. You can win a free Lite annual subscription by tweeting @ahrefs and @MoneyMattersMan and telling us why you should be our winner.