- An Emergency Isn’t a Catastrophe: High Urgency

- 3-6 Months of Living Expenses: This is a widely accepted rule of thumb. It provides a cushion to cover your expenses for several months if you face unemployment, medical emergencies, or other unforeseen events.

- Higher Amounts for Less Stable Situations: If you have a less stable job or significant variable expenses, consider having a larger emergency fund, perhaps 8-12 months of living expenses.

- Start Small and Build Up: Don’t feel discouraged if you can’t save the ideal amount right away. Begin with a smaller, achievable goal and gradually increase your savings over time.

- Keep it Accessible: Store your emergency fund in a liquid account, such as a high-yield savings account, so you can access the money quickly when needed.

- Review Regularly: As your income, expenses, and life circumstances change, re-evaluate your emergency fund needs and adjust your savings goals accordingly.

- Emergency Fund Account: Open a high-yield savings account specifically for your emergency fund. This helps you avoid accidentally spending the money.

- Automatic Transfers: Set up automatic transfers from your checking account to the savings account to build your emergency fund consistently.

- Creating a Budget is Your Friend: High Urgency

- Strong focus on zero-based budgeting, which can help gain control over spending.

- Collaboration features allow for shared financial management with a partner or advisor.

- User-friendly interface with customization options.

- Offers a 30-day free trial to test the features before committing.

- Spending is Optimized

- What’s Your Credit Score?

- Higher Credit Score, Lower Rates: In most cases, a higher credit score qualifies you for better interest rates on loans, including personal loans, business loans, car loans, refinances, and mortgages. Lenders see borrowers with high credit scores as less risky, so they’re willing to offer them lower interest rates.

- Savings Can Be Significant: Even a small difference in interest rate can save you a substantial amount of money, especially on large loans like mortgages. A 1% lower interest rate on a home loan can save you tens of thousands of dollars over the life of the loan.

- Improve Your Score: There are definitely ways to improve your credit score, even if it’s not currently at 760 or above. Practices like paying bills on time, keeping credit card balances low, and maintaining a healthy credit mix (both credit cards and installment loans) can all contribute to a positive credit history.

- Lowering Utilization Helps: Reducing your credit card utilization ratio (the amount of credit you’re using compared to your total credit limit) is one of the most impactful factors in improving your credit score.

- You Live Within Your Means

- Fun is Free

- Reducing Your Credit Card Debt: High Urgency

- Identify: List all your credit cards and their corresponding interest rates and balances. Focus on the cards with the highest interest rates first, as these are accruing the most significant charges.

- Debt Avalanche: This method entails making minimum payments on all cards while allocating extra funds to the card with the highest interest rate, then proceeding to the next highest after each is paid off, prioritizing long-term interest savings.

- Debt Snowball: This approach prioritizes clearing the card with the smallest balance first, creating a motivating snowball effect as quick successes keep you focused.

- Budget Review: Analyze your budget and identify areas where you can cut back on spending. Allocate the freed-up funds towards your credit card debt payments.

- Side Hustle: Consider taking on a side hustle to generate additional income specifically dedicated to paying down your debt.

- Negotiate: Contact your credit card issuer and inquire about a lower interest rate. Explain your situation and willingness to make consistent payments in exchange for a lower rate.

- Balance Transfer: Look for a balance transfer card with a 0% introductory APR (Annual Percentage Rate) period. This allows you to transfer your credit card debt to the new card and temporarily avoid interest charges, giving you a head start on paying down the principal balance. Be aware of any transfer fees and ensure you can pay off the balance before the introductory period ends to avoid getting hit with high interest again.

- Consolidate: Consider a debt consolidation loan to combine your high-interest credit card debts into one loan with a potentially lower interest rate. This simplifies your repayment process with a single monthly payment. Remember, this approach only works if the consolidation loan’s interest rate is lower than your existing credit card rates.

- Track Your Progress: Monitor your progress to stay motivated. Seeing the debt decrease can be a significant motivator to keep pushing toward your goal.

- Avoid New Debt: While paying off existing debt, resist the temptation to use your credit cards for new purchases. This can derail your progress and add to your existing debt burden.

- Student Loans are Manageable

- You Don’t Drive a Ferrari

- Or Live in a McMansion

- You Know Your Number

- You’re Investing For Retirement: High Urgency

- Investing For the Short-Term

- You Have a Little Real Estate

- You Know Your Worth

- You Have a Hustle

- You Have Some Financial Friends

- You and Your Partner Are on the Same Financial Page

- You Know How to Buy Happiness: High Urgency

Disclaimer: This article contains affiliate links, which means we earn a commission if you sign up through the link. This is a testimonial in partnership with Fundrise. I am a Fundrise investor. All opinions are my own.

Being financially stable will mean something different for everyone. Some people won’t feel financially stable until they have a few million dollars in the bank. Some of us will feel as though we’ve achieved financial stability with far less. Being financially stable isn’t just about how much money you have.

There are so many factors at play, which is reassuring, given that not everyone will become a millionaire, but achieving financial stability is possible for all. Certain steps are straightforward and can be completed in just a few minutes, such as checking your credit score. Others, like saving enough for retirement, may take years. And that’s perfectly fine. Consider this a checklist to gradually work through, serving as a roadmap to building a solid financial future.

The list might be lengthy, but none of the items are particularly challenging or beyond anyone’s reach. Many profit by convincing us that attaining financial security is so complex, that we need to buy their books, attend their seminars, and pay for their advice. However, personal finance isn’t as complicated as it’s made out to be.

To prove just how manageable it is, we’ll guide you through all the markers you need to achieve financial stability and demonstrate how you can accomplish each one. Ready? Let’s dive in.

19 Markers of Financial Stability

Financial stability hinges on key practices like maintaining a robust emergency fund, managing debts effectively, saving for retirement, and having a good credit score. It also involves smart investing, owning appreciating assets, and periodically revising your financial strategy. Meeting these criteria ensures you can handle financial challenges with confidence and secure your long-term financial well-being.

Saving

Americans are not saving enough money.

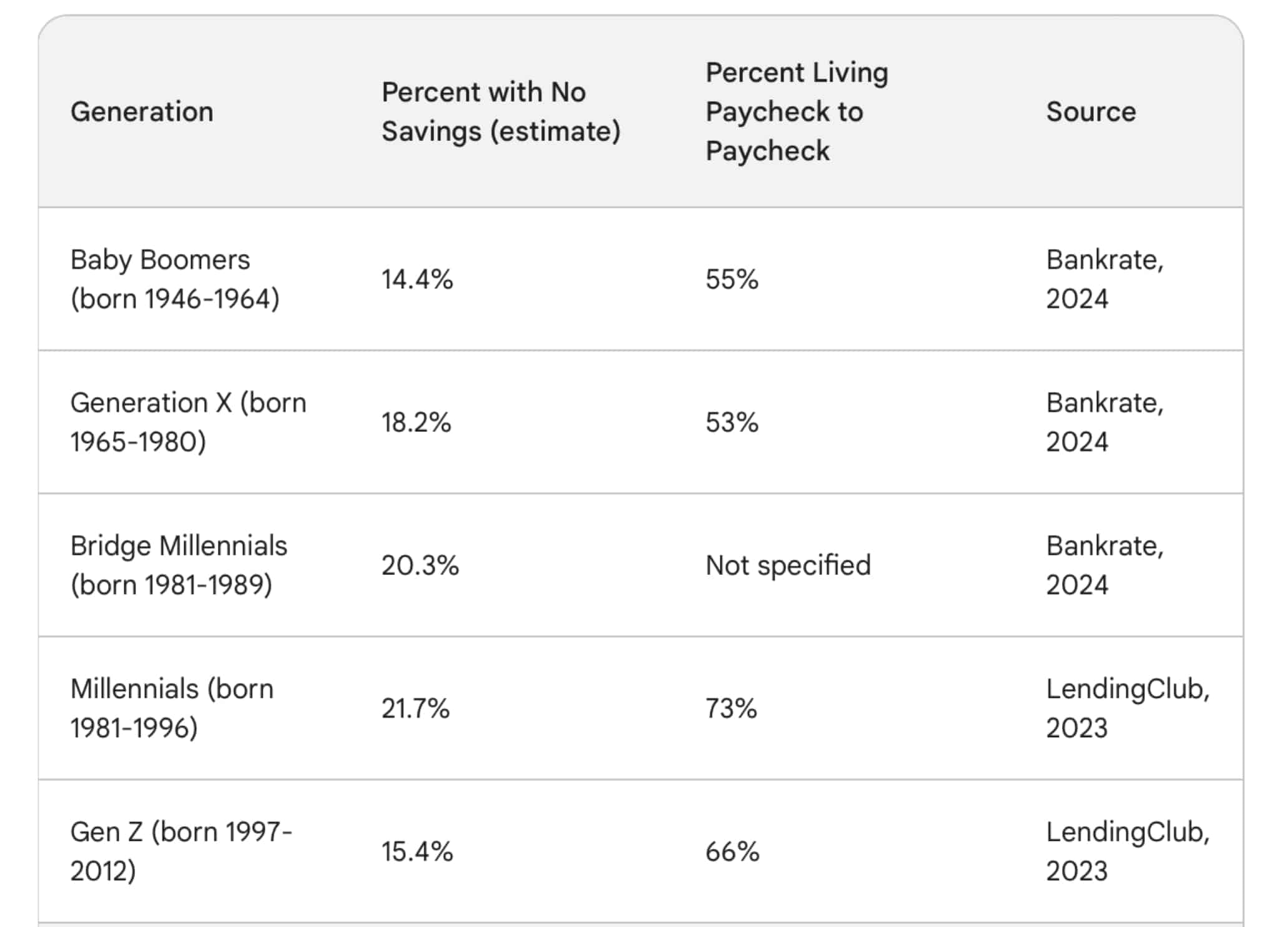

“Only 63% of American adults are able to cover a $400 emergency expense without going into debt or selling a possession, according to a 2022 Federal Reserve survey, it’s clear that many people don’t have enough funds saved for that inevitable rainy day. “

The statistics above are shocking but not necessarily surprising when you consider that 55% to 73% of Americans are living paycheck to paycheck. You can’t be financially stable if you’re not saving.

An emergency fund can mean the difference between a minor hiccup and a full-blown crisis. It provides peace of mind, ensuring you’re prepared for life’s unexpected moments. Need new tires for your car? Your emergency fund has you covered. Fall ill and miss work without paid sick leave? Thankfully, your emergency fund is there to help. This financial buffer turns potential disasters into manageable situations.

How Much Do You Need?

How much should you have in your emergency fund? That all depends on your individual circumstances. Some general guidelines are:

Additional Tips:

That is a lot of money for anyone to save, yet in the face of job loss, a minimal buffer won’t last. While building a 3 to 6-month reserve isn’t as immediate, it’s essential to pursue this goal diligently, ensuring you’re equipped for prolonged financial uncertainties.

Where Should You Keep Your Emergency Fund?

Deciding where to keep an emergency fund sparks much debate. The key is accessibility and maintaining value. We mentioned the high-yield savings account, but here is an approach that is straightforward and effective:

Accelerate your journey towards your financial aspirations with Premier Savings. Tailored to align with both your ambitions and lifestyle, this savings account offers an exceptional APY of 4.81% on balances exceeding $1,000. They value your hard-earned money by eliminating any monthly or annual account fees.

Where exactly is all of this money for your emergency fund coming from? You can often find at least part of it when you create a budget. Most of us spend way more than we realize and spend on unnecessary things. A budget will show you how much you’re spending and where you’re spending it.

Since Mint is no longer available, Monarch Money offers a compelling budgeting alternative, especially if you’re looking for a zero-based budgeting approach. This method, where you allocate every dollar to specific categories, can be more effective for controlling spending. Plus, Monarch boasts collaboration features and customization options not found in Mint, making it ideal for managing finances with a partner or for those who prefer a tailored budgeting experience.

We like Monarch because:

You can also consider You Need a Budget (great for those with irregular income), Empower, or a good old-fashioned spreadsheet.

Budgeting doesn’t have to be complicated. Use the 50/30/20 method. Once you have your budget set up, go through the last 1 to 2 months of transactions and see where you’re wasting money. Start cutting that waste and funnel that money into your emergency fund.

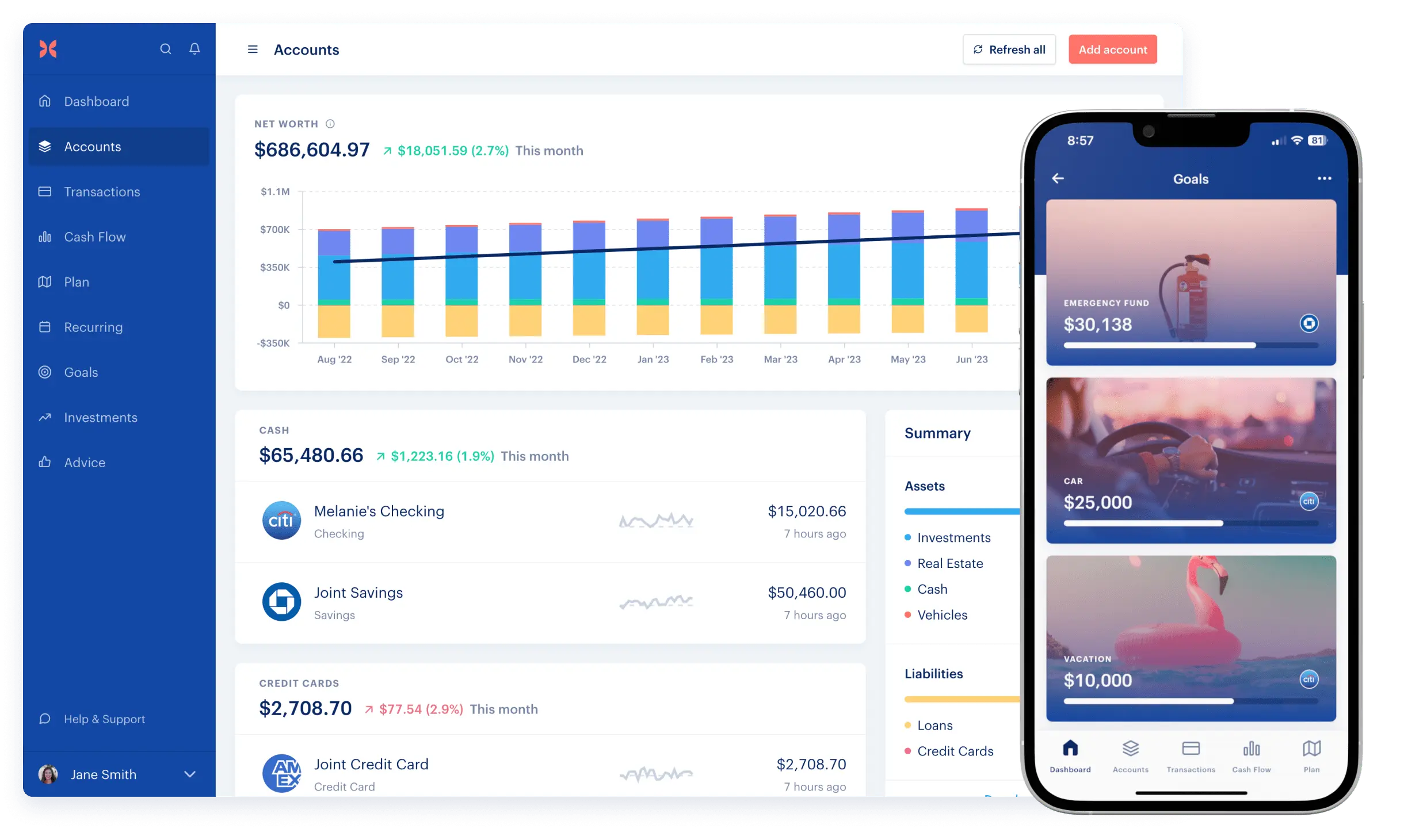

Get clarity, confidence, and peace of mind for your finances. Track all of your account balances, transactions, and investments in one place.

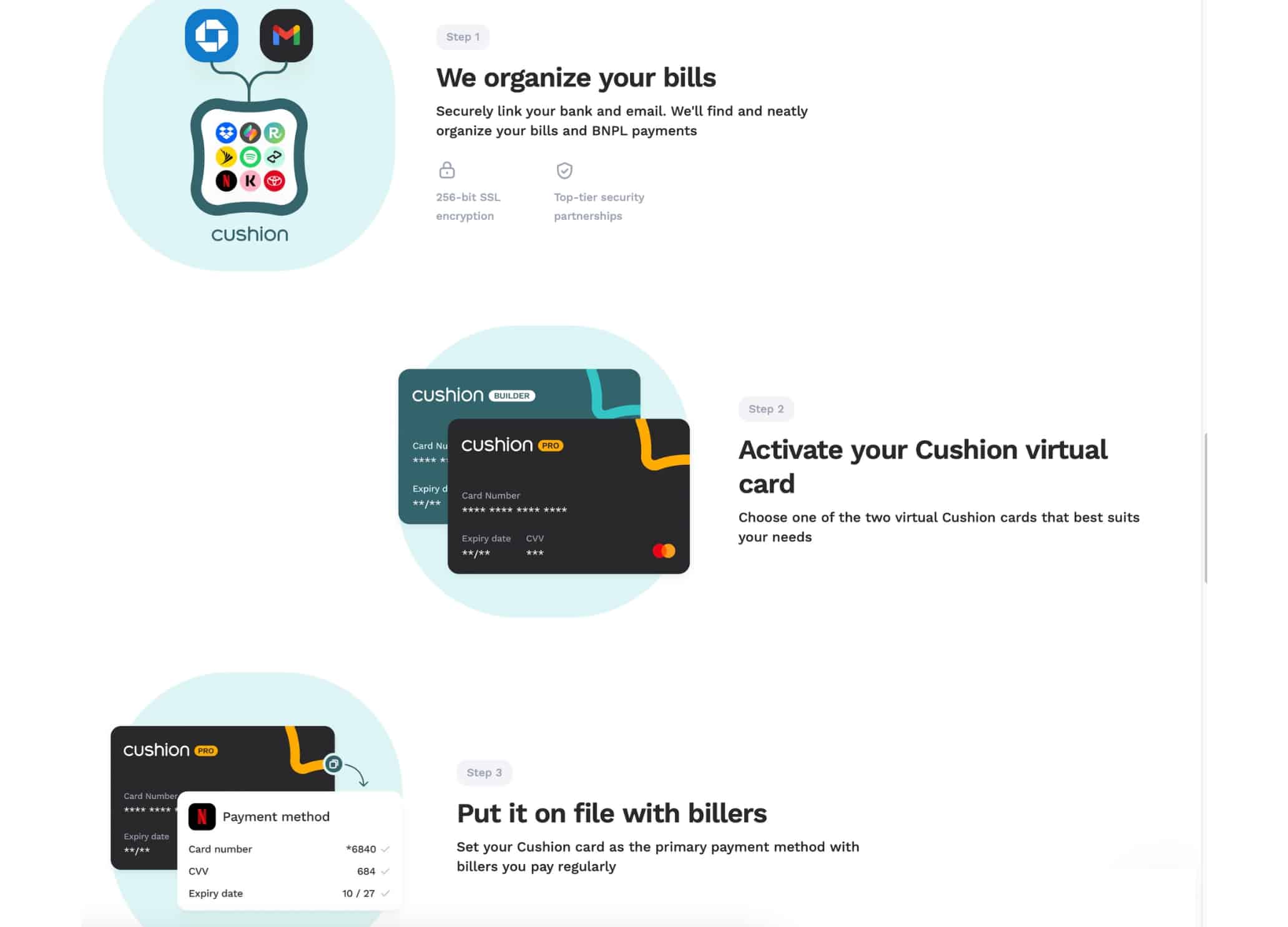

A budget reveals the flow of your finances but cannot fine-tune your spending. However, certain tools are designed to assist in this aspect. Consider Cushion, a tool that helps you manage Buy Now, Pay Later purchases (BNPL) and potentially build credit by reporting on-time bill payments. By giving you a consolidated view of your BNPL transactions, you can identify and eliminate wasteful spending.

Cushion will remind you of upcoming due dates and offers a virtual card to pay regular bills. When you use this card, your on-time payments get reported to credit bureaus, potentially improving your credit score over time.

Bill Shark is another excellent money-saving app. It will negotiate better rates with your cable, wireless phone, satellite TV and radio, internet, and home security providers. You don’t have to search around for a better deal or spend time calling those providers to get it. Bill Shark handles it for you.

You can save money on a move, shopping online, your electric bill, cleaning your house, eating out, and nearly anything else you spend money on.

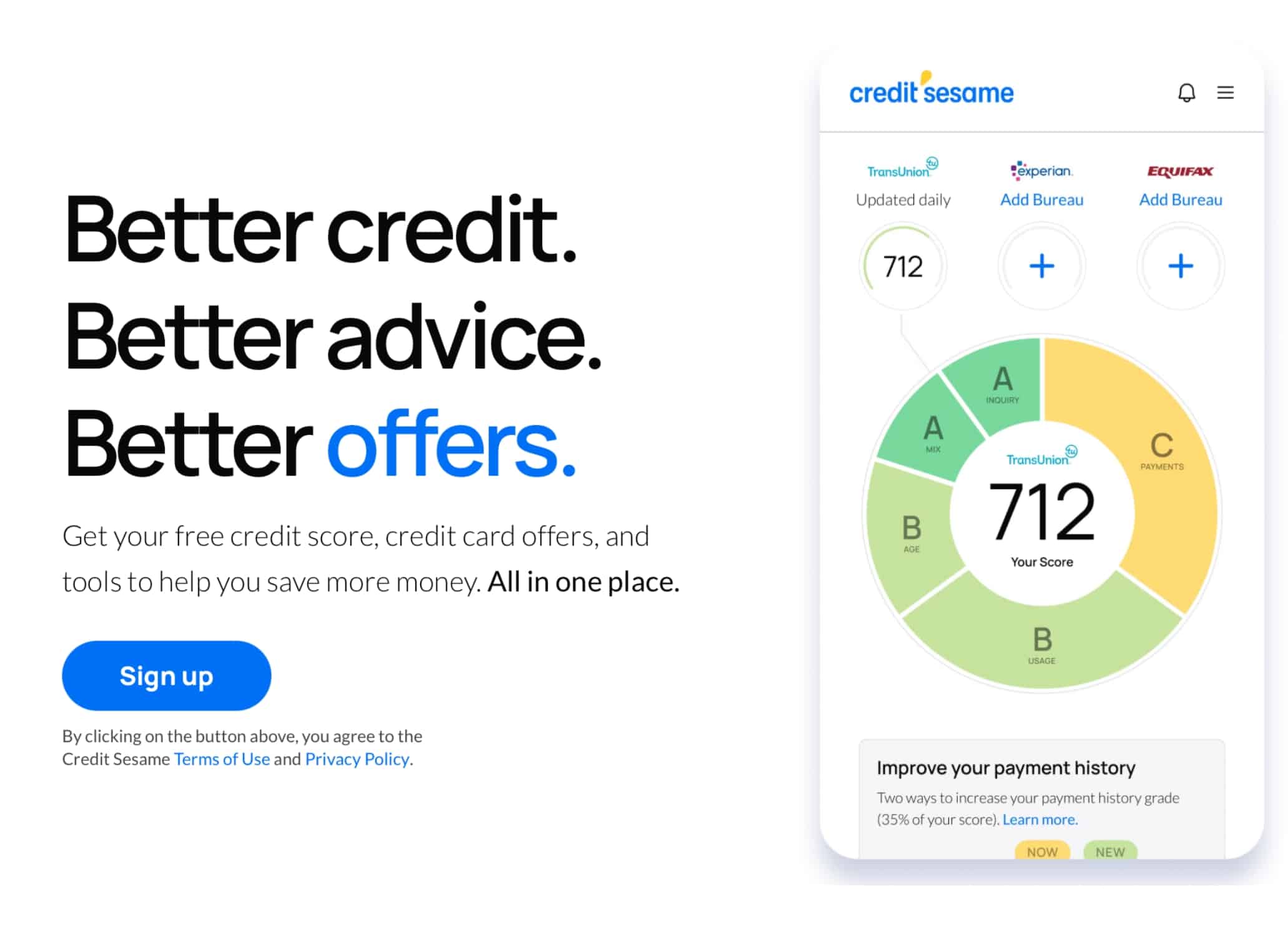

Do you know your credit score? What does your credit score have to do with saving money? A lot.

You don’t need the highest credit score possible (850 depending on which model) but if your score is 740-779, you’re likely to get good rates. If you don’t know your credit score, you can get it for free, including the factors making up that score, at Credit Sesame.

If your score is not at 760 or better, there are lots of things you can do to improve it and certain things like:

The key to becoming financially stable has less to do with how much you make than it does with how much you spend. Spend less than you make and you’re halfway there. The most significant expense for most of us is housing. The general rule of thumb is that total housing expenses (rent or mortgage payment, utilities, homeowner’s insurance, etc.) shouldn’t exceed 30% of your net income (your income after taxes). This is considered a safe and affordable level of housing expenditure.

Living within your financial means is basically about balancing your spending with what you earn. It’s like being the boss of your money, making sure you’re not splurging all your cash on impulse buys or stuff you don’t really need. It means being smart about your cash – saving up for rainy days, cutting back on less important stuff so you can afford what truly matters, and not letting credit cards trick you into spending more than you have.

It’s all about making your money work for you, not the other way around, and keeping stress at bay because you’re not constantly worried about debt.

Spending money can be enjoyable—I understand that. Whether it’s dining out, enjoying drinks, or shopping, these activities offer their own pleasures. However, it’s possible to entertain yourself and others while having a great time without breaking the bank. To help with this, consider exploring inexpensive date ideas and cost-free activities for a Saturday night.

Fiscal flexibility that’s funny, free and delivered weekly.

Debt

Not only do many Americans lack savings, but they are also in debt up to their proverbial eyeballs.

According to the most recent Fed report in Q4 2023, total household debt in the United States reached $17.5 trillion. – Federal Reserve Bank of New York

Home, auto, student loan, and credit card debt fall under the category of consumer debt. It’s important to recognize that not all debt is detrimental; indeed, some forms of debt are more burdensome than others. Achieving financial stability does not necessarily require being completely debt-free. However, minimizing debt is always advantageous. Let’s explore strategies to reduce or eliminate debt.

Prioritizing credit card debt payoff, especially for high-interest balances, is generally a good financial decision after building a basic emergency fund. However, consider your overall financial situation and explore different debt management options to find the best approach for you.

Accelerating Paying off High-Interest Credit Card Debt

Prioritize and Attack the High-Interest Debt:

Increase Your Payments:

Reduce Interest Rates:

Utilize a Debt Consolidation Loan:

Additional Tips:

A personal loan is another option. You still have debt, but if your credit score is good enough, the interest rate is lower than the interest rates on your credit cards. Upgrade offers personal loans to pay off credit card debt (or for any other use).

Ideally, none of us would have student loan debt, but millions of us do.

As of the end of 2023, there are more than 43 million borrowers who collectively owe more than $1.7 trillion in student loan debt in the U.S. alone. Student loan debt is now the second-highest consumer debt category – behind only mortgage debt – and higher than both credit cards and auto loans. The average federal student loan debt per borrower is estimated to be around $37,088.

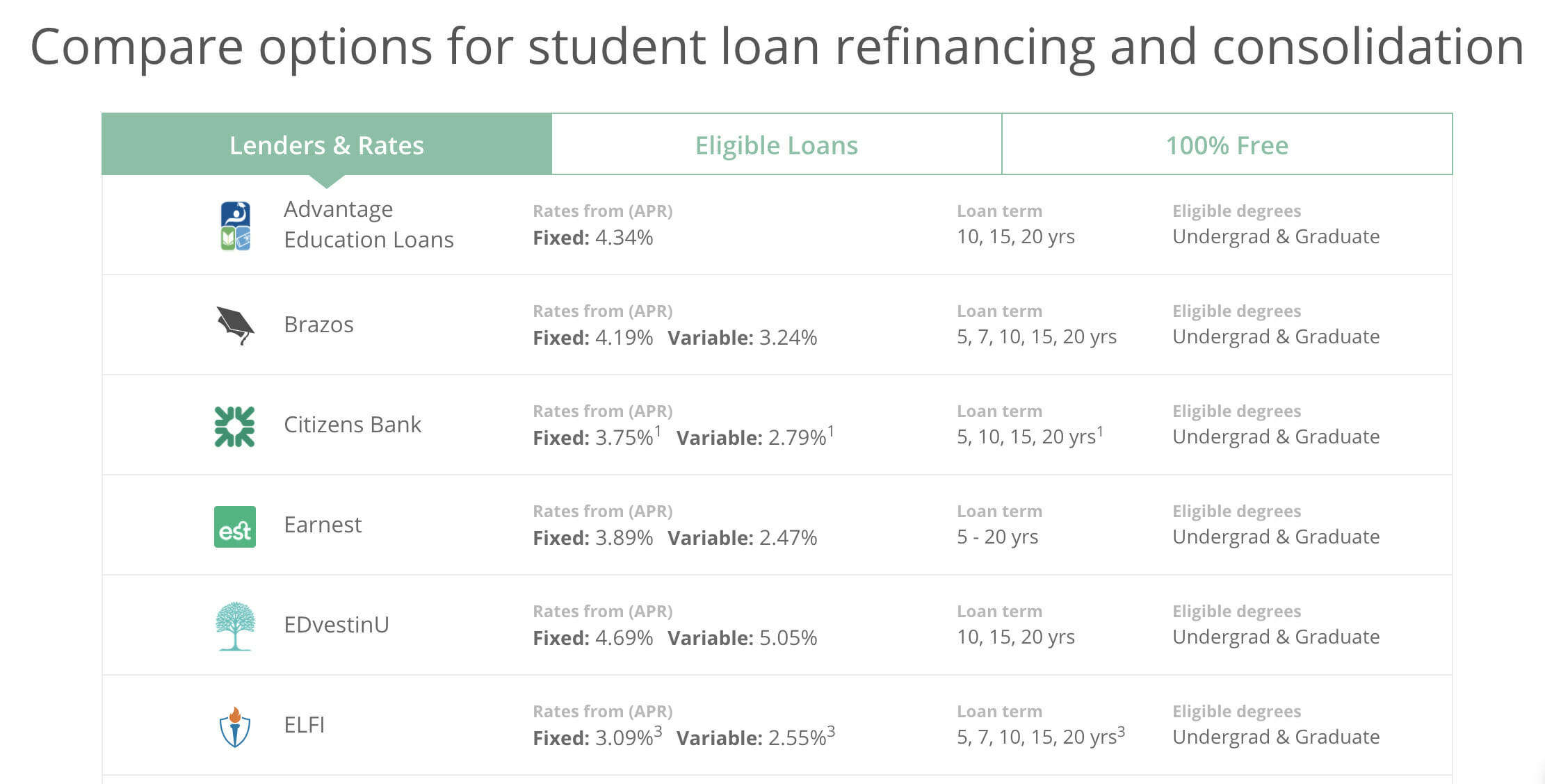

And student loan debt is not the worst kind of debt to have. The interest rates on student loans, particularly federal loans, are relatively low. If your student loans are private, the interest rate is higher, but there are ways to reduce your interest rates for both. Lowering your interest rates with a student loan refinance can save you thousands of dollars over time. You can refinance with Credible as their rates are some of the lowest available.

Credible will show you offers from up to 10 lenders so you can choose the best rate. This window shopping won’t impact your credit score. And don’t forget, you can refinance more than once. If your credit score goes up or your debt-to-income ratio improves, shop around again and see if you can get an even lower rate.

The marker of financial stability when it comes to student loans isn’t necessarily to have them all paid off. You can typically expect a higher return on long-term investments than you’re paying in interest, so you don’t want to forego investing until your loans are completely paid. You can’t make up for that lost time. Your goal should be to have a student loan payment that is manageable.

Many of us behind LMM don’t drive. We live in cities with excellent mass transit, so we don’t need cars. So cars are not something we prioritize, and our advice is to save up and pay cash for a car. But we get it that everyone does not share our perspective.

We made the executive decision NEVER to mention anything about cars again. Not even in an example, because it seems to be such a hot button issue for many people and we get all sorts of crazy, angry emails whenever we bring them up.

So our advice on car loans is to keep them manageable. You know how much car you can afford and you know when you’re trying to act like a baller by buying a crazy expensive car that you cannot afford.

Just like you shouldn’t drive more car than you can afford, you should not live in more house than you can afford. Remember, your total housing cost should not exceed a third of your net income. You should also save enough for a 20% down payment so you can avoid the expense of PMI.

And your home should not be considered a real estate investment. It isn’t. A real estate investment or any other kind of investment is something that makes you money, something a home does not do. Even if you’re mortgage-free, you’re still spending money on things like property taxes, homeowners insurance, and maintenance. A house doesn’t make you money until you sell it and sometimes not even then.

Not every decision has to be financial. There are plenty of legitimate reasons people have for wanting to buy a home to live in, but your home is not an investment or a retirement plan.

Investing

Most of us are not going to become rich from our jobs alone. For every investment banker, there are a thousand teachers, firefighters, and postal workers making low to mid-five figures. And yet there are more than a few teachers, firefighters, and postal workers who manage to retire as millionaires. How? Through investing.

Opening an investment account gives you access to the biggest money-making vehicle in the history of the world — and you don’t have to be rich to do it.

It’s investing and not a six-figure salary that makes people the millionaires next door. So if you want to be rich, but you’re afraid of the stock market, get over your fear of investing.

If you’re going to have a goal, you need to know how you’re progressing toward that goal and when you’ve reached it. How much should you have in your 401k? What is your end goal retirement number? We like the 4% rule as a way to determine your final retirement number.

The 4% rule is a benchmark that can be used to calculate how much money to withdraw from your retirement accounts every year for at least thirty years without depleting those accounts and outliving your money.

Here’s how the 4% rule works. You can withdraw 4% of your retirement money each year for all of your expenses. If you have $500,000 saved, you can withdraw and spend $20,000. But you need to account for inflation too, so you increase the amount of that first withdrawal ($20,000) to reflect the impact inflation has on your buying power.

If annual inflation is 2%, the second year of retirement, you take out $20,400. The next year, $20,800, and so on. You continue these 4% withdrawals and the extra amounts to preserve your buying power no matter what the market is doing or how your portfolio is performing. Adding in the amounts to account for inflation will ensure that you have the same purchasing power in your first year of retirement as your last.

There are plenty of other rules of thumb you can use to get your number, but we like the 4% rule because it’s easy to understand.

Investing and retirement investing are two different things. Retirement accounts like 401ks and IRAs are tax-advantaged. Those advantages are essential for retirement savings. The two most expensive things in life are interest and taxes. We showed you how to minimize interest; investing in retirement accounts is how you (legally) reduce taxes.

There are also penalties for withdrawing money early from a retirement account. That sounds like a punishment, but it’s a good thing. Retirement saving is long-term. That money needs decades to grow so you shouldn’t use a retirement account as a piggy bank. That’s what your emergency fund is for.

Your priority is to contribute enough to your 401k to receive matching funds from your employer. This is free money and the reason we suggest you do it even if you have credit card debt. Not all 401ks are great. Sometimes the fees are high, and sometimes the investment options aren’t great. Empower can take a look and show you how healthy your 401k is. Even if it’s not great, contribute to the match. If it is good, max it out.

If your 401k isn’t great or you max it out, you can move on to an IRA. We’ve covered the differences between a Roth and a Traditional. You’ll have much more flexibility with an IRA than your employer’s 401k.

When it comes to short-term investing, it’s essential to recognize that not all of your funds should be tied up in retirement accounts. Financial goals vary in terms of their timelines, with some being more short or medium-term. Short-term goals typically have a timeline of five years or less, while medium-term goals extend from six to ten years. For example, a short-term goal might be saving for a wedding, whereas a medium-term goal could involve accumulating funds for a

Unlike retirement savings, which have decades to weather the fluctuations of the stock market, the money allocated for these shorter-term objectives doesn’t have that luxury. However, it’s also too significant an amount to leave sitting in a high-yield savings account, where it earns interest. Finding a balance between security and growth is key to effectively managing these investments.

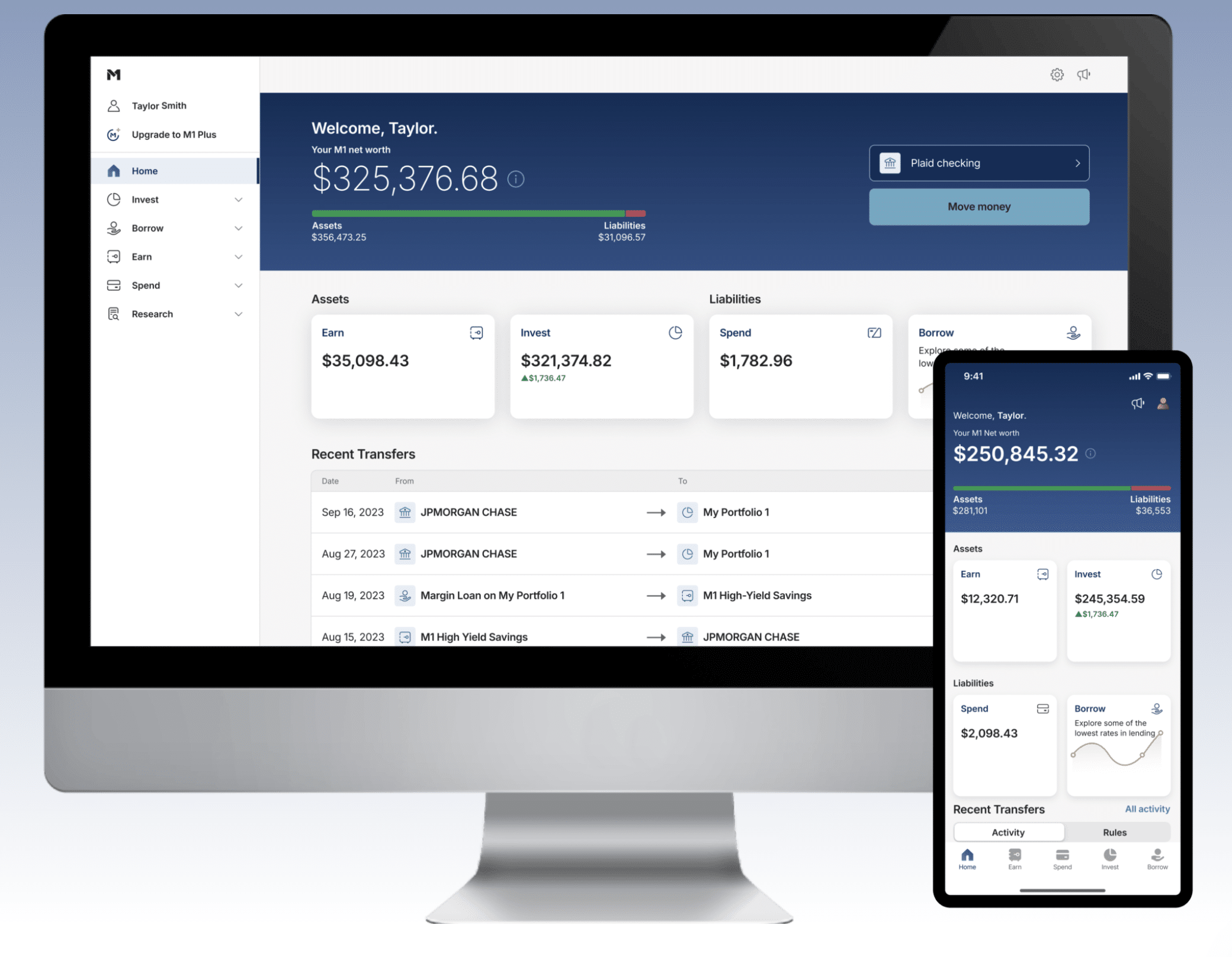

M1 Finance is our favorite

We also love Vanguard for both everyday and long-term investing.

Using a turnkey rental property strategy lets you invest from a distance. Andrew has documented his experiences with rental properties and created a course, Rental Properties for Passive Investors, which details the entire process.

Our proven, data-driven approach to building a portfolio of income-producing rental properties that perform in the long-term.

If you can’t afford or don’t want to own

Keep in mind that eREITs can be hard to sell quickly, and changes in the market can impact the value of your real estate investments.

Making (more) Money

At some point, you’ve cut your spending as much as possible, and the next step is finding ways to increase your income. Alternatively, if cutting costs isn’t your strong suit, boosting your earnings becomes essential.

Employers often try to intimidate employees into staying quiet about their salaries as a tactic to keep wages low. However, it’s actually illegal to fire employees for discussing their pay.

That said, a lot of people are uncomfortable talking about their salary. Lucky for us, we can find this information on sites like Glassdoor, PayScale, and Salary Expert. Use these sites to find out what people in similar jobs in similar areas, in similar companies to yours are making. Knowing what you should be earning is the first step to making more.

Armed with this information, you’re going to ask for a raise. But you have to justify it. Why do you deserve a raise? If you’re offered a raise, negotiate for a better one. If you’re turned down, polish up your resume and start looking elsewhere.

I know, everyone hates the term side hustle. Fine! Propose a better one, and I’ll start using it. The point is, that everyone should have at least one side hustle. Even making a little extra money each month can go a long way to helping you reach financial stability.

It can help you get out of debt faster, grow your emergency fund, or accelerate your investing goals. And if you suffer a job loss, that extra money is better than nothing. Ideally, one of your side hustles brings in passive income.

We all only have so many hours in the day, and we don’t want to spend all of them making money. A passive income side hustle brings in cash without much or any effort from you (Eventually. Sometimes it takes some effort to get the hustle up and running).

Best-selling author Chris Guillebeau presents a full-color idea book featuring 100 stories of regular people launching successful side businesses that almost anyone can do.

Social

Money is often a taboo topic, but it hangs over many social interactions and relationships.

Some people are so poor all they have is money.

Tweet ThisMoney shouldn’t ruin relationships, but it also shouldn’t be a taboo topic. Openly discussing finances is not only healthy for your relationships but also beneficial for your financial well-being.

Who you choose to allow into your life has a tremendous impact on your behavior.

Renowned businessman Jim Rohn once said, “You’re the average of the five people you spend most of your time with.” Bottom line: The people around you matter. You need people — whether it’s co-founders, mentors, family or friends — who will challenge you and make you better, thereby raising your average or helping you maintain a high one.

Make sure some of the people in your life can be considered financial friends. People who have a similar money mindset to yours and who have goals similar to yours. Sure, those slacker friends from college are fun, but you’re an adult now, and you need to surround yourself with people who are financially stable and responsible.

Money can be one of the most contentious subjects in a relationship. There is a lot of room for compromise, but when it comes down to brass tacks, you and your partner have to agree about most money issues.

Get financially naked as soon as it seems you’re heading down the path of joining your lives. It can be tough when there is financial inequality in a relationship, and some men will struggle when she makes more. These things can lead to financial infidelity, which can be as devastating as romantic infidelity.

If you and your partner can’t talk openly about money and come to an agreement about your financial future, you’re heading for a split, and it can get ugly. Your partner must be your best financial friend.

I’m not going to tell you not to spend money on having a good time—I’m all for it. There’s a big difference between buying things and buying a good time, even though some people mix them up.

Spending on experiences makes us happier than spending on material things.

According to research conducted by the McCombs School of Business at The University of Texas, spending money on experiential purchases rather than material ones has a greater impact on people’s happiness. Individuals who spend money on experiences tend to have greater in-the-moment happiness compared to those who focus on material items.

So, go ahead and take that vacation, enjoy that concert, and savor the wine! But skip the temptation to buy a new car, upgrade to a bigger house, or splurge on the latest flat-screen TV.

This is marked as high urgency because everyone reading this works hard and deserves to enjoy the money they’ve earned. So, think about a few things that would make you happy, and go do them—preferably with a friend. Making memories with someone close is why spending on experiences brings more happiness than buying stuff.

How Did You Score?

How many of the 19 markers of financial stability can you check off? If you can’t tick them all, don’t stress—I do this for a living, and it’s normal not to have everything covered. I wrote this to help you get on track toward financial stability, not to make you feel bad.

But seriously, tackle the high-urgency ones as soon as you finish reading this.