- 1. Investing Is Why People Are Rich

- 2. You Need to Look at the Big Picture

- 3. Credit Cards Are a Godsend

- 3. Debt is The Devil

- 4. BANKS are the Devil

- 5. Mint Is Mint

- 6. I Don’t Need Everything

- 7. Staying Home is Okay

- 8. Education is Key (Books, not College)

- 9. Don’t Be Afraid to Ask For Money

- 10. Job Security is a Myth (except for teachers)

- 11. Owning a Home is Not For Everyone

- 12. Build an Emergency Fund for Peace of Mind

- 13. Junk Mail is Junk

- 14. Bad Habits are Killing You…Literally

- 15. Choose Your Friends Wisely

- 16. Do What Makes You Happy

- 17. Hobbies are Important

- 18. You are your own worst enemy

I’ve spent the past 30 years of my life being broke. Sure, I’ve had money, but the problem was I spent it all. This is how I went from a bachelor with his own home and a BMW to a bachelor living with his brother and a Honda Civic, and I couldn’t be happier.

I learned a lot over the last three decades, and I’m now a part of the personal finance world; if you had told me ten years ago, I would have laughed in your face. I was too absorbed in the “I have no money” victim lifestyle to see the bigger picture.

I want to share 18 lessons I’ve learned over the years of living paycheck to paycheck:

1. Investing Is Why People Are Rich

I don’t invest, but I know a lot of people who do, and they all have more money than me…a lot more money than me.

I tried my hand at investing. I bought stock in Sirius before Howard Stern joined — lost a shitload. I bought stock in Pandora — lost there too. I bought stock in Move Inc. — yep, you guessed it, LOST! I’ve had bad luck buying individual stocks.

I’ve since learned that if you want to invest to make a quick buck, that’s a bad strategy that rarely pays off. You should invest for the long term and keep investing. If you are new to investing, go into something simple, automated, and easy like M1 Finance.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

Traditionally when you wanted to invest successfully, you would do two things. First would be a ton of research, picking funds that diversify you enough so you won’t lose your life savings on a bad day.

You also try to make sure it’s aggressive enough, so you grow your investments over time. Nobody wants to miss out on the boom cycle or get destroyed by the bust cycle.

At its core, this is the problem

Another really easy way to get started is to set up a 401K with your employer.

You can also make it simple and start a Roth IRA if your employer doesn’t offer a 401k package. Invest in index funds or lifecycle funds.

These are bundles of stocks instead of individual stocks. No knowledge is required.

Remember, every day that goes by without investing is another day you’re not building wealth.

They're perfect for DIY investors who prefer a hands-off approach but can still pick individual stocks and funds. We specifically use them for the Golden Butterfly portion of our portfolio.

NOTE: Don’t withdraw all your money from your 401k account just because -you’re broke. Yep, I made that mistake too.

2. You Need to Look at the Big Picture

To manage money well, you must make good decisions. To make good decisions, you need accurate data, and it’s tough to do that if your debt, savings, and investments are all over the place.

Although some traditional financial planners can help you target your goals by evaluating your whole financial picture and building strategies tailored to your needs, they typically charge a boatload of money for their services.

The good news is you can do it yourself for free.

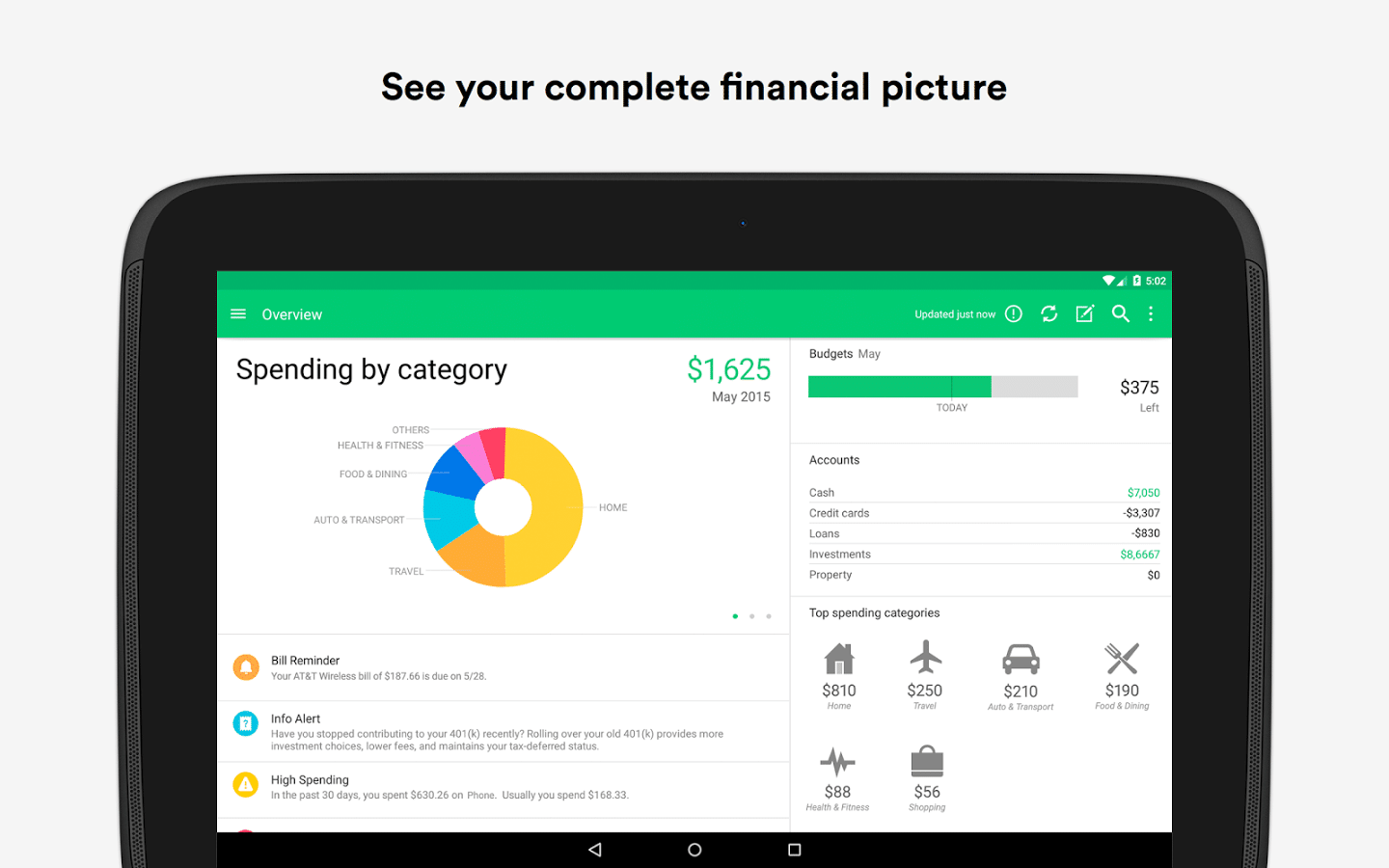

Personal Capital has a free money manager that will keep tabs on your income, expenses, and investments all in one place.

Once you link all your financial accounts, they lay it all out with pretty graphs and charts; it gives you an overview of your net worth, cash flow, spending, and investment allocation.

Tools to help you plan for retirement, monitor investments, and uncover hidden fees. Run simulations on your net worth and determine what it will look like after major life events.

This is our guide to budgeting simply and effectively. We walk you through exactly how to use Mint, what your budget should be, and how to monitor your spending automatically.

3. Credit Cards Are a Godsend

I was up to my ears in credit card debt if you’d known me years ago. When I was 18 years old, and my first credit card offer came in the mail, I jumped for joy and thought to myself, “Free money!”

Yes, the glow of a $500 credit limit was attractive, and I spent all of it on motorized water fountains for my desk…and probably Pez dispensers.

I never took advantage of credit card points and found myself in a seemingly never-ending battle with credit card debt.

I’ve since learned that credit cards are helpful if you use them correctly. Instead of racking up thousands in debt, I’ve paid them all off and only kept one I use for every purchase I make.

It allows me to rack up points and pay the card off every month. With cash-back points, I can now talk about “free money” and not sound like a freaking idiot.

3. Debt is The Devil

As I mentioned, I was in a lot of debt: credit cards, mortgage, car payments, etc. I spent everything anyone would give me, and I was good at it.

Unfortunately, that leads to a shit-ton of stress piled on with more pressure from everyday life. This is a terrible way to live.

Fortunately, I spent a whole year focused on paying off that debt. I’m still not finished because I still have a car and a mortgage, but my credit card debt is gone, and I can’t stress enough how good that feels.

NOTE: I don’t have any student loans because college wasn’t for me, so I can’t imagine having that debt weighing you down. However, if I did, I would do everything in my power to pay it off as quickly as possible. Perhaps a second job, even though I know, that’s not what you want to hear.

Credible's online marketplace connects borrowers with lenders in minutes. Refinance federal, private, and ParentPlus loans. Compare student loan refinancing rates from up to 7 lenders without affecting your credit score for free! Rates range from 5.24% to 12.44% APR

4. BANKS are the Devil

I had a checking account when I was 15 years old. I have switched to over five different banks in my lifetime, and each one was a nightmare.

My first bank was fine, but they were small and very inconvenient. I had a relationship with my second bank for over ten years, but they treated me like garbage because I didn’t know how to manage my money.

I paid so much in overdraft fees that it made me sick, and I spent hundreds to have an account with them.

I moved over to ING Electric Checking; not to go into too much detail, but I am no longer allowed to bank with them. I’ve been blacklisted.

The most recent bank began charging me a monthly fee to have an account because I’m no longer employed (like an average person) but instead work for myself. So now I’m switching to my fifth bank, which claims to have no fees.

I urge you never to pay bank fees. We recently recorded a podcast episode all about that topic.

The only savings account I have is Opportune, and it’s automated and adjusts to me because I’ll be damned if I need to revolve my life around a savings account.

5. Mint Is Mint

When I started as a reader of this very blog, Andrew reached out and forced me to create a Mint account, and it’s a good thing I did. I spent the time plugging in all my account information and debts.

I soon had a 50,000-foot overview of my spending habits, which made me sick.

However, having that view at your fingertips helps you to make intelligent decisions about where your money goes. It allowed me to plug spending leaks and pay off my debt faster.

Just the simple act of checking my Mint account every day was a reminder that I had to get in shape — like being naked in front of a mirror while standing on a scale.

Start using Mint, I urge you! In fact, we just launched our book Mastering Mint which is all about using Mint effectively. Check it out; it’s EPIC!

6. I Don’t Need Everything

I was an impulse buyer. If I wanted a new laptop, I’d go out and buy a new laptop. I never saved for anything in my life, and I would slap it on a credit card and pay it off later — or so I thought.

I bought a king-sized bed — I didn’t need it.

I bought a BMW — I definitely didn’t need it.

I bought a condo — I absolutely didn’t need it.

I didn’t need anything!

Buying stuff doesn’t make you happy; what you do with it does. I slept alone in my bed, drove to my tedious job in my BMW, and am now in a crazy amount of debt because of my condo.

Take stock of the things you already have. You probably have enough right now to be happy; if not, find out the things that genuinely make you happy.

Buying a new car won't make you happy if you have nowhere to go.

Tweet This7. Staying Home is Okay

I bought a very expensive condo and thought I better use it. I stayed home a lot, and you know what? It wasn’t that bad. I saved a ton of money by staying home and chilling with my dog, Reggie, and I didn’t miss out on much.

Instead of going out to dinner, I made my own EPIC dinners. If I was lucky, I had someone to eat it with.

Instead of going out to drink more beer than I should, I would invite friends over with beer and THEN drink more than I should. Safer too!

8. Education is Key (Books, not College)

At the beginning of 2013, I decided to become better with my money, so I read a bunch of books about the subject, including The Simple Dollar and I Will Teach You To Be Rich.

These books (and this blog) have seriously changed my life for the better. I no longer stress about money and think about wealth in a new light — none of which I learned from my years of “forced” education.

You don’t need to enroll in a university to be rich. Heck, you don’t need education to be rich (it’s my life goal to prove that). All you need is willpower.

You need to decide that you’re ready to be rich. Don’t be the guy who plays the lottery and expects luck and the gods to choose you; they won’t. Instead, man up (or woman up) and read a book…and this blog – we’ll stop you from being broke :-)

9. Don’t Be Afraid to Ask For Money

I’d be the guy who would work for free and never ask for payment because I was embarrassed.

You need to remember that money makes the world go round, and everyone knows it.

No one will be offended if you ask for money after doing something for it. I’m not saying you should stand out on the street and beg for change, but if you ever find yourself in that situation — and I genuinely hope that you never do — you need to earn the money you’re asking for.

If you feel underpaid at work, ask for a raise. Trust me; your boss won’t give you a raise if they don’t have to — no matter how great your work is.

You have to ASK and ask often. If you don’t get it, ask someone else who is more willing, even if that means switching jobs, which leads me to my next lesson…

10. Job Security is a Myth (except for teachers)

I need to get this tidbit out of the way: I have a slight hatred for teachers. There were only one or two teachers I can recall that helped me in a significant way. Every English teacher I’ve ever had (except Mrs. Beidka) failed me. It’s the reason I spent only three weeks in college, too — apparently, I was too creative.

Tenure doesn’t exist for the rest of us. We don’t get locked into our jobs after four years of doing it well enough not to get fired.

And even if you are the most outstanding employee the company has ever seen, a small budget cut can send you packing and last in line at the unemployment office — I should know.

Therefore, you need to think about your life as a whole and where you want to be. If you’re not where you want to be, move on. Keep moving; it’s perfectly okay. Don’t fall into the trap of being comfortable and scared or that it will look bad on your resume (that’s complete bullshit!).

Live your work life as if every day is your last — because it actually might be.

Work your way to the top, ask for more money, be agile, and you will succeed.

Tweet This11. Owning a Home is Not For Everyone

If you’re married with kids, it might be worth buying a home if you plan to live in it for 30 years and like the area. Otherwise, owning a home might not be the best move for you. I know it wasn’t for me.

I’m a bachelor who needs flexibility, and owning a home has been nothing but a headache and burden for the last five years. I’m not saying it will happen to you, but be aware of some of the facts about homeownership before you settle in:

- You need to fix things when they are broken.

- You need to do yard work if you own a single family.

- You need to pay property taxes.

- You need to sell it at some point (maybe).

These might not seem like bad things, but for me, they were, so be cautious of them. There is nothing wrong with renting. Right now, I rent, and I love it. I have little responsibility, and I can move whenever I want without dealing with the devil banks.

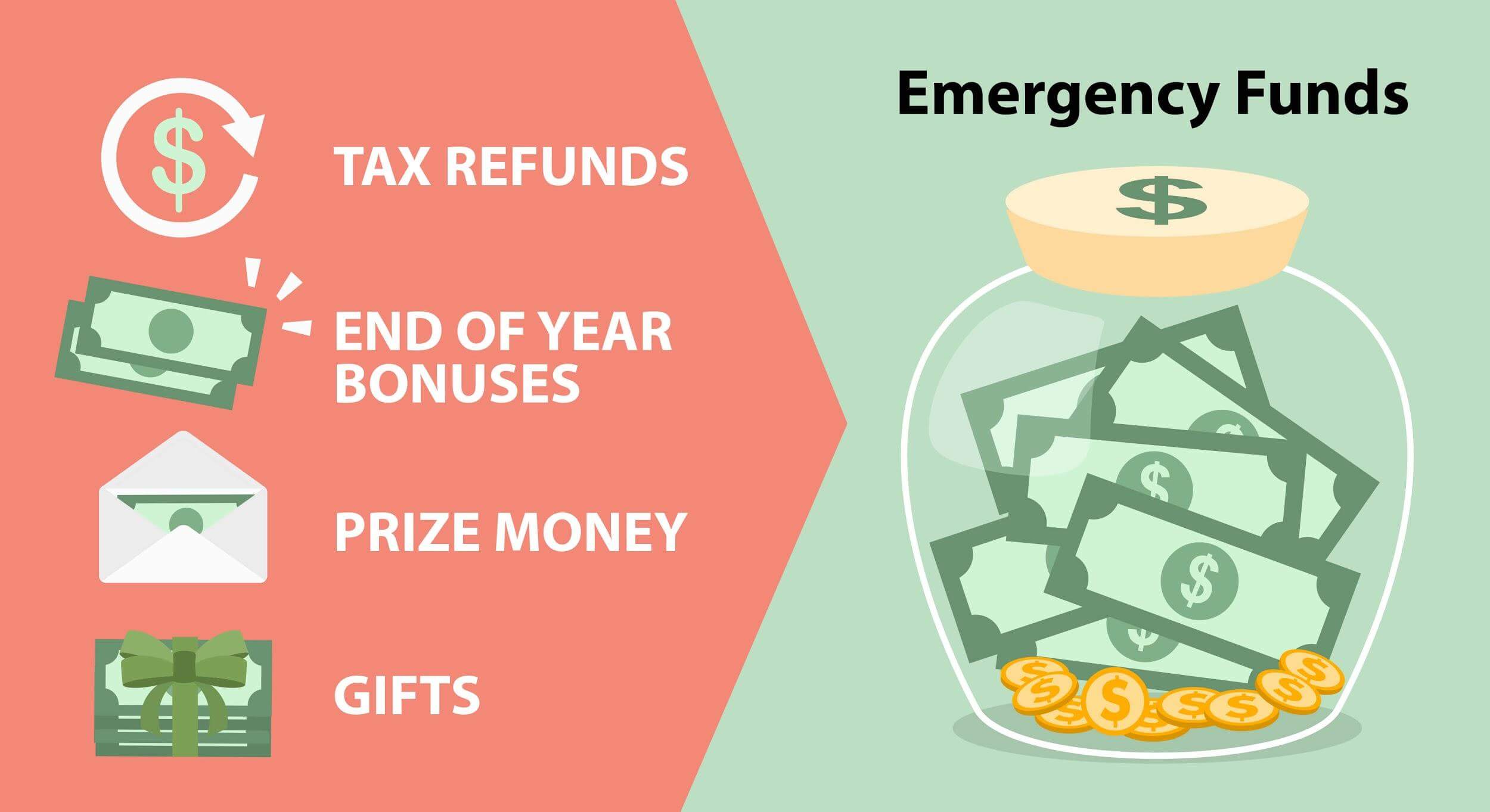

12. Build an Emergency Fund for Peace of Mind

I followed the philosophy of I could get hit by a bus tomorrow, so what do I need to save for? What a bad philosophy.

I spent 30 years without a backup or cushion to help get me out of a jam. The car breaks down? Put it on the credit card. I went over my cell phone minutes and put it on the credit card. Not good, friends. Not good.

I now have an emergency fund with about $2,000 that I never touch. It’s the “just in case” fund. I am having it will relieve stress in your life, even if you never have to use it.

You’ll want to put your emergency fund in a high-yield savings account.

13. Junk Mail is Junk

I would subscribe and signup for every offer that came in the mail. I would hold on to coupons for things I didn’t need. All of these things are worthless! If you want a credit card or a coupon, you’ll find it when you need it.

Also, you should NEVER take an offer from a credit card company that comes randomly in the mail. You should do your research and find the card that will work best for your situation and provides the best rewards.

The best advice would be to cancel junk mail as I did continually. You won’t miss it, I promise.

14. Bad Habits are Killing You…Literally

I used to be a smoker and a heavy drinker. Guess what? That’s not going to help you with your financial situation at all. Smoking costs a ridiculous amount of money (about $2,000 a year), not to mention the healthcare costs you’ll need later in life.

Drinking is the same. Even though I love my beer, I have cut back.

Cutting back on beer has helped me to lose weight, which will save you money — and I don’t get crazy hangovers all the time. Also, drinking costs more than smoking if you’re doing it a lot.

There are plenty of other habits that are killing you. Make a list of all the habits you’d like to stop and download the Coach. me App to track them. I wrote a whole post on this very topic.

15. Choose Your Friends Wisely

It’s been said that “you are the product of the five people you spend your time with,” and I take this to heart.

You need to make a list of your friends and put them into two categories: toxic and non-toxic (do yourself a favor and don’t tell people you’re doing this).

You’ll learn that some of the people you hang out with are not worth spending time with anymore. Maybe whenever you hang out with them, you come home feeling like shit (whether emotionally or because you’re forced to drink).

Perhaps all your friends do is spend money on frivolous crap, and you find yourself doing the same things. Stop it!

Surround yourself with people that truly make you happy.

Tweet This16. Do What Makes You Happy

I’m going to ask that you make a list of the things that make you happy. Not a mental list, but an actual list with a pen and a piece of paper. Write down things in life that you love and that don’t cost any money.

For instance, you could write: walking the dog, drinking coffee, or laughing. You can do these things if you have no money, and you’ll know they’ll make you happy. If you continue to do the things you love, Everything else won’t seem as important, like a BMW.

17. Hobbies are Important

I know some people with no hobbies, and when I ask them what they do to occupy their time, it’s usually TV. While I’ll admit that there’s nothing wrong with TV, I’d be mad at myself if I didn’t mention that I think it’s the dumbest thing you can do with your time — especially if you’re watching Here Comes Honey Boo Boo or Duck Dynasty.

Hobbies not only help your mind, but they will make you happy and, perhaps, save you money at the same time. Exercising, snowboarding, homebrewing, writing, or any activity that engages your mind or body is a better use of your time.

Dig deep into yourself and choose a hobby that you think will benefit you and make you smarter. I started brewing beer, which provides me cheap great-tasting beer and a wealth of math knowledge.

18. You are your own worst enemy

The only thing that’s holding you back from being wealthy is you. It’s not the government or where you live; it’s you. You need to quit blaming others (I know I have). I took it upon myself to be happy and wealthy, and so far, I’m achieving that with the lessons I’ve learned over the years.

I hate to say that it took me almost half a lifetime to learn (I think I’m old), but I’m glad I finally did.

These are just the lessons I’ve learned, so I hope you can share some of the ones you’ve learned, whether you are broke or not.

Fiscal flexibility that’s funny, free and delivered weekly.

I live South Jersey (actually, I just refer to it as Philadelphia). Follow me on Twitter and we can chat about pools, beer or internet marketing.